Agree with your point…They are offering 3 in 1 Trading a/c with zerodha but yet to have ASBA/UPI facility for IPO…

1 Like

7 Likes

Retro tax case won by vodafone.

Positive?

2 Likes

This is vodafone and not VI

2 Likes

I think the next 4 quarters will be in deep red. Am I missing something?

Covid will be causing a lot of stress right?

10% GNPAs as base case

My first Q & A session that too i completed the entire 49 minutes in one go, This guy seems to be very truthful, So my question is are all the CEO’s Speak in this manner or this guys really is good. I have 10% of my Folio in this stock, I feel i need to increase that after listening to him.

3 Likes

Please listen and read to him and management for last 3 years and decide. Nothing against management, they must be doing great job but constantly saying good and truthful things but results not reflecting. I have said before that they were aggressive in commentry precovid when I used to listen to them. Realised that conservatism in commentry, caution is better than optimism in finance Sold out at oppotune time, converted to HDFC Bank and do not listen anymore. Are they still as optimistic as ever before?

Disc. Not a buy/sell recommendation, only thoughts which can be completely wrong.

4 Likes

Did you see the video?

With all due respect, this seems like a case of level 1 investigation versus level 2 investigation. At a first glance, there is indeed a lack of PAT and EPS. At a first glance, “every quarter there is something or the other”.

When one takes the pains to do the deep dive, to do the level 2 investigation, to go through the investor presentation, AR and the AGM, one finds out that the fundamentals of the bank are indeed improving. The retail CASA + TD is growing rapidly despite the pandemic (some large banks CASA declined in the pandemic, if i recall this correctly, but please don’t quote me on this.). This is very important for a large bank since the alternative is commercial deposits which are very flaky and unreliable. Even if they did 0 loan growth and simply keep growing CASA, their profitability and NIMs will keep improving. Erstwhile IDFC and Capital first both utilized commercial sources of Deposits at 8.5-9%. Substituting with 7% CASA will itself improve NIM by 1-1.5% over the long run. Some of that has played out, more will play out.

These interpretations are subjective. Asking for others’ opinions only displays their biases. Every investor must individually investigate the facts and form their own opinion (reducing for biases as much as possible). If i could pick 1 statement about this bank for disagreeing with it 10,000%, this would be the only statement I would choose. The management commentary is extremely conservative and so are their actions. Read through the AR. They guided for 30% CASA in 5 years since FY18. They have achieved it in FY20. Is this conservative commentary and actions being ahead of the expectations, or aggressive commentary? I would humbly suggest to you to also consider whether this might be a case of confirmation bias in your case. When one has switched to HDFC Bank, one might find it difficult to treat information/facts about IDFCF in an unbiased way (this is true for every human, not just you).

Management has been as upfront, honest and fiscally prudent as I have ever seen. They have been very conservative and proactive in creating provisions even for standard accounts like Vodafone Idea on a suo motu cognisance basis. In fact when certain clients threatened/appealed the ceo that classifying them as NPA would be bad for the bank, the CEO shot back saying “you take care of your problems and I’ll take care of the bank’s.” He also reassured the investors that the bank will never bow to a customer when it comes to classifying an account as an NPA.

Just to drive home the fact that I myself do not suffer from confirmation bias in this investment and to balance my post a little bit, please also find the list of genuine risks that are part of this investment:

- The bank’s model is very different than that of HDFC or any large bank. Many of their first time customers have not even filed an IT return and forget about cibil scores. The bank is path breaking in that it creates a new market by providing cash flow based loans to small entrepreneurs for small things like buying a buffalo or a goat. Cash flow based lending models will come under some stress due to covid crisis since cash flows are exactly what is being attacked by a lack of consumer demand for many products. Many SMEs might be forced to shut shop if there are prolonged subsequent lockdowns. The mitigation from bank side is to provide provisions aggressively right now and in subsequent quarters and also raising “Insurance capital”. Another mitigation would be to restructure the loans as per the reduced cash flows of the businesses. For example, bank can provide an extended moratorium of a year if they want to. I believe they can safely take up a hit of 4-5% of book becoming NPA and survive the covid crisis.

- Let us assume that the distribution of loans provided by the bank to various MSMEs across various industries is X(say 30% to agri, 30% to hospitality, 40% to services based; this is only an illustrative example not real numbers). Post-covid world might result in secular changes in customer preferences. As an example, a lot of things are shifting from real world to digital. Most offices realized their sales costs are much lower if the sales happen virtually. Any MSMEs which might have supported sales related travel, will secularly lose business and might go bankrupt. The bank must continue to understand the economy and adapt its loan disbursal strategies in accordance with the changes in the economy. It is a risk whether the bank can actually execute on this since we have no visibility into whether and how they track these secular sectoral headwinds and tailwinds.

- The legacy IDFC book is infra heavy and will continue to face headwinds. We should expect high NPAs from this book until the bank is successfully able to take it down to 0 (an investor can track over quarters whether the bank is actually doing so or not).

Conclusion: There are good reasons for not investing in the bank, but i believe those reasons and risks are the flipside of the strengths of the bank. The very thing which provides this bank a secular runway to grow loan book 10x or 20x in next 10-20 years, can become a problem in cash flow crises like corona or if the bank is unable to keep up with secular changes in the economy. I do not think a good reason for not investing in the bank is the management being aggressive in commentary or “results not reflecting”. In fact, the results are reflecting, imo.

Disc: Invested, 10% of PF. Will wait for the more clarity to emerge regarding the full impact of covid crisis to playout (Q4FY21 or Q1FY22) before increasing allocation (of course i reserve the right to sell off the position at any point without notice if facts emerge counter to my investment thesis or if i find a better opportunity).

14 Likes

Thanks for the long post and aggressive feedback. Honestly, I do not have time and intention to read through details and respond. I agree I am biased which I clearly stated in earlier posts and also acknowledge I can be completely wrong. My only intention of recent post was to the gentlemen who invest based on management truthfullness, goodness etc. as they according to me do not matter much, specially in a lending business and also specially as all these intangibles are subjective. So we as investors must be as aggressive as you with facts and listen to any such videos and commentries with a pinch of salt. As always, I can be completely wrong in my assessments… thanks

4 Likes

I agree with this post, Sahil. To add to this I believe another major risk for the bank is unsecured loan. The bank is partnering with a lot of fintechs which are granting unsecured personal loans. The example that you mentioned about cows and buffaloes too consists of unsecured loan. God forbid, if we face another major economic/health crisis, this unsecured loan book might prove to be a huge problem.

3 Likes

Borrowing requirements of small businesses are going to increase as unlocking progresses. Even West Bengal and Maharashtra have been forced to open up from first week of October. If businessmen start defaulting or delaying payments then they surely can not expect further financing.

1 Like

It is for a fact that IDFC First is a high risk high reward bet.

There are many optimistic keywords on one side like,

Increasing Core deposits, Retail assets: wholesale ratio, expanding NIMs, growing at 20+% for a very long term, P/B re-rating, Niche fintech tieups like CRED,NIYO,ONE card,Flipkart paylater, Amazon paylater etc , controlled GNPA<2 , nearing the end of cleaning cycle, ending tenure of high cost NCDs by 2021 etc etc

On other side, my real concern are…

- Yearly credit cost of 2-3% which is super super HUGE considering ROA is hardly 1.5% at peak ( this is way before system being in stress, Before ECL, Merger & during 120 day provisioning times)

It’s ok to target high risk segments to make 10% NIMs with high credit cost… but, if reward comes at 1.5% why don’t i simply go and but some HDFC which will grow at 20% with high P/B dilution.

-

Rich getting richer and poor getting poorer phenomenon - I somehow see massive change in organised retail… 3-4 years back our T2 town flourished with lots of local retailers established since 20-25 years… now folks like Reliance got into play and doing 4cr monthly runrate within 1 years… that’s massive 30lak/month EBITDA which would’ve been earned by people living within my T2 Economy. Not just Reliance retail, there is reliance trends, more some organised Chai companies & many more sucking cash from these small economies and taking it back to Mumbai.

This way though with inflation, growing capex & productivity in these T1+ economies small entrepreneurs may not go bankrupt but, their cashflows will be severely stressed/not grow much… making big banks serving top tier stronger and Small banks serving only T2+ not so richer. -

Internet addiction, lower attention spans, rising risk in millennial lending & emerging of smartphone addict babies phenomenon…

I don’t want to eloborate on this, read few reports earlier on how credit risk in increasing every decade… it is one major concern for me in banking sector… if banks don’t properly price the credit it’ll be pretty painful for them in long run…

This is specifically relevant for IDFC first… because, these folks try new to credit lending a lot. Though they find some gold mines in niche pockets most can be painful. -

Increasing AUM & Housing Finance book… This will naturally contain the NIMs as spread and risk is relatively less in this segment… but, my main concern is… folks like HDFC,Kotak are aggressively tapping IDFC first markets… now, People like IDFC will find a new to credit borrower lend to him at 10%-12% now our vultures like Axis, HDFC, Icici,Kotak with their low cost deposits might …will wait for 18-36 MOB seasoning and attract the customer for Balance transfer at lower interest rates with a topup… this will significantly decrease lifetime value and disrupt the economics of risk reward. ( HL balance transfer will not attract any foreclosurecharges) - I have seen this penmenon through telecalling marketing and even through local branches of these big banks.

-

New Co-lending, Securitisation & PTC weapons emerging in last 2 years…

These three will help banks with good low cost liability to pass on credit to niche pockets of customers which are catered by NBFCs… NBFCs in turn instead of worrying about ALMs, CARs can focus more on acquisitions and collections.

So, basically new age lending apps & established lenders can forge partnership with big banks and can make cool 20+% ROEs for a very long time - this will make big banks equally competitive in this segement.

We have dozens of examples in private space as well as listed (eg: moneyview, Edelweiss fin, Indostar,paisalo etc) -

Not building Proper banking franchise rather just building only the lending equation. Retail Banking is basically a business of acquiring granular retail customers, looking at their financial lives in and out… such connect with these customers if leveraged well, can have HUGE cross sell potential…

Look at Kotak , subsidiaries itself are valued at >1lakcr

ICICI whenever they need growth capital/cover losses they’ll do OFS in some subsidiary and boost networth, look at HDFC Bank… their NBFC subsidiary itself which is valued at 90kcr is around 70% of their capital base…take SBI their card business share itself is worth 35kcr for them, it’s Amost 20% of their market cap.

So, building allied business is massively over looked by the management… their can simply put aside some 50-100cr and let the show run rather than 10 years down the line realising they should build allied businesses to grow or to boost capital base… transactional banking, payments, wallet etc are huge float businesses which are overlooked.

Focus story is overrated, businesses are built by prudent managers taking ownerships and achieving their milestones and not just by 3-4 management folks running the show. -

Concerns about the great valuation re-rating that might never happen.

Honestly Capital First didn’t trade at more than 2X P/B sustainably for long… it traded in that range only between 2013-2017 where Finance companies are valued based on multiples.of future equity dilutions and even DHFLs of the world traded at 2X book… by 2018 when stress started our Capital first hid behind the IDFC Bank mask…

On other hand we have banks like Federal & Karnataka Bank(not apple to apple comparison) which are trading below 1.5 book for a very very long time… So, when I see vaidyanathan guiding for 13% Roe and 1.5% ROA …I feel there might be good chance that this franchise will trade at below 2× book even at most of the time I’m bull run.

Valuation not getting re-rated will have cascading effects on dilution & value creation.

Would be great if some of my fellow investors give points on my concern areas.

Also, one more short term concern & opportunity point…

Dec & March numbers will give % restructured assets … roughly 50% of that number can be removed from capital base to arrive at realistic P/B … That can either put the stock in consolidation mode for some time if numbers are good or will get us a good DIP if % numbers are bad… should evaluation retail segement credit costs across these stress periods to take a long term call.

Disclosure: Not a shareholder yet. Have considerably good # of Futures positions on rollover mode, planning to accumulate more. waiting to become a shareholder next year.

13 Likes

HI manikya Saiteja,

Just adding my 2 cents.

These are not keywords. These are the reality of the business. You could claim you do not trust the management and say that they’re lying. That is definitely a possibility. But if we trust the management and the numbers they put out in AR, Investor presentation, AGM, then these are more than keywords and hypotheticals. This is real change which is happening on the ground.

Apologies, but where did you get the 2-3% credit costs number from? The bank has always guided for GNPA < 2% and NNPA < 1% and also been able to meet the guidance until now, meaning credit costs of ~1% which is inline with most large banks. The ROA of 1.5% is not peak ROA but the ROA that the bank will have after the infra and wholesale portion of the book has been cleansed. In no way is this an upper bound on the ROA for the bank. In a falling interest rate environment, even a 1% reduction in FD rates will mostly leave the bank with sticky CASA and higher ROAs in medium term.

Drawing broad macro conclusions from anecdotal evidence suffers from the generalization error problem. You cannot create any performant model with 1 data point (or 10, or 100). Reliance retail is not trying to put the kirana store out of business, it is partnering with them. “Grocery sales of Reliance Industries is estimated to be over $4 billion and the firm has been working on a Kirana-driven delivery model under its new commerce strategy. This means on-boarding Kirana stores and digitising them via merchant POS (point of sale) machines” from here. I think it is dangerous to fall for the narratives they flash on CNBC TV18 and ET Now screens every day about “Big getting bigger” and so forth. The truth is, most efficient businesses win out in the long run. Whether they are big, or small. The MSMEs also have very fierce government protections and I would take any talk about a trend against MSMEs with a big spoon of salt.

Being able to lend to the unbanked and underbanked. That is their entire business model. Whether they will be successful or not, only time will tell. My 2 cents are that it is generally the big companies which are ok defaulting on loans, not the small entrepreneur. The small entrepreneur is hungry for growth. The small entrepreneur knows their strengths and their weaknesses. Credit risk management is the bread and butter for any bank. This is certainly a risk. The eventual NPAs which come out of covid crisis will definitely be a litmus test for the bank. If these are low (for some subjective definition of low), this will only be further proof of their good credit risk management skills.

Not sure what internet addiction has to do with this thread. If anything, IDFCF by tying up with fintech start-ups is making good inroads into millenial credit seekers markets.

I am sure the bank is aware about this too, and would not want to grow housing finance Assets too aggressively.

This has actually been covered a bit in the thread a few posts ago. Request you to please read. They bank to or cater to different segments. Talking about hypotheticals and anecdotals is all well and good, but do we have any real facts and numbers for how and where HDFC and Kotak is going after IDFC’s key client base?

By this logic, there should be no space in India for NBFCs at all. Companies like Bajaj Finance should not even exist. Everything can be done by HDFC bank. Reality is not so simple, unfortunately. HDFC bank is a giant. Giants are slow and difficult to change. There is a great video on Youtube (that im not able to find right now) where aditya puri asks a Two-wheeler dealer why they do not tie up with HDFC bank for loan disbursals and why they prefer Bajaj finance. The dealer says its the tech. BF is able to process loan application with 2-3 data points within minutes. HDFC bank requires a form to be filled up and processes loan application in 1-2 weeks. The processes matter. The technology matters. Video KYC matters.

Can we reason about this from first principles basis? How will the bank make 20% ROE? When the profits are shared between the NBFC and the Bank.

Also, isn’t it better for IDFC to act as both the bank and the NBFC thereby enjoying higher ROE than a bank which outsources the actual lending to an NBFC? I’m a bit confused about your reasoning here. Lastly, if such tie ups are actually profitable (for the bank), then wouldn’t the same option also be available to IDFC First?

Is this the listed company? if so, they are severely loss making: Edelweiss Financial Services Ltd financial results and price chart - Screener I don’t know if I would even reference edelweiss fin in a discussion about 20% ROE ![]()

All the good things will happen. As investors, one of the most important virtue we need to abide by is patience ![]() Right now the management is focussing on the core banking which requires focus. They are launching credit cards soon. They could potentially do a reverse merger with IDFC which would give them exposure to AMC. They have a tie up with Zerodha for Demat accounts. Everything happens in due course of time. How can you build a large building, if the foundation is not strong? The foundation of a banking company is always the lending business.

Right now the management is focussing on the core banking which requires focus. They are launching credit cards soon. They could potentially do a reverse merger with IDFC which would give them exposure to AMC. They have a tie up with Zerodha for Demat accounts. Everything happens in due course of time. How can you build a large building, if the foundation is not strong? The foundation of a banking company is always the lending business.

This is a inverted way to think about things. If the bank can sustainably grow earnings, rerating is inevitable. If it cannot, then i do not even want to invest in the bank (the valuation re-rating is a cherry on the cake, not the cake!).

Valuations are always secondary to growth and asset quality for lending institutions. Once the growth picks up, so do the valuations. That is what makes a big compounder. As investors we need to focus on the fundamentals (NPAs, growth, NIMs). The valuations follow as a consequence, or corollary.

15 Likes

Thanks Sahil for such a detailed response, I do agree with your views which is backed by numbers. The narrative about going digital seems very fancy , we could refer to the video interview done by VV with a taxi driver in Mumbai who was paying a whopping 120% https://youtu.be/fvgJkOcbQwM, most of us are not aware of the reality, we are just discounting a man who has been in the retail industry for 30 years

2 Likes

Hi Sahil,

Thank you for sharing your opinion on my points of concern. I’d like to re-iterate I am holding a good chunk of my financial securities portfolio in IDFC First & I too am hoping for 10X.

Coming to your reply, Most of the opinions that you have shared are the first cut impression after observing management commentary for long- Even I know it & have that bias but, most of my concerns are in the 2nd layer when you have a more holistic picture on entire credit spectrum rather than a single bank. let me explain on your comments.

I am also looking at the same data as my fellow investors & see that stuff is getting better- wouldn’t dispute this.

- GNPA and NNPA are final numbers, you are missing out on recoveries. You can always provision more and move bad assets from books and keep a lean NPA profile[You can see this in (provision/AUM) % - don’t track this for after the merger coz management says they are one-time. see the number for few years pre-merger].

- Drop in repo will eventually passed on to depositors & borrowers with some lag- so, wouldn’t look much into this as a return expansion driver.

Definitely not a TV channel narrative- I hope you understood my 4cr run rate evidence in a T2 town. You are right on scale part. apart from Agri,in almost all the businesses i see efficiency is achieved in scale. also, yes to some extent we have different procurement policies,cap subsidies,Mudra and other initiatives for SMEs - Not sure how big & profitable can this 17lakcr market will become.

Not to mention JIOs kirnana network will be financed by my Piramal, over night PEL will have access to huge proprietary channel- unrelated here.

Haha this is more of a Macro opinion on credit & risk, I somehow think these psychological impacts on humans will have bearing on some risky segments. Hope with tech, these acquisition & monitoring scorecards inside financial institutions will be churned more often & price the risk properly.

-

HL is mandatory if you want to grow your AUM. Products like GL, TW,PL will run down much faster and you cannot show AUM growth in this.

eg: Muthoot for managing an AUM of 35k cr used to disburse 70kcr every year. If folks like HDFC disburse 70kcr in HL/LAP every years they will become what they are today within 3-4 years . Infact i remember seeing 40+% of bajaj fin AUM in mortgage. so, when you are talking in lakhs of cr AUMs, the presence of mortgage portfolio is inevitable. Not all banks can be like Bandhan Bank who managed to disburse low tenure micro-credit at scale as well as grow in double digits.

. Infact i remember seeing 40+% of bajaj fin AUM in mortgage. so, when you are talking in lakhs of cr AUMs, the presence of mortgage portfolio is inevitable. Not all banks can be like Bandhan Bank who managed to disburse low tenure micro-credit at scale as well as grow in double digits.

In fact i remember Vaidyanathan saying they’ll pursue HL as an important segment going forward.

You missed my main point here, I am taking ONLY about Balance transfers. Acquisition is a skill, retention is more of a commodity.

Once if you are already underwritten and performing well, Banks will undercut you. I remember many prominent NBFCs having trouble with this. they do all sorts of things to control Balance transfers. anyways, if me as a consumer paying 20k Housing emi and if someone comes to me and offers me to convert and pay only 18-19k EMI- I’d do it next min.

Probably the telemarketing and on ground folks I’ve met across different states made me think like this.

I’ll explain this in simple words, after 2018 end i.e after ILFS crisis. entire NBFC sector was struggling with raising funds. then all these wonderful tools like Securitisation(Passthrough certificates, Direct assignments) ,Co-lending & Onward lending came into light.

a) Passthrough certificates(PTCs): are ones where NBFC lend out and later pack it in a certificate and sell to banks and take the cash from them. NBFCs will still continue to take the credit risk but most cash is taken back from the bank while selling the loan portfolio.

- This PTCs have credit loss absorption provisions which will make NBFCs to keep ECL+ extra cash in terms of deposit as a pledge to banks…this is blocking capital for NBFCs so then came Direct assignments.

b) direct assignment, NBFCs sell out the loans they have given to banks, but this time with entire credit risk. also, in INDAS you have provision to book upfront income arising from such sale.

so, NBFC will lend out at 15% yield, sell it out at say 12% and book the 3% yield right way. this is very very high ROE model but, NBFCs will have low lifetime value of the customer so, in order to sustain such high ROEs they should continuously source more loans.

c) Colending- model where NBFC and Bank will tieup to underwrite some segment. Bank will act as source of capital NBFC will act as on-ground guy. These two folks together will contribute some capital 80-20 types and arrive at some blended interest rates of some 9% for bank -15% for NBFC types. This way NBFCs will have higher yields than normal and customers will get lesser interest loans.- NBFC will enjoy super high ROE at the expense of loan book growth.

-This has issues with both Banks & NBFCs agreeing on underwriting standards so, integrations itself took till 2019 end and 2020 for many of these finance companies.

d) Onward lending: Our PSU banks are more into this, Banks will give credit to NBFC mandating them to give the credit only to some specific segment. Banks can consider the PSL assets sourced from this category for their PSL targets. so, win win for banks and NBFCs - NBFC capital base is utilized here but still, this is enabling Banks to pass on credit to NBFCs which target Priority sectors.

Now, Such tie-ups are profitable for banks with low cost of deposits i.e at 5% types and good liability franchise. their lending rates to NBFCs are 9-12% will still cover the risk and give adjusted returns. So, i am saying cheap Banking credit is indirectly flowing into IDFC First target markets though other NBFC competitors.

you are referring to lagging indicators, Bad credit decisions will haunt your book for years. I am referring to a pretty new phenomenon and industry-wide structural changes with learnings from past. you will see these in terms of numbers during this decade once cleaning is done. else, you can read between the lines monitor credit changes over past 3-4 years across entire spectrum you’ll get good picture.

wouldn’t comment on this- this is the same as what management guided. I like this, but as a shareholder who wants to see this institution as a 2lakcr company- I feel you need more pillars to stand solid.

Credit card will support the ROEs- totally agree with your view.

Fee income from distribution is good, but you are missing out on equity value.

eg: we don’t get rich from P&L, we get rich from equity. Imagine SBI, being a super cool distribution franchise- rather than building their own insurance business if they have relied on some ICICI Prudential they would have made cool 10-20k cr / year on fee income but would have missed out on building an additional 80kcr equity worth of business.

Please checkout the DCB bank, Federal bank,Karnataka Bank [Not a apple to apple comparison] - but there can be a slight chance for this if the bank doesn’t show stability in return ratios.

That said, have been seeing too many people repeating the same narrative that comes from management every quarter- so added points which i feel might be some risks.

My concerns are probably on a structural level.

Also, adding a couple of points from my optimistic perspective[Apart from the ones which are widely circulated around]

-

There are 12-13 banks in top 100 for both China and USA. For India, it’s hardly 1[in terms of market cap]. I think lot of these midsized banks will have a good growth trajectory and rerating with time.

Banks are really cool businesses, just the credit policies, procedures & brand value is proprietary- if it’s proper you can consistently scale from 1Mill$ to 100bill$ business. -

With growing credit and expected 2,00,00,000 crs outstanding credit by probably 2025-2026. even a minor expansion in market share puts IDFC first at 3 lak cr size &

banks like IDFC can consistently take market share from PSUs which stands at 65% now. -

IDFC First has a cult like brand following, It has an emotional connect with 9lak strong retail shareholder and many many more borrowers. Since this is a business of trust, it has good chances of attracting huge CASA, TDs. Not to mention, many retail shareholders in IDFC First might be working with corporates who might even approach IDFC First to build relationships with their organizations- Such is the brand following and trust on IDFC.

- Infact even i though of leasing out my commercial property to IDFC in my T2 area coz i believe their services are needed in our place & the brand acquaintance as a shareholder.

- In one instance, evaluating credit partner for a leading fintech company and IDFC first was the first priority on my mind.

- Even seen this phenomenon across other people in social media.

-

CRED experience: Had a 850 credit score- got a credit line from IDFC first without a single doc. charging 14% interest without any prepayment. tried to check the experience- simply awesome. I can get unsecured credit at 10.5% in the market[by going though all that documentation], chose to take IDFC first by paying 1.5% disbursement charges & at 14% interest - because of ease of use. [BDW cred has 3mill high worthy customers-imagine the book size]

not to mention, if cred is coming up with their own credit card top 1% worthy people in India- imagine who is the preferred partner. -

out of 9Lak cult shareholder base even if 4 lak move to IDFC cred cards, they’ll have 1% credit card market share- I am moving to ONE Card anyway.

-

Had a conversation with on-ground staff while opening an account with IDFC F- amazed to find out that even KYC staff have such a deep understanding about their strategy in terms of products, Expansion & Liabilities.

7.Banking as a service model: I like the way they built this model, Fintech lender as a segment is outdated. we have fintech engrained in our day to day use. be it credit for your old cab rides, renting out furniture from rentmozo, consumer purchase in amazon, flipkart paylater etc. IDFC First is cleverly tapping this segment. It makes sense for all the digital age companies with retail franchise to enable credit in their apps- to increase offtake of their services as well as increasing brand loyalty.

When i list down which lender fits better for these new agent internet companies to tap for long run- I have only IDFC First on my mind. Aggressive lending to the untapped customer base[Will cover more customers than any other banks underwriting policies], low cost liability, higher spread revenue for fintech, higher yields for IDFC, No beating around the bush on hidden charges.

[Clix capital too if they acquire LVB].

NIYO is also one such good neo banking platform built on IDFC partnership.

17 Likes

Hi all

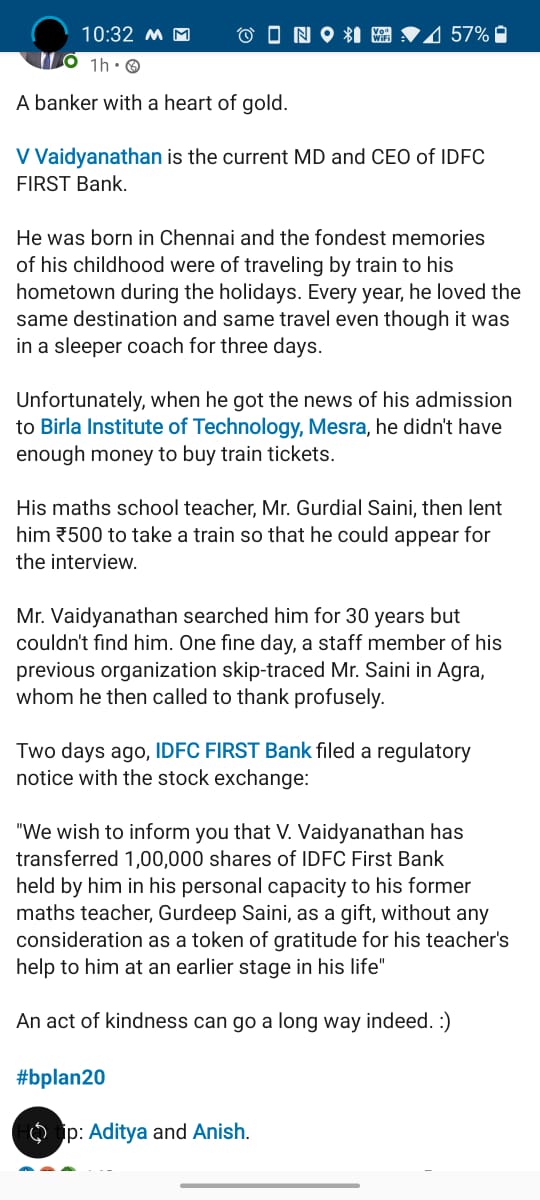

I think this instance and many before shows Mr V as a kind hearted soul with empathy. The above story is indeed true as I heard it from a person who worked with Mr V earlier (if I were to believe that too).

But I think this is Mr V’s personal involvement and we should not mix it up with the bank’s operations.

Also this amount is insignificant to what he holds. The story of the maths teacher emerged a few days ago. But Mr V actually had made another gift in the early part of August this year too. That story did not come out in social media I think. All the gifts are verifiable on BSE.

Was going through my notes from Peter Lynch’s book last night and he had a say on this - Insiders sell stock for multiple reasons. But buy their stock for only one reason.

So let’s move on

Rgds

6 Likes

A small positive development for bank’s retail and MSME loan book:

Center will bear the cost of interest on interest for loans up to 2cr in the march-August (6 month) period which will provide some respite to the borrowers (MSME and individual borrowers) and cash flows for the bank.

5 Likes

IDFC is carrying these bonds at only 50% value; a 9% bond with one year maturity yielding 27% is valued at around Rs 85 vs a face value of Rs 100.

Will this deal have some positive impact in IDFC bank and other lenders to VI.

Regards

1 Like