On IDFC First I mean. ![]()

I would like to understand if this happens, what will be the effect of this on IDFC First?

On IDFC First I mean. ![]()

I would like to understand if this happens, what will be the effect of this on IDFC First?

No effect at all on the bank.

Reverse merger in this situation will just involve the distribution of all bank shares to IDFC shareholders and IDFC ltd no longer being a promoter of the bank. There will be no other change and doesn’t impact the bank in anyway.

The IDFC first bank share value can be decreased because of availability of IDFC(promoters) shares in market. But it may changed if its absorbed by HNI & Institutional investors.

If reverse merger happens then bank will also get mutual fund business

AUM under management crossed 1lac crore recently.

Also bank has to allocate shares to IDFC share holders

All in all good for bank in long term

Reverse merger news is purely speculative in nature.

Hi All,

Does anyone have a source from where I can find out the Loss Given Default on various types of loans in the Indian Banking context.

Or any data on how much collateral IDFC First would be carrying against the different lending segments.

The Supreme court judment of Voda has any material impact to IDFCFirst? Though they conservatively provisioned in the right way… the fall of stock price is again over reaction - as market expected the judgment will favor IDFC bank and raised, now it is not positive over reactng… any views from experts in this forum?

Hi All,

RBI has modelled for around 8 % GNPA for Private banks in its stability report after Covid.

Anyone here have any idea about the assumptions behind this?

Can IDFC keep GNPAs below 8% or so?

I’d be very interested in this as well.

The impact on fundamentals is well known. i think its hard to comment on the vagaries of the stock market.

source? When i google searched I found this:

If this is for the banking sector as a whole, 8% might be very good. it was 11.1% in FY19, 9.1% in FY19 (not sure about FY20).

I believe it is somewhat positive. IDFC Bank has anyway made the necessary provision. The judgment gives SOME hope of recovery. Difficult to comment on the stock price movment.

How big a blow can this be?

This is a blessing long awaited. Mr. Lall is one of the most incapable banker/lender inthe history of corporate India.

The way infra loans were disbursed and handled afterwards speak loudly about capabilities of Mr. Lall and his team. Good riddance!!!

Won’t be surprised if the stock price react positively.

Disc. Invested in IDFC limited.

Had some thoughts but I’m not too sure if my thinking is correct. Putting it here for those more experienced in banking to weigh in.

The bank has provided ~600 cr for covid related provisions, over the past two quarters. It seems quite clear that the Vodafone 1500 cr will not be required for that a/c. So cumulatively, today around 2100 cr has already been provided for.

Given the loan book of approx 1 lakh cr, if the bank has 6% NPA’s in a few months, that is around 6000 cr. The restructuring proposed by the RBI requires a 10% provision for restructured amounts i.e. around 600 cr. So the current provisioning actually accounts for 20% NPA’s which get restructured. Alternatively, if the NPA’s remain at industry expected levels (5-6%), almost the entire Vodafone amount can get written back.

Would it be correct to conclude that the bank’s current provisions are easily in excess of what will be required in the near term, and in fact quite certainly there will be some write back, whether 500 or 1500 cr. As the loans get restructured, some may still default but that will be spread out over the next few years.

Big question mark that remains is the Supreme Court verdict on interest upon interest and the current stay order on NPA recognition. As a lawyer myself, quite frustrating to see the judiciary constantly interfering where they have no domain expertise.

I would not be so sure about this. Vodafone-Idea: Rs 25,000-cr won’t last Vodafone-Idea beyond 12-18 months: SBICAP Securities - The Economic Times

imho, vodafone is still in a battle for survival. 97000 cr of debt, losses that keep growing over time. Interest outgo which equals Operating profits:

On a separate note, I can see IDFC First Bank tying up with fintechs like Cred and OneCard. These companies are providing unsecured personal loans. I understand that these are being provided to customers with high credit scores but the bank itself is not screening these customers. What do you guys make of it? (let’s keep in mind the risk of unsecured loans in the times that we are in)

Fair points. The bank doesn’t need Vodafone to thrive though, or even be profitable. Just to survive and not go into insolvency till the repayments are due.

Given the talk of equity infusion, the investors will also be fully aware of the funding gap. The debt you speak of will also be payable in installments over a long period. It seems a little illogical for investors being fully aware, to put in money if the company were to go insolvent in the near future. Simple projections will show at least the short term viability to them.

My understanding is that the debt with the bank is payable relatively soon, though I don’t have a source for this information. If so, I’m fairly certain Vodafone will pay its dues as the other option is insolvency where the promoters as well as the investors will lose control.

Even if we exclude the Vodafone potential write back, the bank seems to have already provided enough for ~6% NPA which is what seems to be the industry expectation. Even if they take similar provisions again in the coming two quarters, there seems to be a strong likelihood of provisions being taken care of in this calendar year, unless the NPA’s are way higher than the industry.

So we can expect the BV to start expanding from CY2021. These are my conclusions, but again, more knowledgeable people are welcome to point out where I may be going wrong.

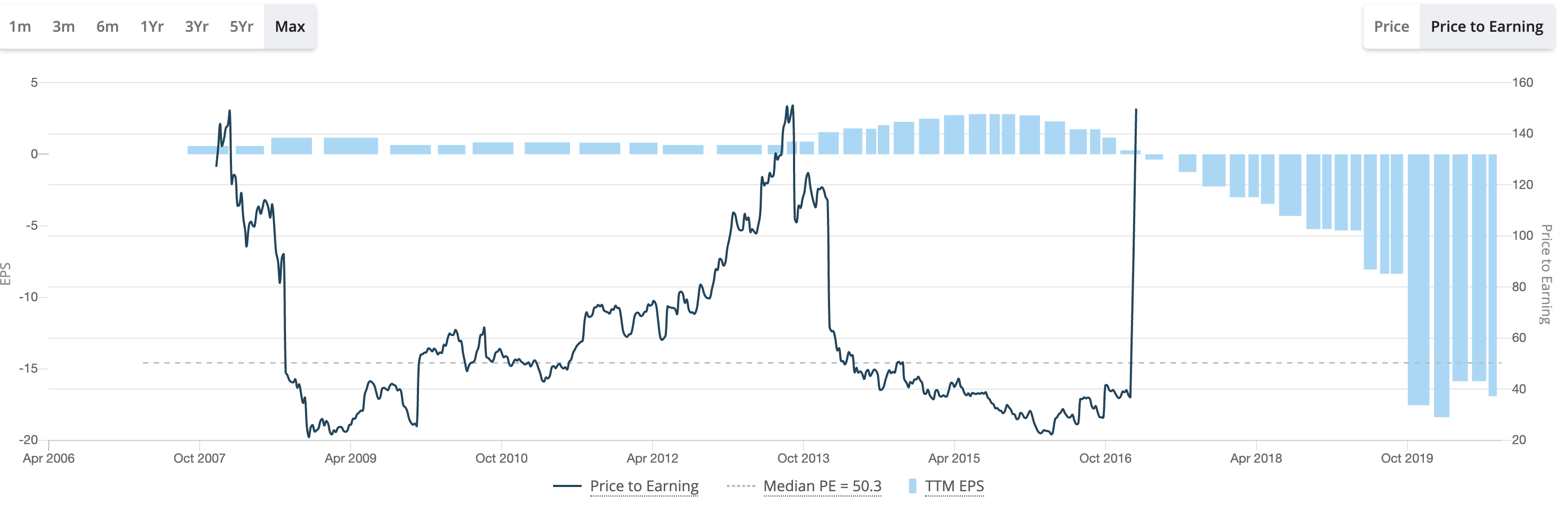

I would urge you to take a look at their current finances, attaching screenshot below:

I would very much like that as well. Any idea when the VI payments are due? (if my memory serves me right vaidya had said in an interview that it was due in July end). They are not defaulting on their payments until now, which is a good thing.

Any sources please?