Thanks for your advice. Point noted.

1 Like

@prashant_kishore - Did any one ask about the management to host conference calls for every quarterly results

Yes, so many people asked this question.

I didn’t listen VV reply to this question properly. So, i have not added to above summary. I am not sure about the final decision, but yes many asked this question.

1 Like

1 Like

After Q1 results, Arihant capital has raised the target to Rs 39.

2 Likes

PrabhudasLilladherPvtLtd_IDFCFirstBank(IDFCFBIN)-Q1FY21ResultUpdate-COVIDimpacttokeepreturnratiosdismal-Sell_Jul_29_2020.pdf (649.8 KB) EdelweissSecuritiesLimited_IDFCFirstBank-Earnings-positivequarteruncertaintylingersresultupdateQ1FY21Hold_Jul_30_2020.pdf (1.3 MB)

Some more reports

Not invested and not planning to invest.

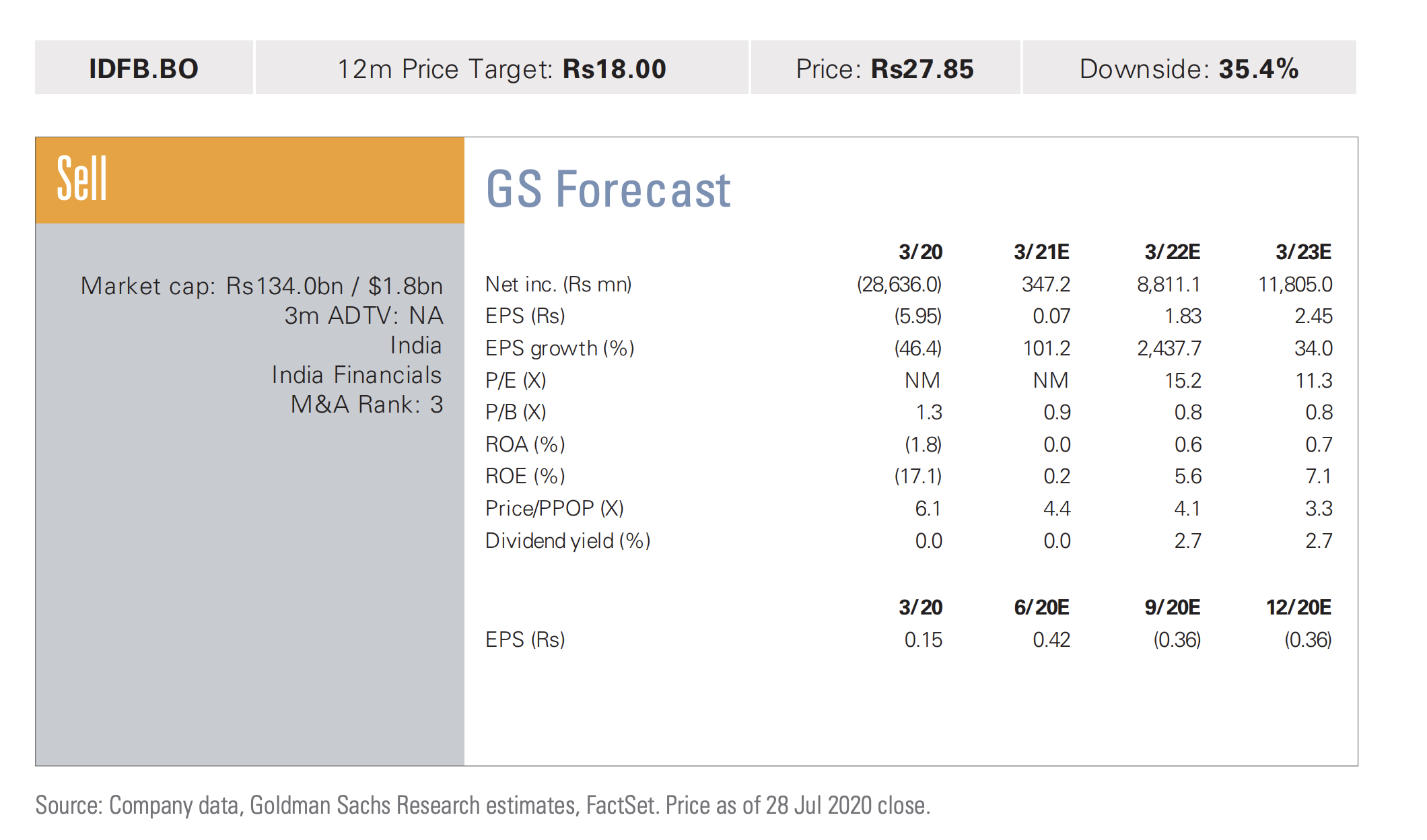

Thanks for sharing. These reports make me more and more confident of relying on independent thought and independent analysis. The exact same set of numbers can always be interpreted as glass half full or glass half empty. The goldman report in specific is funnily incompetent in my humble opinion and I will prove with facts why:

Observe how Goldman essentially forecasts a strictly increasing EPS and ROA and ROE each year, including 1st time positive EPS in 2020 and EPS of 2.4 rupees in 2023. Now if the bank is slowly turning from loss making to profitable with EPS becoming 2.45 in 2023, why would the P/E ratio become lower from 15 in 2022 to 11 in 2023? The entire piece seems like a hit-job to me. These institutions have vested interests front, right and center. If they are overweight on HDFC bank (as an example) or any other portfolio bank, it makes perfect sense for their analysts to interpret numbers for competitors in the worst possible way (often without much logical justification). On the contrary, they would try and paint a very rosy picture for their own portfolio stocks. For these reasons, I prefer to only rely on the facts from such reports, and not the opinions.

Disc: Invested and adding a little every week.

16 Likes

I was coming with same kind of analysis but it’s good that someone posted the same with relevant facts. Sometimes these reports are so misguiding that any one can spot them in a glance. And then giving a target of Rs 18 sums it up well!

Disclaimer: Invested and adding in every dip.

2 Likes

The good thing from the point of view of people like us who are investors is that if and when the bank does turn around there will be a lot of institutional money that will chase this story.

Then only the positives will be seen by these ‘experts’.

A telling example of their so called expertise is the fact that everyone used to keep harping on how the bank will not be able to raise CASA since it is so hard, how will they retailise etc etc.

Now no body questions that.

Infact if Covid had not struck then their research recommendations from a year ago would have been looking extremely stupid and they would have started mentioning only the positives of the story- ‘strong private equity backing’, ‘World class management pedigree’, ‘great implementation’ and suddenly the PB target would be 2.

These guys write english essays rather than research reports(most of them) and hence the slow death of active investing (by firms with so skin in the game)

9 Likes

The p/e target given by them is the current price vis a vis projected earnings. Not their projected p/e with ttm eps in 2022. With the earnings going up the p/e is bound to be lower. So they’re not saying the valuation will keep going down over the years, rather they’re giving you multiple current valuations, based on current and future estimated earnings.

Do agree though that they’re taking a fairly negative view. The bank is essentially a bet on the future, while they’re only looking at the current negative picture. Closely monitoring the moratorium book, vv is known to under promise but if they don’t come to 10% by August, it may be time to book some losses and wait for things to stabilise.

3 Likes

IDFC First Bank’s book value is very close to current price. Axis Bank is currently trading at P/B multiple of 1.33. I think 1.2 multiple for IDFCFB is possible but more likely to see less multiple expansion than Axis from this level.

Few powerful concept i have learnt and practiced is (after very costly mistakes over the years!):

- it is ok to book losses if one is merely shifting from sector/companies with headwind to sector/businesses with tailwind. Rotation.

- Point 1. is most efficient use of money and is driven by fundamental and technical view. Fundamentally I strengthen my portfolio by making it strong given current realities. Technically, market pushes up business with tailwind as that is where most of the buying is and so my portfolio becomes resilient. Plus role of hope reduces significantly.

- Value investing only works if there is a clear near term trigger. Else cheap may become cheaper before that eventual trigger arrives in the future.

IMHO - Financials is the sector with most headwinds currently. And within financials, most mid-tier banks (RBL, Indusind, IDFC First) and most if not all MFIs are facing lot more headwind than the larger peers (HDFC, ICICI).

Not invested.

2 Likes

Can forum members throw some thought on the large Equity float that IDFC First has.

What are the negative and postive(if any) due to such a huge float.

Disclaimer : Invested

1 Like

I think a large part of the headwinds constitute the moratorium and the unknown NPA issue. However, if the moratorium book comes down to ~10% in a month or so, as promised, I think that issue would be largely taken care of.

Aside from that, based on my limited understanding the bank seems to be performing well on all parameters. The credit growth may have been subdued this quarter (flat), but I’m fairly certain that will pick up soon, and in all other respects they are performing very well. Instead of comparing to HDFC or Kotak (which we know this bank isn’t right now), it would be better to compare to IndusInd, Axis etc. as the more achievable targets.

3 Likes

The recent RBI allowance of restructuring of loans (without changing ownership or downgrading the borrower) for retail individuals, corporates, MSMEs is quite a game changer. This effectively means that the NPAs will remain hidden for years (i believe the restructuring allows for tenure extensions as well as moratorium extensions up to 2 years).

Couple of videos I saw on this:

– Aug 2020")

My take: This is quite a smart move on RBI’s part. The conditions make it quite clear that this only applies to entities who have been affected by Covid19. The conditions are pretty strict. There are enough entry barriers. As of March 1, you should be a standard account to get a restructuring. The restructuring should be decided by Dec’20. Banks need to keep 10% provisions on post-resolution debts.

For large corporate loans, the restructuring has to be vetted by a central committee/panel headed by KV kamath. The most strict rule is that 30 days of default would tag the account as NPA. The rules are really strict. At the same time, they allow breathing room for a genuinely impacted entity.

Disc: invested, full portfolio is on this thread.

5 Likes

Cheers Sahil. So basically, idfc first bank has already guided for 28% to 10 percent end of August. Now the moratorium isn’t extended… so in all probability they will restructure those 10 percent loans in September. Knowing how conservative VV is even after restructuring he will provide more than the stated amount percent of provisions for those especially from msme and large corporations related to the travel, tourism , entertainment, infra sector. So overall those 10 percent NPAs (im assuming these woild be the genuinely distressed ones) would then get spread over the next few months/quarters due to the restructuring. In the mean time they’ll be very strict about lending and will not lend to those affected sectors and similar accounts since they have a good idea about who not to lend to now. so the risk of new NPAs will be low. So overall the percent NPAs per quarter will not be as high as everyone is actually imagining. And if they are conservative and scrupuluos(which they are) then we can expect flat growth but normalisation in NPAs over the next few quarters. Hmmm… i think waiting for this NPA issue to clear before investing may not be the best plan anymore since it may just get diluted over many quarters and may end up becoming a non issue sooner rather than later . Ofcourse that is if they do manage 10 to 15 percent by August 31st… and management has always done what they say they’ll do. The deterioration of book value may not even happen in this scenario. Unless I’ve understood this wrong of course. Cheers

3 Likes

The restructuring is precisely to ensure they do not become NPAs. All efforts are being made by RBI to make sure genuinely affected companies get time to restructure debt. As an example: a road construction company which pays down debt from toll collected on highways is distressed. they could increase the tenure of the loan, reduce emi and would hence end up not becoming an NPA.

Yes. This was precisely the intuition behind the RBI decision. They do not want companies which were operational pre-march to become NPAs due to covid.

This is what an investor would hope for. Btw as i had pointed out in earlier post, the process for NPA recognition will become more stringent for these stressed assets. 30 days of non-payment will convert them to an NPA. Frankly i find the RBI action to be very balanced. If a business/retailer can prove their cash flows have been impacted by covid, they can even get a 2 year moratorium from the bank, this is entirely up to the discretion of the bank. Bank can lower the interest rate, bank can increase the tenure of the loan, ask for more of a down-payment, larger collateral, everything is fair game.

As we had discussed earlier, the banks with correct processes for dealing with stress will emerge relatively unscathed from this, whereas those with poor risk assessment processes will take a larger hit.

Disc: invested, full portfolio is on this thread.

9 Likes

How to interpret this? How this is going to affect IDFC FIRST? @sahil_vi Tagging expert here.

2 Likes

Can idfc Ltd can distribute it’s holding shares of idfc first bank to IDFC ltd share holders after sep 2020 locking period?

I am no expert on Reverse mergers

I saw these 3 videos which explains the concepts well although they are in Hindi:

- https://www.youtube.com/watch?v=VMeJ6Cio4zY

- https://www.youtube.com/watch?v=WI7RL8eaK-4

- https://www.youtube.com/watch?v=v5x1ao7SmTs

From what I could make out, in essence it is like a buyback of shares by IDFCF by paying cash to the shareholders of IDFC and reverse merging IDFC Ltd with IDFCF bank. In any case in next 5 years, IDFC ltd has to reduce its shareholding in IDFCF bank to 15% over next 5 years. So the reverse merger might be 1 efficient way to get around that (from what I can understand). For the same earnings, the EPS could go up by ~66% (depending on how they finance the reverse merger) while book value would not change. Share capital would shrink by 40%. This would need to financed with cash (as per the video’s hypothesis).

Overall this is only a rumor at this stage and might not be worth thinking about a lot.