Part of any intelligent analysis is focus on outliers. The co’s rapid growth and performance on metrics has certainly been an industry outlier for last 2-3 qtrs.

This makes me skeptical - what is this Bank doing that others aren’t which is facilitating such performance? Is it genuinely a differentiated strategy, focussed execution or the dark side of it - simply a cooking up of things. Have been studying this for some time now ( incl. the wonderful posts on this forum) but still not able to figure this

From a Bank’s customer perspective - Thr earlier strategy of less branches and more processing online seemed to me a good sustainable cost saving move. But now it seems, they are opening more branches as well.

The thing is… they aren’t outperforming the industry. Far from it. What they’ve been doing is they’ve been in such a bad scenario over the past few quarters and years that all they are doing is cleaning up their bad books. Their revenue last year was equal to Kotak Mahindra revenue in 2016 so net interest income was never their issue. All they are doing is going from being non profitable to being slightly profitable by moving from bad practices to good practices(low retail, low casa to high retail, high casa etc). So by no means are they an outlier. Theyve just adopted good practices from good banks with the aim of reaching a good bank level from a terrible starting position. That being said their customer centric focus and good use of technology+capability to give 7 percent interest on a savings account is helping them too. Overall I wouldn’t say there’s a dark side to this. There was just a terrible side and now it’s slightly better and hopefully in the future it will be good. In my eyes it’s the definition of a turn around story with very low downside. It’s better investing at the lows in these scenarios since there’s not much lower to go lol. The Moratorium issue will be a huge overhang on this bank and financials overall this year though.

Disc: invested

Wat I meant was, if u trace VV from his CapitalFirst time, thr also the growth was in good 25-30% range since inception till the merger. Here again, if u see wat they mentioned as thr 5-yr objective, they achieved it in 1-2 yrs.

I’m trying to figure out the reason for this - this is either super-brilliant execution ( meeting ur objectives well in advance), pure coincidental luck or some cooking-up of books

If cook up happens, the results could have been further boosted and better… and no provision required for voda… i see many pharma (no fundamental) & chemical companies in commodity nature commanding premium… anyway - time has to tell how things are good. Have humble expectation and minimum percentage in each company that you invest in - ready for 1x loss. dont go more than 20% of your investment in your top holdings - should save 80% in others. If your 20% becomes 60% - just leave it to run ahead by taking off 10% from the table. So you are sure of overall good return. We can bet on Management/size of market/smartness of the company as parameters. emerging institutes like IDFCFirst/AU small may give some good chance

VV has been rescuing companies in both positions… it’s easier to take a poorly run company and then get 25% growth from a relatively poor position. It’s difficult to take a already functioning good company and then make it grow 25% from that relative position. I’m hoping we reach a point where we need to discuss whether VV can take a good company and make it even better since if we reach that stage it means us investors would have already benefitted greatly by then … And tbh VV does the opposite of cook the books. He always puts extra provisions even when he doesn’t need to and always gives cautious commentary and then outperforms. I’ve yet to feel slighted by the management and it honestly feels like I’m part of the board of the company due to that lol. It’s probably this cautiousness that has led to a stagnant price. They could ve easily shown profits and skyrocketed but they chose not to and I appreciate that.

I am inclined to agree but then Mr V Vaidyanathan’s past track record makes me hesitant towards thinking in this direction. In Charlie Munger’s words, I am also personally biased because I realise his way of thinking (what I consider clean and transparent) actually adds real economic value to not just the business but the entire ecosystem.

Now I am not saying HDFC doesn’t do that but I am yet to get educated on how HDFC Bank or other similar banks like Kotak Bank behaved back in their early days. Were they too very customer centric and people oriented banks?

Consider another large bank and a large NBFC player (ICICI and Capital First), since Mr V Vaidyanathan was at the helm of ICICI for a considerable duration and entire duration for Capital First - he has proven that his ideology and way of thinking works time and again.

Another thing from personal experience in general - It is not necessary that the way one person behaves (say being customer centric / people oriented - e.g. liberal towards moratoriums, etc.) has to be mutually exclusive when it comes to making profit in business to another person’s behaviour (the one who is business/money driven, thinks more about not being nice but being a shrewd business person). Both personalities work and have time and again proven successful in various industries across the globe.

There’s a successful Ratan Tata, Anand Mahindra, Warren Buffet, Charlie Munger, Mohnish Pabrai group and so is a successful Jeff Bezos, Carl Icahn, etc. You get the point!

Happy investing

Disc: Not invested - Just came across Mr. V V last week while reading up on inspiring personalities and their achievements in Indian Banking Ecosystem.

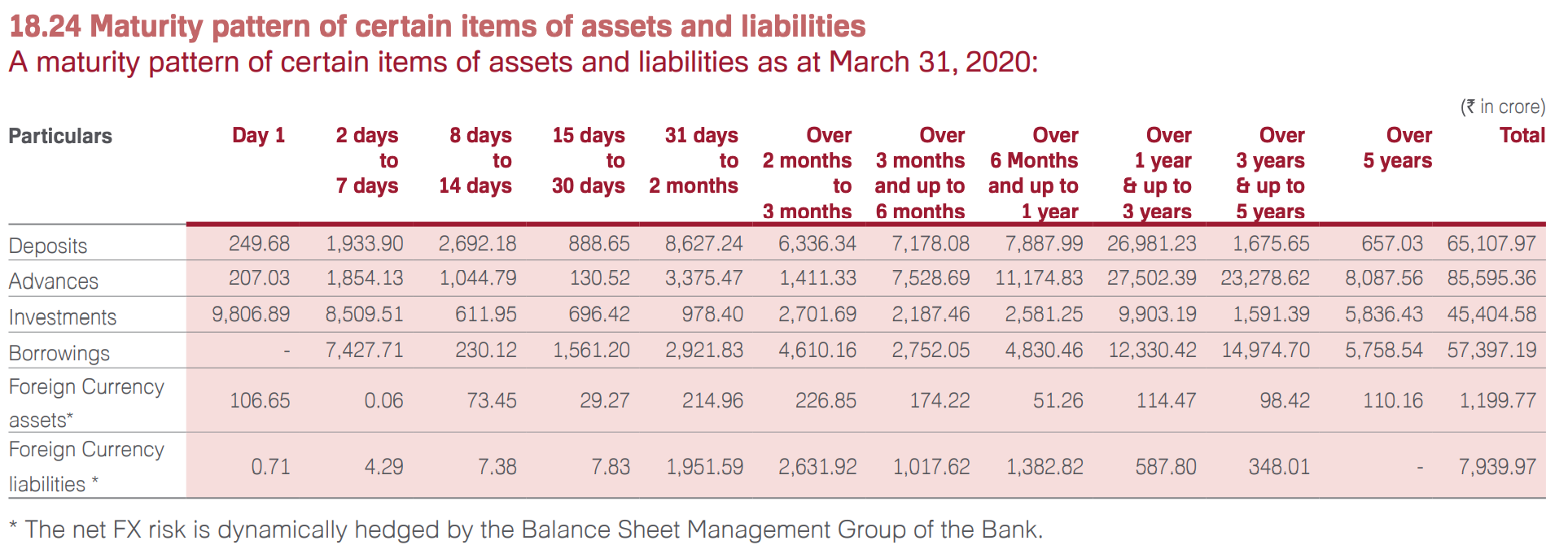

Treasury assets decreased from 73K crore to 58K over last 12 months. Bank’s treasury holding seems large compared to size of its balance sheet. Why is bank holding 58K/150K ~ 40% of the assets as a treasury assets?

I guess most/all of these are government securities which must be providing less returns than high cost borrowing/CD based financing. Even corporate presentation doesn’t provide any insights into reason for these large holdings or discussion about large reduction in last 12 months or going forward.

Yes.

The earlier strategy of less branches & more online was with Dr. Rajiv Lal, his vision was of new generation bank.

But, they couldn’t grow with that strategy. Retail growth was very slow.

With VV the vision is build a good retail focused bank. He wants to have CF business model under the banner of a Bank. It’s working well.

I see a moat here, with his focus on Banking on the Unbanked, focus on retail

Disclosure : IDFC First bank is my top holding

Being customer centric is vital for business. However one must remember that if a customer starts eating into your business and causing losses then he is not a customer but a parasite and to be avoided. I feel that the previous success of VV has demonstrated that he recognises this difference. His statement of being customer centric should not cause alarm. First responsibility of any management is towards the owners/shareholders and they know it.

I second that.

VV is an honest person plus he has a vast experience in raising the Banks to a decent stage from scratch. He has implied his methods successfully first with ICICI and then with Capital first. So the main equation which says Good management bad company fits very well in his case and Warren buffet always says that Good management bad company vs Bad management Good company- choose the former one!

Second thing is whatever targets were kept by him whether it was CASA ratio/CASA, wholesale to retail transformation, no. of branches etc. are being met well before time and sometimes he is exceeding our expectations.

So I am investing on Bank’s future which looks great because of its dynamics, well management and very low penetration in MSMEs/rural areas loans. Stock may or may not respond for 1-2 years but it will definitely follow the actual value once everything keeps falling in place. This happened with Rain Industries too when the stock hovered around 30-35 for 2 years and suddenly exploded to rs 300-400 in 2018. Although it has different story but underlying principle remains same that buying will follow the results.

Disclaimer: I had spread of 9-10 stocks earlier in my portfolio which has changed to only 1 i.e. IDFC Bank so my views may be biased as I am heavily invested in it.

I am very bullish on idfc first bank long term as seen by my posts above… however, I feel the risks need to be discussed too especially since it’s your only stock. There will be a cap on nbfcs and banks this year and maybe next due to the Moratorium overhang. So even if everything looks good for the next few months banks and nbfcs including idfc bank won’t explode. There will be higher npas than usual even with the best of management so book value could get eroded even if it’s just a small amount. During this period you can take your money and invest it in pharma/chemicals (there are a plethora of companies… I won’t name them) and theoretically get a 100 percent return in 1 to 2 years. Once the moratorium overhang goes you can come back and buy idfc first bank at a similar or slightly more expensive or slightly cheaper rate. So it’s all about opportunity cost for 1 to 2 years. Investing in sectors with tailwinds makes sense now. However, I wouldn’t book losses if bought at higher levels since long term this will be a star. It’s just that it’s story may stall for a year or two and till things improve you can potentially make a lot of money elsewhere and revisit this later and potentially buy a lot of more stocks of idfc with the profits made elsewhere. Just playing devils advocate here but don’t expect too much and don’t get frustrated owning it for the next year if it remains rangebound if you decide to commit to it.

Is it possible for us to monitor whether this payment ended up happening or not? Worst case (time wise), would we expect this to be revealed in Q2 results?

PS: Did anyone attend the virtual AGM which happened on July 30? If so, could you please share your notes or observations? I could not find anything on the internet. And couldn’t attend due to day job.

It is surprising that Vodafone has not protested against the provision made by IDFC first Bank inspite of the account being standard. I am sure it has shut off any hope of bank financing for Voda till this provisioning goes off from the IDFC books. No bank or financial institution will come forward under such circumstances.

How does a dying organisation find time for such a thing?

There is no way Reliance let’s Vodafone live.

Either through 5G rollout or through cut throat pricing, Vodafone is the living dead already.

They have anyways submitted evem to the Supreme Court that no bank funding is possible.

Have u analysed cash flow for Vodafone, Jio boasting of 2

39 cr subs however VLR figure is 77% which shows that actual base is 30 cr, Voda actual base is 27 cr, last quarter EBIdTA margin at 37% despite loss of subscriber. Just a comparison losing 50 Lakh migrant subscriber will add revenue of 500 cr at recharge of 100 which is high nd adding 2 Lakh RedX subscribers will add revenue of 264 cr. Mukesh will not be able to shut Vodafone, it will thrive nd prosper again. Wait nd watxh

Yes, I have attended IDFCB AGM meeting. It was good experience. Let me share few important point which i remembered:

-> Someone asked about mutual fund or credit card scheme near future like other larger bank.

VV- No plan for mutual fund near future, but IDFCB will be launching credit card soon.

-> Someone asked about any plan to reduce 7% interest rate on saving account as it is burden for bank in covid-19 situation.

VV- No plan to reduce interest rate as of now. Yes, IDFCB is providing higher interest rate compare to other bank, but if you see capital first interest rate, it is is 8~9%, so compare to CAPITAL first, 7% is cheaper.(Explained in Annual report)

-> Someone asked about any plan for reversing Vodafone idea provision.

VV- We will not reverse the provision as there is no clear picture on Vodafone idea issue. Bank will reverse the provisioning only when bank find out Vodafone idea issue is resolved completely.

-> Regarding 2000 cr allotment.

VV- We are facing covid-19 like problem first time in history and nobody is completely aware how far it goes. The money is for bank insurance in difficult time. As of now we didn’t see any major problem with IDFCB near future. Those money will used for bank growth if required.

-> Someone asked about plan for opening new branches near future.

VV- We are looking at COVID situation closely and based on that we will take decision whether need to open branches aggressively or not for this year. If covid-19 situation is not coming down, instead of opening branch aggressively, bank will focus on digitization. Already using Video KYC feature.

-> Someone asked about opening personal twitter account.

VV- I find social media is distraction for me. I want to focus on work, there is lot of work daily, have tight schedule and cant handle social media account. There is separate team for Social media account and is handling all the social media query.

Please let me know if any one having specific question related to AGM meeting. I will try to remember and summarize.

I will add more point if i remember.

adding one more point:

Some people asked- How safe my money in IDFCB because we have seen recent issue with PMC bank and Yes bank ?

VV- Your money is completely safe with us, no problem with bank. Some people invested their life saving to this bank. To them, i want say that If you keep money with our bank(saving account, FD, RD etc), your money is completely safe, there is no issue. But some people invested their life saving money to equity. To them, I want to say that you should not invest all your saving to one equity. You should not do that. This is not right way to invest and You should diversify your investment properly.

Found additional details in the annual report about investments held by the bank. Large percentage of the holdings is required under SLR and it involves holding of government securities but bank also holds additional investments which seems much higher percentage of its total assets compared to other banks such as HDFC Bank.

… And tbh VV does the opposite of cook the books. He always puts extra provisions even when he doesn’t need to and always gives cautious commentary and then outperforms. I’ve yet to feel slighted by the management and it honestly feels like I’m part of the board of the company due to that lol. It’s probably this cautiousness that has led to a stagnant price. They could ve easily shown profits and skyrocketed but they chose not to and I appreciate that.

… And tbh VV does the opposite of cook the books. He always puts extra provisions even when he doesn’t need to and always gives cautious commentary and then outperforms. I’ve yet to feel slighted by the management and it honestly feels like I’m part of the board of the company due to that lol. It’s probably this cautiousness that has led to a stagnant price. They could ve easily shown profits and skyrocketed but they chose not to and I appreciate that.