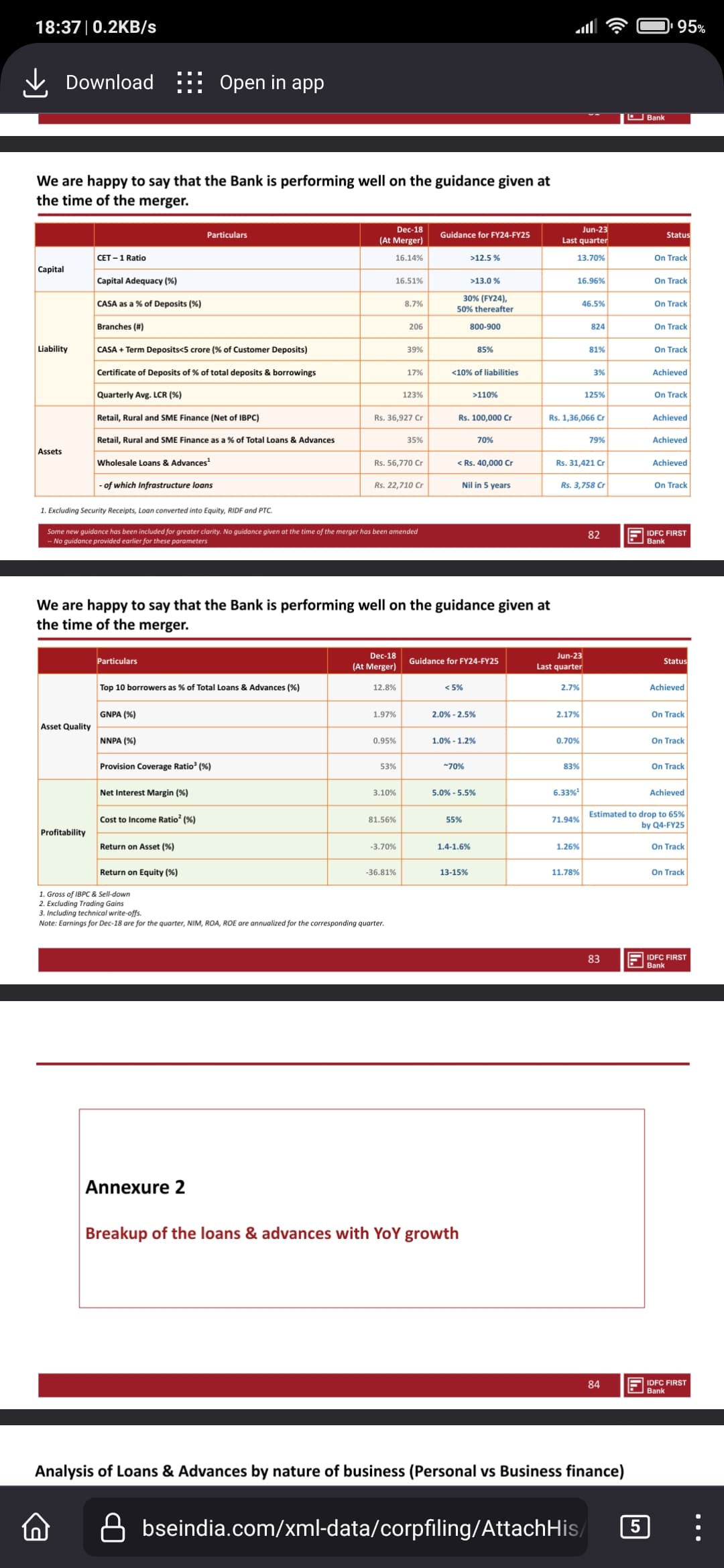

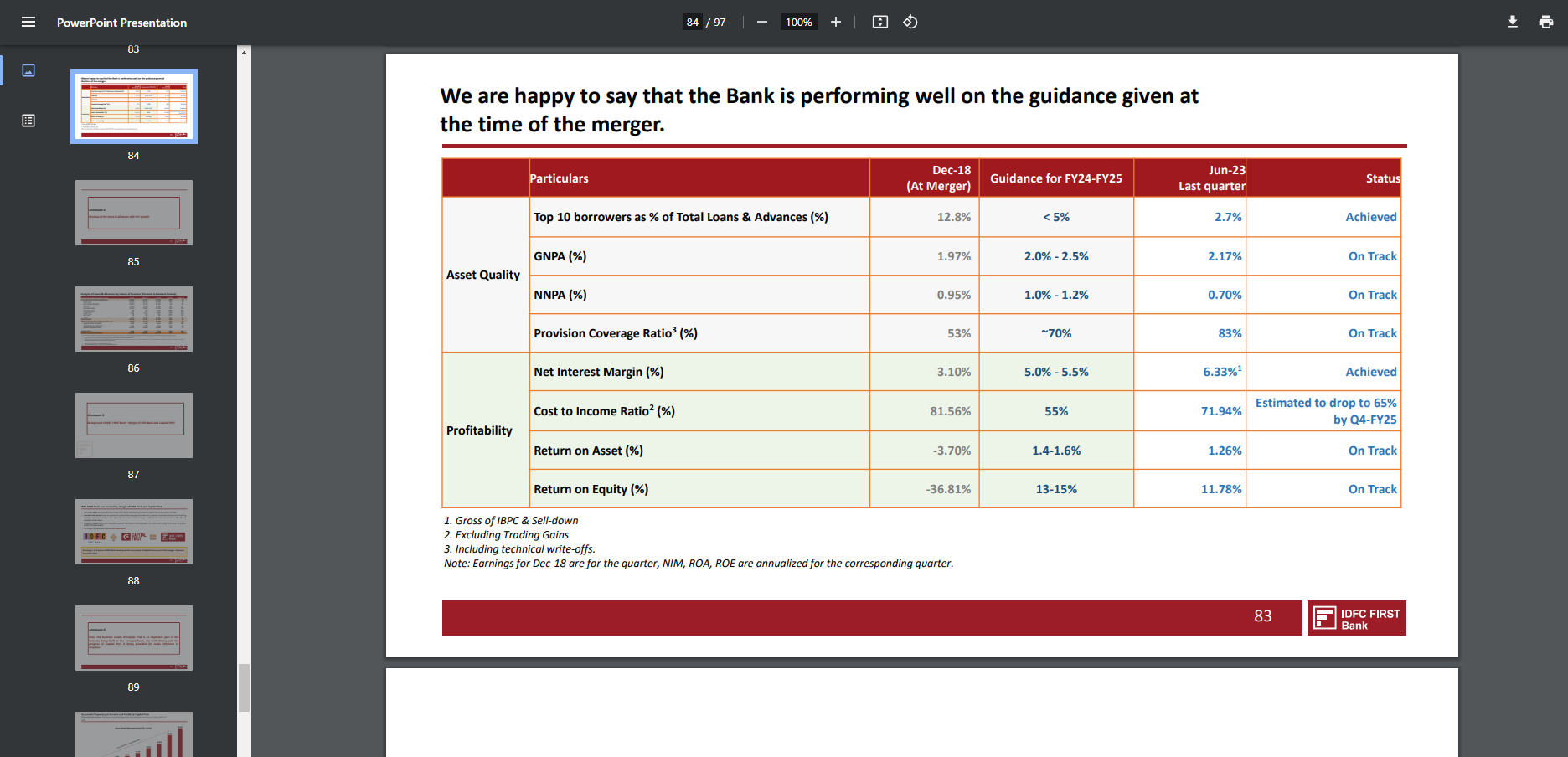

I am posting on this forum after a long time. Bank has been performing better than my expectations on all fronts except C/I and next parameter in line which the management will address is C/I for which the bank’s target is 65% by Q4FY25. This target itself indicates that huge operating leverage is going to play out in the next 18 months.

Regarding whether the valuation is expensive or not, I would say it depends on how far you are looking into the future and your confidence on the management to deliver. My own estimates indicate that the bank is going to post a core PPOP of 9600-10000 crs in FY25 and an EPS of Rs 7.7-7.8 in FY25. It might sound optimistic to some people but then these are my estimates based on my model and I reserve the right to be wrong.

IDFC First and IDFC Merger offers a good arbitrage of 15-16% to IDFC First investors to sell the bank shares and buy IDFC Ltd. There will be tax implications but then eventually you have to pay tax whenever you sell the stock at a later date too. I have converted my IDFC First stock to IDFC Ltd. So with the transaction, which yielded me 15%, I used 7% to pay my taxes(making the gains till Rs 87 tax free) and the rest 8% to buy more of the bank via IDFC Ltd.

If one is buying IDFC Ltd at 124 today, he/she is effectively buying IDFC First Bank @ 80 which in my view is not expensive at a P/E of 10.4 FY25 earnings( For a bank targeting 18% RoE by FY26) or P/B of 1.43 FY25 Book Value.

Don’t you think 7.7 for F.Y. 25 is too optimistic…from current F.Y. EPS which is expected to be around 4.5-4.8 rs. with 705 crore existing shares and 3200-3400 crores of profit, that is a 60-70% jump in EPS in a single year…am I missing something here…

This is quite possible as management itself is guiding PAT increase of about 50% as there is a huge operating leverage play. FY23 EPS was 3.75 and if they are able to grow at 45% CAGR, then FY25 can be around 7.8. This is not factoring equity dilution, in that case they need to grow more that 45% to justify above estimate.

Management has guided for a core PPOP increase of 40-45% for FY24 and FY25. If core PPOP increases by 40-45% and provisions are expected to increase at a lower rate of say 27-30% then PAT will grow at a much higher rate of around 55%. Considering the extinguishment of shares from the reverse merger process, shares outstanding will be some 688-689 crs. This yields me an EPS of Rs 5.05 and Rs 7.7(based on share capital of 688 crs after merger). Once the market sees such kind of growth, rerating is very much possible.

The bank should end the current F.Y. with approx. 3800 crores of profit (55% growth over last year) if we want to believe that the bank will perform according to the guidance even when NIMs are expected to shrink across the sector due to rising deposit rates in general and rising expenses like BCCI sponsorship for IDFC First in particular…looks tough but I will be pleasantly surprised if they do that …

To drive share price, valuation pays equal part as growth. I have sold my RBL bank in 2018 at 5 times book value. So valuation still have scope to increase with consistency in reported earning and increase in RoE. Though none of the private bank is trading at 5 times book now, we do not know valuation given to banks will increase or collapse? If both shows increasing trend, valuation will increase and vice versa.

Disclosure: Holding

Exited the bank last week looking at the over-optimism in the market and the QIP placement done recently. The bank had become 40% of my overall portfolio and hence wanted to re-balance as well.

I may be wrong but shifted the proceeds to banks like HDFC which are not market favourite right now and no-one like it as it gives me MoSafety. The bank may keep doing well but market may not reward as much as market gives the best returns in terms of surprises and I believe that phase is over for bank.

Will keep tracking as I like the Jockey of this Horse

In the forthcoming approvals NCLT might take time.

Key one would be SEBI; i have notion that SEBI might not approve 6% Holdco discount. Might ask boards to revisit, since this is not in favor of IDFC Ltd’s shareholders.

Disc.: Invested in IDFC Ltd (32% of PF) hence heavily biased.

I am not sure if SEBI is the right authority to comment on valuation, it is for the shareholders to decide and if they feel aggrieved by the exchange ratio, they may approach the NCLT (and not SEBI).

Q2 results and press release… disappointing at first glance, no QoQ growth for a bank which has just started its journey towards normalisation of profits in last 1-2 quarters and promised 40-45% growth in operating profits in current and next year…looks like the train is already losing the steam…

. 085d0b79-8a1d-4bab-9280-c07b5949a92c.pdf (4.5 MB)

. 0e272e1e-e4f3-4b72-aff4-4b913118774d.pdf (418.6 KB)

I generally extend benefit of doubt to companies for misrepresentation of data or inaccurate reporting. But I don’t do it for banks and specially for IDFC First whose brand is built on transparency.

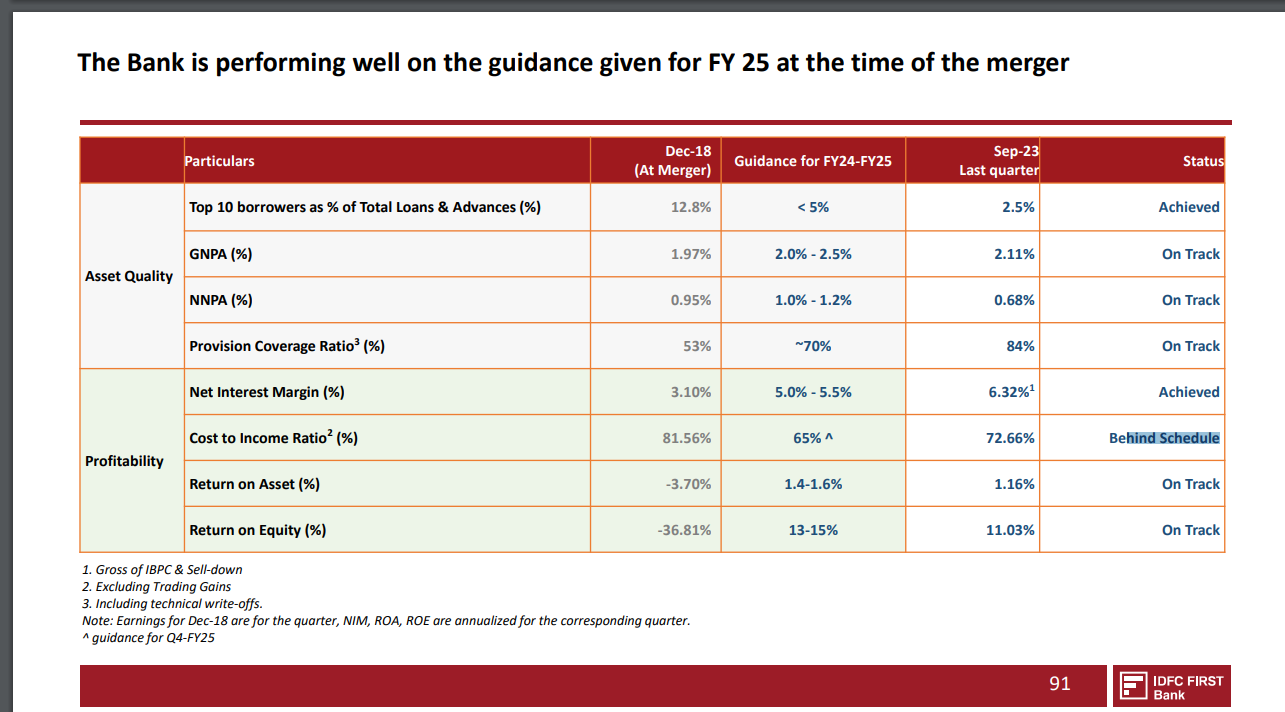

They quietly changed the target for cost to income ratio in the investor presentation from 55% to 65%. Now, they are allowed to change the guidance however the slide still says we are performing well on the guidance given at the time of the merger. Saying this, they shouldn’t change the guidance. 65% was not the guidance AT THE TIME OF THE MERGER.

It’s this kind of inaccuracies that start to question the intention behind miscommunications. Attaching the screenshot for comparison.

I don’t believe it is a case of miscommunication. In the Q1 FY 2023-2034 investor presentation, they updated the guidance, indicating an estimated decrease to 65% by Q4-FY25.

Book Value per share as in Oct.'23 (post fresh equity, QIP) is Rs. 43.48.

Have done some simulation for 1 yr i.e. Sept’24, considering:

With pressure to meet Cost to Income target of FY 25, opening of new branches shall not be aggressive, more focus on business growth in current branches.

4% QoQ growth in BV

5% increase in Q1’25 in BV with reverse merger

No fresh equity

Simulated BV at end of Q2’24 comes out to be Rs. 53.41 per share. That means currently, Bank is available at 1.6 times 1 year forward BV (1.5 times if invested via IDFC Ltd).

Disc. Invested from lower level via IDFC Ltd., largest holding. Hence, biased.

Reverse merger will add approx. 1 rs to book value…so for book value to increase from 43.48 to 53.41 bank will need to earn profits of 6100-6200 crores in next 12 months i.e. average 1550 crores per quarter compared to current profit of 750 crores per quarter…which is almost flat from last 3 quarters…or am I missing something here…

There is no QoQ Page in Key Highlights, although one can calculate easily. Earlier bank used to give both YoY and QoQ in key highlights section. May to hide muted QoQ growth.