When the merger is going to complete for this with IDFC.

This time period has taken the pace off the stock price movement.

Once it is done. i believe it is a long term bet. This bank is very aggressive to take the market share.

1 Like

I think the way bank business is organized, it can be a good long term bet too. However a lot is riding on a single man (but that was the case with HDFC too). Except C/I ratio, all other matrix are in good shape.

Having said that, HDFC grew in the times, when the competition was low. Now every banking product (e.g. car loans) in itself is a sub sector with multiple companies competing.

I would love to hear your reasons for holding the stock if you are planning to hold for atleast 3 more yrs.

5 Likes

My only reason for holding is the potential growth in coming years. Near term, I’m looking at about 150-200 by Dec-24. I don’t have a long term price target, as I want to keep holding it forever, with the hope that bank starts giving some dividend in next couple of years.

Even if we take a pessimistic view of just 8% QoQ growth in Net Profit (half of average 17% for last 6 quarters), it easily translates to minimum 1 rupee increase in EPS every year, and thus minimum 20 rupees per year increase in price (assuming long term PE range of 18-20). Obviously, one has to always remember the famous saying that market can remain irrational for an extended period of time. Having said that, I feel that the bank surely seems to be capable of giving numbers much bigger than my assumptions.

Looking forward to hear critical thoughts about this calculation from experts in this forum. Thanks!

the best banks are trading at 3x BV approx, why IDFC bank would trade at say 4-4.5x ? just keep excel away while counting future returns.

Its already 3.5x for me and holding and I would expect 20% cagr over next 4-5 years . if it reached 150 in next 12 months I would exit .

1 Like

In HDFC times, their main competition was lazy PSU banks, hence they were having an easy market to capture. Now its very competitive. But I think, if we want a fast growing bank and still conservative approach, then this is good option. And I dont understand the selling part. We are in India. And indian market is 25% financials. If we want our money to be invested in market, then we have to be invested in this bank. Otherwise by selling this bank, where will we go? Do we plan to invest in chinese banks, on a lighter note…

6 Likes

If we go from BV side, then there is approx. 3% increase in last few quarters (except one outlier of 6.8% in Mar-23). Reverse merger will enhance it by 5% and QIP would probably offset it in equal weightage, so almost net zero impact from these two events. From that calculation as well, the BV goes to around 48-49 by Dec-24. Considering 3xBV, price again comes close to 150.

1 Like

QIP will increase the BV as it may happen at 2.25x book value…

Book value can reach 52-53 by the end of F.Y. 25 if we consider the profits of 7 quaters along with merger and QIP…

3 Likes

IMO it is a long term story. Best is yet to come. Legacy high rate borrowings will get replaced with low cost funds, c/i ratio is going to come down in next two to three years, credit card business will also start contributing to bottom line, NIM of 5.5 to 6%(which is very rare in other banks) is likely to continue as repeatedly promised by Mr VV, net NPA around 1% and growth of 25 % … All these factors are likely to re rate the bank in the future . So holding for the long term without bothering for ups and downs and consolidation etc.

3 Likes

I partially agree with your point but partially have different view.

I do not believe we HAVE TO invest in financial stocks just because financials form large part of our index / total mcap. My personal belief is invest where we can make money. Please note I have nothing personal against this bank. I am part owner too ![]()

I agree finance is big part but banks are looking lucrative only because of all the deleveraging that has happened post covid shock. All the banks have strong balance sheets. Corporates have reduced debt considerably (at the cost of low private capex). Now when the private capex pick up, bank will lend more and there will be growth. But for how long? 3 yrs? 5 yrs? Some day the party will stop. Its a cycle.

I find this statement very optimist for the reason mentioned above. Past 3 yrs went in balance sheet cleaning (for banks and corporates). Government did all the heavy capex. Private will pick up (may be post elections). So there can be growth for next 2-3 yrs. but the competition is equally intense. Currently, the bank is strongly placed to make the most of coming growth but future is uncertain. Its hard to decide right now to hold it for decades (my personal view).

Can you please suggest how did you calculate this BV ratio? according to me, current multiple is 2.4 (price 94 / bv 39).

by giving this multiple, you are placing the bank in the leagues of HDFC & ICICI & Kotak. ![]()

I agree with all these triggers. But don’t you think rerating has already happened? I believe price has run up the fundamentals. Now bank will have to deliver on all these parameters to ensure the current multiples sustain.

Once again: Nothing against the bank. I have invested in it too. All I am saying is be extra cautious. Borrowing analogy from @Worldlywiseinvestors , we are riding a tiger here. tightly pakad ke rakhna.

3 Likes

1 Like

But why do it before Q2/H1 results? Do they have something to fear?

1 Like

Visited a local branch in Nagpur today. Sharing below insights after spending a good one hour interacting with the local customer experience manager -

-

Work culture - two of the employees I interacted with were Ex Axis and Standard Charted who joined the bank in last two years and said this bank relatively has a relaxed work culture. There is no pressure to cross sell products that customers don’t want. Particularly insurance is something other banks pushes very hard to sell and it often creates a bad experiences with the customer.

-

branch performance- the specific branch crossed 104 cr in CASA and per their estimate should easily add 100 cr by another year. The newest branch in town that was opened earlier this year, breakeven in 4 months. Their is a pull demand for multiple loans and one of the key competitive reason is bank offers a higher limit loan than the standard limit one would get from the competitive bank. This is for the secured loans.

They did acknowledge the practice of requesting customers to do transfer before the month end like every other bank , however also confirmed that customers have been sticky with their deposits. -

it was evident that they admire the leadership of Mr. Vaidyanathan and the simplicity in his conduct.

Thank you,

Ram

27 Likes

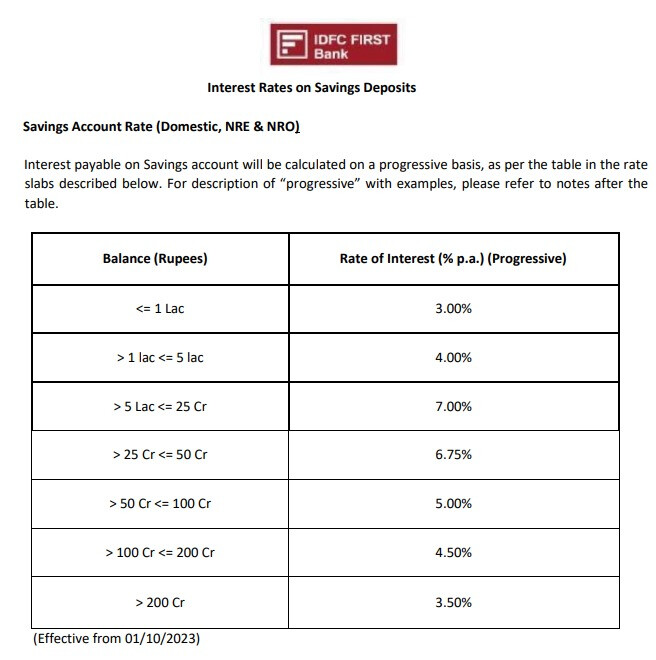

It seems that there is a strong need for funds. They have also increased the interest rates for savings bank deposits above 5L. Previously this threshold was 10L.

1 Like

But have decreased under 1L from 4% to 3%? This is where all the savings will come from.

And most people are keeping under 5L only so interest savings for bank

1 Like

The floor price of the QIP issue is Rs 94.95/- per share. The bank can offer a max of 5% discount. I.e floor price can be reduced to INR 90.20/- based on the market situation. I think this is the reason for correction today.

On a positive note,

CARE has upgraded the existing rating of the Bank’s long-term debt instruments amounting to ₹ 1,874.68 crore from ‘CARE AA / Stable’ to ‘CARE AA+ / Stable’. This is a positive update for the company.

3 Likes

Can anyone throw some light on why the futures contracts are trading at deep discounts? Is this QIP effect or some other reason?

Definitely…One of their employee was requesting me near September end to add more funds in savings account…And today I looked at one of his colleague’s whatsapp status where they are enjoying probably a bank sponsored trip in Europe ![]()

![]()

3 Likes

Setting tough goals and then rewarding the concerned employees is (IMHO) one of the best and a very inexpensive way to grow business. Unlike increments, foreign trips are one time expense and enable employees to have greater exposure, social/ cultural education, broader world view and higher self confidence. It makes the high performance employees more motivated. Shareholders should welcome such a policy as long as it is well designed and correctly targeted.

4 Likes