Book value post merger would increase by 4.9% post merger. Exact number shall be known at that time basis prevailing BV.

Did quick Back of Envelope calculations:

Current # shares : 705 cr

Post merger # of shares : 670 cr (on like to like basis)

Current SH’s fund : 30,700 cr.

Projected SH’s fund : 35,785 cr.

Increase in SH’s fund in Q2’24 is ~Rs 1100 cr (w/o equity dilution)

Around 15-16 crore shares will get extinguished at the time of merger, so number of existing shares of the bank after merger will be around 690 crores and not 670 crores…

If we consider shareholders fund of 30700 crores and reduction of shares by 16 crores then that will raise BV per share from 43.5 to 44.5 i.e. 1 rs…rest of the 9 rs. will need to come from profits…adding 9 rs. in next 12 months seems impossible considering flat QoQ performance…

Did the maths, q on q numbers on growth metrics are also very strong which is the main thing. The main thing to watch out is A. Whether deposits are rising. B. Whether loan book growth is sustained. C. Whether asset quality numbers are maintained. Rest all matters like pbt pat etc. fall into place automatically. So could be for other reasons.

On a separate note, the concern I have is lack of growth. Other banks seem to be growing much better. Even large private sector banks 7 times rhe size are growing at 20%, this bank is stuck at 25%. Expect better than this for an early stage bank.

The loan book has increased by Rs 10,000+ cr QonQ. The NIM % is maintained at 6.32%. Provisions have increased marginally in-line with the loan book. Still, I wonder why the pre-operative profit has not increased? Any idea?

If I see the segmental results, the treasury income has dropped significantly from Rs 203 cr to Rs 89 cr, QonQ. This seem to have affected the profit numbers. Any idea what this constitutes and reason for such a sharp drop? Is it going to be lumpy or unpredictable in future? I believe a person who knows the banking industry can explain it.

Otherwise the numbers are as expected. Faster growth is desired, but without sacrificing the quality of loan book.

On growth, what i understand is that the bank is still cautious in a increasing lending especially on corporate loan book. I’m waiting for the investor call.

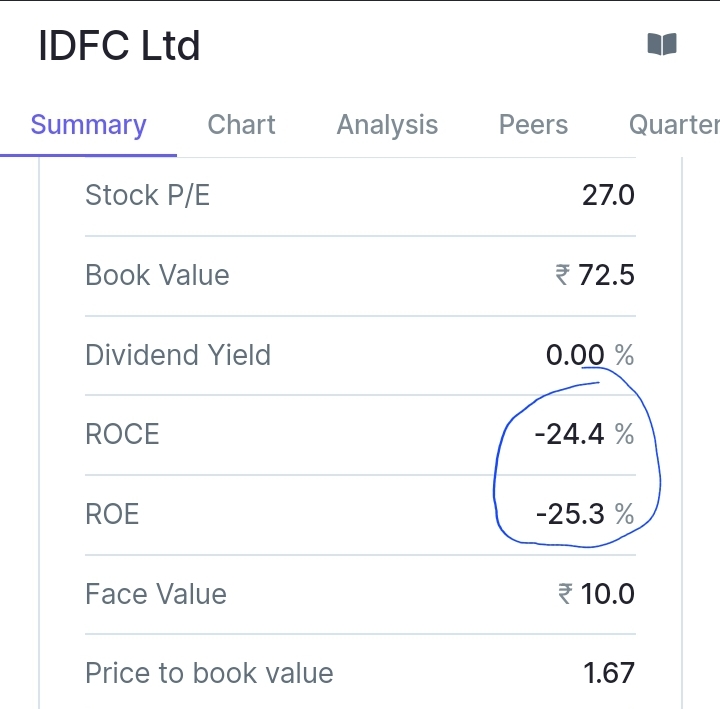

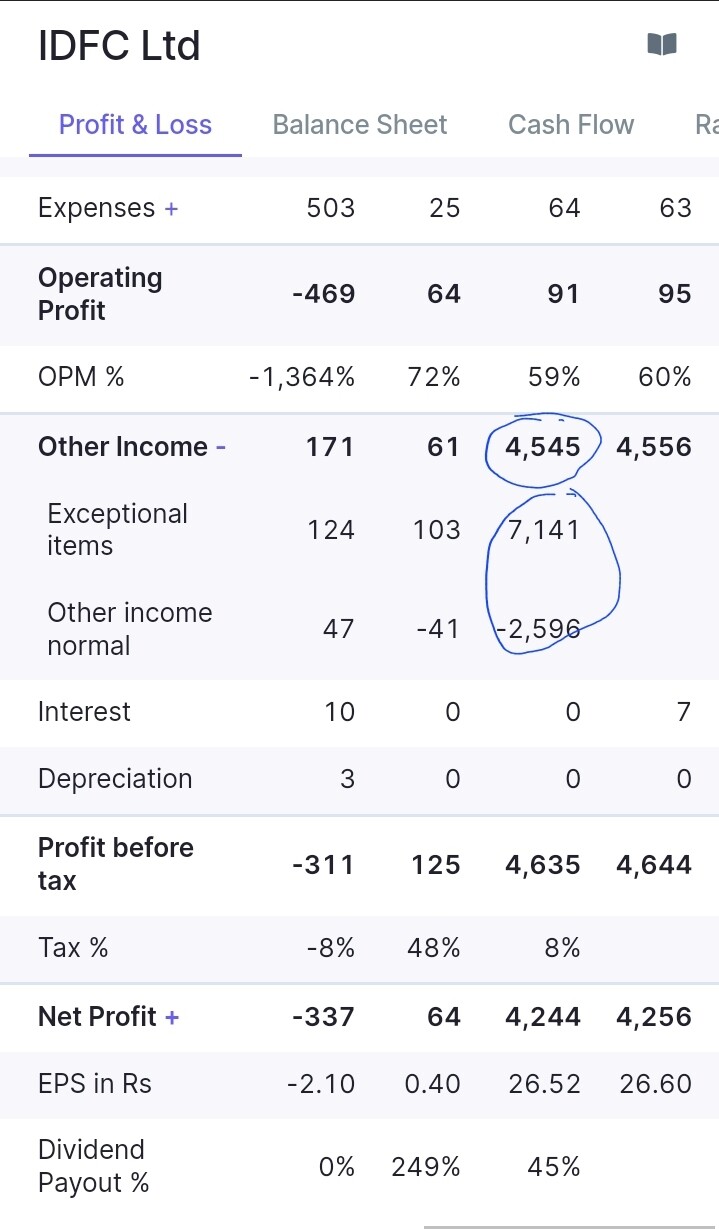

How will ROE increase post merger? i.e considering current ROE is lower/negative for IDFC, won’t it pull down ROE of IDFC First? ROE is negative if the exceptional income is removed! Not sure of its continuity YOY. Pls correct me if my assumption is wrong.

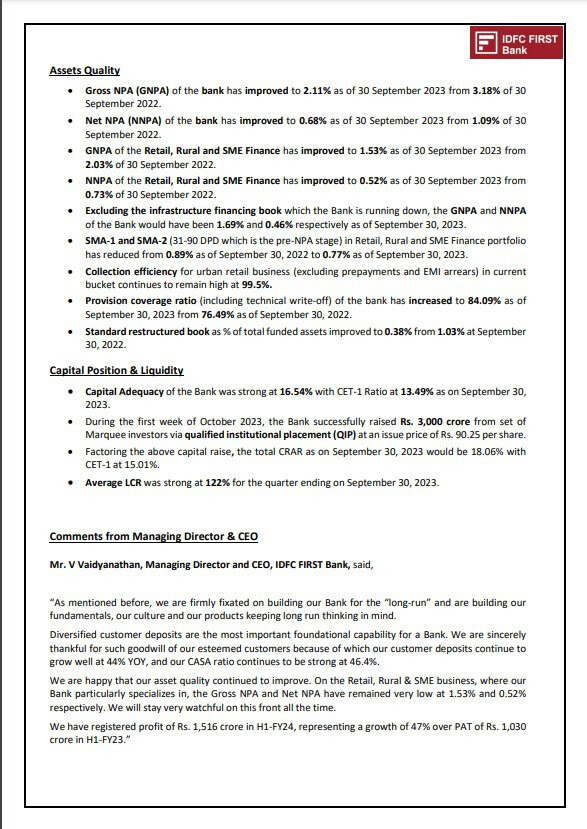

The key takeaways from the provided information about IDFC FIRST Bank Limited’s financial results and performance for the quarter and half year ended September 30, 2023, are as follows:

Profitability:

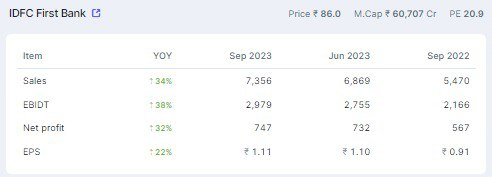

Net Profit for Q2-FY24 increased by 35% year-on-year (YoY), from Rs. 556 crore in Q2-FY23 to Rs. 751 crore in Q2-FY24, driven by strong growth in core operating income.

ROE of IDFC F Bank increase has no link with IDFC Ltd’s merger. Since IDFC’s entity shall get extinguished, it’s ROE angle doesn’t impact that of bank.

My hypothesis is : ROE of the bank shall improve going forward basis the following:

Operational leverage kicking (26% of branches opened in last 18 months)

Focus on Guidance of FY’25’s Cost to Income ratio target

Wow! I am amazed at the amount of interest the esteemed forum members here have in IDFC First Bank.

Read the Q2 investor presentation now and most of the metrics (except two) looked fine to me. The two that did not are the CASA ratio and the Cost-to-Income ratio. Now while I am no finance virtuoso, the deterioration in either of those two metrics to me did not seem remarkable as such. So all in all, a fine result set. I must also admit that the transparency of the leadership of the bank is a case study in itself. Loved it!

Edit: In addition to this, I would also love to share a recent personal experience with IDFC First Bank.

I called their UK Toll-Free number today (on 30-Oct) as I wanted to understand their process to open an NRO/NRE account. I was pleasantly surprised with the simplicity on the documentation side and with the fact that they also offered me a doorstep collection of the said documents from my UK residence. This is a dream for an expat considering the toil most other Indian banks (including private sector) makes us endure in both these areas (at least in the UK). I will try to update this part of the comment as I undergo the process and have more useful information to share.

In Q2FY24, IDFC First incurred operating expenses of ~2700 Cr. ICICI Bank has around 8-9x number branches and incurred opex of ~6000 Cr in Q2FY24. I suspect a large portion of IDFC First’s operating expenses pertain to very high commission paid to intermediaries to aggressively push for loan origination. There may not be high operating leverage benefit as these commissions are variable cost.

How come no analyst asked this question? The data has been available since the last 3-4 days

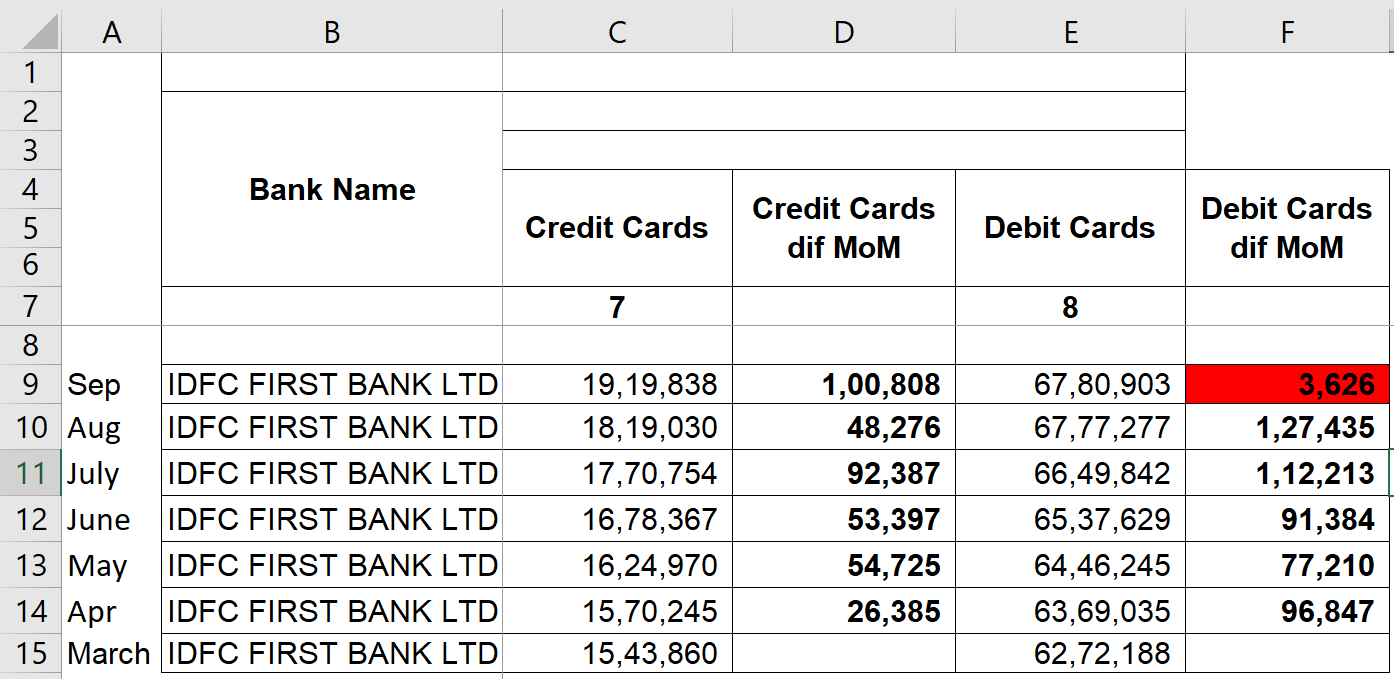

The bank boasts a healthy CASA base, but then why in Sep 2023 only 3K new Debit Cards were issued?

Did the bank face a lot of account closures in Sep and hence net addition is low, or New Account Opening has slowed down significantly?

One of the analysts did ask about it indirectly. His question was regarding the customer acquisition numbers per quarter.

Vaidya responded that in the previous quarter, the acquisition rate was about 1.5 lakhs per month, which has now dropped to 70-80k per month. The bank is focusing on acquiring quality customers who maintain balances with the bank, rather than amassing millions of customers. This approach prevents overcrowding in the bank and ensures a positive experience for existing customers.

For sure , but its more about the time horizon. In the long run (approx 3 years or more) Vaidyanathan has given a guidance of high teens in terms of ROE(~17%, could be even higher considering his general conservative nature) . So if you look at the long term the price is still reasonable.

Banks like HDFC and ICICI are stable banks and ROE can not increase further from here. So short to medium term they look more value for money. But in the long term I still think IDFC will provide better returns.

i agree with the bank policy if they are trying to create a niche for customers of certain profile. It is not possible for a bank to service their customers well if they try to provide all services to every customer coming through the door. Every bank should first decide on its customer range then only it can design its products and delivery system to ensure proper co-relation between income and cost.

IDFCFB has already decided that it will not touch Infra customers and only 15% to 20% loan book for wholesale customers. The retail customers have already been segmented and being fine tuned as they go forward. I am invested since 2018 and I feel the bank should give superior returns for next three years and then settle down for normal growth as per their competency.

Hi I’d bought IDFC first Bank for an average of 93. Now it’s 83. Now I realise I should have gone for IDFC Ltd instead, due to the merger. Does it make sense to sell IDFC first Bank at loss now and buy IDFC Ltd which is also available at a reduced 114 now?

I’m quite new here. Thanks

There is an arbitrage of 10-11% if you buy IDFC Ltd. If you are a medium- long term it makes sense if you buy IDFC Ltd and wait for the arbitrage to vanish. But you need to be patient

Risk: If IDFC first bank corrects, IDFC ltd may also correct. You need to keep this in mind.