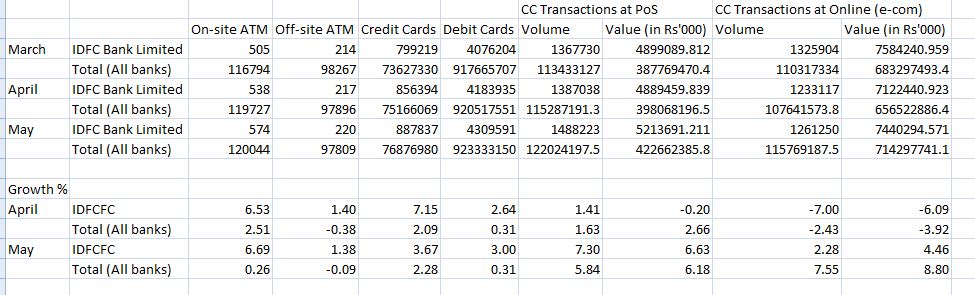

Credit card data for March, April and May is compiled and is given below.

4 Likes

As compared to March 2022 number wise credit card growth seems to be slowed down in May 2022.

I think some points in this post needs to be corrected

The Basel-Pillar 3 disclosures made quarterly cover a broad range of risk based disclosures. The specific disclosure you are referring to is to measure the risk arising out of asset liability duration and rate mis-matches. It is not sensitivity to the govt bond portfolio.

Banks being in the business of borrowing funds to lend out, have a risk of timing and amount mis-matches of their assets and liabilities. If, say, their deposit maturity profile matches exactly with their lending profile, then the world is ideal - the spread just beautifully falls into the bank’s profit lap. Reality is unfortunately not as kind. For instance banks may borrow / get deposits that mature sooner than their lending matures. If such is the case, then the bank needs to find other ways to fund maturing deposits/ borrowings than solely from its lending and while it can refinance, it runs risks of changes in interest rates and spread. So is the reverse case where banks liabilities stretch out longer than their assets (this is quite a risky situation).

These are risks that the bank needs to manage (called ALM risks - asset liability management), and is managed via Asset-Liability Committees. To help know these risks, measures were introduced called Traditional Gap Analysis and Duration Gap Analysis. They are quite simple. A bank puts out all maturing assets and liabilities in specific time buckets (maturing in 1 day, 2-7 days,…3-5 years, >5years) and a positive or negative gap of A-L would give an indication of the gap in every bucket. If it is positive then there are risks associated with repricing the asset and if it is negative then there are risks associated with funding the liability, in each time bucket. Changes in interest rates amplifies these risks. And we need to remember there is an interest rate for every duration; overnight rates are different from 3 month to 1 year etc, and these interest rates plotted over the duration of the asset is a curve and is called an yield curve for Govt (i.e risk free) assets of such duration. Now if assets and liabilities are of different maturity then they are at different points on the yield curve (adjusted for risks).

A shift in the yield curve, esp suddenly can create unforeseen risks for the bank and for the system (Lehman was unable to roll-over its papers). This risk is captured via Traditional Gap Analysis, which says how much of Earnings is at Risk if the yield curve moves up or down; and Duration Gap Analysis, which adjusts these risks for time value of money and says how much of net worth is at risk (fancily called Economic Value of Equity) for such movements.

This is done for the whole book of the bank and not just a govt portfolio (termed as Interest Rate Risk in the Banking Book).

Separately it cannot be seen that ‘the bank has been shifting monies to rbi repo’ based on these disclosures. To be clear repo is a borrowing mechanism and not an investing mechanism used by the bank, generally for short term liquidity management. The bank has to provide high grade collateral, which by itself the bank will not have much of (maybe to the extent of SLR). Reverse repo is an investing mechanism, where the bank can park funds with RBI as rates (obviously) lower than repo rate. At heights of Covid banks were seen parking substantial sums as rever repo with RBI.

This is perfect. There is however a negative as well, which a good banker will always keep in mind. Rising NIMs with rising borrowing costs will impact both, credit quality and credit demand negatively. The bank’s existing book can deteriorate at the margin, and new book can be slow to come by.

I once had the great fortune of meeting someone senior from India’s foremost financial institution. He said ‘credit is not about lending, anybody can, it’s about collecting’. Keeping this in mind brings a certain attitude towards risks always present in a bank.

27 Likes

They’re quietly working on building the bank’s own network for collection - MyFIRST Partner SmartCollect. There’s also a mature referral network now with more than a million downloads. With enough data this can also help ensure quality of new borrowers remains consistent - by rewarding people who consistently refer quality borrowers and by penalizing others who don’t (pay them less per referral).

Both of these apps were introduced post covid and seem to be very successful. Digitizing processes like this early on will go a long way in reducing opex long term.

They also seem to be planning to go big on education loans - IDFC FIRST Uni. Released only couple days ago, just saw this as I was looking up the other apps. App itself is snappy and has lots of features for students! I would encourage everyone to download and check it out yourself, there is no need to sign up.

12 Likes

Credit Card spends were expected to slow down as their co-braned partners are shifting away from them especially ONE card.

With new regulations on Fintechs credit card sector is bound to have disruption with advantage banks.

If you get time check out debit card data with similar comparision on spends.

The have stated to charging debit card charges and will be interesting to see how it affects the spends.

IDFC bank gets into agreement with STAR for selling insurance policies

2 Likes

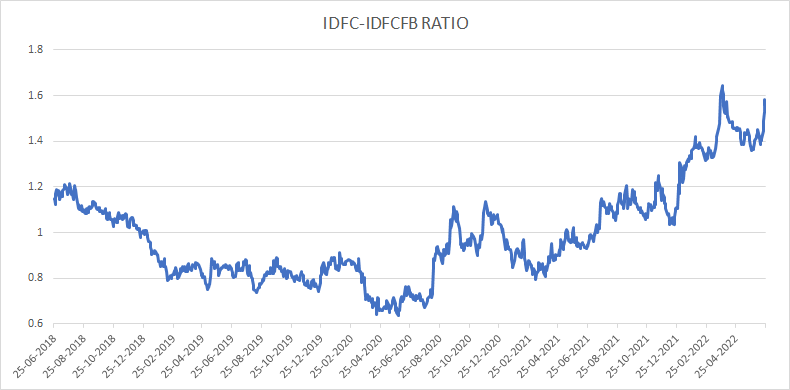

IDFC - IDFCB ratio currently close to the highest its been at 1.6x. Historically this has been a good time to switch from IDFC Ltd to IDFCB.

3 Likes

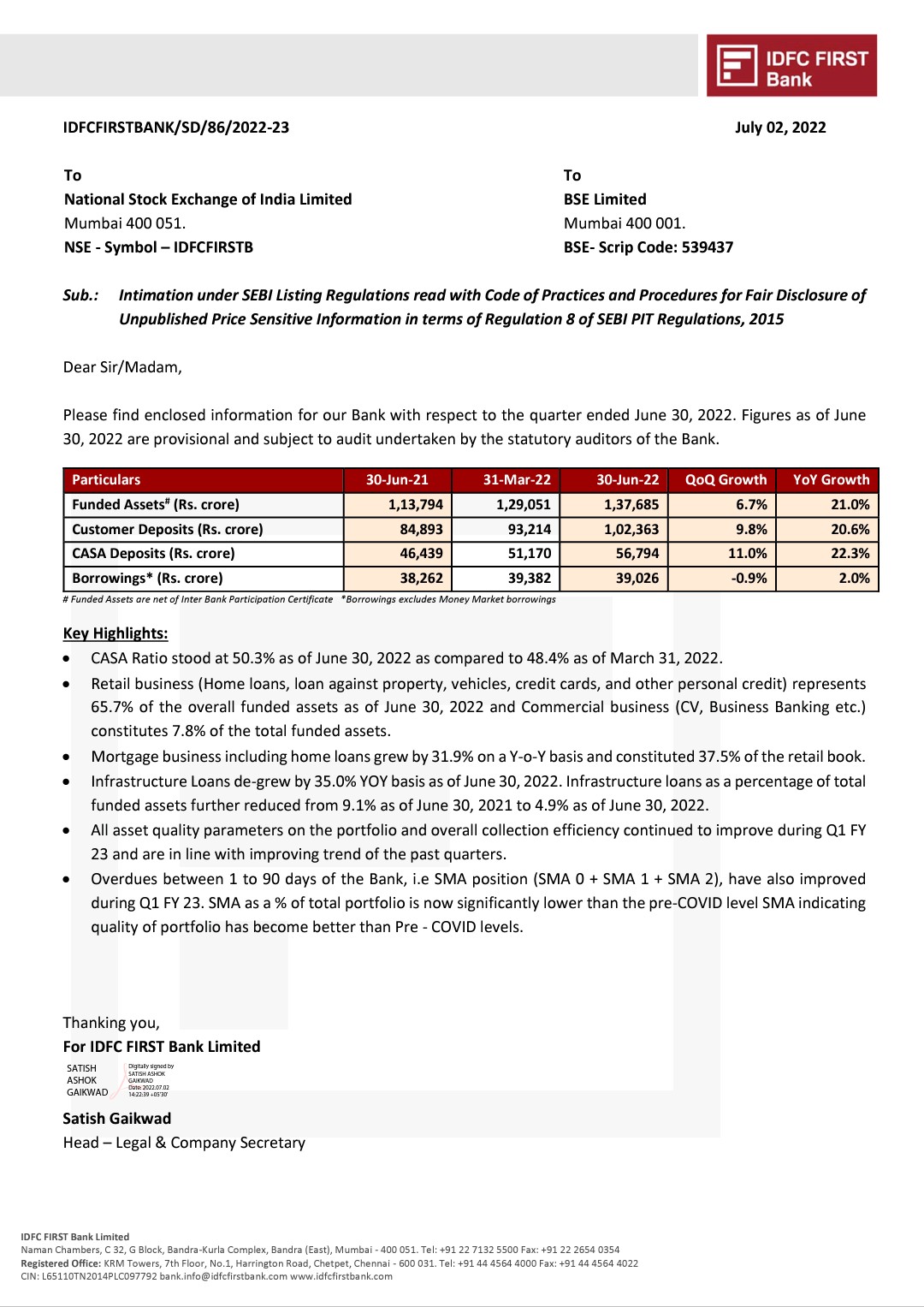

Q1FY23 Results to be announced on July 30th, 2022.

https://www.bseindia.com/xml-data/corpfiling/AttachLive/e617447c-2005-4fb8-a0ac-deaf4200b98d.pdf

Credit Rating released. Worth look into it. Gives insight about interest rate and NCD maturity.

72507c61-3dc6-4c50-8e1c-1490beb60d66.pdf (1020.2 KB)

4 Likes

If we keep aside the merger, macro economic threats, etc , core business of the bank is progressing well. Consistency in CASA , increasing retail loans and now good news that the SMA is lower than pre covid level. Eager to know how it is progressing on profitability parameters now.

5 Likes

Growth in funded assets is in line with expectations. I also expect profits to be in line with expectations set as such by the commentary in last Quarter:

Due to three specific factors (a) legacy high-cost liabilities, (b) retail branch/ ATM/ liabilites set up expenses, and (c) set up of credit

cards, there is a net profit impact of ~ Rs. 500 crores/ quarter. This is reducing every quarter.

It will take a good year for the effect to start showing. Or at least three more quarters. Till then, it’s best to keep low expectations from the stock price, and very high expectations from the management.

Note how we early investors are showing patience with the stock price. During Covid it was provisioning after provisioning every quarter that kept the net profit subdued, and now it’s operation costs.

I mean to highlight this because there are other big investors that are attached with the stock who have voting rights and will want the reverse merger to go a certain way.

10 Likes

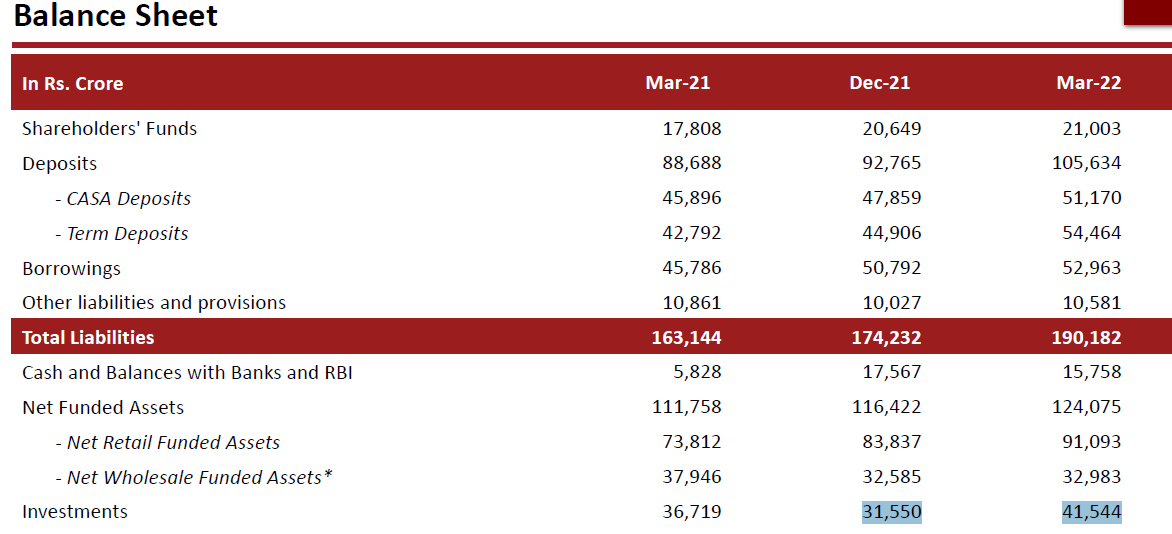

The growth in assets QOQ is decent even if it’s lower than last quarter, however the big issue this quarter is the hit the bank will take on their Treasury book due to the increase in bond yields. The 10Y Gsec has moved up by around 60bps in this quarter alone which is an 8.5% move. This is more than close to double of what it moved last quarter and IDFCB had reported a loss of Rs 9 crores in Q4 on account of this. IDFCB has an investment book of Rs 40,000cr and a further investment of close to Rs 20,000cr in NCD’S etc. That’s a total of Rs 60,000cr that will be impacted. Now all bonds don’t need to be MTM but even if we assume that half the holdings need to be then even a 2-3% hit on that book of Rs 30,000cr will mean a loss of Rs 600-900cr. That’s massive for IDFCB as its PBT is just around 450cr before accounting for any trading losses. So my question is are we looking at another loss generating quarter for IDFCB? If bond yields move up to 8% this quarter as predicted by many economists then will we have another loss in Q2? The losses are notional yes but it impacts the reported profitability and if the first half of the year is a total washout earnings wise then we are looking at a low single digit ROE for FY23 as well. I am a long term bull on IDFCB but every year seems to throw up a new surprise, and frankly I find it hard to justify even a 1x P/B multiple for a low single digit ROE Bank in the current market.

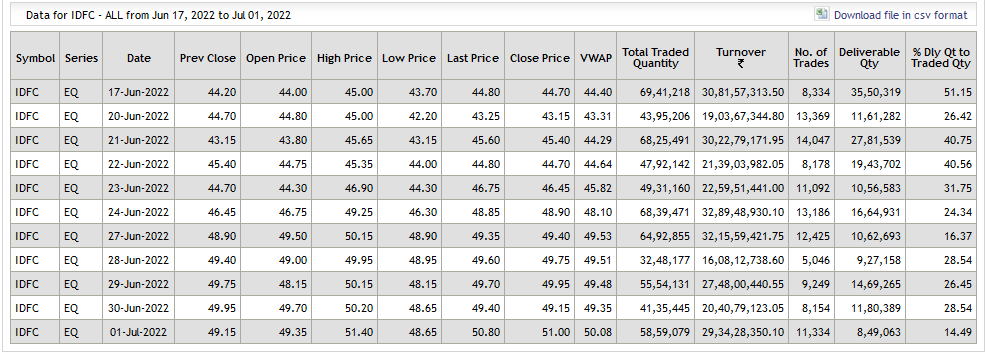

I have all my exposure to IDFCB via IDFC and I am going to use the current 20% appreciation in the IDFC stock to reduce my exposure by 50% and move into cash until more clarity emerges on the earnings. As mentioned by @Puch above the IDFC-IDFCB ratio has moved to 1.6x, which is at top end of the range and considerably reduces our margin of safety. At best the merger ratio will be at 1.8x but even that is a good 18 months away and I am worried that the AMC deal might collapse as market conditions have changed significantly. At a 1.6x multiple I don’t feel the margin of saftety is sufficient and I am happy to wait on the sidelines for a better entry price. Lastly if you see the current delivery data on IDFC then you will see that it’s the lowest its ever been at just 14% on Friday. This means that the increase in the price currently is being driven not by long term buying but by day traders. The stock is up by 22% in just 10 days and close to my average price, so will utilize this opportunity to reduce my exposure.

Edit: Added delivery data below-

Edit 2: IDFC-IDFCB ratio-

7 Likes

My thoughts are exactly the same… i can’t see the sorry face of vaidyanathan again… first dhfl then Vodafone then COVID now the rise in bond yields… seems the bank ROE will improve only in the year 2024 or 2025 untill and unless they pull off something miraculous. and there is no permission from RBI to spread the MTM losses like they allowed the banks last time when the bond yields spiked. Seems another disappointing quarter for the bank.

2 Likes

Any idea if IDFCF has IFR provisions that can be used to offset the (notional) losses? Also banks have been asking RBI to spread this over the entire year.

Waiting for the latest annual report to be released so that one can verify if and how many reserves are there or already utilized in FY22.

“Its best to keep low expectations from the stock and very high expectations from management”. I find this truly funny, i couldnt help laughing! It’s a very original line too. Its amazing how people are really supporting this management despite losses and losses since merger. Dont forget, for one reason or the other, Dewan housing (600 cr), reliance capital (1500 cr), Vodafone (3300 cr), DTA (~700 cr), Goodwill accounting (~1600 cr), multiple infra accounts, COVID etc etc the management has been posting losses. Book value has come down, plain and simple. Yet everyone has “very high expectations from management”… wow!

Depositors increase deposits 6-7X, investors give them Rs. 5000 crores of capital, debt guys give them Tier 2… I find it fascinating that they keep posting losses and we people keep supporting. Never seen anything in my life like this before.

7 Likes

The reasons you listed are very valid. But it’s also reasonable to ask who is responsible for all those accounts. Are those loans given by the present management or the erstwhile idfc bank. For any reasonable mind it is not hard to find wheather management is genuinely focussing on improving business or not. Once all these issues sorted out bank will post profits.l

13 Likes

So firstly, the assumption that the bank may have to take a 2-3% hit on its entire 30000 cr gsec portfolio is entirely wrong. Any bank holds bonds in 3 categories which are HTM, AFS and HFT. Only securities held in the HFT category require MTM provisioning.

To give you some empirical evidence, 10 year gsec yield moved from 6.45% to 6.84%(total 39 bps)from 31st Dec,2021 to 31st March, 2022, yet the bank posted a trading loss of only 25 crs. In the current quarter the yields have moved from 6.84% to 7.45%(total 61 bps). The bank has been consciously reducing the HFT portfolio in anticipation of a rising interest rate scenario. From the above data, in my view the bank can make a loss of 45-55 crs in Q1 instead of 25 crs made in Q4. Please do let me know if I am missing something here

16 Likes

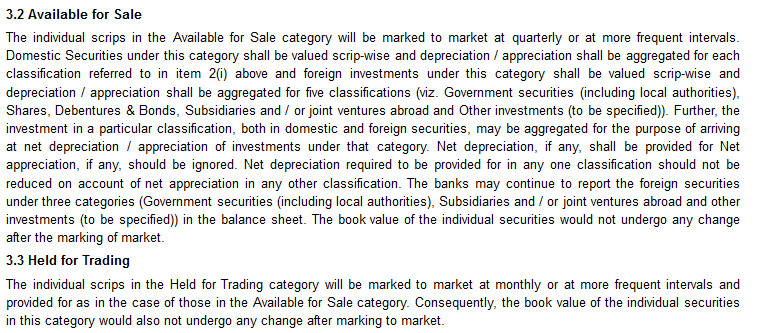

This is incorrect MTM provisions are required for HFT and AFS securities, see below from the RBI website-

Secondly I have only taken 50% or 30,000cr of their total holdings so there is enough margin of safety.

Please provide a source for this info, as per their last presentation their investments went up by 10,000cr from 30,000cr to 40,000cr-

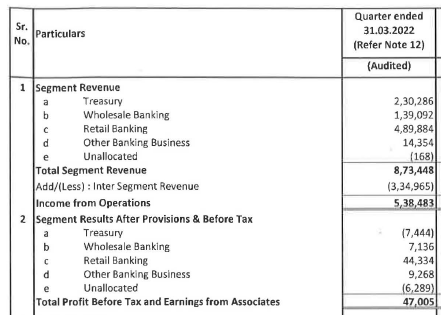

Treasury losses were 75cr in Q4FY22

This loss is after accounting for the yield/income from investments. So for example say they had income on investments of Rs 300cr in Q4FY22, MTM losses were Rs 375cr for a net loss of Rs 75cr from the Treasury segment. Now in Q1FY23 if income stays the same but MTM losses double to Rs 750cr then we will have a net loss from the Treasury segment of Rs 450cr.

9 Likes