Might there be some hope of an Investment Fluctuation Reserve amount to offset some of these losses?

There were net profits in past two fiscals.

Disc: invested

Might there be some hope of an Investment Fluctuation Reserve amount to offset some of these losses?

There were net profits in past two fiscals.

Disc: invested

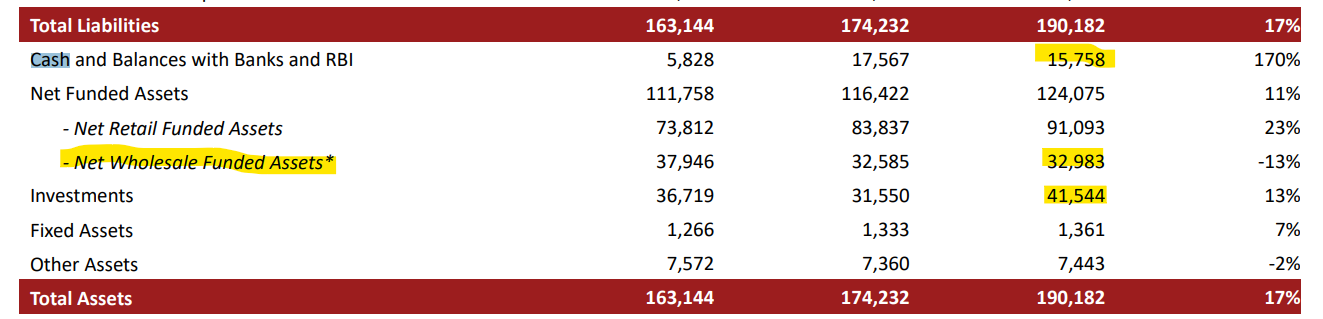

So, the balancesheet of the bank states that they have a 15758 crs balance with banks and RBI which really does not have any risk of interest rate fluctuations as it is mostly call money or with very short maturity.

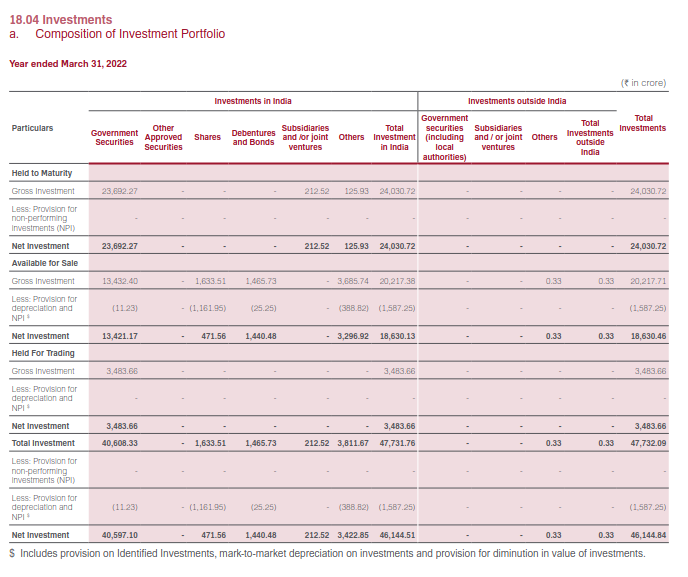

On your point that the investments in Gsecs has increased from Rs 31550 crs to 41554 crs QoQ, it is very important to see the maturity profile of this investment to understand the interest rate risk. Please check the maturity profile in the basel-III disclosure as on 31st March-2022 as given below:

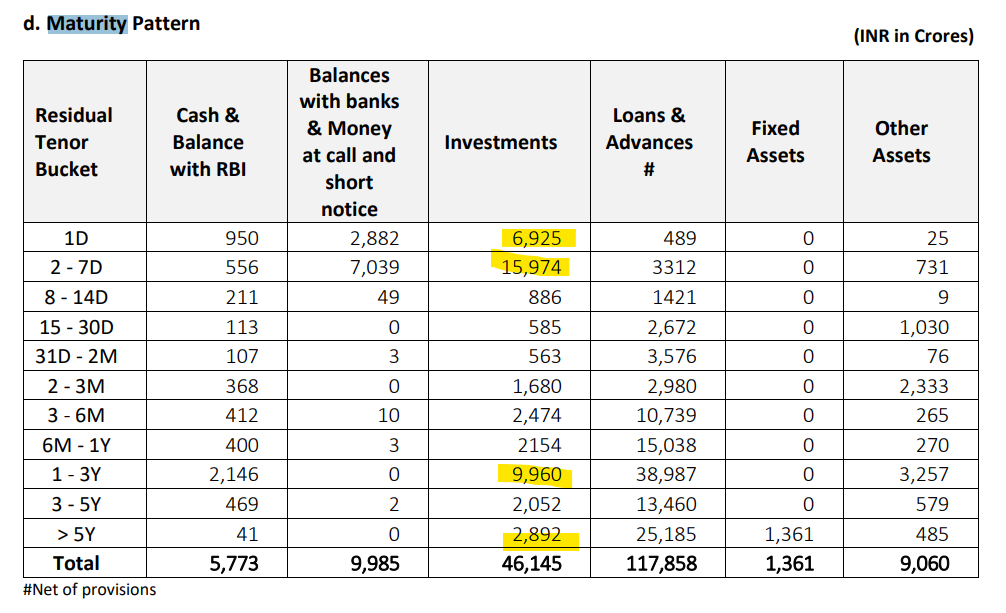

The amount of Rs 46145 crs includes Gsecs and investments in NCDs of corporates. Investments in Gsecs from the balancesheet of March-22 is Rs 41544 crs and the rest out of Rs 46145 crs(which is Rs 4601 crs) is investments in NCDs which are held to maturity. The amount in Gsces is highly in favour of ultra-short term maturity papers with more than half of it (Rs 22899 crs) parked in gsecs maturing within 7 days which carries no interest rate risk. Only Rs 2892 crs of investments are held in bonds having a maturity of more than 5 years and this too may include NCDs which are held till maturity.

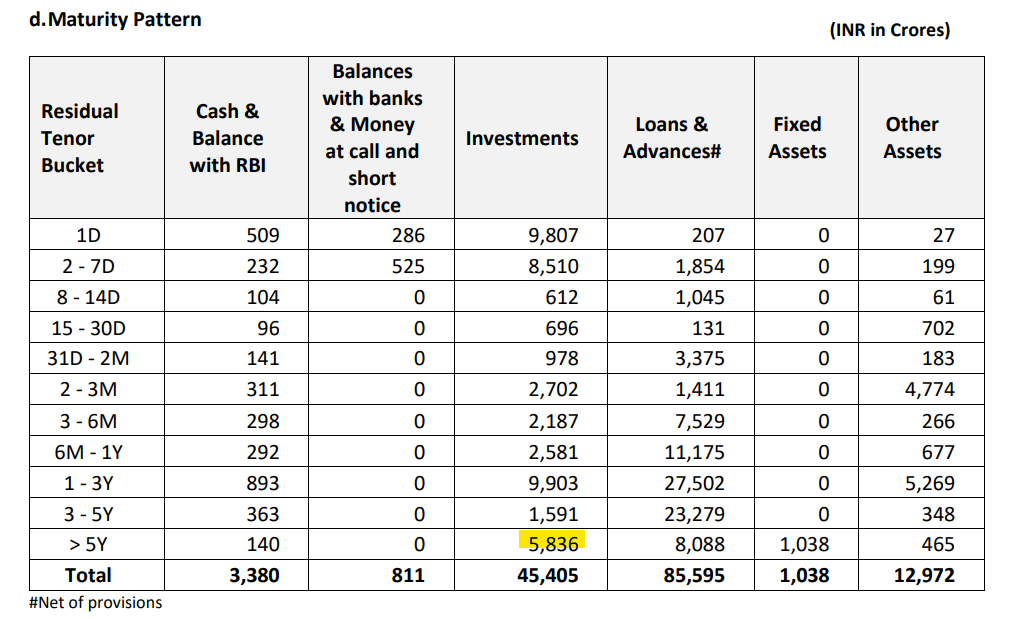

If you see the basel-III disclosure of March-2020, you will see the following:

So, in the last two years from Mar-20 to Mar-22, even though the balancesheet size has grown from Rs 149,200 crs to 1,90,500 crs, the management has very prudently reduced the maturity profile of gsecs anticipating a rising interest rate environment.

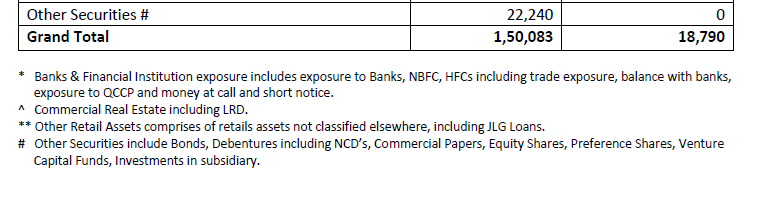

I don’t think this is accurate, RBI has very specific rules for what securities can be carried in the Investments book. The Basel 3 document shows that there are other securities of roughly 20,000cr most of which I suspect are bonds and debentures and shown under Other Assets + Loans & Advances in your table-

Not sure one can say that the NCD’s are HTM. RBI again has strict rules for what securities can be carried in the HTM category and its limited to 25% of the investment book. There are ofcourse certain exclusions to this rule but in my experience most banks don’t exceed 30% in most cases.

The detailed guidelines are here Reserve Bank of India - Master Directions and its almost impossible for an outsider to say with any certainity what % of the book needs to be MTM without having access to the detailed balance sheet which is why I had assumed 2-3% hit on the investments + bonds book. Even in your table if we exclude the short term maturity investments and only take the 6M+ investments + other assets its totals upto 22,000cr+. A better approach might be to look at the P&L and see the difference in the Treasury segment results between Q3 (when 10Y bond yields were mostly stable) and Q4 (when bond yields went up by 39bps).

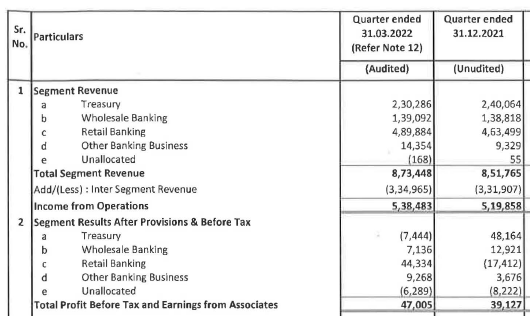

In Q4 the Treasury segment reported losses of Rs 75cr, whereas in Q3 the same segment had reported profits of Rs 481cr, that’s a difference of Rs 550cr. Is all of this due to MTM losses? We can’t be sure but a vast majority of it would be due to MTM losses.

Yes the 10Y bond has moved up by 61bps but the damage in the 5Y, 3Y and 2Y part of the curve has been much more severe. 5Y bonds have moved up by almost 100bps in Q1 vs 5-6bps in Q4. The 3Y has moved up by 91bps in Q1 vs 18bps in Q4.The 2Y has moved up by 120 bps in Q1 vs being flat in Q4. These are 15-20% declines in valuations in a single quarter!

All of this put together explains why the losses could be quite significant on the Treasury book for all the banks including IDFCB. If the MTM hit was say 300cr in Q4 then it can easily be 500-1,000cr+ in Q1; as an IDFCB bull I hope its really not the case but I think it makes sense to move some holdings to cash especially if your exposure is through IDFC Ltd.

See all charts below-

Agree these are all erstwhile IDFC Bank issues. My frustration comes from the fact that as Capital First Shareholder, the value multiplied by 5 or six times, but that the trajectory is not continuing after the merger. Moreover, other peer banks have much better financials in terms of ROA ROE, but they dont seem to enjoy such P/E commensurate to their earnings, or P/B commensurate to their ROE, not they get goodwill and support from everyon. Hence my earlier message.

Hi guys,

Just wanted to ask are the SLR investments also effected due to fluctuation in interest rates or it is just the NON SLR investments which get effected.

Since bank trade heavily in FOREX with good amount of leverage so, during such volatile times when rupee is depreciating at a rapid pace how does it impact the bank and what is the rule position according to RBI for the accounting of profit or loss in this segment.

I would be grateful if somebody can explain this.

thankyou

Hi guys,

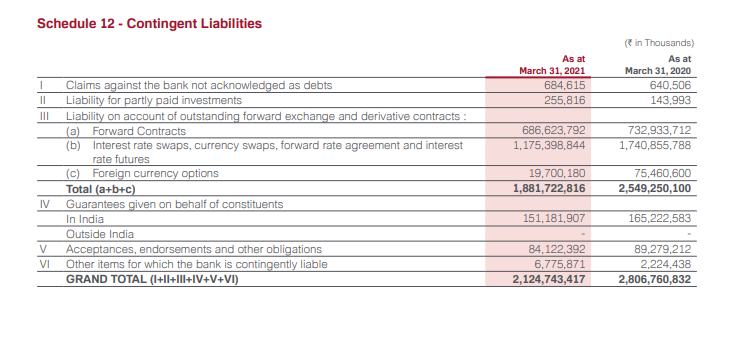

The reason for me to ask the above question is IDFC bank has a contingent liability of 2.14 lakh cr. The definition of contingent liability is a potential liability that may occur in the future does this definition exactly apply to banks. I have also noticed that major part of this contingent liability is forward exchange and derivative contract. So If anybody could explain that during such volatile times is there a possibility that some part of this contingent liability becomes a liability and also what is the rule position according to RBI for the reporting this. At last if somebody could also explain as to why banks take such heavy leveraged position in FOREX which is almost equal to their entire asset.

I am in learning stage and have lot of interest in banking industry. If anybody can spare some of their valuable time in explaining me this it would not only be helpful to me but many more.

Thankyou

Nippon India Arbitrage Fund Growth was the buyer of 20,602,200 shares in Jun 2022 constituting 0.33% of the paid up equity of the company.

Source: trendlyne.com

And Quant was the seller !

Quant entered in IDFCB in April 22 and completely exited in June 22. Quants investment is mostly based on Technical analysis.

Banks do not trade in forex derivatives, its interest rate and currency hedging contracts which they execute on behalf of their clients when they opt for interest rate swaps. This exposure is usually high because for each loan which is getting hedged - the interest rate swap derivative position will have approx 3-4x position.

Also pls note - interest and currency hedging ir prevelant only in corporate loans and small tickets loans are not offered these services.

These contingent liabilities will arise only if client defaults. But not the whole exposure wil become accountable for loss, only mtm gets accounted for loss and usually bank has all rights to execute and cancel swaps if client doesnt pays up.

Just for Info

Idfc first bank has created application for students seeking higher education loans and scholarships.

I think this is a first of its kind and the website looks super clean

Annual Report is out. On first glance looks like there is a lot of information about new initiatives (3000 clients for Cash Management, Wealth Management AUM at 6536 Cr, up 97%) and describes various activities in detail. Also includes many graphs, “Graph 4.3.3: Reducing First EMI bounce rates” is particularly interesting compared to pre-covid.

Lots of growth in the FASTag ecosystem, not sure how I feel about increased focus here. Good for retaining CASA accounts but hopefully they’re able to generate good amount of fees as well from B2B partnerships.

Total employees at 27804 as of March 2022. Median increase in employee remuneration ~10%, but NIL for Vaidyanathan.

Rural banking is growing pretty well.

As on March 31, 2022, the Bank has engaged 10 Corporate

BC partners (including its wholly owned subsidiary IFBL)

and has total 11,522 customer service points, including 601

rural business corrospondent centres, present in 29 States

& UTs. In FY 2021-22, the Bank has opened 4,320 new customer

service points and total of 4 crore transactions were performed valuing 15,220 crore.

Further, the Bank has disbursed 8,625 crore of loans.

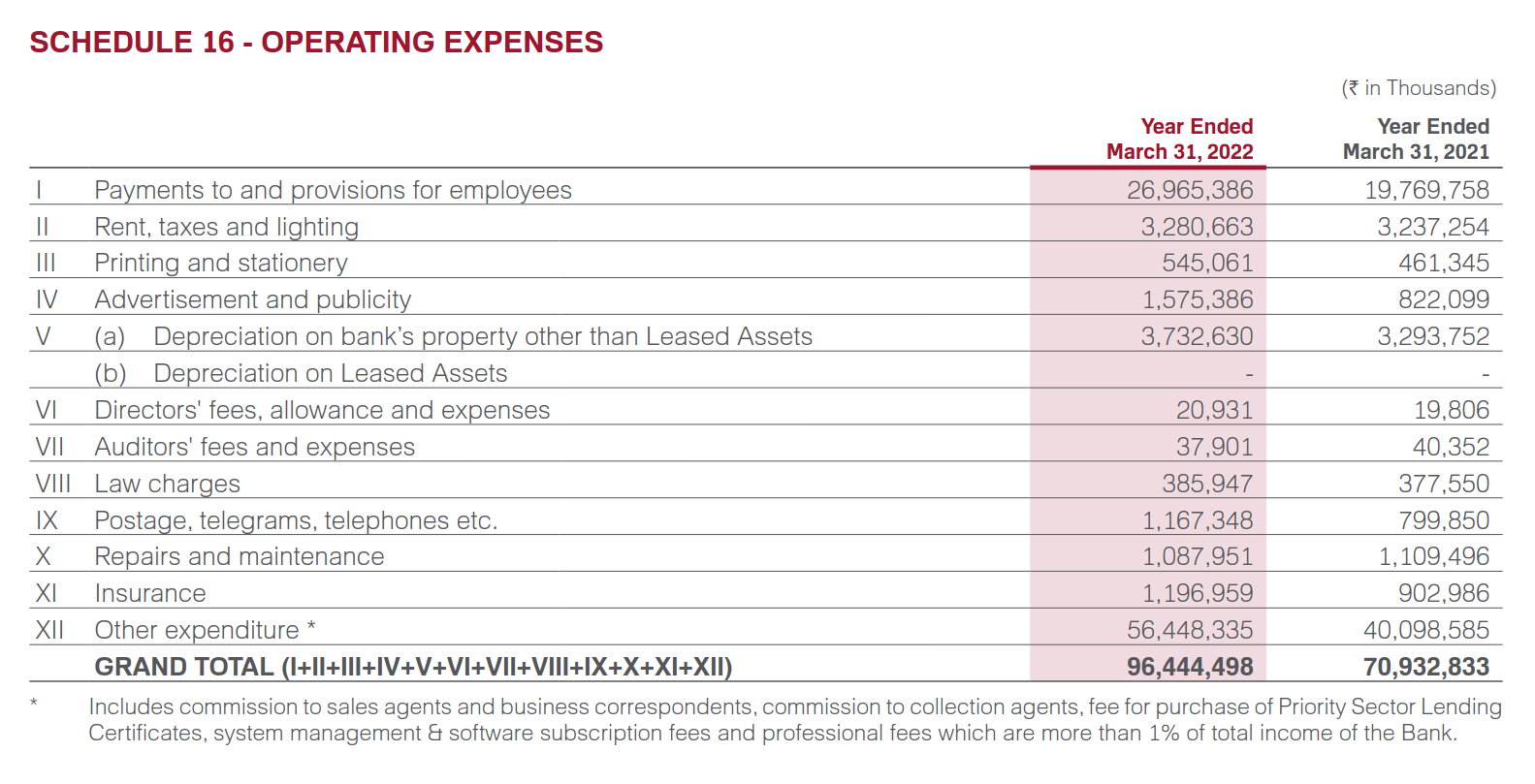

Operating expenses:

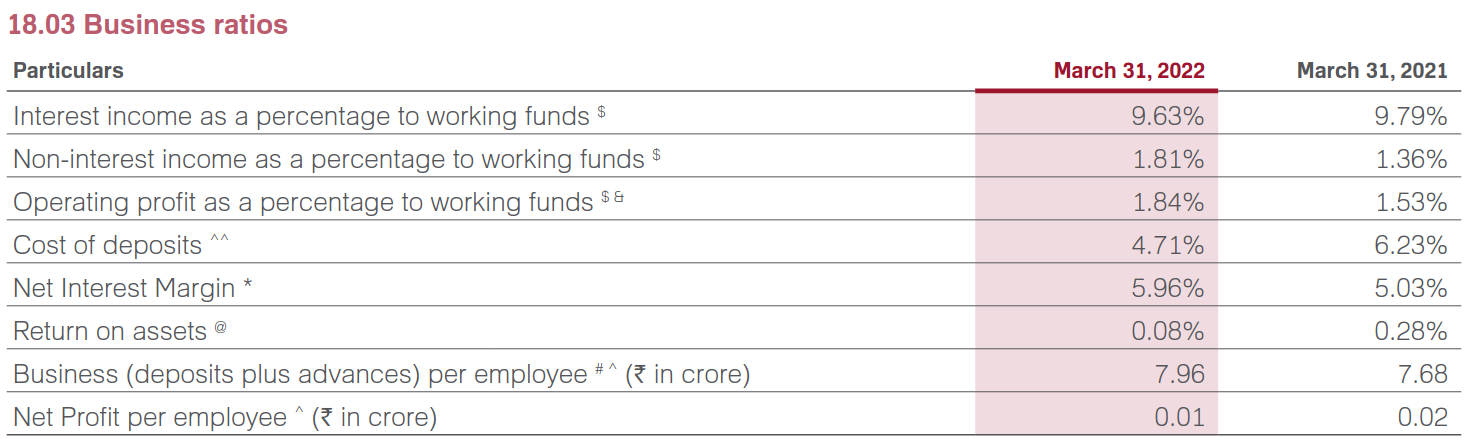

Business ratios:

There is a note about treasury activities in the MD message section but it feels short and vague.

TREASURY ACTIVITIES

The Bank’s treasury operations are largely to service client’s

hedging requirements and for balance sheet management.

We have a comprehensive limit framework including

Present Value of a basis point (PV01), VaR, NOOP limits,

Stress testing etc. which we adhere to. As far as proprietary

trading is concerned, our advice to the trading team is to be

conservative at all times.

There is a also section about 10Yr Gsec yields in the Management Discussion & Analysis section but could not find any commentary about impact on profitability.

I saw some posts about investment fluctuation reserves, this is what the balance sheet says:

Full details about HFT/AFS and HTM holdings are on page 192. Bond experts please analyze ![]()

I guess we can only hope they reduced HFT/AFS after March.

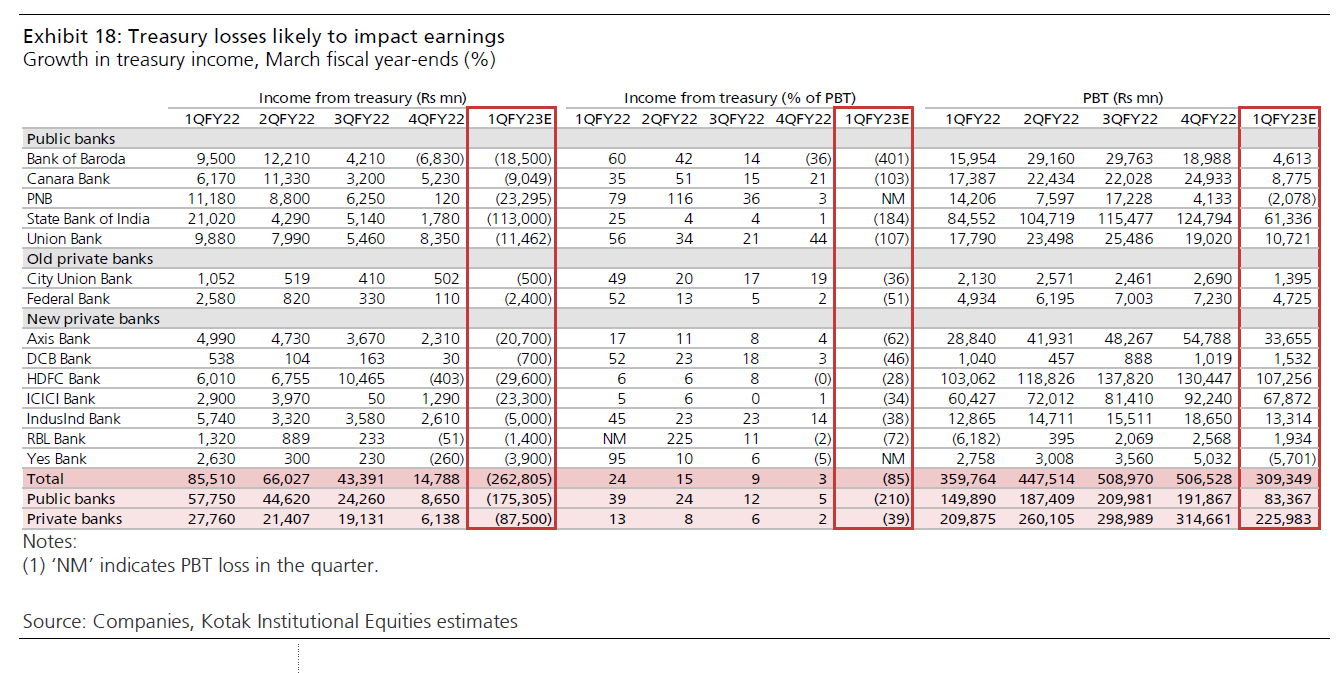

As I had mentioned above the losses on Treasury holdings for the banks could potentially be substantial; Kotak has come out with some estimates of Treasury losses, and they are as below-

SBI- 11,300CR

HDFC- 2,900CR

AXIS- 2,070CR

ICICI- 2,330CR

INDUSIND- 500CR

YES BANK- 390CR

From the work that I have done I think the losses could potentially be higher but let’s see.

Full details here-

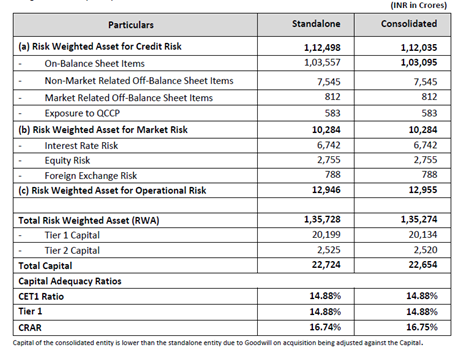

IIB and Yes Bank have an Investment Book of Rs 70,000cr and Rs 50,000cr respectively that are closest in size to IDFCB so I think it would be fair to assume that Treasury losses for IDFCB could be around 400cr. This effectively means that there will be no profits for IDFCB in Q1, if treasury losses are higher then the bank could even report a loss in Q1 especially as the IFR the banks carries is 0. If the situation persists in Q2 then the first half of FY23 will effectively be a write off for the bank. Now some investors might point out that these are just MTM losses and in the long run the impact will be minimal if the bank continues to hold on to the securities; this is true for most banks that have large operating profits with high capital adequacy ratios, but we can’t say the same for IDFCB as the short-term impacts are very real. IDFCB has the Balance Sheet of a large bank while having the bottom line of a small finance bank; so while it might be great to see a quarterly loan book growth of 8-10% for the bank its not sustainable unless the bank is able to generate commensurate profits. What do I mean? Let’s see the CAR Table from the Basel 3 filing for March 2022-

Now the bank grew its loan book by around 10,000cr in Q1FY23 so all things being equal we would expect that RWA would increase by a similar amount. Assume that this trend continues in Q2 and Q3 such that there is an increase in RWA by 30,000cr in the first three quarters. This means the RWA has increased to 165,000cr; now if the first half of the year is a writeoff for the bank due to Treasury losses and they generate 400cr of profit in Q3FY23 then their Tier 1 Capital will increase to 20,600cr in Q3FY23. Using these figures, the Tier 1 CAR will come down to 12.5%; both Basel 3 and RBI guidelines allow a minimum of 10.5% for this ratio but ask any banker and they will tell you that a Tier 1 ratio below 13% is going to set the alarm bells ringing at any decent bank. As a result, the bank will have no option but to raise equity capital by Q4FY23 to increase the Tier 1 ratio or they will need to dramatically slowdown their growth; this is how these Treasury losses have an impact of bringing forward the equity raise for the bank.

The above is a definite negative for the bank as it can lead to additional equity dilution at possibly not the best market timing, a situation similar to 2020, but it’s a much bigger negative for IDFC Ltd shareholders. I was initially planning on using the current rally in IDFC Ltd shares to sell 50% of my holdings to generate cash but after running the above and below calculations I decided to completely exit until the risk-reward is in my favor. My thesis is as below-

On closer examination of the above scenarios and with the general uncertainty in the market at the moment and in particular with the Q1FY23 results for IDFCB I felt the risk reward in owning IDFC had come down considerably and it was better to wait on the sidelines for a better entry opportunity. If the bank will deliver 10% ROE only in FY24 then 1x BV is not exactly mouth watering in today’s market especially if further dilution is going to be necessary. I might be wrong in taking this call but it’s a risk I am willing to take at the current valuations especially if the likelihood of the second scenario keeps increasing.

In the short term, market is a voting machine. Thus, 1Q23 earnings might matter to some extent for temporary volatility.In the long term, market is the weighing machine. The trajectory of asset quality, of cost to income, of the growth matters a whole lot more than a 1-off treasury income loss. An investor is much much better off reading the annual report released few hours ago.

Everyone knows banks will suffer treasury losses which is why banks have been derated. However, banks have started to move upward & are being rewarded for good Q1 core performance & results. RBI’s repo rates are near pre-covid levels, inflation seems to have peaked in India & expected to peak in USA in next 3-6 months. I think the thread would be much better off discussing the minuche of what is contained in the annual report,

Humans might think of themselves as being rational beings, but we are more like rationalising machines (make a decision to sell or buy, then find supporting evidence for it).

Only future can tell us whether owning a full fledged private pan india bank with 7% NIMs, 10% ROE (Q4FY23: 3 quarters away), 20-25% growth, 70-80% retail book, 50% CASA turns out to be a good or a bad investment decision.

Do remember that market values the trajectory more than the number itself. a Bank with 15% ROE ends up at 10% going down deserves low valuation. A bank turning from loss-making to single digit to 10% ROE will not be valued same way.

Just see the annual report. They have provided a lot of data which should give confidence to any investor with >12 month time horizon for investing.

To evaluate a turnaround bank on equity dilution is missing the forest for the trees imho. What one should evaluate is the bridge to 10% ROE. Anyway the merger with IDFC is a 90% done deal. Equity dilution has to happen either through IDFC or otherwise. The only point is that by Q3 or Q4 all banks are expected to do better so dilution might happen at 1.5 pr 2x book so as to grow book value.

“Sell now buy later” is in essence timing the market. Nothing wrong with it. I prefer to do it too. But only when i see 2 years of pain in front of me. To try to do this micro level management for 1-2-3 Q is too hard imo because one also has to consider “what is in the price”> Time to sell IDFC bank was pre-wave2 at 60 rupees, now is the time to buy, imo ![]()

At end of day all of us are justifying our biases, my bias to add is justified with positive data, and @valueseeker9 bhai’s bias to sell is justified with negative data. Only thing is, if i am right about the direction of positive data, i expect my decision to be the correct one.

By selling, one can avoid 1-2-3 Q of pain (even that is questionable because what wedont know is what in the price. Even if we assume 0 profit in Q1 due to treasury losses, many investors would see it as a buying opportunity given that the fundamentals of the core bank are improving. so it is tough to say how the price will react in short term) only by buying right (at right valuation, the right business) can an investor expect a sufficient appreciation of capital.

Disclaimer: invested, adding more.

I thank you all for the wonderful discussion, I learnt from it. In one of my earlier notes, I was wondering how a bank that is posting just 6% ROE (annualising Q4 22), is quoting 1.2 X book. in fact if you go back in time, they were valued even higher (prior to the Voda news of KMB explosive letter giving back the company to government, and prior to the Russia issue where all banks corrected). They have frankly been very richly valued all the time for their low ROE. If you notice, even in my last post, I was complaining why this management and VV are so highly talked about (literally EVERYONE from media to analysts to TV shows talks highly about them), when the bank is not delivering PAT end of the day.

But after reading the Annual Report, even a critic like me is sort of appreciating them in my mind, as no matter what the numbers (PAT is still v low imo), the managment has given tremendous clarity, very detailed set of numbers, not just NPA, they have given SMA0,1,2, cheque bounce everything. maybe this is the reason people believe them so much. what the Q1 will look like God knows. But atleast I am beginning to understand how the management works and explains things from the AR.

In banking as in all of investing, numbers are an outcome. yes bank had numbers. What happened to it?

first & foremost is management. Management, Management, management.

Would someone like to guess the ROE of kotak bank? Its 13%. Why then does it get a premium. There are several reasons but imp most important among them is “management”. Market is valuing the longevity of the franchise.

The true value of a pan-india retail focussed bank growing at 20-25% cannot be overstated.

Incremental loans from IDFCF are at 17% ROE. Eventually at some point (3-4 years out) the ROE will converge to 17% as well.

of course that ride will not be all smooth. Patience will be tested.

often times ‘capacity to suffer’ is itself a moat (both for the company & its investors).

A quote I read from a market veteran sometime back that huge stock rerating occurs when ROE expands from 7-8% to 10-12% than when it expands from 12-13% to 14-15%.

![]() , link of the video, where Mr. Anup Maheshwari ( IIFL turn around opportunity fund ) mentiones about maximum rerating when ROE is moving from single digit or 10% to 15%

, link of the video, where Mr. Anup Maheshwari ( IIFL turn around opportunity fund ) mentiones about maximum rerating when ROE is moving from single digit or 10% to 15%

From min 16 to 17. ![]()

Some quotes are hard to forget, rightly so ![]()