Think the market is starting to now realize how beneficial a rising interest rate environment is going to be for IDFCB. So it’s pretty common knowledge that a rising interest rate environment acts as a tailwind for bank’s NIM’s as the rates on advances tend to rise much faster than rates on deposits, this is especially true for retail focused banks with granular loan books and limited bargaining power of customers. So like other banks IDFCB will benefit because of this too, maybe slightly more due to its retail heavy book.

However the part that is most interesting and which will act as an additional tailwind for IDFCB’s NIMs is below-

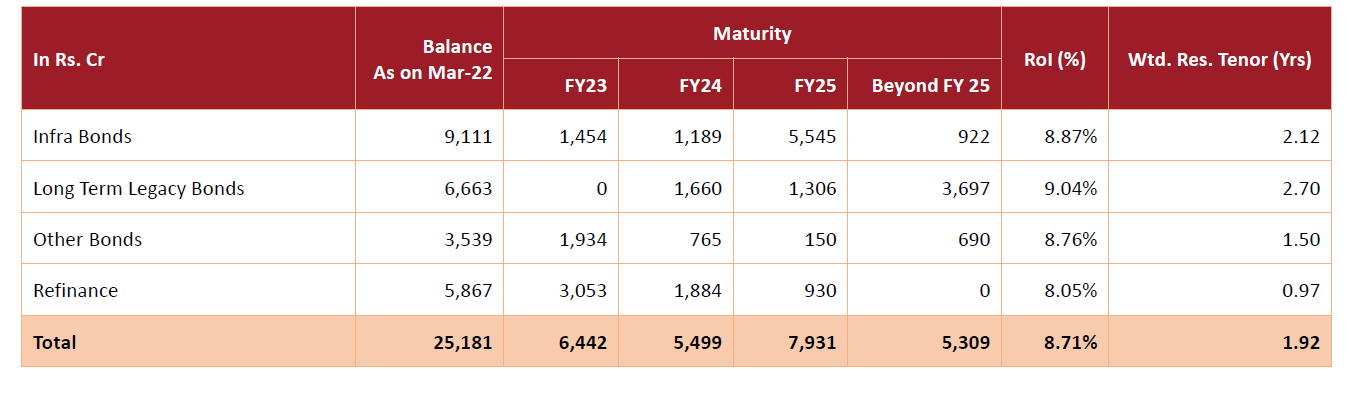

These ofcourse are the dreaded high FIXED cost deposits that IDFCB inherited from IDFC and that have been a drag for the bank over the last few years. Now as we start transitioning into a high interest rate environment what will start to happen is that the drag these deposits were on the overall NIM’s will start to dramatically reduce. The average ROI on these deposits is 8.7%; now 12-15 months back IDFCB was able to raise term deposits at around 5-5% so the drag was almost 3-3.5% due to these deposits. Now fast forward to today and the 10Y Govt bond is trading at 7.5% and AAA Corporates are issuing bonds between 7.5% to 8% in the markets. Pretty soon term deposits and FD’s of banks will also be at similar levels; as a result the drag from these high cost deposits will dramatically reduce and possibly be just around 1% for IDFCB. This is a pretty big deal and the relative loss the bank was suffering due to these high cost deposits should reduce dramatically.

In Q4FY22, IDFCB reported NIM’s of 6.2%+ despite paying 8.7% on 25,000cr+ of legacy deposits. What will change going forward? IDFCB will still pay the same amount on these fixed cost deposits but the lending rates for the ENTIRE system will move up. So IDFCB’s average retail lending rate will move up say from 14.5% to 16.5% (along with the entire banking system due to the higher costs of deposits) while the cost of deposits on this book will stay the same. This along with the first tailwind can have a dramatic impact on the banks NIM’s and I wouldn’t be surprised if at the end of FY23 IDFCB NIM’s are closer to 7%. Remember every 0.5% or 50 basis points increase in IDFCB’s NIMs means an additional 1,000cr to the pre-tax bottom line (as there is no additional cost and operating leverage kicks in) which is pretty significant for a bank expected to report around 1,500-2,000cr in profits in FY23.

Most interest rate increment cycles last 2-3 years so the other good part is that most legacy borrowings will be over by the time system interest rates start to decrease again.