From where you found that there will be treasury losses??

1 Like

Is idfc first holding good chunk of government bonds , then it can post losses

Price going down is not a worry but is there something which we are not aware and the market is.

The stock has become worst performer in entire banking pack. Looking at the guidance and future plan all seems to be good but trend is not reflecting the same.

Can someone please help in this group with some inside what may be going wrong which I am not seeing.

Performance wise also they are achieving what they have said.

9 Likes

As per me the TTM profits are 130 odd crores due to large provisioning in Q1 2022.

Once Q1 2023 results are out we can see the adjusted TTM PE rations stabalize.

Currently the PE ratio is flashed 150+ everywhere and once Q1 results are reflected in TTM there will be some relief.

1 Like

FII and DII selling in IDFCFB, Correction in overall banking Space and midcap banks in particular, possibility of slowdown in economy which may effect credit growth and slippages in retail loans of IDFCFB in FY22 due to covid.

These are the factors i can think of for the correction. I think the market has overdone the selling although I may be completely wrong.

2 Likes

Most of the banks will post tresury losses this quarter. Due to its high liquidity idfc first bank post even higher losses compared to other established banks…

Excess liquidity is not invested in long term bonds but instead kept with the RBI at the REPO rate.

4 Likes

A lot of comments in the last 2-3 days are about the correction in the stock price and frankly, I did not expect this price on the stock.

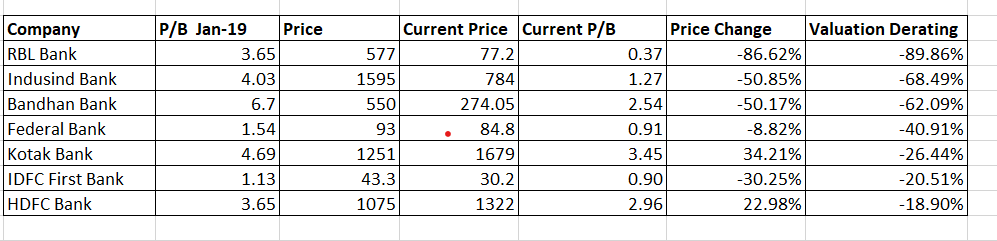

We need to understand that the financial sector in the country has gone through a tremendous amount of stress from Sep-2018 till date. IL&FS Crisis, DHFL, Reliance Capital, PMC Bank, Yes Bank, Covid 1.0, Covid 2.0 and now loss of complete confidence on RBL Bank. I have tried to collate data as to how the crisis in the last almost 4 years has affected valuations in the sector.

NBFCs have been biggest losers in this period with P/B ratios for most players contracting to unimaginable levels. L&T Finance, Manappuram, AB Capital, M&M Finance, Edelweiss, Ibulls housing finance have seen a valuation derating(P/B) of almost 60-80%.

Banks have relatively performed better than NBFCs but there has been a valuation derating in most banks except ICICI Bank and SBI. I have collated a table which is posted below:

Valuation derating has been calculated as (((Current P/B)/(P/B in Jan-19))-1)*100. If you see, in all cases(except IDFC) price change is higher than valuation derating for the simple reason that book values of all the banks except IDFC has gone up in the period under consideration.

For IDFC, Book value has corrected from 38.1 at the time of the merger to 33.6 currently. Main reasons for the erosion of book value are 2 large legacy accounts and the arrival of Covid during a high cost structure period of the bank which left hardly any operating profits to offset Covid related provisioning and hence resulted in huge losses. I would still say that given the decline in book value, the market has derated IDFC mildly as compared to other banks. Can we take this as a positive or does it mean more derating is around the corner? No one knows.

Bear in mind that the annual report will be released anytime in the next 12-15 days. I am also looking forward to the quarterly update expected in the first week of July and particularly will monitor CASA and deposit mobilisation.

24 Likes

Quite simply, IDFC bank is being treated badly for primary one reason: low RoE.

Kotak Bank has twice the advances of Idfcfirst bank, but annual Net Profit is 12000Cr. Whereas, Idfcfirst banks NP is 132Cr.

This picture will change in the future.

But, until then, there will be volatility in the stock price. If this stock was the only one falling, then I’d be worried about the possibility of the thesis failing. Else, it’s just market volatility. Money going out.

9 Likes

Looking at the volumes clearly there’s some heavy selling happening here.

Could be due to patience running out for many.Also might have used to oppurtunity to switch to better performing stocks due to the overall market downfall.

Interesting IDFC Ltd is moving up today.Not sure what’s cooking.

Important thing to monitor now is July 1st update of Q1 Provisional numbers and then the quarterly numbers which should give clarity to lot…

2 Likes

1% Equity change hands @ 29.6/share - CNBC

In my opinion the stock has relatively higher negative sentiment because of consistent low profitability - the longer this takes the higher the likelihood of raising funds through more equity dilution.

The only way to improve market perception and gain trust of large funds is through a consistently rising profits trend. They were on their way to do this but covid second was a huge set back - reduced asset quality and increased opex. RM uncertainty is also an overhang.

Holding the stock has been an interesting experience for me. Started accumulating since June 2020 through Nov 2020 (no changes since). Stopped just as the price was going up fast. Saw the unrealized profit/loss go from -20% to +141% during this time. Was interested in adding at 40 but didn’t have enough cash to buy as much as I would like (I prefer buying in bulk at attractive prices). 30 is even more tempting, if prices stay at these prices for the next few months I will try to increase my holding by atleast 25%.

Fundamentally not much has changed, at least in my view. Two main things that will affect profits going forward would be asset quality (new book, not much seasoned) and opex.

Can someone answer how the rising rate environment affects the long term infra bonds that bank has on balance sheet? Positive/negative or neutral? I would assume neutral because they are fixed rate bonds. But since bond prices go down when yield increases, can the bank buy them back at lower prices effectively redeeming them? I don’t know much about bonds so I’m curious.

The money needed to buy these bonds can as well be used to build assets/lending book that deliver higher interest income than that paid on the bonds. So it is more profitable to lend than to buyback the bonds. If the yields go up, generally so will the lending rates so it will still make sense to lend than to buy back.

The bonds may have to be lived with, except, if the bank feels rates are going to go down, it can enter into an Interest Rate Swap - swapping its fixed interest payments to floating.

The impact of a rising rate environment is to make the cost of funds for the bank more competitive, to the extent of the fixed cost component of the legacy bonds. That’s because for the bank only the floating component of the CoF will rise and the legacy is fixed, while for the market that has no such legacy, all their funds will rise. So it is relatively positive.

5 Likes

In raising rate environment, bonds held by banks go down in price. As banks need to follow “mark-to-market” accounting, such price erosion will reduce the profit. (trading losses ??)

If the bonds are maturing in couple of years, then the notional losses would be less. On the other hand, if the bonds average maturity is more than 5 years, we will see

substancial losses from the bond portfolio.

1 Like

But is IDFCFB holding any bonds?. Bank is giving 6 to 7% interest on saving. Why will it own bonds which provide very low returns?

Sir if the bank has excess liquidity and currently is unable to build the asset/lending book aggressively isn’t it better to redeem them and save interest cost. Why i asked this question because currently I see a bank redeeming its bonds which have maturity after 1 year from now

1 Like

Subject to those conditions, yes. However if a bank is growing its loan book as rapidly as this one, at the rate of lending it does, then it may not want to.

There could also be other considerations not apparent to us. For eg because these bonds carry tax breaks, it may be the case that they cannot be sold or bought back till maturity (like 54EC REC bonds).

2 Likes

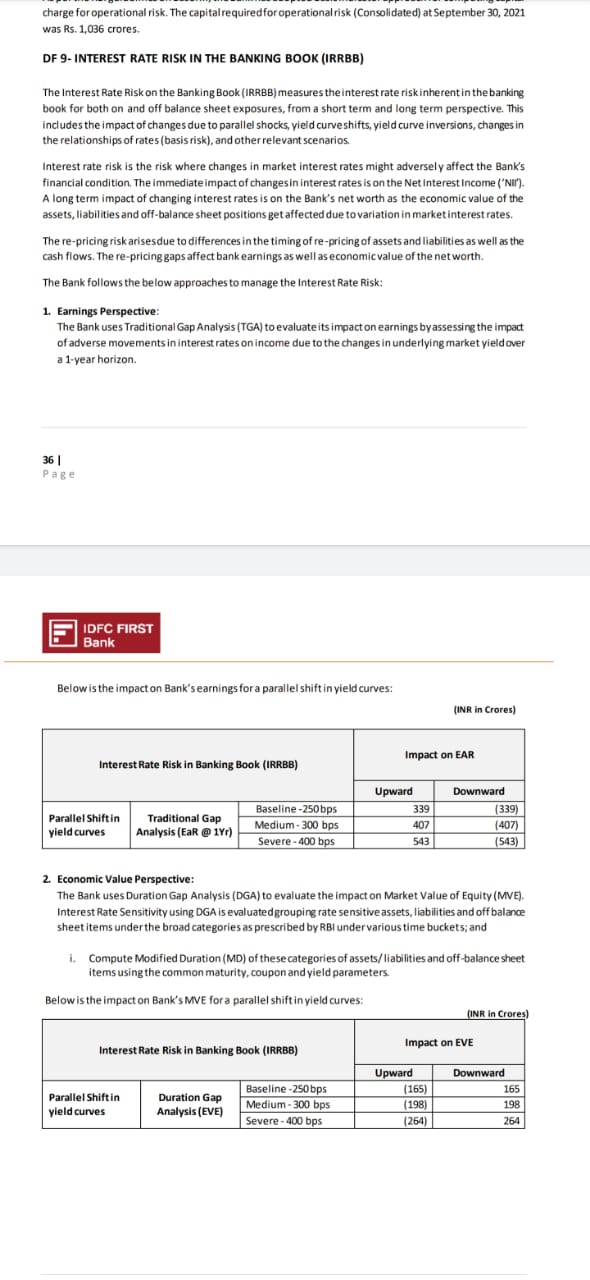

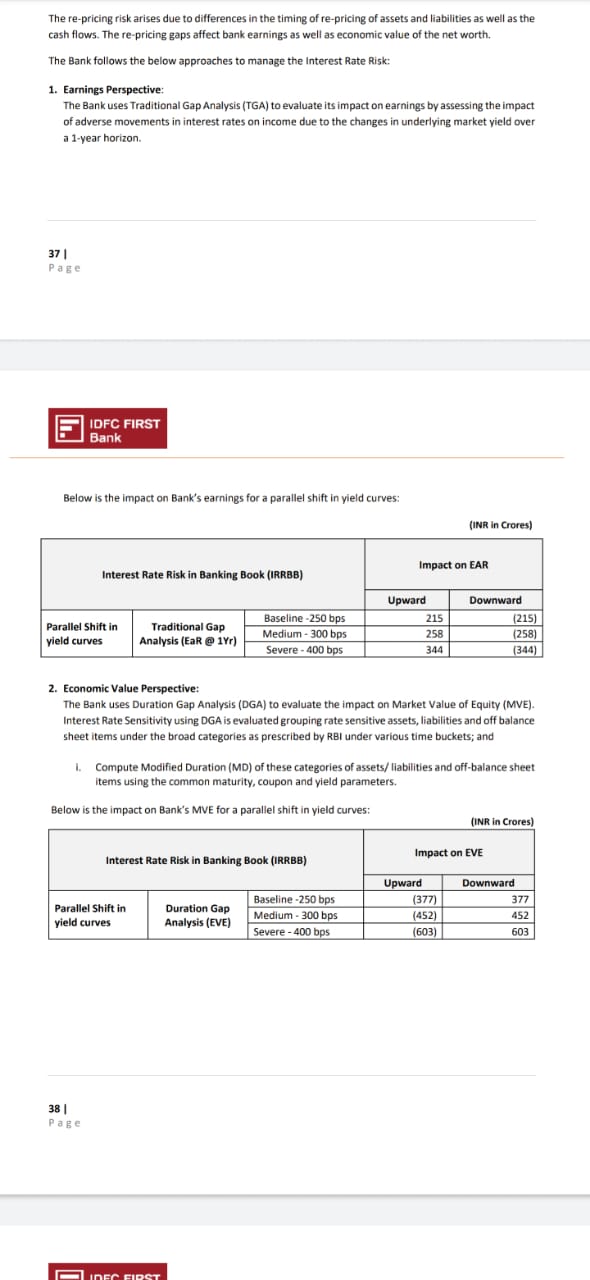

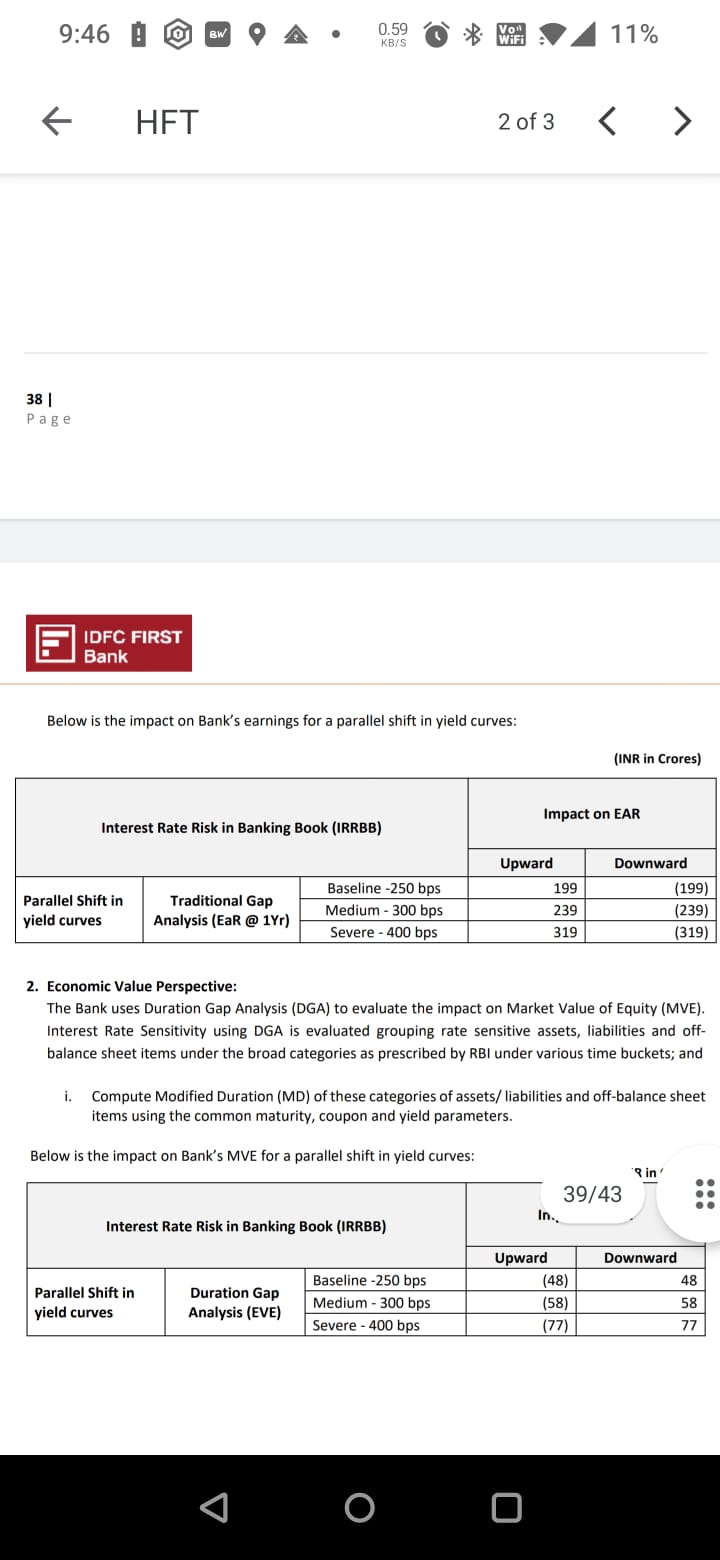

Check the Basel disclosures made by the bank.

Q3

Q2

Q4

The bank has to disclose the interest rate regime sensitivity to their govt bond portfolio. What we can see is that for last 3Q bank has been silently preparing for a high interest rate regime.

That for a 250bps increase in rate, the 1-off 1-time loss might be 48cr. Now, since Indian interest rates have been adjusted <1% the estimated loss should be < 20cr by linear extrapolation.

Do keep in mind that this is the calculation according to the duration & coupon rate of the bond. Market forces can cause a larger or smaller loss, so to be safe i expect a 20 ± 10 cr loss in treasury in Q1

As we can see, bank has been shifting monies to rbi repo to make it’s ride smoother in anticipation of an interest rate cycle.

Can we please go back to analysing the core biz & not the non core 1-off 20 cr potential loss in next Q?

Disclaimer: invested biased,

Data based on discussion with @manikya_saiteja_gund

13 Likes

Not referring bonds in assets, they’re not significant. My question was about the bonds that are liabilities, the bank is paying high interest for these. Because of merger the bank had to own responsibility of these bonds that were issued by the erstwhile IDFC Bank a long time ago.

These bonds have a significant (negative) effect on profitability so I wanted to know if the bank can get rid of them without big losses. But based on @diffsoft’s answer looks like we have to live with them till they mature.

Friendly note to investors new to IDFCF: if you weren’t aware of these bonds (and other legacy issues), please go through all the material bank provides and at least one year’s worth of discussions on this forum.

@Puch has already discussed the impact earlier, you can see his post here IDFC First Bank Limited - #2634 by Puch