The bank is at the extremely depressed valuations at present. And staring at good growth in earnings. Yes, stock may go down for another 10 to 20 percent but if you take period of next 2 to 3 years the price may reach what it was in March 2021.

3 Likes

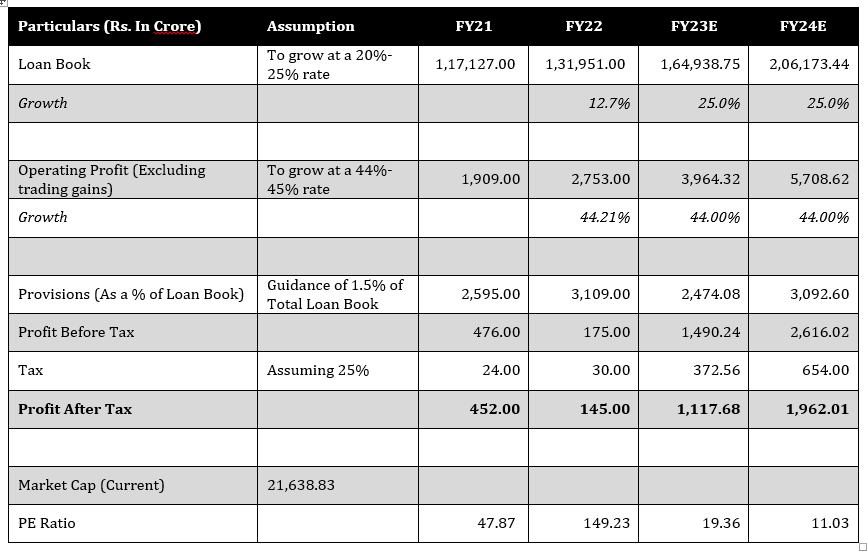

VV has given a guidance for 13-15% ROE by FY 2025. I have made a projection assuming the following :

- Loan book growth at 22% for 3 years.

- PPOP Growth of 45% for 2 years and 25% for 3rd year.

- Credit cost of 1.50% for all 3 years (He has guided 1.50% for only FY 2023).

- Trading gains at 530 crores (Same as FY 2022 , for next 3 years ) - I know it will come down but i have taken it as constant since ICICI securities has taken it as unchanged.

Going by my estimate PAT for next 3 years comes to 1720 cr, 2692 cr and 3326 cr.

ROE at end of March 2025 is 10.70% and ROA is 1.53%.

I hope by saying 13-15% ROE he means 13-15% for full year and not annualized ROE of last quarter of March 2025.

3 Likes

Report RBI to go for another 0.40 percent hike in rates at next week's policy review meet: Report

Rate-hike is a certanity.

This will bode well for the bank, more than other banks. Reason: high cost bonds will cause that much lesser drag on NIMs.

4 Likes

More specific numbers :

2023 PAT - 1720 cr

Net Worth - 22723 cr

2024 PAT - 2692 cr

Net Worth - 25415 cr

2025 PAT - 3326 cr

Net Worth- 28741 cr

Average Net Worth - 27089 cr

ROE for FY 2025 - 12.27%

Annualised ROE for Q4 2025 - 13.28%

2 Likes

Net worth would be much higher given either the reverse merger would happen or funds would be raised. ![]()

Yes if AMC money is not accepted by bank and RM happens , then few shares will be cancelled… In that case , ROE will improve…

But if funds are raised (Which will happen in 2024) , Networth will go up but ROE will remain suppressed…

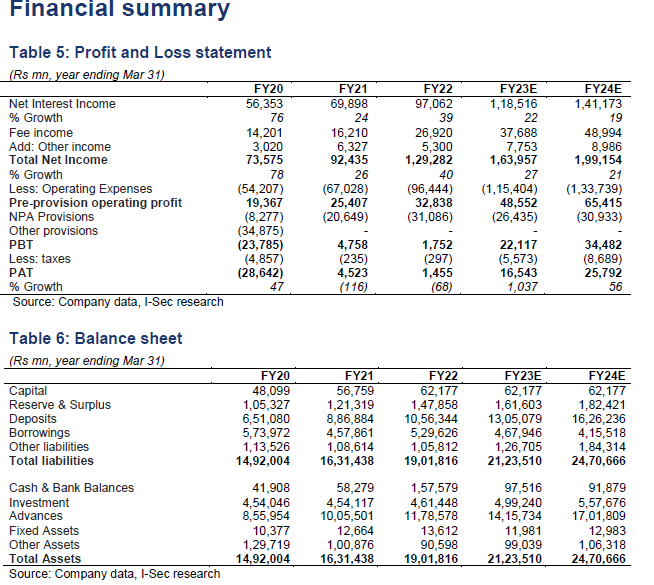

I’ve made a similar projection too. This one accounts for provisions.

The sources of my assumption about guidance are as follows:

LOAN BOOK GROWTH

-

Q4FY22 Investor Presentation

“Loan book to grow from here on: We have made significant progress during the last three years (FY 19-22). We expect the loan book to grow at ~20-25% on a sustainable basis from here on for the foreseeable future.” -

Q4FY22 Earnings Call

“You see that if you were to get a sense of where the loan book will grow from here on for the next few years, we think that to grow the loan book from overall loan-book, retail, wholesale all put together to grow that and between 20% to 25% it should be very possible.” -

Interview with Financial Express

“We are starting from a small base in the context of India’s size, and in India, growing 22% from a small base is not a big deal. We have strong capabilities for credit appraisal in all our businesses. We are also growing our wealth management, cash management, trade solutions and deposits. All of these can grow at 25% comfortably from our base.” -

Interview with Business Standard

“Now we feel that each of these businesses, whether its consumer loans or wheels or SME or home loans or loan against property, everything will grow in this country. So, so really for us to grow 20-25% on home loans or other businesses it’s really no problem at all.” -

Interview with ET Now

“This year we are expecting credit growth – retail, wholesale all put together – to maybe 20-22%.”

OPERATING PROFIT

-

Q4FY22 Investor Presentation

“Strong Growth in Operating Profits: While the loan book grew by only 13% YoY, the Core Operating Profit has risen by 44% from Rs. 1,909 crores in FY 21 to Rs. 2,753 crores in FY 22. This clearly demonstrates that our incremental business is highly profitable and we are beginning to see strong improvement in operating leverage. We expect this phenomenon to continue to play out over the next few years, which will result in increase in overall profitability and ROE” -

Interview with Financial Express

“What is your key focus for FY23?”

“Profitability. We have addressed assets, asset quality, deposits — everything. Now it’s only profitability to be addressed. It will happen from this year. You will see a sharp increase in profits in FY23. Our operating profits grew from Rs 1,900-odd crore in FY21 to about Rs 2,700 crore in FY22, a growth of 44%. We expect another similar jump in profits in FY23 and … in FY24 also. That’s the pace at which the profits are rising at our bank. One day, you will suddenly wake up to the potential of our bank.” -

Interview with Business Standard

“Last year our operating profit book grew by 44%. We expect that next year as well, and the year after that we believe that sort of track can be maintained. You can watch the results to get more confidence.” -

Interview with ET Now

“Last year, our loan book grew by only 13% but the operating profit grew by 44%. It reached Rs 2,700 crore this quarter. Now that tells us something about how the operating leverage is kicking in. Our own sense is that operating profit can again compound by another 44-45% next year and by another 44-45% the year after that. That is how we think the numbers will play out.”

PROVISIONS

-

Q4FY22 Earnings Call

“At that time if you recall I had publicly said to all of you that our Q2 provisions will be less than Q1, Q3 will be less than Q2 and Q4 will be less than Q3. I’m happy to share the following numbers with you as it turned out. So, our gross Q2 provisions were 475 crores, Q3 provisions were 392 crores and Q4 provisions are only 369 crores. The sum total of all these four numbers are Rs. 3109 crores. Now our average loan book for the year was ~Rs. 1,18,700 crores. If you divide, you’ll get a number of 2.5% to 2.6%. Now you can think and calculate for yourself that in a COVID ravaged year, where Q1 was so hard hit and by the way, in Q1 there were lockdowns across the country. I can’t say across the country but across the large number of states, is practically a national lockdown but there was no moratorium. So, slippages were there. This despite such a quarter and a year our credit loss for the whole year was only 2.55% to 2.6%. You can do the math, somewhere there between the two. I think it’s 2.6%. So therefore, if a COVID ravage year it was 2.6%, really, it’s not hard for you to also believe us that next year when the guiding just for 1.5%, we have done our math for that. If we take annualized credit loss then for Q4 our annualize credit loss was only 1.2% now. So that’s 1.2%. We are guiding for 1.5%. We kept ourselves sufficient cushion when we say that next year, we’ll do 1.5%. Therefore, there is enough data by our side that when we were running this, so earlier it was 2.5%, now even in a COVID year its 2.5%. Now we’re guiding for 1.5%. So, you get the drift. Therefore, we believe that we are building pretty much a phenomenal model at our end where we are able to lend to multiple segments of the market” -

Interview with Financial Express

“Also, provisions are down every quarter. In the latest quarter, annualised provisions are only 1.2%.” -

Interview with ETNow

“For the upcoming year on the credit provision guidance, we are guiding for only 1.5% of the loan book and that tells us how conscious we are about asset quality. We are approving between 40% and 60% of the application that come to us.”

12 Likes

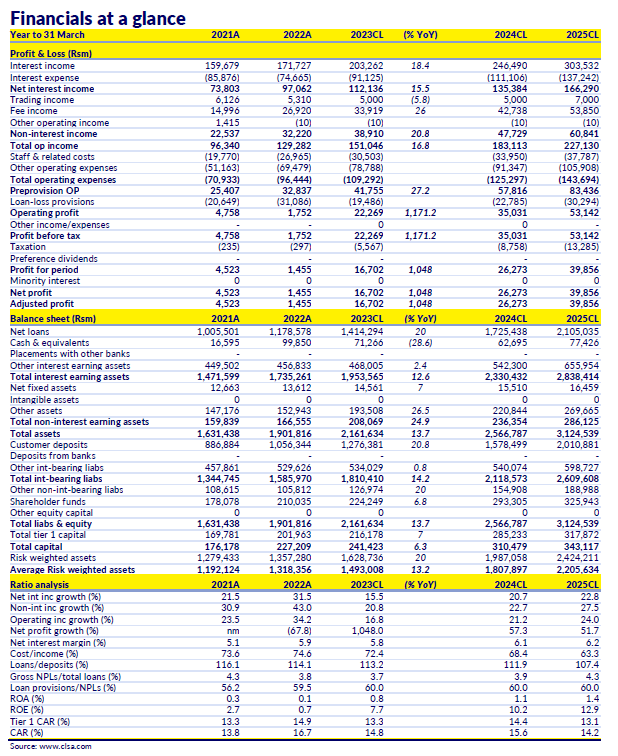

CLSA estmiates; they are showing a 13% ROE in FY25 despite assuming a Rs 5,000cr equity raise in FY24. Last two quarters of FY25 the ROE is 15%+.

ISEC Estimates-

4 Likes

Can you please share the full report of CLSA … Thank you…

1 Like

Conservative NII estimate by CLSA and slightly pessimistic loan loss provisions estimate. I don’t expect full-year provisions for the bank to cross 2k cr. I do expect PAT to be in the vicinity of 1800 to 2000crs.

1 Like

Numbers as projected by CLSA do meet my own expectations… Few 100 crores here and there is fine…

Loan book will be much bigger than 1.4 lakh crores in FY 2023…

1 Like

Lot of positives here already and I am personally invested. But can someone come up with a bear case for IDFC First to get another perspective? For me it has to be:

- Reverse merger overhang - Unsure how this will play out. IDFC Ltd is after all promoter of the bank and there are more than few ways how this can turn out.

- Corporate book is still large part and may cause NPAs

- Slowdown in Credit offtake - This would effect overall banking sector.

- ROA / ROE not hitting target of 1.4% / 15% by FY25.

- Raising funds - Tier 2 and equity dilution.

Any other bear case / overhang if someone can come up with?

Disclosure: Invested.

11 Likes

To add to your list,

-

Key Man risk:

The entire bet is on V. Vaidyanathan, and his leadership and ability to retain top management. His vision has been communicated clearly to his shareholders. But if he is no more a part of the organization, for whatever reason, every projection can and will be questioned. There is no idea about who will be at the helm and how competent the bank will be without him. -

Competiton Eating them up

IDFC First bank faces stiff competition in the lending space from the likes of Godrej, Poonawala and more. They will consistently have to find new avenues of growth. A significantly low ROE compared with its peers is also a matter of concern.

3 Likes

Credit Rating Reaffirmed:

2 Likes

The rating report lists Risks mainly due to NPA and Liquidity, where liquidity is mentioned as adequate.

The worst of NPA is behind us. Covid was the litmus test, IMO. Considering how new the bank’s operations were, Warburg Pincus invested a good amount around Rs.20, when the bank was in the eye of the storm. That goes to show the corporate good will VV has.

6 Likes

A lot of points in the CLSA report are way off the mark from rationality in my view:

-

CLSA assumes an NII growth of 15.5% in FY23 vs FY22. Management has guided for an overall loan growth of 20-25% which means that CLSA is assuming NIMs will compress and lead to slower NII growth vs loan book growth which is contrary to management guidance that NIMs can still grow from here on. My estimate for NII for FY23 is 12550 crs vs CLSA estimate of 11213.6 crs.

-

CLSA assumes that core fee income for FY23 will be 3391 crs. If one just looks at the Q4FY22 fee income, it stands at 841 crs. If one assumes that Fee income will grow by 6% QoQ for the next 4 quarters from the base figure of 841 crs in Q4FY22, one arrives at a number of 3900 crs in fee income. One must also take into account the fact that fee income has grown by more than 10% QoQ for the last 2 quarters and the momentum is very stong. In my view, Fee income will cross 4000 crs in FY23.

-

In my view opex will grow at a faster pace than what CLSA has assumed. Opex growth should be between 20-22% in my view and opex will reach 11750-11800 crs in FY23.

-

Overall I feel numbers are underestimated and company should beat estimates by a good margin. My PAT estimate for FY23 is 1900-1950 crs.

14 Likes

Where we can find CALSA’s report ?

I was egarly waiting for this to happen, i feel it will boost for credit card industry…

6 Likes

The short run of FY 23 does not matter, as long as it is in the zone of what you/ clsa is saying, and as long as there is consistency, and as long as the medum term path is clear. For the medium term say fy 25 if we go with clsa estimates of pat of 4000 cr, and if the company delivers on these lines, it will be quite an incredible achievement. From no casa (< 10%), no earning power… (NIM of 1.9%), No pat (loss making), poor liabilities structure, and poor infra loan book. if from there the company can come to the CLSA nos, it will show the capability of the institution and give us (and analysts) the confidence for the future from there on. Let us see if the management can deliver on the lines projected by CLSA. as far as ROE is concerned it will depend on equity raised. I assume analysts will trend the ROE from there on for next three years and try to project value.

10 Likes