Investment banking - Will suffer with lower markets since the primary market pipeline with fall at an alarming pace when markets go into extended corrections. This is fee income where employee cost is the highest cost, ICICI Sec has shown the willingness to let people go during bad times so management can take necessary steps here to cushion impact on profitability from this segment

Broking - Once again, not much control on the top line here. What I find interesting is that ICICI Direct keeps coming up with newer features and functionalities, their product management team looks solid to me. The bulk of the revenue depends on the cash turnover, F&O revenue will probably account for just 15-20% of the revenue going by whatever rudimentary numbers I have run over the past week. This segment is all about operating leverage, costs will not scale with revenue during good years while they can bite disproportionately during years when income falls. The key variable I would track here is market share which can indicate a weakening competitive position over the medium term if it trends down. I would not worry too much about fluctuation in revenue since that is a function of the industry itself

Distribution - This is a much more predictable and solid segment, key question is how much of upfront commissions have they been booking over the past 3-4 years. Managements will never directly answer this question, I will attempt to get a sense of this by speaking to some industry guys over the next few days (wealth managers and AMC folks). If the upfront revenue component was high, expect a fall in revenue over the next 12M as the SEBI directive on a all trail commission model kicks in

The real big risk I see here is that there is a huge dependence on ICICI Bank for customer acquisition, if any regulatory change prevents ICICI Direct from having desks at ICICI Bank branches this can materially impact their competitive position and market share. Some finer work needs to be done to assess this probability.

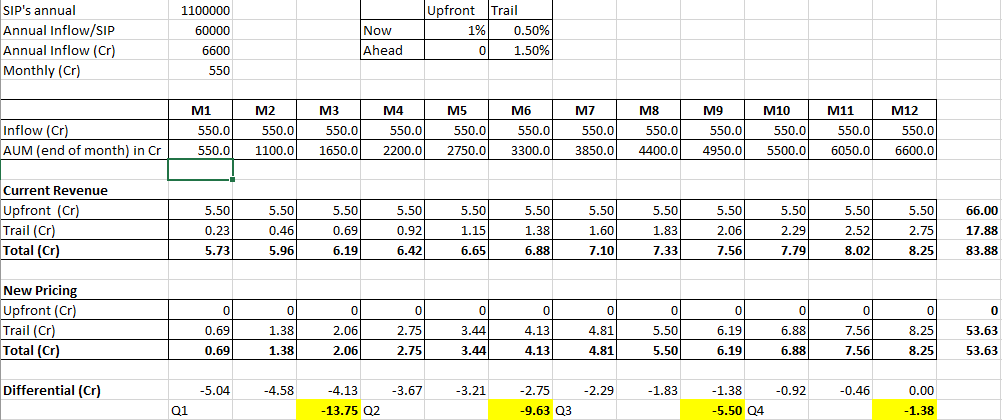

No of SIP’s triggered in last 12M (as per H2 report) = 1.1 Mn

Assuming average SIP = INR 5000

Monthly gross inflow from SIP = 550 Cr

Current pricing for most MF equity schemes is 1% upfront and 0.5% trail per year from day 1

Assuming overall commission stays the same, after SEBI directive the mix will be 0% upfront and 1.5% trail per year

Once you cast these numbers and try to estimate the impact (purely for the annual SIP book of 6600 Cr mind you), the exercise is pretty interesting -

In short, impact on the first 2 Q’s post the SEBI directive on the MF revenue will be huge. From Q5 onward (of the transaction being executed), trail model actually becomes more predictable and steady assuming the AUM remains constant.

For H1, MF revenue was up 18% to 150 Cr

I would not be surprised if the Q3 and Q4 MF revenue actually shows a dip YoY even if the AUM base is higher. One needs to understand that the same trend of revenue as projected above for SIP will hold for lumpsum equity MF investments as well.

On top of this there will be the impact of reduction in TER for large AMC’s which they will pass on to the distributor (HDFC AMC Q2 presentation states this in black and white). This means a double whammy is likely in Q3 and Q4 on income from MF distribution.

With Investment banking and Prop trading income expected to remain subdued and brokerage income showing only a slight growth, remains to be seen if FY19 will be better than FY18 in absolute numbers (my take is that they could be lower, yet to quantify the total impact)

I’ve also done channel checks on what the commission structure from MF for ICICI Sec Wealth management has been all these years, looks like it was a mix of upfront and trail based on the inputs I have received so far.

What remains to be done -

Try to get a sense of the risk due to ICICI Bank working as a customer acquisition channel for ICICI Sec, if something is changed here by the regulator the impact on future customer acquisition can be huge

Get a sense of what % of MF AUM comes from UHNI families (those with an MF book of 50 Cr and above), they will most likely move to the advisory/RIA model where they pay the advisor a % of AUM rather than do transactions through the regular route. In this case return in assets (fee as % of AUM) for this segment will be way lower than what ICICI Sec is currently making. Try to quantify this impact if one can, this is expected to impact over the next 2-3 years

Get a sense of the operating leverage involved from the customer base point of view. Hardly 20% of the customer accounts are active, the dormant people whenever they start investing will most likely do it through ICICI Sec rather than go somewhere else

Get a sense of what scenario is being discounted by the CMP and see to what extent the above risks are being priced in

Totally agree with this from my personal experience , started with ICICI but now completely stopped using it.They offered 5000 Rs /- Free brokerage if I start using it again but still did not go back to such high charges.

I think they all follow a particular structure which is beneficial to them and shifting to a completely different structure makes them lose their current hold and may fail them in the new front too. Or maybe they believe that this low-cost model will not sustain as users expect new services which are costly to everyone and cannot be delivered at low cost.

Specifically speaking, there is an argument that Zerodha is suitable for delivery and other platforms with no room for error are suitable for trading as even a second can make a difference when you are trading for the day, as we need a stable platform that executes our orders fast.

Q3 results of Isec are along expected lines. ISec income is highly correlated to delivery turnover at NSE. although a large number of orders may be in F&O segment, those are low yielding orders. Over last several years Isec’s ADTO has seen a higher proportion of these low yielding orders hence yields are dropping.

Delivery based orders in cash segment with its fat commission rates is the real bread and butter for Isec and other full-service brokers. This income depends on market cap growth and overall delivery % on exchanges. In FY 19 so far, average market cap has remained flat and delivery volumes as a % of total volume has gone down from 28% to 25%. This trend will continue for another one to two quarters.

FY

NSE Mcap

NSE Turnover

Delivery Turnover

NSE ADTO

ISEC Income

ISEC PAT

Turnover / Mcap

Delivery %

1997

419,367

294,503

32,640

1,176

70%

11%

1998

481,503

370,193

59,775

1,520

77%

16%

1999

491,175

414,474

66,204

1,651

84%

16%

2000

1,020,426

839,052

82,607

3,303

82%

10%

2001

657,847

1,339,510

106,278

5,337

204%

8%

2002

636,861

513,167

71,765

2,078

81%

14%

2003

537,133

617,989

87,956

2,462

320

108

115%

14%

2004

1,120,976

1,099,535

221,364

4,328

372

157

98%

20%

2005

1,585,585

1,140,071

277,102

4,506

230

64

72%

24%

2006

2,813,201

1,569,556

409,353

6,253

474

157

56%

26%

2007

3,367,350

1,945,285

544,434

7,812

438

64

58%

28%

2008

4,858,122

3,551,038

972,803

14,148

749

150

73%

27%

2009

2,896,194

2,752,023

611,535

11,325

518

6

95%

22%

2010

6,009,173

4,138,024

917,705

16,959

746

124

69%

22%

2011

6,702,616

3,577,412

979,269

14,048

708

113

53%

27%

2012

6,096,518

2,810,893

785,268

11,289

718

77

46%

28%

2013

6,239,035

2,708,279

797,504

10,833

706

72

43%

29%

2014

7,277,720

2,808,488

823,042

11,189

812

89

39%

29%

2015

9,930,122

4,329,655

1,276,589

17,818

1,210

295

44%

29%

2016

9,310,471

4,236,983

1,252,658

17,154

1,125

239

46%

30%

2017

11,978,421

5,055,913

1,479,963

20,387

1,404

339

42%

29%

2018

14,044,152

7,234,826

2,019,893

29,410

1,859

559

52%

28%

2019*

14,279,083

5,961,185

1,476,491

32,087

25%

Upto Dec 2018.

Source NSE, Company

Isec income has dropped in FY 19 inspite of higher ADTO because of falling delivery volumes. Delivery turnover as a % of total turnover is at a decade low of 25%. Also, FY 18 was a big year with ADTO and delivery volumes both rising more than 40% so in comparison FY 19 is subdued.

Revenue grew by 12987 million as compare to 139505 million for nine month FY18

Overall non-broking revenue contribute 46 % of overall revenue. Distribution Revenue went up by 7 % while broking revenue and corporate finance revenue decline by 6 % and 24 % respectively

Growth in distribute revenue impacted during the quarter because of significant regulatory changes related to mutual fund commission

Broking and corporate finance revenue decline mainly on account of high revenue base in last fiscal and muted market condition

PAT stood at 3692 million compare to 4024 million last year nine month.

Cost decline marginally from 7353 million to 7304 million in the nine month FY 2019 a decline of 1 % implying net margin of 28 % for the nine month this year similar to the nine month last year.

ROE stood at 55 % annualized

Company had added 3.2 million new client in nine months FY19. Resulting in total operational account increasing from 3.9 million to 4.3 milion. In terms of client engagement company overall active customers increase by 10 % to 12.2 lakh in nine month FY19 over 9 month last year an increase of 12 %. It was also there on NSE active client from 7.5 lakh last year to 8.4 lakh client in this year.

Key Highlights

Highlights of Broking Business

Industry brokering volume was up by 58 % YOY led by 62 % growth in relative ADTO and in 4 % growth in equity ADTO. During the same period ISAC ADTO grew at 48 % , Equity ADTO volume growing ahead of market at 10 % and derivative ADTO volumes growing by 51 %

Company market share was at 8.5 % in nine month FY19 compare to 9.1 % in nine month FY18.

Total brokerage revenue excluding interest income which contributed to 54 % of revenues in nine month FY19 decrease by 6 % same period last year. From 7489 million rupees to 7040 million mainly on account of decline in delivery based volume.

Retail brokerage revenue decline by 7 % from 6676 million to 6197 million and institutional broking revenue increase by 4 % from 813 million to 844 million.

Interest income from company brokerage income has grown by 17 % from 1125 million nine months last year to 1350 million in nine month this year primarily on account of margin front deployed with exchange

In distribution business revenue grew by 7 % YOY from 3272 million in nine month 2018 to 3510 million in nine month

Fund Raising from Equity decline by 77% YOY Decline 2019 and contribution in total revenues has increase from 24 % in nine month FY2018 to 27 % in nine month FY2019 .

Mutual fund average AUM was 346 billion rs in nine month of this year a growth of 19 %. From 292 billion in nine month 2018 compare to the market AUM average growth of 14 % on YOY basis. Mutual Fund revenue was 2103 million in nine month of this year a growth of 6 % from 1119 million nine months of last year. The upfront commission will get added to the trail income going forward. Focus on SIP has resulted in a 17 % YOY growth in SIP trigger in last month of the period to 0.6 million in nine month 2018 to 0.7 million in nine month 2019.

Life Insurance revenue grew by 4 % from 302 million in Nine month 2018 to 314 million in nine month 2019.

Investment Banking Business

Equity market show decline of 77 % in terms of funds mobilized or raised resulting in slowdown in ECM activity of the company.

Investment banking revenue 862 million rupees in nine month of this year. A decline of 24 % from 1136 million in nine month of FY2018.

Going forward IPO activity is expected to increase by 730 billion worth of issues filed with SEBI.

Continue to focus on advisory capabilities and as a result company has been chosen as advisor in various 10 deals for this 9 month 2019 compare to 5 deals of whole of FY2018.

Company acted its financial advisors to LIC of India to increase in equity stake in IDBI bank upto 51 %. Also has been selected as advisor by finance ministry for NII deals.

Mutual Funds and Asset under management up by 8 % at 22.9 trillion as on Dec 31st 2018 on YOY basis from 21.3 trillion as on Dec 31st of 2017. It get large support from consistent SIP Flows and Robust participation of Retail investors despite volatile market. Two significant regulatory changes in the form of security on saving of Aadhar Data and dis-allowing payment of upfront commission to distributors has an direct impact on business. First impacted company digital client acquisition which led significant impact on mutual fund revenue.

In December company has structured its long term strategy. For retail business company had shaped a twin strategy more client more engagement aided by technology edge which company will further intend to enhance by adopting the strategy of digital openness to compete in the ever evolving digital market space . For institutional business company continue to Cater the need of institutional clients by helping them with appropriate solutions through the life cycle.

Company with continue to give good ROE by diversifying the revenue.

Initiative undertook

Digital acquisition T20with the objective of faster client acquisition on boarding post Aadhar supreme court judgment. Redesign the digital process of client acquisition and will re-deploy the T20 product.

Company launche revolutionary new EATM order with which retail investor will get Real time credit of sales proceed in their Bank account when they will sell stocks in the BSE in that instead of waiting days of T+2 days under the current settlement system . The fact is this service is open to all at no extra cost is testimony to customer first approach for the strengthen of strong liquidity base proposition

Launch a mobile app for business partners team of more than 6500 IFA in north side . This app will assist partners to initiate mutual fund transaction on behalf of their customer , provide information on behalf of customer analytics and crack their receivables which was early available only on desktop version.

Launch a unique offering for private client called Direct U under advisory services. This offering leveraging power , technology advisory or parent pricing to enable clients to invest digitally in direct schemes of mutual fund through the ICICI direct platform. Direct brings client a process base assessment defined asset allocation strategies and active investment advisory. It also provide integrated portfolio reporting in the analytics of investments and capital gains statements on digital platform through tier AUM link structure with zero compensation from manufacturer thus insuring alignment of interest.

Q&A

On retail proceed what is the blended brokerage and what is the plan forward ?

Kindly Elaborate on the mutual fund Upfront and trail commission ?

Company don’t drive business from a yield perspective because volume is not only a mixture of equity but also a mixture of derivatives and there is a big range in which options operate on per contract basis so when revenue will be divided by volume so it get influence by derivatives volume and delivery volume. Equity is more high yield part of the business but in last nine month the derivative customer is engaging in a lot more with brokerage platform. So combination of both is important for company so company is more focus at business level in which customer engaging and getting customer acquisition up . In terms of market share company is between 8.5 to 9 %. Company is continue to add customer

From April 1 there will be changes in terms of commission depend on size of mutual fund so there will be broadly 25-30 % impact for most people in the mutual fund industry and company would be in similar range. Company will not impacted much because company had already move into a high trail model even much earlier. Company do see the upfront coming back as trail over a period of time.

What is company outlook on cost to income ratio ?

Cost to income ratio for company was about 57 % right now The total expenses have decline marginally on a YOY basis. Most of fix expense has remain flattish or minimal increase and variable expense has come down as a result of this overall cost to income ratio remain flat or minimal decline. Going forward also cost will be key focus area for the management. Company don’t expect big scale movement on the upward side so it is more of inflationary or control growth from here on. So cost to income will be more a function of revenue. Employee expense will be little part variable may be 75 : 25 as industry follows. As a strategy company want to hit 20 %. .Company has target of 50 % cost to income ratio by FY2022.

On other expenses how much will be variable and related to volume ?

Other expenses would largely be not related to volume. Operating expenses is the one which variable at volume where there is a decline on YOY basis of about 14 %. The other expenses refer largely to fix kind of cost like rentals, So there can be a minimal inflation going forward also. Right now it is 6 % YOY kind of growth.

What would be the fair comparison after several impacts coming in mutual fund industry ?

It would be fair to compare FY18 with FY20 as it was a non-impact year and in FY19 all changes will come and again FY20 will be no impact year.

What percentage of company portfolio is on trail commission compare to upfront ?

Bulk of revenue is coming from trail but from now everything will be on trail.

Employee cost last year was 550 Cr but comparing to peers company have much larger base for example comparing to Zerodha they only have 1200 employees so does company is over invested in this modeling or company will adjust the employee and technology whenever the time is right ?

Company have two parts one is Twin strategy or more clients or more engagement . Within the more client strategy company certainly want to build 3-4 stands of strategy. One stand of strategy will be digital and how to make them much more effective in company own through co-operation of a stronger brand. Second part is partnership with ICICI Bank where company will continue to focus on that . Third will be company partnership with business partners across the country and that will stay important stand for customer acquisition. So for underlying all of these three things will be a digital technology base strategy whether it means a fully online kind of acquisition or assisted by online. For example company product is T20 that company launch it about last quarter. Company has taken a step back given that supreme court ruling but with a new process company is now back with the T20 strategy. Therefore company focus on customer acquisition will stay.

The opportunity is very large so therefore company look at digital tools to sell to people to gain more efficiency and productivity. Company have one of the largest feet on street on wealth team. So company is running 5 different business under one brand and all of them are moving to digital from offline from various different mixtures. The focus is to look at productivity and digital efficiency going ahead.

How will be the advisory business run going forward ?

It will be based on AUM of particular individual customer. There is nothing company get from manufacturers on account of revenue in this product so company has targeted it toward ultra HNI who will see the performance of advise and will be willing to pay a separate advisory fees for the same.

What is company margin funding book for the quarter ?

Roughly about 500 Cr

As now Zerodha is number one stock broker so does company need to reduce pricing ?

Company have 1.2 million customers who are active with company over the nine month period and company is looking to customers as investors who come to platform through their life cycle and there is different part of wallet need it could be broking , mutual fund , IPO , NPS so company is thinking about the customers very different. Also to ensure liquidity to the customers. But customers has put a different valiance to some of these things so company is also assisting what is customer want and right now company focus is substantially giving value to various different ways . The EATM was an offering in that direction in which company can get 50,000 at the time of selling shares in next 30 minutes. So company is giving different value of to customers in terms of knowledge , service, pricing or liquidity.

Does sequentially does company active clients have gone up ?

Active clients have gone up from 1.2 million to about 1.22 million.

Does the 30 % decline in yields in mutual funds is regard to FY18 if the industry is at 100 basis point so it will go to 70 basis point by FY20 ?

Yes

Kindly Elaborate on the loyalty program how will it pan out ? What was ADP of reserve in terms of equity and derivatives segment ?

Under loyalty company will be come up with membership type of program which will allow customer to benefit from different services from the company. Customer will be doing similar for all sets of customers who traces for this business but there was lot of progress in the strategic initiatives but again company will continue to do that overcoming quarter as well.

Total ADP for the company was 530 billion overall. Breakup in Derivative and equity will be similar as industry of 95-96 %.

Does company is moving from distribution to direct going forward ?

No company is moving from distribution to advisory to only with ultra HNI client. The service like the advice to control on portfolio that combination is merits a fee base structure . With a soft launch company do believe that there is a good case for product like this. It will help company to grow business with HNI clients. It also give open architecture for incase of HNI the whole difficulty of moving between fund even if customer go direct it become very easy for customer.

How is the attraction seen in EATM materially and how company is financing the FLOAT that company is providing to the customer ?

EATM has been very well appreciated in the market so it has got customer Delight. In terms of actual number they have grown well. This product was offered exclusively on BSE to begin with so there also growth is influence by the volume over there.

It will be financed by the company so there is a CAP of 50,000 which put for customers. Discussions are going on to launch it on NSE on this front.

I expect flat fee trading (For eg. Rs. 200 per trade etc as brokerage) becoming norm in next 2 years for no frills customers (without any advisory, research support)

If big name brokerage like Charles Schwab have started offering free trading for its customers, I think its only question of time when it will come to India. It is already there with smaller players like Zerodha etc.

So all of the above will bring in more clients but will put big pressure on margins of all brokerage firms in India. Clearly negative for ICICI Securities.

Can’t say free trading but yes, brokerage free trading has definitely come to India. Commission free brokers like Finvasia, Wisdom Capital allow traders to trade all segments for absolutely zero brokerage. Discount brokers definitely will have to face a hard competition in future.

ICICI Securities has had a very sharp correction in the last 2 months. From a price fall perspective I-Sec looks attractive. Though returns ratios and margins are very good, a 4% CAGR revenue growth over the last 11 quarters does not seem sufficient to move the needle on already high margins and return ratios. Unless there is a meaningful top line growth, I feel I-Sec could at best be a value trap. Happy for any alternate views

Regards

Disc: Not invested in I-Sec, Looking at investing in I-Sec

Nitin Kamat from Zerodha said he is not worried about old players getting into discount broking but he will worried about players like Paytm and others who will enter fresh as they can come with disrupting and aggressive plans and technology from fresh.

I was checking Bajaj Securities and the pricing it seems they are charging less than Zerodha in F&O trade

Bajaj securities charging F&O trade 9 per order

Zerodha charges 20 per order

Though delivery charges for bajaj sec is 0.99/ order and Zerodha has no charges for delivery. But I think majority of the volume is generated in F&O segment.

I was reading after Manish Sonthalia recommended ICICI sec in yesterdays ETNOW webinar stating that cost of compliance for many small broker will make the industry consolidate and big 10-15 brokers will have all the market. After Karvy fiasco customers will move away from small brokers and move to reputed names. He also said its a platform business where cost is minimum and volume growth can be immense though margins would come down.

I was using ICICI Direct earlier and shifted to Zerodha. Apart from 0 delivery brokerage, I personally love Zerodha’s platform and I think it is simpler and much better than ICICI Direct. Apart from this , they keep of adding new functionality for traders and investors e.g. Sensibull for option trading, Coin for Direct MF purchase, Smallcase of portfolio advisory etc.

i have been recently tracking this stock. I witness the company is meeting institutional investors every other day, i also understand that sooner or later the ICICI Bank block will come to market to bring down their shareholding below 75%. Are such frequent investor meets a regular feature for this company or is the ICICI block coming soon?

ICICI Securities - Annual Report: Focus on a one-stop financial intermediary

ISEC’s Annual Report offers insights into the company’s strategy on five key

points:

creating scale,

increasing ARPU,

improving customer

experience,

increasing digitization, and

further improving operational efficiency. Initiatives such as the formal tie-up with ICICIB and subscription plans (Prime and Prepaid) have resulted in the number of active/NSE-active

clients growing 16%/27% to 1.4m/1.0m.

The company increased its market share in terms of NSE-active clients by 40bp to 10%. While the Distribution segment is facing some challenges, we believe it should stabilize in the near term.

With cost-cutting going well, we expect a 400bp reduction in the C/I ratio to 52% by FY23E, resulting in 19% PAT CAGR.

Recent regulatory changes are likely to accelerate consolidation in the industry, and ISEC is expected to be a major beneficiary of the same.

Good results by Angel broking, looks like financialization theme has accelerated in last few quarters( MF are different animal but Brokers are in for a sustainable growth)

ISEC to likely report good numbers,

Patterns visible

Industry consolidation with smaller players losing to bigger players

Tech adoption making it covid immune,

Financialization theme tilting towards equity broadly and within segment higher focus on direct equity

Operating leverage visible with platform enabled transactions

Initiated tracking position in ISEC and Angle - basket approach

Outstanding result as expected in above post, YoY Qtrly revenue up by 50%+, Profit over 100%, operating leverage visible with operating margin expansion by 9%. QoQ performance equally impressive

All product lines delivering well, with sept qtr eps at 8.63 and half year around 15, for full year 30+ eps looks doable and at current PE ratio of 25, it looks all set to do well ( possible rerating as well)

Add with other ingredients of high RoCE, low/negative working capital, high dividend payout and a business which generate sizable free cash flow. Operating leverage playing out with underneath digital platforms giving non linear scale( more so in case of pure play broking houses such as Angel).

These businesses exhibit pseudo consumer tech platform characteristics IMO and for now seems better placed then AMC stocks( with direct equity catching fancy). Best part is rapid growth at real profit and cash flows, unlike cash guzzling fintech players.

If you listen to Angel concall - Digital word is used in almost every other response by management. They seemed too eager on that front…

Incremental user base addition Sustainability is the biggest lever, both icici security and Angel have called out trend as sustainable - organic and at cost of tail end players.

Would be of value to hear thoughts from @zygo23554 and other fellow VPers. Performance sustainability/ industry landscape/ risks…

Disc: Added Angel and ISEC recently and plan to add more. Also invested in HDFC AMC