Story

ICICI Securities is the largest retail broker in India and operates popular ICICIDirect.com website. 63% of total revenue come from broking business, 90% of which comes from retail clients. As of March 2018, ICICIdirect had approximately 40 lakh operational accounts of whom 8 lakhs had traded on NSE in the preceding 12 months.

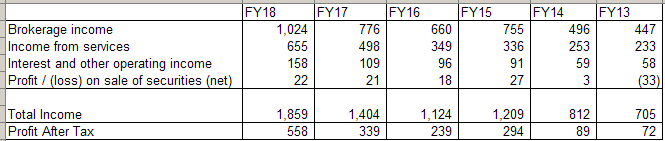

Sources of Income

Source: IPO Prospectus and FY 18 Earnings release.

Brokerage income consists of brokerage services offered to retail customers and institutional clients for trading equities, equity derivatives, currency derivatives, ETFs and overseas securities.

Income from services consists of commission from distribution of MF, life insurance and other financial products and fee income from advisory services.

Interest and other operating income consists of interest earned on bank fixed deposits held with exchanges as margin for brokerage business, interest earned on margin funding and interest earned on trade receivables.

Profit on sales of securities is the result of proprietary trading business.

Company’s classification of revenue is somewhat confusing as different terms are used in income statement, MD&A in RHP, segment results and results press release. Here is the summary if various business (totals may not add up due to differences in terminology).

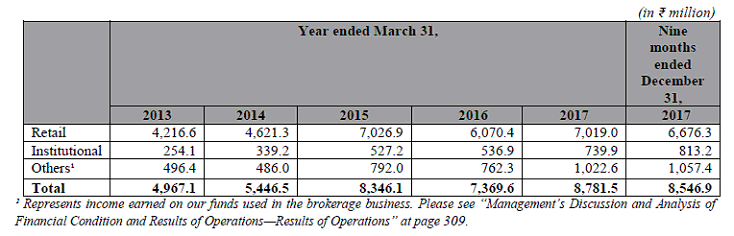

Brokerage Business

Broking business is operated by 200 of own branches, about 2600 branches of ICICI Bank and 4600 sub-brokers and authorized persons. Over the years share of revenue from broking business has come down from 90% to 63% as other sources of revenue like mutual fund distribution, advisory, investment banking are growing.

Source: IPO Prospectus

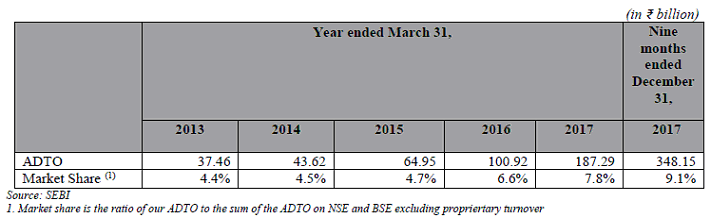

Company has steadily gained market share in trading business.

Source: IPO Prospectus

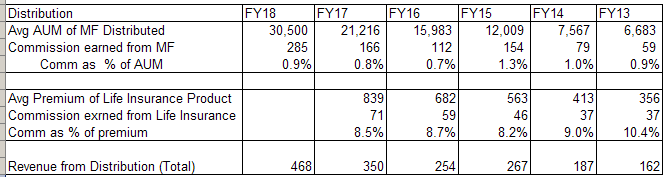

Distribution Business

ICICI Securities is the second largest non-bank mutual fund distributor in India. It distributes third-party mutual funds, insurance products, fixed deposits, loans and pension products to retail customers for commission income. Except insurance products, company does not distinguish between the third-party partners whose products it distributes based on affiliation. Company earns recurring commissions for longer-term products.

Here are some key statistics of distribution business.

Source: IPO Prospectus and FY 18 Earnings release.

Investment Banking

investment banking business consists of equity capital markets services and financial advisory services that cater to corporate clients, the government and financial sponsors.

![]()

Source: IPO Prospectus and FY 18 Earnings release.

Treasury and Trading

Under treasury and trading business company manage treasury assets and engage in proprietary trading.

![]()

Source: IPO Prospectus and FY 18 Earnings release.

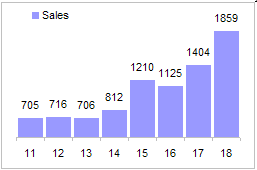

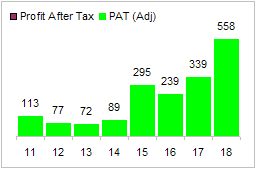

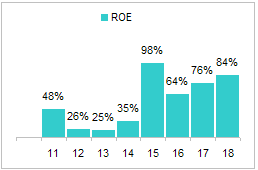

Charts

Source: IPO Prospectus and Capitaline.

During years of 2011 to 2014, equity markets were subdued and company’s revenue and PAT stagnated. Profits are on high gear since FY 2015 when current equity rally has began.

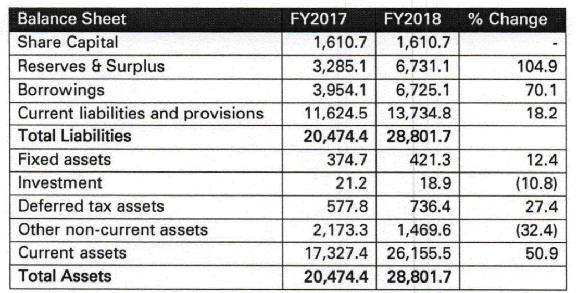

Balance sheet

Source: IPO Prospectus and FY 18 Earnings release.

Company has a strong balance sheet with no long term debt. The borrowings are largely for margin funding business. Company does not need any fixed assets and most of the current assets are held in the form cash or margin deposit with exchanges. Company earns interest income on these assets.

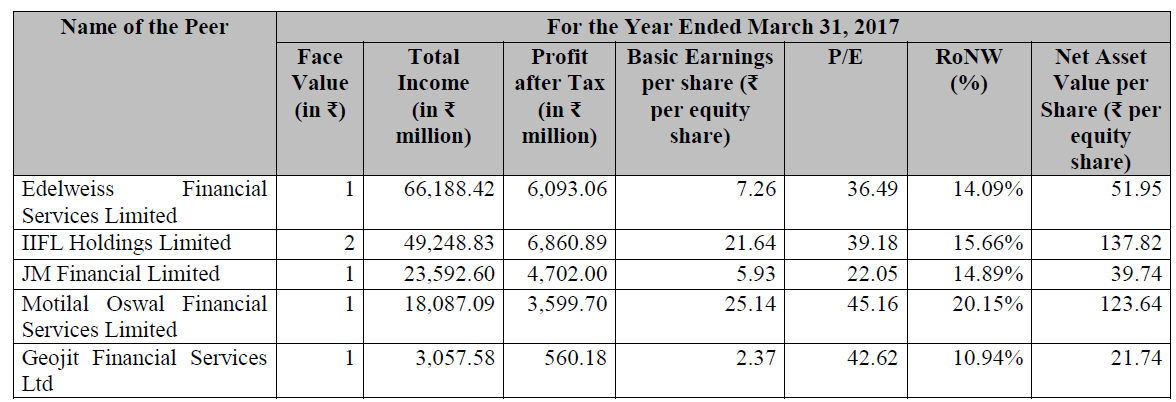

Peer Comparison

ICICI Securities is a pure-play broking and commission business and fund based revenue is minimal at present. Most of the peers earn a substantial portion of their revenue from funding activities and consequently have leveraged balance sheets, low ROE, lower operating leverage and high financial leverage.

Source: IPO Prospectus

Investment Rationale

Increasing Domestic Participation in Equity Markets

Indian markets until recently were dominated by FIIs. Over the last years, DIIs mainly mutual funds and retail investors have been a growing influence in the markets. This has resulted in diversity of opinions, lower volatility and increased depth of equity markets.

Strong macroeconomic factors such as growing gross domestic product, rising affluence, increasing formalization of economy, lower inflation and falling interest rates have contributed to the growing shift of household savings towards financial assets. Consequently, India is witnessing increasing retail and domestic institutional participation in Indian equity markets.

Growing share of financial assets

Household savings are increasingly shifting from physical assets to financial assets. The share of financial savings as a proportion of household savings has increased steadily from 31.1% in fiscal 2012 to 41.5% in fiscal 2016. The share of financial savings is likely to rise further, as stable inflationary trend is generally expected to diminish the behavior of physical savings such as investments in gold and real estate. In the past, positive real income growth and low inflation have had a positive effect on financial savings. According to CRISIL Research, the yields on 10-year Indian Government securities have reduced from 7.4% in April 2016 to 6.9% in October 2017 (Source: RBI). This falling interest rate cycle has helped channel higher investments towards equity instruments.

Leadership Position in brokerage business

ICICI Securities is the largest broker in India and is well placed to capitalize on the growing equity markets in India.

Margin Funding to grow

SEBI last year allowed brokers to offer margin funding. ICICI Securities has started offering margin funding and as of FY 18 has a funding portfolio of 556 Cr. Although small at the moment, this can grow over next few years.

Share of non-broking business growing

Share of non-broking business has grown from 10% in FY 13 to 35% in FY 18. This has resulted in lower cyclicality. This trend is likely continued further.

Highly profitable operations

Over last 3 years company has earned average ROE of 75%. Company distributes 50% of profits as dividends. Even at the bottom of the cycle, company has earned 25% ROE, more than what peers earn at top of the cycle.

Valuation

ICICI Bank came out with an offer for sale in March 2018 for Rs 520 a share valuing the company at 16,765 Cr or about 30 times TTM eps of 15. However, due to subdued market conditions at that time, IPO was undersubscribed and stock listed at 14% discount to offer price. Company is currently (April 21 2018) trading at 18% discount to offer price at Rs 425 or about 25 times FY 18 earnings. Given high ROE, leadership position, and growth prospects of the industry, this valuation appears to be fair. Cyclical nature of the business and current stage in the cycle will prevent any expansion of the PE ratio. Future returns are likely to come from earnings expansion.

At current price, dividend yield works out to be healthy 2%. Given the high profitability, company generates enough internal accruals to fund growth and pay decent amount of dividend.

Risks:

- Business is highly cyclical as revenue and volume of business both depend on level of equity indices while costs are fixed.

- Company has high operating leverage. A rise in revenue will directly flow to bottom line but a drop in revenue will also directly to flow to bottom line as costs are largely fixed. Over time, costs are likely to rise while revenue may drop occasionally depending on market conditions. In such a scenario, PAT can drop substantially.

- Company could be at a cyclical high right now and revenue and PAT could drop in next couple of years if markets drop.

- ICICI is one of the most expensive brokers in India for retail customers. Company will face stiff competition from discount brokers. Company has managed to retain its pricing structure even when discount brokers have grown in last 3-4 years.

- ICICI Securities competes with ICICI Bank for distribution of mutual funds and other services.

- Almost 75% of accounts on ICICIDirect are non-operational.

- Business is highly regulated.

Disclosure: No position but interested. Views are welcome.