All these stalwarts in broking business are going to die soon unless they consolidate

User experience of opening an account with Zerohda, UpStox (funded by Tatas) , there is a rumor Kotak is about to launch its own discount broking platform (they already have their own 3 in 1 like other bigges )

All these nice reports, views and research reports are icing on the cake, all these reports are freely available for a serious investor on many sites like market mojo, trendlyne etc…, on top of that the investing community on social media (including this VP space) you look for it you will find it. So these additional features are icing on the cake.

There is a famous add of Maruthi Yacht - after listening all the features the buyer asks "Kitna deta hai (Mileage )

Biggest disadvantage of ICICI is they lost the first mover advantage they didn’t see the threat coming and eating their share year after year. Now Upstox is second highest just behind Zerodha. (The same discussion happening on cams in another thread, they are also having that barrier for now - FOR NOW )

There is also another Myth the discounted brokers cannot survive in the longer run. Zerodha completed 10 years and it is profitable and from the recent update from Mr Kamath we can understand they give ESOPS to the staff and allow them to sell them if they want at a very good premium.

ICICI Securities is learning. It came out with prime plans where you get reduced brokerage % when you pay some fixed sum. For example 900Rs prime plan would bring down brokerage from 0.55% to .25% and by paying Rs 9500, you can get brokerage reduced to 0.15%. Also they have made their prepaid brokerage plan attractive under which if you prepay Rs 150,000 (plus GST), they will charge only 0.09% brokerage (and will refund you prepaid amount over a period of time). The best earlier was prepaid of Rs 200,000+GST and brokerage of 0.15%.

Although the brokerage is still higher than discount brokers like Zerodha, they are moving in right direction. With all due respect to Zerodha, there are few investors like me who are ready to pay some premium for comfort of big bank/brand backing my demat/trading account. Its just an individual thing, I guess. ICICI is now reducing the cost difference between themselves and discount brokers, making it attractive for some customers to stay with them longer (I was thinking of leaving them earlier)

But this also means lower margins of similar volume of business. So new customer acquisition is the only mode to compensate for the losses by lowering brokerage.

The biggest problem of ICICISECURITIES or the best feature of ZERODHA is that in ICICI we need to add margin for individual derivative positions. In Zerodha the margin requirements are consolidated. I used to do derivatives in ICICI long time back. But Zerodha is much more convenient. So icicidirect will continue to lose traders over the long term. I still use the margin features of icicidirect delivery. I think because Icici also has a bank they can support margin buy and sell in delivery.

update on competition : Mumbai, November 26, 2020: In a boost to the investing prowess of the Indian retail investors, Angel Broking

has opened itself to API integration via SmartAPI. The free-to-integrate feature enables any platform,

including startups and stock advisories, to execute real-time trades via Angel Broking while also empowering

algo traders to deploy their programs in 5 programming languages.

At present, the platform supports Python, Nodejs, Java, R, Go. SmartAPI has paved the way for the

development of end-to-end trading services for over 2.83mn Angel Broking customers (as of Oct’20).

Believe Zetodha charges for API access, Angel has taken them head on.

ICICI security is way behind tech focused platforms but they have their own set of customers and relevant offerings.

Tail end brokers likely to see consolidation wave, quite interesting space to see how tech is truly transforming industry and reaction by each of top players.

Invested in ICICI security and Angle - tracking positions

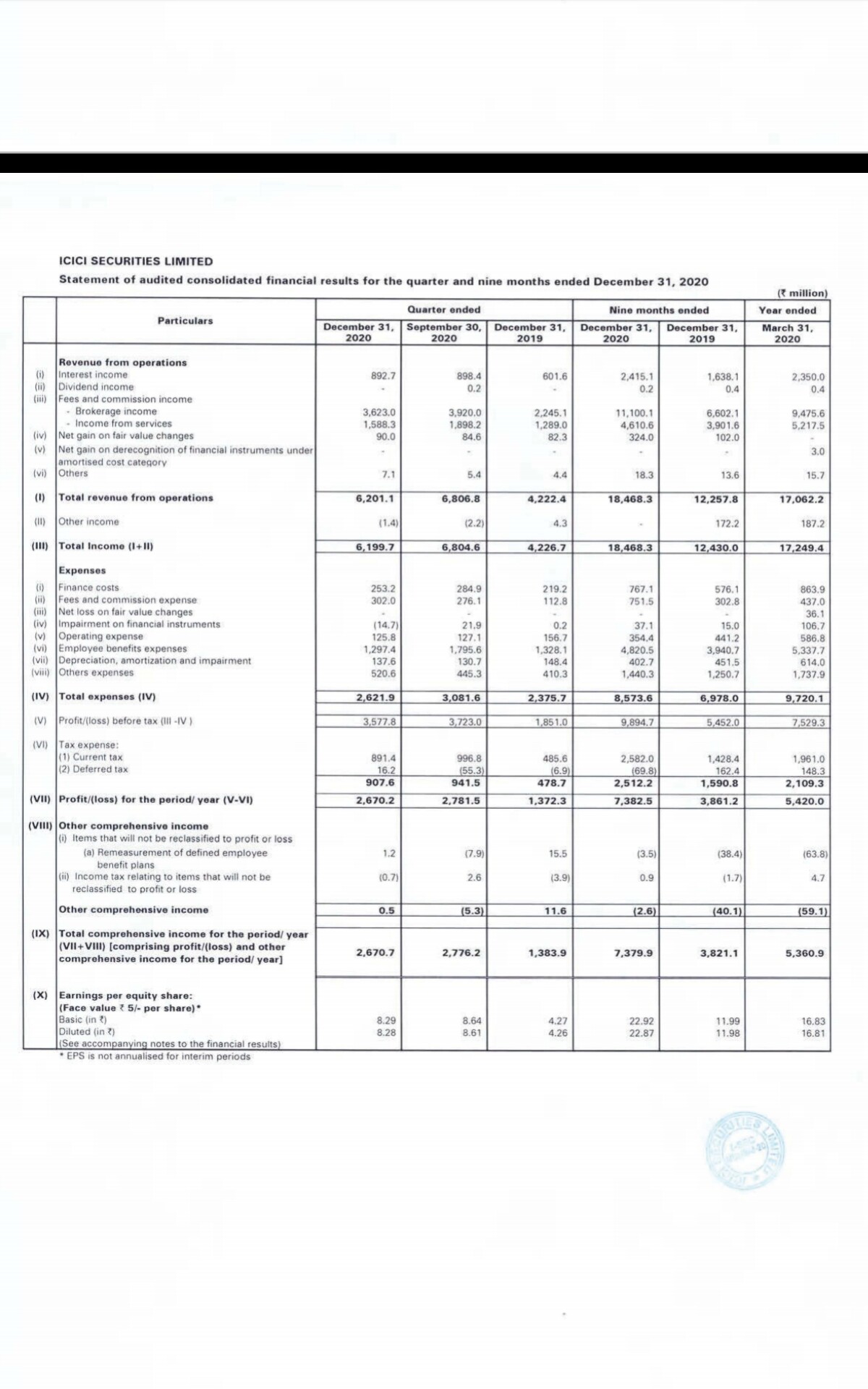

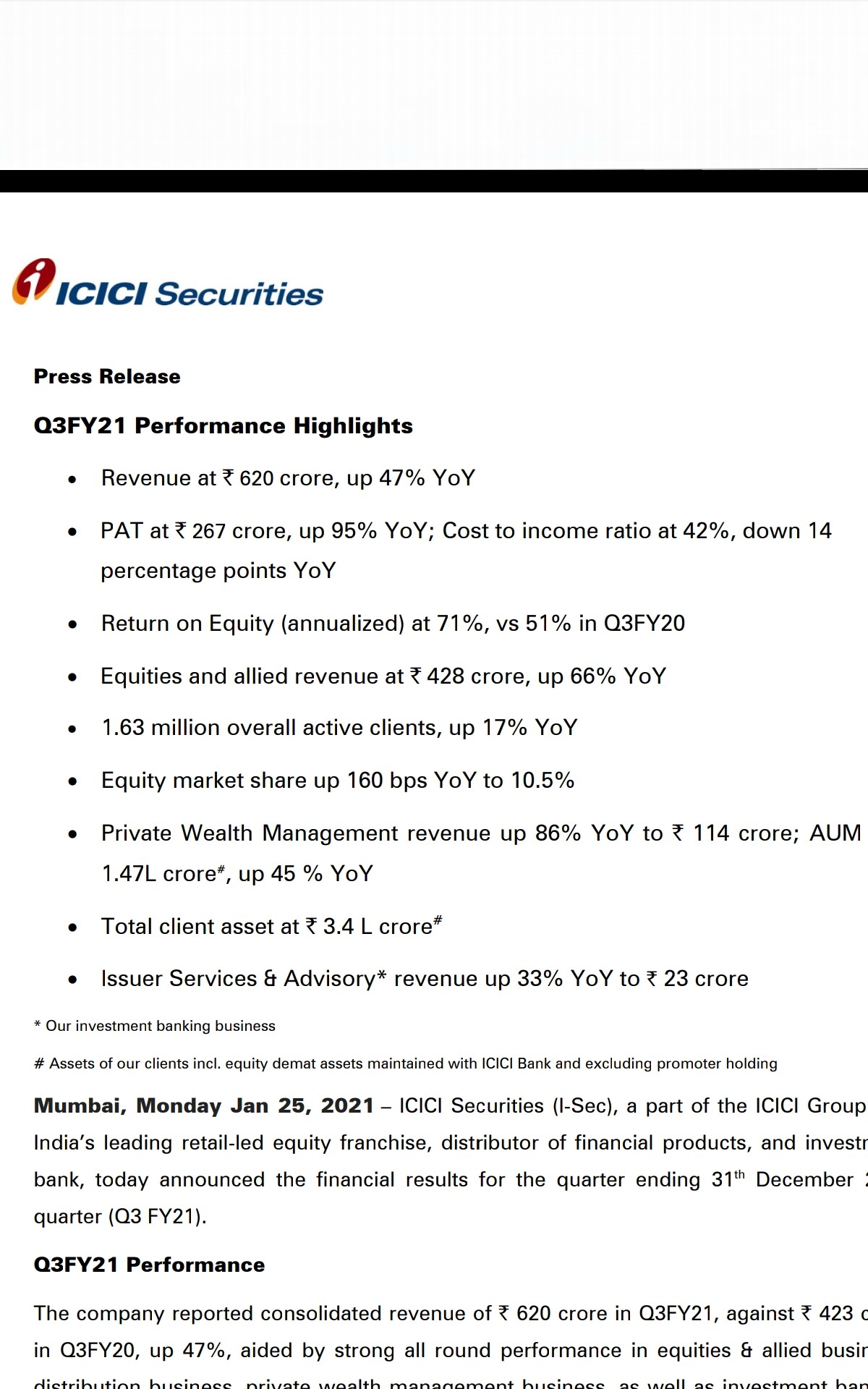

Good performance continues, reassuring to see all business lines performin well, operating leverage playing out with substantial margin improvement. YoY and 9month stands excellent.

QoQ slight revenue dip, on expected lines, profit less impacted with cost effectiveness.

This industry is a clear exception with no attempts to show any buying interest even in today’s huge rally.

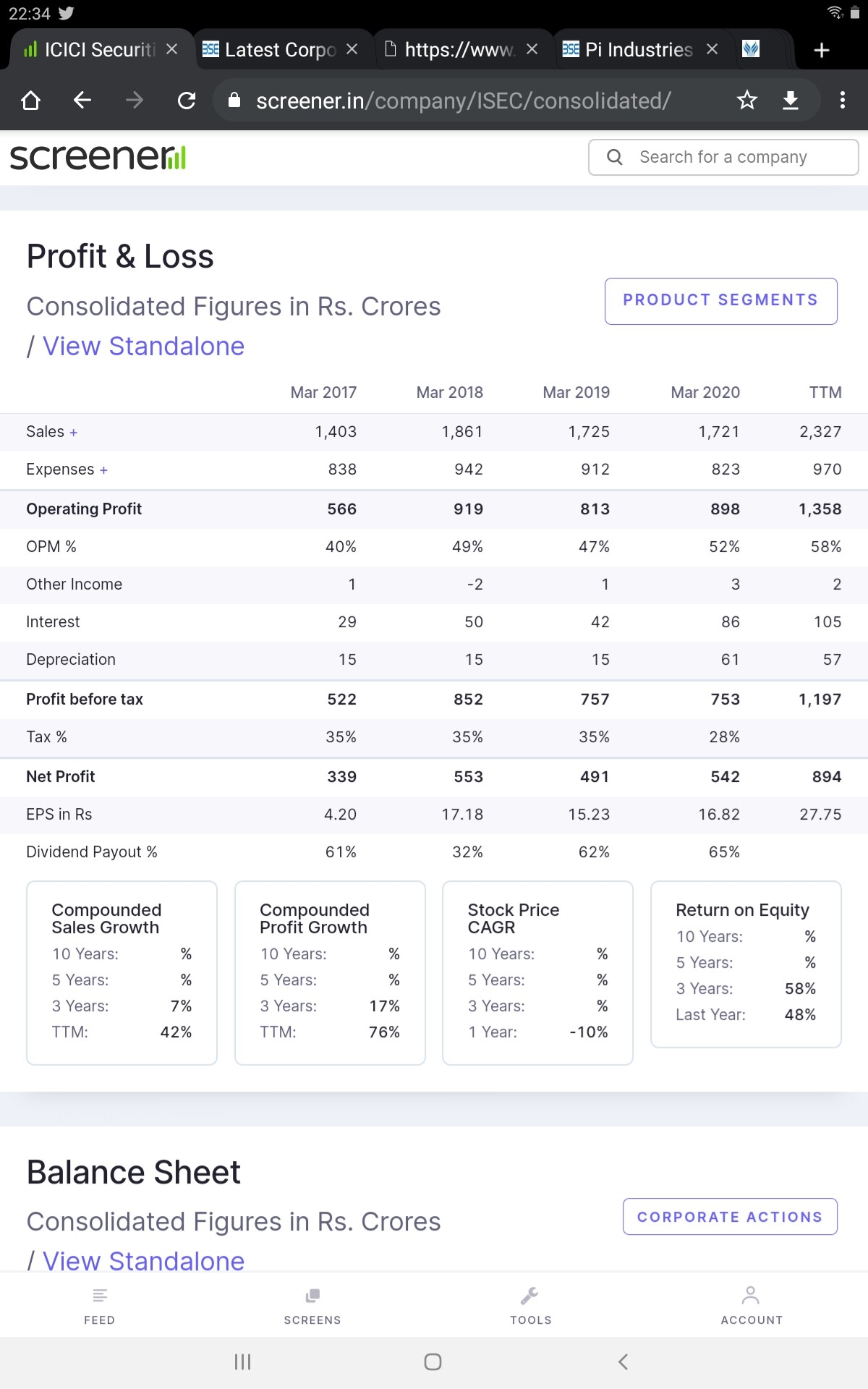

We have a very high op margin ( increasing every year), with operating leverage visible and solid sales growth business available closer to single pe ratio.( considering cash)

Covid has got huge customers on boarded and they may not be active once things normalize — QoQ numbers do not show any dramatic fall yet, infact mild rev drop but margins increased. Maybe Q4 will show a better sustainability trend.

Cutthroat discount in broking business, it has bottomed out on pricing and can’t go any lower with near zero prices, and this is still very high margin cash generating business. — Maybe mkt will like to see QoQ trend with lower customer addition/drop outs.

ISEC has multiple revenue lines and each performing well, a strong parentage and would benefit once some consolidation plays in industry or when new addition dries up and small players feel heat.

Invested as tracking position - sense the story is structural shift - only time will tell - risk reward is favorable though looks week on charts

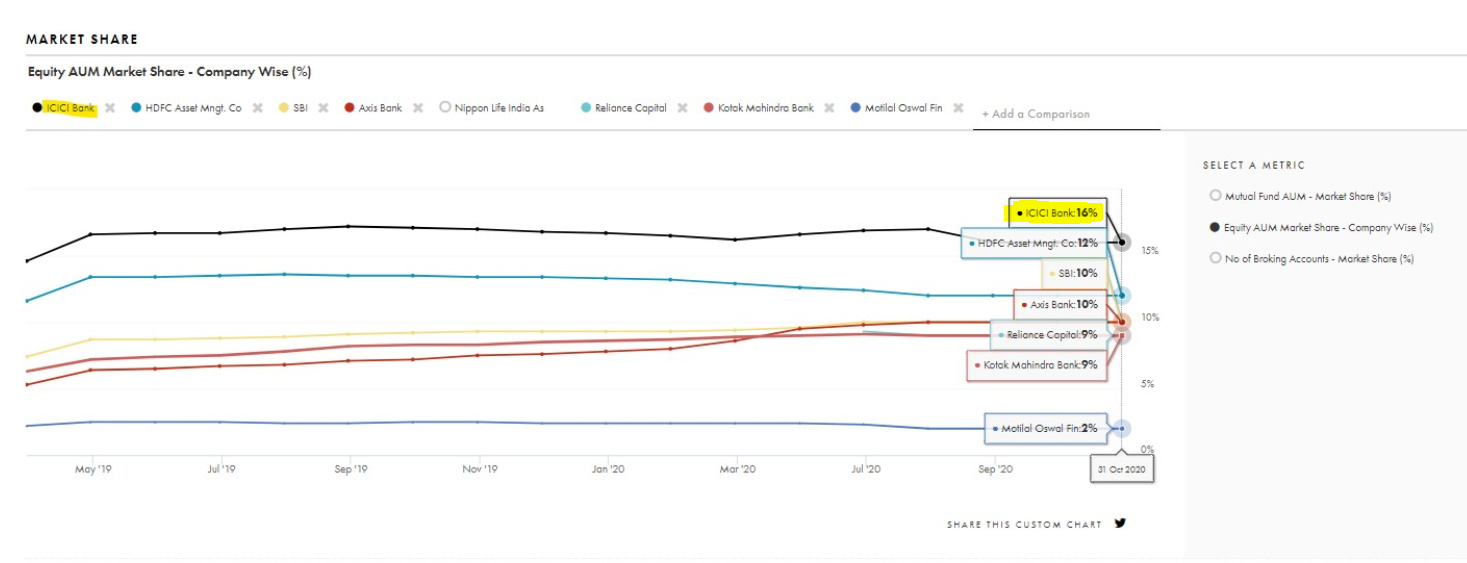

ICICI Direct at third place in terms of active clients. Last quarter Angel Broking had taken over ICICI but now they at fourth position.

If this trend continues it could be a really good sign for ISec. This sudden change seems to happen due to their change in product mix, especially the new NEO plan.

I have my 3 in one ICICI direct account since last 10 years…

I had tried a couple of discount brokers in the past with a view to save on brokerage on stocks and mutual funds.

But somehow , I was not happy with the new-age brokerage systems and processes … so called discount brokers. e g. While doing investment through Paytm money, 3 transactions failed in a total of 10 transactions. When the transaction failed, money was debited to me, MF units were not bought , and my money stuck in the system for 4 days…where as with icici sec, with thousands transaction, there was not a single instance where transaction failed, and my money was stuck.

So decided to stay with Isec.

Duscl: Invested @360 level…may be biased. Please do your own assessment before investing

• New clients acquired during Q4 were at 3.54 lac vs QoQ 1.39 lac & YoY 1.06 lac mainly led by focus on digital strategy.

• Share of client sourcing from ICICI Bank has declined from historical level of 80% to less than 45% in Q4FY21. Digital sourcing has been the key contributor to increase in clients in Q4FY21.

• Active clients were at 19.1 lac vs QoQ 16.3 lac & YoY 14.8 lac.

• Market share in equity (cash intraday & delivery) is at 9.6% vs QoQ 10.5% & YoY 9.1%. Market share in derivatives was at 3.0% vs QoQ 6.3% & YoY 8.0%. Despite loss in market share on QoQ basis, the co posted strong revenue growth of 16% QoQ in brokerage segment, this is because of reduced business in the low yield intraday segment while the high yield cash delivery segment continued to do well.

• Revenue contribution of equity (cash intraday + delivery) is more than 50% for the co while derivatives is less than 50%. Contribution of delivery within equity (cash intraday + delivery) revenue is more than 50% for the co.

• Co believes tracking derivative market share will not have any meaning as that wont have any bearing on the revenue, especially since the co has launched the Neo scheme (identical to discount broking schemes)

• Regarding Neo product, co is looking at a customer as an avenue for cross selling multiple products over next many years and not as a trading brokerage generator in immediate term as is the approach adopted by the new discount brokers.

• 2nd phase of new margin rules started from March. Despite this, equity ADTO in March was at the same level as it was in Nov (before the new rules), while derivatives ADTO was higher than Nov. However compared to Feb, there was a decline.

• Co has been offering new propositions to attract customers like - Global investing platform, Lowest MTF rate of 8.9%. Co has a market share of 20% in MTF.

• Cost to income has declined to 40% vs QoQ 42% and YoY 57%. Co expects it to stabilize in between 40-50%.

• Announced final dividend of Rs. 13.5 per share.