While the video is informative, I completely disagree on the valuation part. If we start assuming that this stock will eventually trade at 13x PE in 4-5 years timeframe, each and every decent business in India would look expensive on similar parameters. India as a country and insurance industry in particular has large growth runway. Till India’s GDP keeps growing above the world average and any company’s earnings and cash flow keep growing at decent rate, such steep PE contraction is unlikely on sustainable basis. If one applies such valuation framework on quality stocks having good growth visibility, one would certainly miss these and will be left with lots of value traps. Analyzing earnings and cash flow growth potential is most important, instead of worrying much about 5-10% lower entry point.

Two quotes from Motilal Oswal’s 25th wealth creation study:

“Time is a friend of good companies and enemy of bad companies. In 25 years, successful companies grow to unimaginable levels in sales, profits and market cap.”

“Stock returns are slaves of earnings power and growth. In the very long run, valuations

matter less.”

The video is quite biased and valuation is considered on a few assumptions made. While doing valuation he doesn’t consider inorganic growth, interest cycle, rise in insurance premium etc. (even a 0.25% change in interest rates makes a huge difference).

In the end, the markets are never efficient and valuations won’t be just on the textbook method.

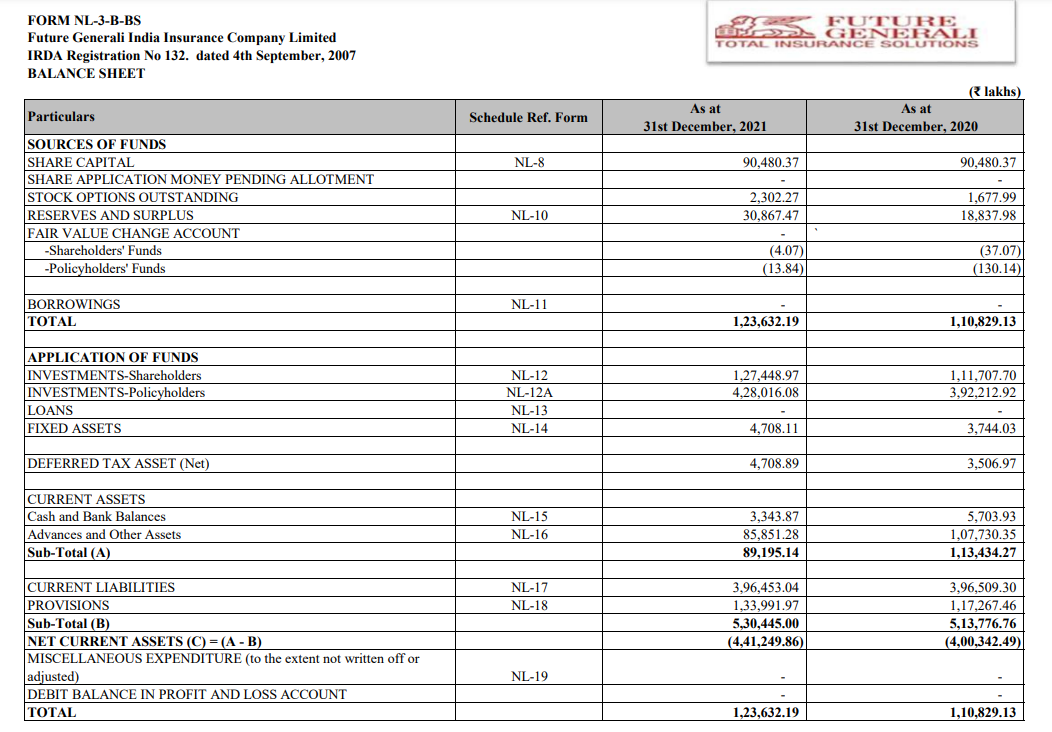

Italy’s top insurer Generali said on Friday it had completed the acquisition of 25% stake in its Indian non-life insurance joint venture, increasing its holding to 74%. Generali said it had agreed to pay 145 million euros ($153 million) to debt-laden Future Group, its partner in Future Generali India Insurance (FGII), for the stake.

$153 Million = 1,150 Crs for 25% stake.

Total Valuation of the business = 4,600 Crs

As of Dec 2021, networth of Future Generali General Insurance was Rs. 1,236 Crs.

Recently IRDAI has announced that life insurers can now sell full fledged health insurance plans. Previously most of the health insurance were part of the general insurance division. How this will affect pure play general insurance companies like ICICI Lombard… Now ICICI LOMBARD will have competition from life insurance companies like LIC and their own sister concer life insurance division ( ICICI Pru life)…

Definitely ICICI Pru will launch their own health insurance products

When it comes to Banca partner ICICI BANK. Whom they would refer incase if cross selling health insurance…

Will they have conflict of interest between both life and general insurance arms…

Are there any possibilities of merging both the arm to form one single insurance company?

Health insurance is not a very attractive proposition for banks.

Annual rollover of policies as opposed to long time commitment in the case of life insurance

Lower premium as opposed to a ULIP where a customer signs up to invest 50K every year. Lower premium amount automatically results in lower commission

The bulk market is always directly covered by the health insurer sales teams themselves. Group health is an institutional sales model

The average health insurance premium for a 35 year old is less than 10K per year for a 5L annual cover, even at 10% commission the intermediary will hardly earn 1K per policy.

Selling health policies through banks will not be easy. There is just too much sales effort involved for banks to take this seriously irrespective of what IRDAI says.

If life Insurers are allowed to sell Health Insurance products, specially Mediclaim, then it will have huge impact on current Health insurer. The most adverse effect will be on Star Health as most of Star Health agents are from LIC of India agents. Once LIC themselves start Mediclaim all these 12 lakh LIC agents will sell LIC mediclaim Instead of Star Health and Care Mediclaim.

Currently Even ULIP Plans have commission ranging from 2 % to 10% only. Gone are the days of 25 to 35% commission still Bank people are selling ULIPS aggressively then they will surely sell Mediclaim where commission rate is 15 % ( not 10%) Also there are other Fringe benefits and competitions by which another 5 to 10 % is given indirectly.So it still is quite attractive compared to mutual funds and Ulip products for Banks

also average premium for age 35 with wife and 2 kids …family floater, the premium is around 25,000…which is quite considerable and worth pursuing for product

With health insurance you end up selling every year since health insurance goes up with age. In life insurance customer commits to a single premium or regular annual payment for 7-10 years. Sell a single premium policy and you get the fat commission to meet your monthly revenue target.

Life insurance is a product that gets clubbed with investment, customers do not see it as a pure expense. Banks don’t sell too many pure life cover plans for this reason. With health insurance, it is seen as a pure play expense since there is no return expected on this. This is a much tougher proposition to sell for the average privilege banker who hardly has 2-3 years experience.

Banks may sell but they will prioritize life insurance over health insurance any day. Life insurance is also a much bigger market annually that is general insurance. ICICI Lombard has GDPI of ~16,000 Cr annually while SBI Life does more than that every quarter because of the higher renewal premium component.

Rather this increase in premium of mediclaim works in favour of companies. In life insurance, premium remains same for 20-30 years, while mediclaim premium increases due to 3 factors

due to client entering the next age band

companies increasing the premium arbitrarily

Govt increasing GST

Due to frequent increase in premium, the commission also increase and thus it motivates banks to sell mediclaim more. Also mediclaim can be easily portable every year and currently IRDA has allowed banks to sell mediclaim of 9 different companies, thus if client is not happy with claims of one company, bank ppl have the option of 8 other companies to port his policies, this will increase the stickiness of clients.

Also due to covid pandemic, awareness of mediclaim has been very high among public and they have realised that even though mediclaim is an expense, still its now under essential category of purchases.

Also there are seperate sections of Income tax rebate of 80D and 80 D(D) of Income Tax Act which also motivates ppl to purchase mediclaim, while in case of life Insurance there is just 80C of 1.5 lakhs which is anyways exhausted by PF, PPF and housing loan principle , and hence no more an attractive factor to purchase life insurance.

Here is the data from the IRDA Annual Report 2021 -

Within Life Insurance - Individual segment

LIC gets 93% NBP from agents

Private Insurers get 54% NBP from banks

Within Health Insurance as a segment

Banks bring in just 8% of the individual premium

Agents bring in 74% of the individual premium

Banks bring in 12% of the group premium

Brokers like Marsh, Aon Hewitt bring in 45% of the group premium

Overall market size -

Life Insurance premium for FY21 - 6,28,000 Cr

Life Private sector premium for FY21 - 2,25,000 Cr

Health Insurance premium for FY21 - 63,700 Cr

Health (private + standalone health) premium for FY21 - 35,000 Cr

Banks bring in ~1,20,000 Cr p.a. premium for private life insurers

Banks bring in hardly 3,500 Cr p.a premium for private health insurers at best

That is a ratio of 34:1 at the premium level, now translate this into fee income for the bank

Also divide this by the number of branches to get branch level throughput

Then divide that number by 3 to get per privilege banker throughput

Then evaluate one time sale effort Vs annual sales effort for Life insurance Vs Health insurance

I think we have to wait and see the impact. Primarily, the life insurers have couple of large synergies selling health: same distribution network (agents) and same customer. However, they still start with a massive disadvantage. Indemnity health insurance is a fundamentally different product than life. Lot more service oriented vs life which is more sales oriented. SAHIs have built their service networks over time:

Large network of hospitals servicing claims. Ability to do cashless claims at these hospitals. Further, due to the large volume of treatment coming through a large insurer such as Star, they are able to negotiate better rates at these hospitals. Building this up will inevitably take time for any new entrant.

Inhouse claims servicing: helps in reducing frauds, identify right treatments and costs. Helped by data analytics due to large number of claims being serviced.

More volumes = more data around claims and underwriting = ability to underwrite better. We have partly seen this with Star even having policies for people with pre-existing diseases.

Given the above and given that as of now commissions to agents are capped at 15%, I dont see why any existing SAHI agent would chose to underwrite an indemnity policy from a life insurer rather than a SAHI such as Star.

It is likely that for a life insurer to be successful selling indemnity policies, they will have to endure underwriting losses (due to high claims and high opex initially) for many many years while they build up these capabilities. Obivously this is difficult to do in a public market setting. We also have to remember that life insurers were allowed to sell indemnity policies till a few years ago and were scarcely able to make a dent.

@zygo23554 I read through the entire thread and noticed that you invested sometime in 2020/early 2021. The price has remained flat at best if you are still invested.

Can you share your views on how you expect this to play out given that we ar in an increasing Interst rate environment ateast for the next 2-3 quarters.

Also curious if you have calculated the cost of float for icici lombard over the years? That alone will provide insights on the philosophy of the company - underwriting profitability or volume growth.

If the cost of float is significantly Below investment return then this becomes an intersting idea.

I saw alot of comments about investment book And reinvestment rates around 6-7 percent. I think the fine print is whats the effective rate for a corporate for 3-4 year old bond and the approx 15 percent equity that icici lombard is allowed to hold in the investment book.

Corp book is 50 percent , g secs are 30-35 percent and the rest is equity

Assuming that the equity book at 15 percent and gives 15 percent ( long term nifty return) then 2.25 percent of your targeted 6-7 percent is already delivered.

I think the effective return on the investment book is going to be higher than 7 percent

A few days ago, I was checking car insurance premium of a 16 year old car - 1100cc - hatchback. Previous policy was from Digit Insurance. Quotes given to me (direct purchase on website of the insurers): Digit: 4500+ (OD + TP), Acko - 2500 (didnt offer OD maybe due to age of the car). ICICIGI - 3000 (OD + TP). Ended up purchasing from ICICIGI. Experience was smooth and in a few clicks policy was sent over email. Had a few queries. Contacted customer care. Smooth experience so far with customer care too.

Also, I compared premium for a comprehensive cover of a few other car models recently purchased by my friends. I see the zero dep premiums to be 10-15% higher than Acko (which in my observation is the lowest premium player in the motor market).

Q3FY23 results show good growth in health segment. Auto is still flat but given above, I am optimistic for Auto growth to come in.

competition is fierce but ICICIGI seems to be standing tall with the offerings. I think as and when the insurance environment stabilises we can be assured that big names like ICICIGI should do really well as they have the bandwidth and reach