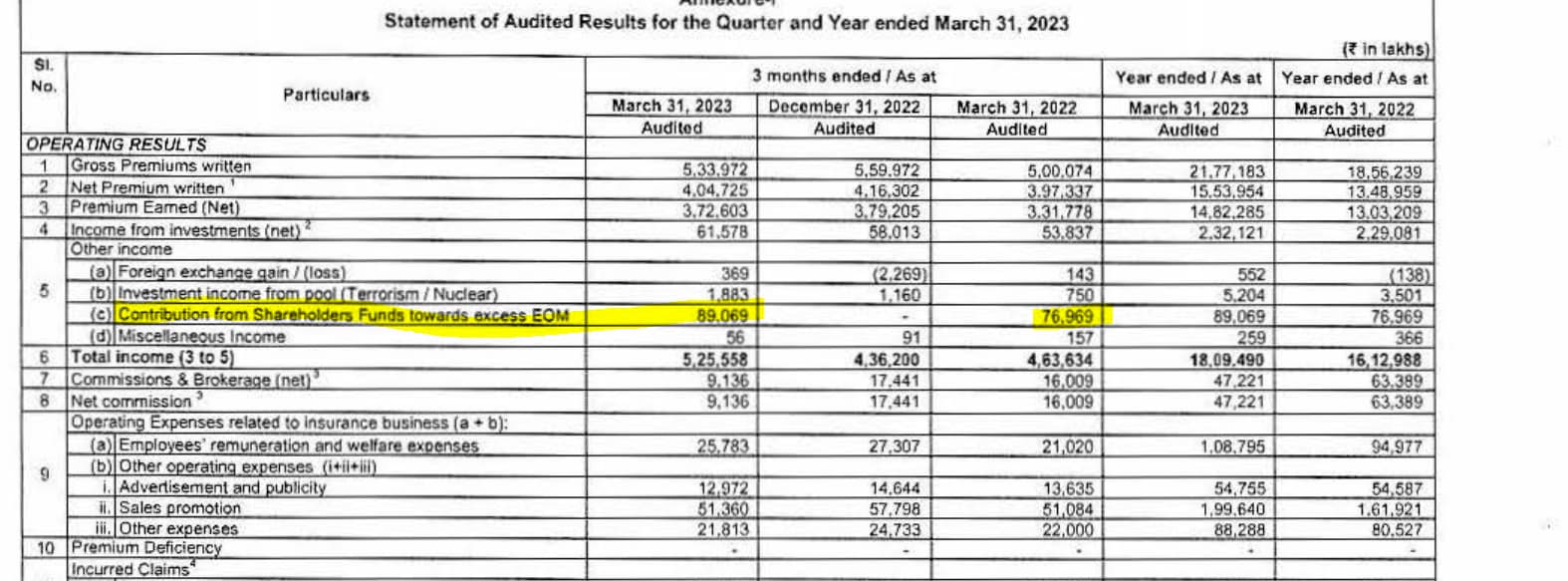

poor results, other income added to cover up the operational loss

As I can see ICICI Lombard has always reported loss at operational level in March quarters for 3 years, 2021, 2022 and 2023.

Is this common with all insurance companies OR Is this specific to ICICI Lombard?

Also, they report high Other Income in March quarter to cover up this loss. What is this Other Income and Is it always reported in March Quarter? My initial understanding was that this could be income from the Investment Portfolio of any insurance business, but I may be wrong. I am understanding this business only for last few months/quarters.

2 Likes

If you see the other income section in the financial statement, the other income is coming through “contribution from shareholders funds towards excess Expenses of Management (EoM)”

Insurers have set EoM levels as a percentage of the premiums they collect. This means that if premium collections are low, the allowable EoM levels will also be limited.

This excess expense should be charged to Shareholders account and thus you see this entry.

Investment income is not part of other income but still it also doesn’t show the true profit. An insurer may decide to go slow on volume because of low insurance rate; the earned premium may not be sufficient to cover the claims for that year and insurer might have to sell some investment to cover the claims.

2 Likes

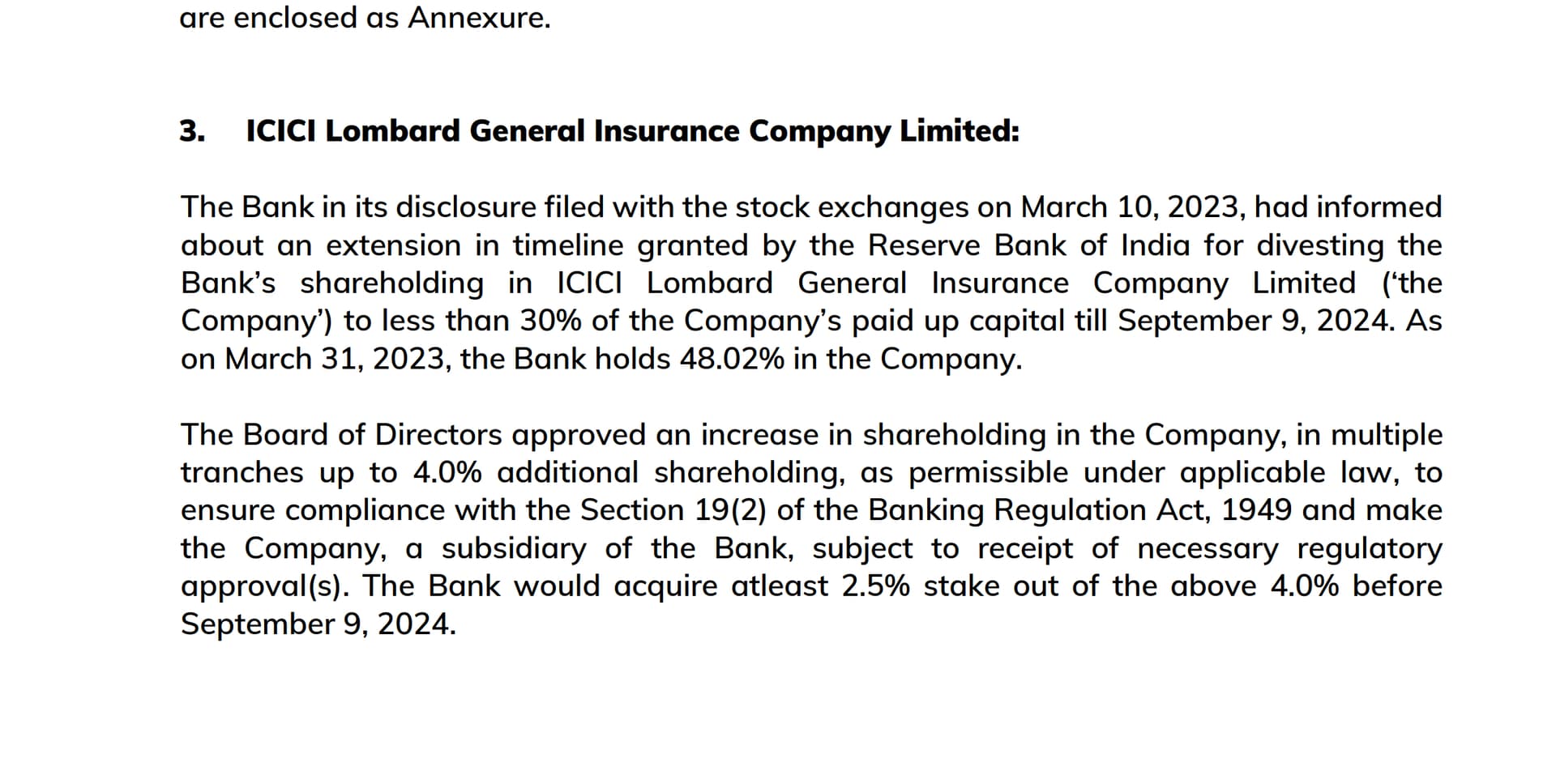

ICICI Bank board has approved to raise shareholding in ICICIGI by 4%. Earlier it was assumed that they will take take shareholding below 30% which would lead to a 18% stake sale.

4 Likes

Can anybody please explain this decision by ICICI? I am not able to understand the rational behind this decision. Why they have decided to increase the stake, while they are supposed to reduce it?

Also, why market has reacted so positively to this move?

Per RBI guidelines banks can have less than 30 % or 51% stake (or more) in their listed entities. In my opinion ICICI Bank was not able to exit as valuations were not decent, so they decided to acquire 4% of equity to comply with RBI rules.

Any alternate view is welcome.

1 Like

This actually strenthens ICICI bank a bit more as its now a subsidiary of ICICI Bank.

1 Like

I have a query on Combined Ratio (CR) being reported by General Insurance companies.

CR = Loss Ratio (LR) + Expense Ratio (ER)

LR = Claims Incurred (Net) / Premiums Earned (Net)

ER = (Net Comm. + Exp. of Mgmt) / Net Premiums Written

The denominators of LR & ER are different. However they are being summed to report CR. This is resulting in under-reporting of CR. As per Investopedia definition, the denominator of ER should also be Premiums Earned (Net).

Please check if I am making sense.

The company announced their FY24 results and they are as follows:

1/5: ICICI Lombard reports impressive FY2024 results! GDPI increased by 17.8% to ₹247.76 billion, outpacing industry growth of 12.8%. Excluding crop and mass health, GDPI growth was 17.1%.

2/5: Combined ratio improved to 103.3% (102.5% excluding CAT losses), compared to 104.5% in FY2023. This marks increased efficiency and better risk management.

3/5: Profit before tax (PBT) grew by 21.0% to ₹25.55 billion in FY2024. In Q4, PBT surged 21.9% to ₹6.98 billion. The Board proposes a final dividend of ₹6.00 per share.The overall dividend for FY2024 including proposed final dividend is ₹ 11.00 per share.

4/5: Return on Average Equity (ROAE) was 17.2% for FY2024, with Q4 at 17.8%. Although slightly lower than FY2023’s 17.7%, still a strong performance.

5/5: Solvency ratio stands at 2.62x as of March 31, 2024, up from 2.51x last year, well above the 1.50x regulatory requirement.

5 Likes

Took key support at 200 Moving average and downtrend reversal happened.

It is coming near next key resistance. If it breaks then the next will be near All time high.

The fundamentals looks very strong and the Insurance sector is tend to grow in any means.

Stable and increasing margins are key metrices to check out.

2 Likes

IRDA circular dated 15/12/24 has substantially increased the fire insurance rates by 2-3 times. Fire insurance is around 15% for listed general insurance companies and will see a significant improvement in profitability.ICICI Lombard and Bajaj may get an increased share of the fire insurance business as the main reason for the clients opting for smaller insurance companies was a lesser premium. Fire premium is same for all companies after the recent circular.In addition,ICICI Lombard may report high growth in the health insurance segment led by Elevate.

7 Likes

3 Likes

Icici Lombard -

Q4 and FY 25 results and concall highlights -

FY 25 highlights -

Gross Direct Premium Income @ 26833 vs 24776 cr, up 8.3 pc vs an Industry growth of 6.2 pc

Combined ratio stood @ 102.8 pc vs 103.3 pc for FY 24

PBT @ 3321 vs 2555 cr

Capital gains @ 802 vs 551 cr in FY 24

PAT @ 2508 vs 1919 cr, up 31 pc YoY

Q4 FY 25 highlights -

GDPI @ 6211 vs 6073 cr YoY, up 2.3 pc vs an Industry growth of 1.7 pc

Combined ratio @ 102.5 vs 102.3 pc YoY

PBT @ 668 vs 698 cr, down 4 pc YoY

Capital gains in Q4 stood @ 6 vs 156 cr in Q4 LY

PAT @ 510 vs 519 cr, down 2 pc YoY

RoE in FY 25 vs FY 24 stood @ 19.1 vs 17.2 pc

Breakdown of company’s product portfolio -

Motor Own Damage - 20 vs 19 pc

Motor Third Party - 20vs 20 pc

Health, Travel and Accident - 29 vs 29 pc

Fire - 12 vs 14 pc

Marine - 3 vs 3 pc

Crop - 5 vs 4 pc

Others - 11 vs 11 pc

Company’s motor insurance Mkt share stood @ 10.8 vs 10.5 pc YoY

Breakdown of company’s health insurance portfolio -

Individual - 21.4 vs 18.8 pc

Group - 23.1 vs 30.6 pc

Group - Employer to Employee - 55.4 vs 50.6 pc

Company’s retail health Mkt share grew from 3.0 to 3.3 pc in last 1 yr

Company’s investment book stands @ 53.5k vs 48.8k cr YoY ( with leverage @ 3.74 vs 4.09 pc ). Annualised return stood @ 8.42 vs 7.98 pc

Excluding Crop insurance, GDPI growth in Q4 would have been 4 pc

Segmental growth in Q4 -

Motor - 6.5 pc ( due pricing pressures and reduced off takes in new car sales )

Health Overall - 3.7 pc

Retail Health - 7 pc

Commercial Lines ( like marine, fire etc ) - 3 pc

Industry’s combined Ratio @ 113 pc ( Motor Insurance’s combined ratio is the worst @ 123 pc )

Company’s breakdown of Motor Insurance business -

Private Car - 53 vs 51 pc

Two Wheelers - 25 vs 26 pc

CVs - 22 vs 23 pc

For full FY 25, segmental GDPI and loss ratios -

Motor - 10740 vs 9634 cr ( up 11.5 pc ), loss ratio @ 64.2 vs 65.2 pc

Health - 7673 vs 7117 cr ( up 8 pc ), loss ratio @ 82.2 vs 78.9 pc

Crop - 1425 vs 1175 cr ( up 21 pc ), loss ratio @ 89.2 vs 88.4 pc

Property and Casualty ( like - fire, marine cargo, engineering, liability ) - 6995 vs 6851 cr ( up 2.1 pc ), loss ratio @ 60 vs 68.6 pc

Investment income in FY 25 @ 4250 vs 3610 cr, YoY

Investment income in Q4 @ 877 vs 954 cr, YoY

Recommended a final dividend of Rs 7 / share at the end of Q4. For full FY, dividend stands @ 12 / share

As sales of CVs pick up ( vs LY where the capex activities remained subdued ), company expects some pickup in Motor Insurance business. Their Base in private cars business is already high. For full FY 26, expecting a mid single digit kind of growth in GDPI for the Motor segment

Should be able to grow the Health ( retail + group ) business in double digits

Commercial Insurance ( engineering + marine + fire + liability ) has been growing slowly in last 4-5 yrs. Seeing some pickup going forward. Worst seems to be behind

Q4 Corporate health loss ratio @ 97.2 vs 88.1

Q4 Retail health loss ratio @ 64.8 pc vs 64.6 pc

Pricing pressures did see some relief in the Fire Insurance Industry in recent past vs the intense price war / irrational pricing going on previously. This is a key positive for the company going forward

As the Industry discipline improves ( ie rational underwriting vs intense competition and irrationally low qutoes on underwriting ), it should augur really well for ICICI Lombard. It should help them grow faster and improve their profitability even further

Disc: holding, biased, added recently, not a buy/sell recommendation, not SEBI registered

5 Likes