In case anyone wants to join Q4 and FY 2020 earnings call on Saturday, here are the details…

2 Likes

Some important points on the results:

- The company has defocused the high-risk crop segment due to higher claims witnessed in this segment.

- Drop in motor premiums was related to moderation in auto volumes during FY2020 and reduced focus on CVs.

- Retail health premiums declined 40% yoy owing to lower disbursements by NBFCs and HFCs. The company has increased focus in this segment by launching new products, providing value added services and diversifying distribution channels.

- Fire premiums increased 43% yoy in FY2020 owing to rise in tariffs and higher focus on commercial businesses.

- Group health increased 63% yoy owing to increased penetration into SMEs and mid-segment companies. The company has moderated in this segment in 2HFY20 owing to rising pricing pressure.

- Travel insurance will likely witness steep decline in FY2021E owing to restrictions on travelling. Additionally, increasing risk aversion among travelers will likely lead to a ripple effect and this segment will remain weak over medium term.

9 Likes

Dear members ,

Pardon my ignorance or if I am missing something.

How come investment book is greater than gdpi+book value(assuming all of the book value to be liquid assets) . For example gdpi for fy20 is 13300 crs and book value is 5300 crs , but investment book is 26000crs, how do they get remaining 7500 odd crores for investment, do they borrow at cheaper rate and invest at higher yield ?

Do have a look at their balance sheet, you will find huge amounts in other liabilities & dues payable. This is what is called float (other people’s money).

Yes you can call it as borrowing around 0% (Combined ratio close to 100%) and investing at a yield of ~ 6-7%.

Investment book consists of shareholder assets and policyholder assets. Policyholders assets are assets backing Outstanding claims for prior years and current year.

There is no leverage in the investment book.

@vivek_mashrani, @zygo23554, @ashwinidamani:

Excellent Work.

As usual, Kedar(@zygo23554) really coached on the process of inferring numbers. Vivek did the heavy lifting to start the topic and Ashwini kept raising questions, which ensured homework for curious souls.

Take a bow, Sires.

@zygo23554:

How do you collect so much data? Too much work for a mortal like me and looking for a better alternative.

Few things that came up in my research:

The equivalent Ratio is the SOLVENCY Ratio, which represents the Liquidity ability. IRDA barred Reliance health from policy distribution since it violated this key criterion:

https://www.business-standard.com/article/economy-policy/irdai-bars-anil-ambani-led-reliance-health-insurance-from-selling-policies-119110701262_1.html

Yes:

Read NL-29 @ https://www.icicilombard.com/docs/default-source/public-disclosures/2019-20/fy/nl_29-q4-2020.pdf

Read NL-36 @ https://www.icicilombard.com/docs/default-source/public-disclosures/2019-20/fy/nl_36-q4-2020.pdf

Do share your findings as I am unable to decipher on my own.

How about using an Equity Investor’s desired rate of return as the Cost of Equity? I think that is what finally matters.

One additional key risk for the company is ‘CREDIT RISK’ of the corporates in general as 64% of the company’s investments are in Corporate Securities. In the past, the company declared ‘Downgrading of Investment’ under NL-37 @ https://www.icicilombard.com/docs/default-source/public-disclosures/2019-20/fy/nl_37-q4-2020.pdf

In FY-20, the ‘Total Industry’ (on GDPI basis) grew by 12%. The ‘PSU General Insurer’ grew by 6% and the ‘Private General Insurer’ grew by 12%. However, ICICI de-grew by 8%, but both Bajaj and HDFC Ergo- the closest competitors - grew by 18% and 8% respectively. The reason for the same is 100% degrowth of ICICI in the Crop segment.

The GDPI share of Top-3 is as below for FY20:

Disclosure: Understanding the business. No Investment.

Data Source: www.irdai.gov.in

3 Likes

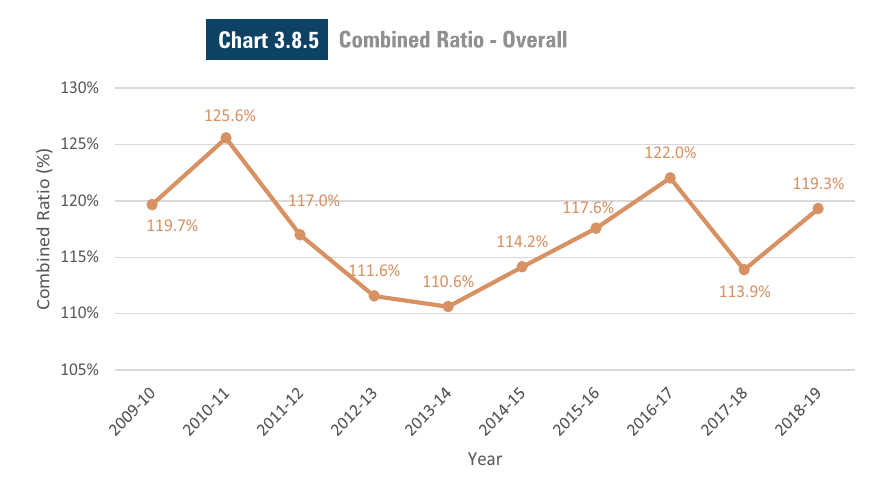

In the last 7 years, the company made underwriting profits only in one of the years (FY-19) ( Source: Company’s ARs ).

The above fact should be seen in the context of the industry’s combined ratio. As shown below, Industry has not made underwriting profits in the last 9 years ( Source: Insurance Industry’s Year Book from GI-Council ):

The reasons stated by the GI council are:

As evident from the Industry’s combined ratio, products offered by the companies do not have pricing power and policy premium pricing is the real differentiator. Besides that, the companies cannot control claims expenses, which consumes the biggest pie of net revenue (75%+).

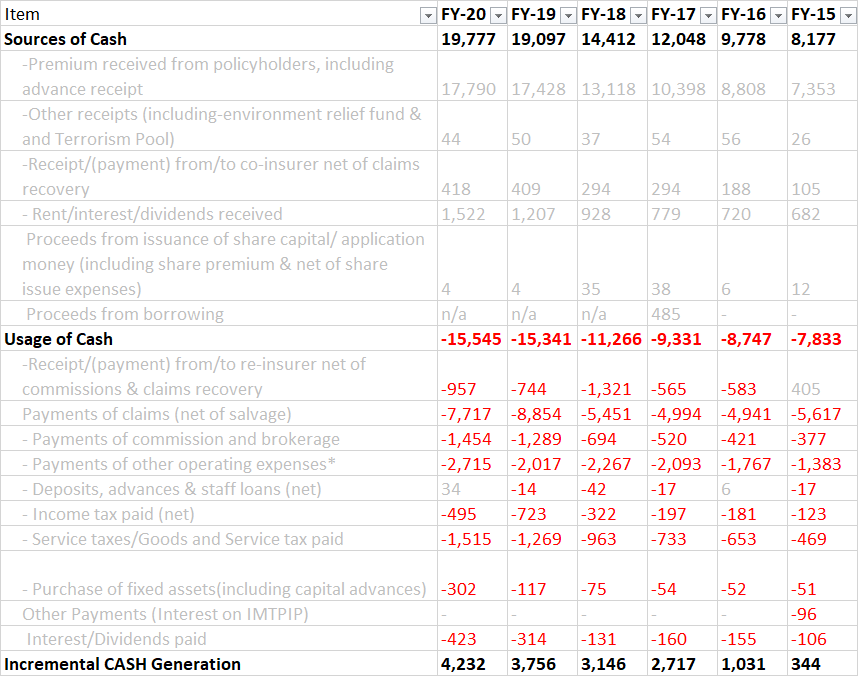

In such a scenario, companies that have the ability to collect the most premiums on a YoY basis and earn reasonable returns on investments can bear the losses from underwriting and declare Net Income. On this aspect, ICICI Lombard has done well ( Source- Company’s ARs ) :

Consequently, the cash generation ability reflects in the growing size of the Investments:

In the nutshell:

- No pricing power in the business-> Companies MUST continue spending to occupy mindshare.

- Competitors compete on the basis of pricing → Low-cost operator will do better.

- One of the reasons noted under reasons for underwriting losses- Increase in compensation awards by courts- shows that SOCIAL INFLATION will spiral in the future and might be a big problem for the companies that are heavy on long-duration policies.

------------**********************-----------------

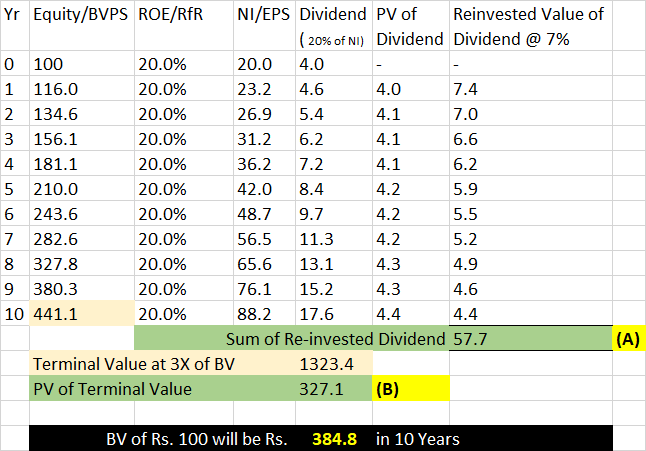

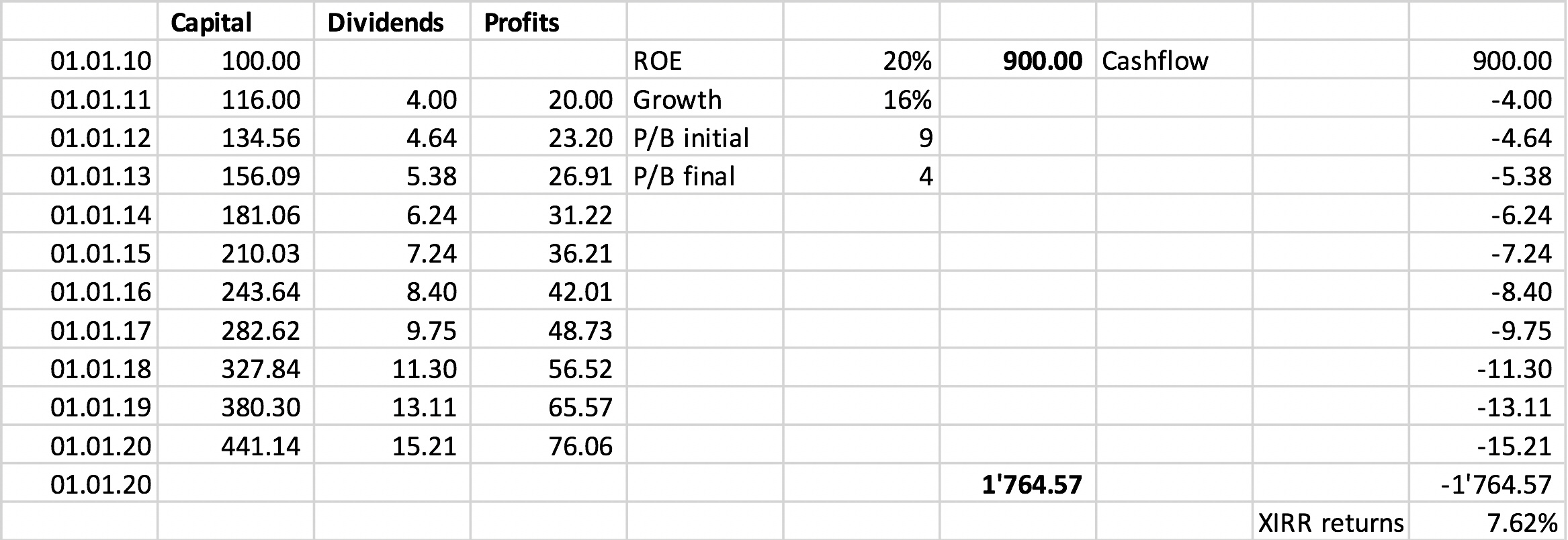

Now on the discussion about BV of 3X or 6X in 10 years which was partially answered. Pardon me to initiate it again as the same is not about the key topic of this thread. Since it took me time to understand, I shared so that it helps people like me.

Here is the maths (BV will be 3.84X in 10 years) - @harsh.beria93, @vivek_mashrani, @ashwinidamani:

A fact on ROE that should always be in our thoughts: Paying 3X of BV for a business with ROE of 21% results in an effective ROE of ONLY 7% for the investor. However, Marginal addition to BV by the business does grow at the original ROE .

P.S: No investment.

5 Likes

Good questions asked by Mr. Bharat Shah on investment book.

earnings-call-script-q4-fy2020.pdf (371.2 KB)

Can someone explain me this part from conference call

"But in quarter four, what we explained as a part of the opening remarks, some of the health benefit portfolio is something that we havenot seen as much growth as what we would have expected it to be. And that part of the business is something that we have been

historically reinsuring. And to that extent, commission income that we would have earned on that part of the business is relatively lower

on the health side you mentioned that because of your probably shift from benefit to indemnity, the reinsurance commissions have come off"

Does that mean when the reinsure the benefit part of health insure they get commission out of it or they are saying that as benefit part of health insurance has reduced so their commission has reduced

Health benefit part is sold mainly through NBFC and banks, where they do have acquisition costs in form of commission but since it is reinsured, the reinsurer contributes to the acquisition costs in form of commission.

For Health Insurance segment FY19, acquisition costs < reinsurers commission. It looks like it was mainly due to the benefit insurance part of the portfolio.

Overall, net commissions have increased due to the less offsetting effects of reinsurance commssion.

1 Like

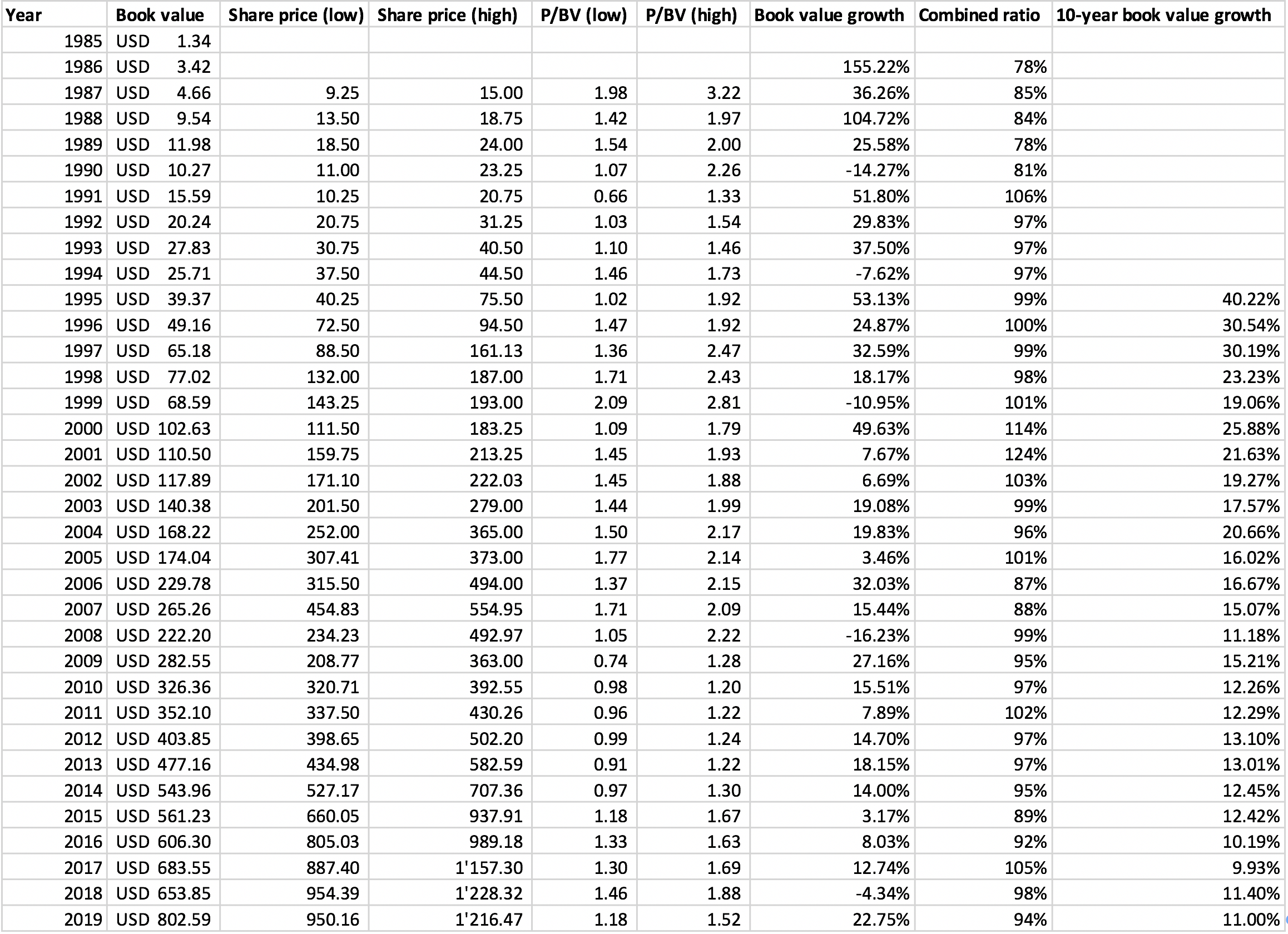

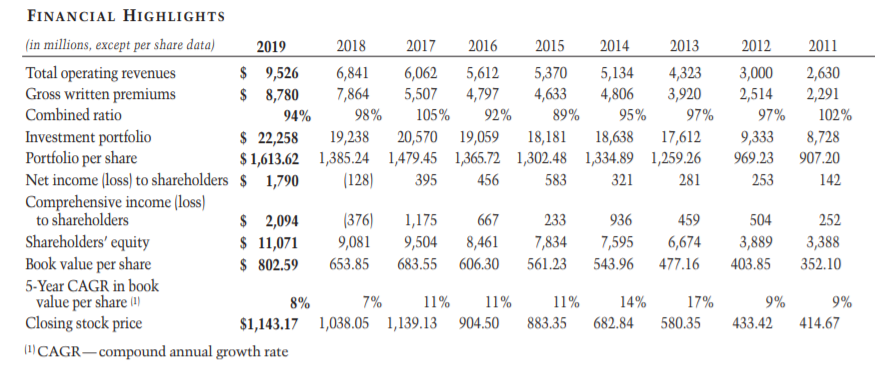

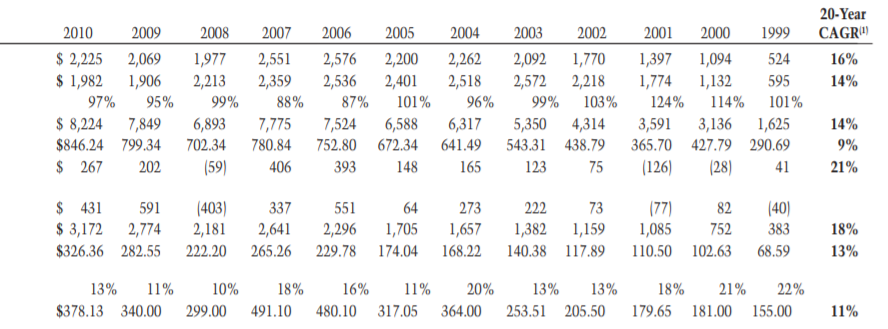

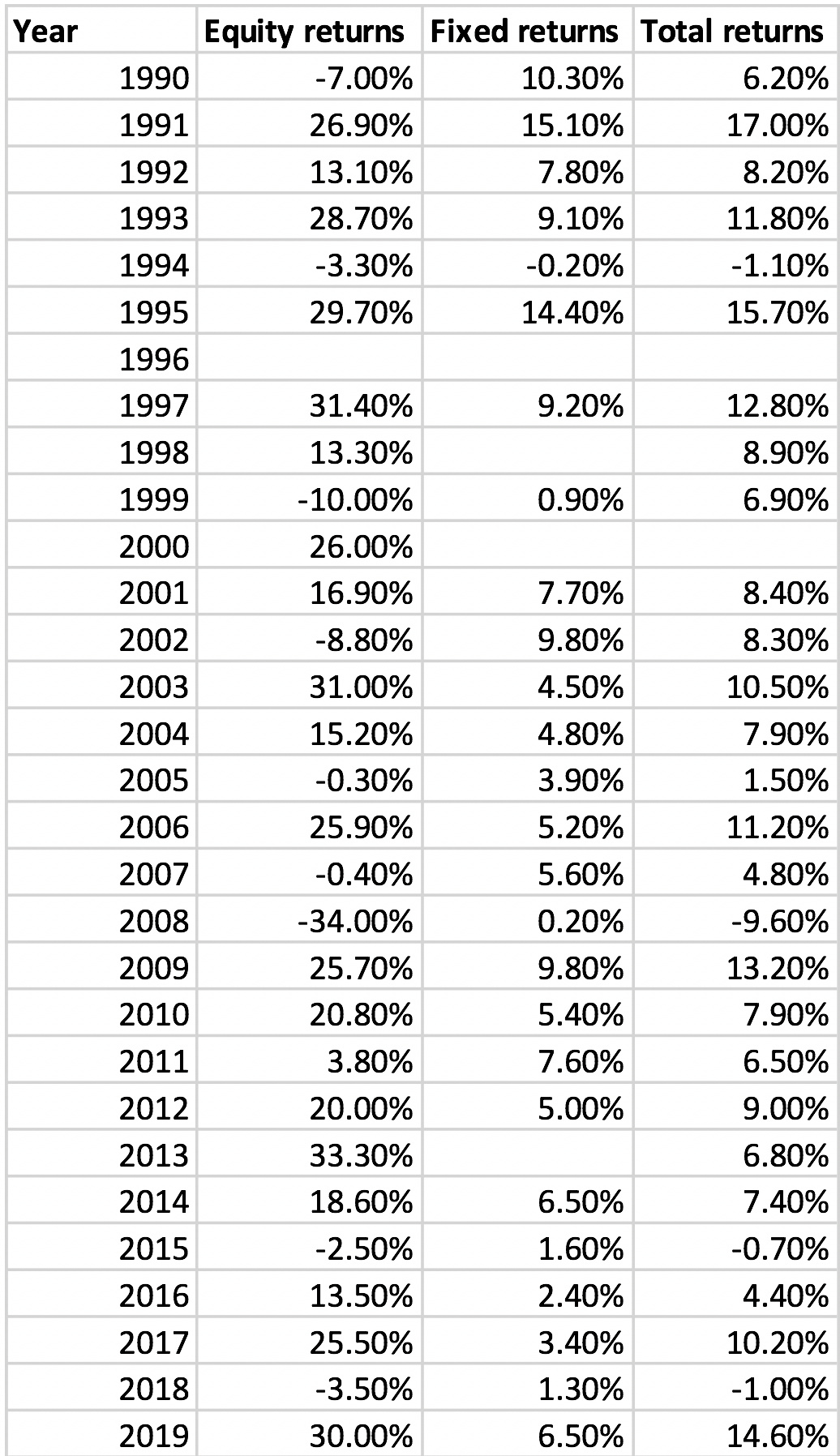

Honestly, I do not understand the current valuations of Indian insurance companies. Globally, insurance companies are valued relative to their books. I have shared the detailed valuations of Markel Corp (global leader in specialty insurance) with a track record of 34 years (book value growth ~ 20%).

During the initial part of their life cycle (similar to the stage of ICICI Lombard), they were growing their book value at 20-25% maintaining a profitable combined ratio in most years. During their rapid growth years, the maximum valuations they quoted at was 2.5-3 times book. As recent growth has tapered down to 10-12% they now quote at 1-2 times their book value. All this when their underwriting business is hugely profitable.

Now lets assume ICICI lombard is able to maintain its ROE of 20% over the next decade, gives 20% dividend and reinvests 80% of its profits back into the business. The current valuations are ~9 times book. Lets say an investor gets in now and is able to exit at ~4 times book (which is not at all conservative), returns will be ~7.62%. @Surender - You are right in your valuations.

4 Likes

@harsh.beria93 - Context is everything in valuation. I would spend more time comparing the business parameters before looking at valuation parameters

From the Markel Corp annual reports -

Looking at pure business numbers comparison before we get to valuation comparison…

How much is the gross written premium per book value?

For Markel this ratio is < 1 while for ICICI Lombard it is > 2

In 2010 this ratio was <1 for Markel while it was > 2 for ICICI Lombard

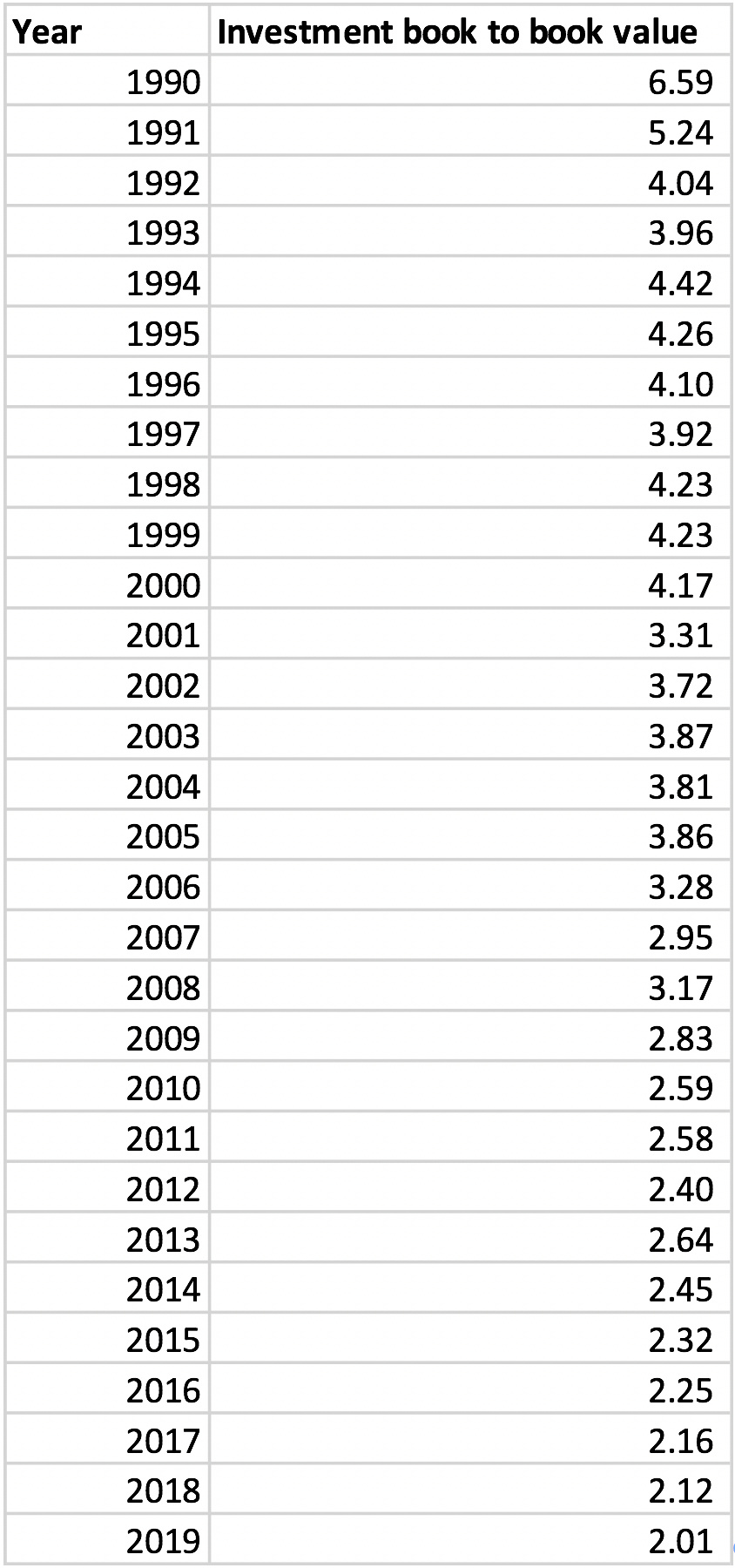

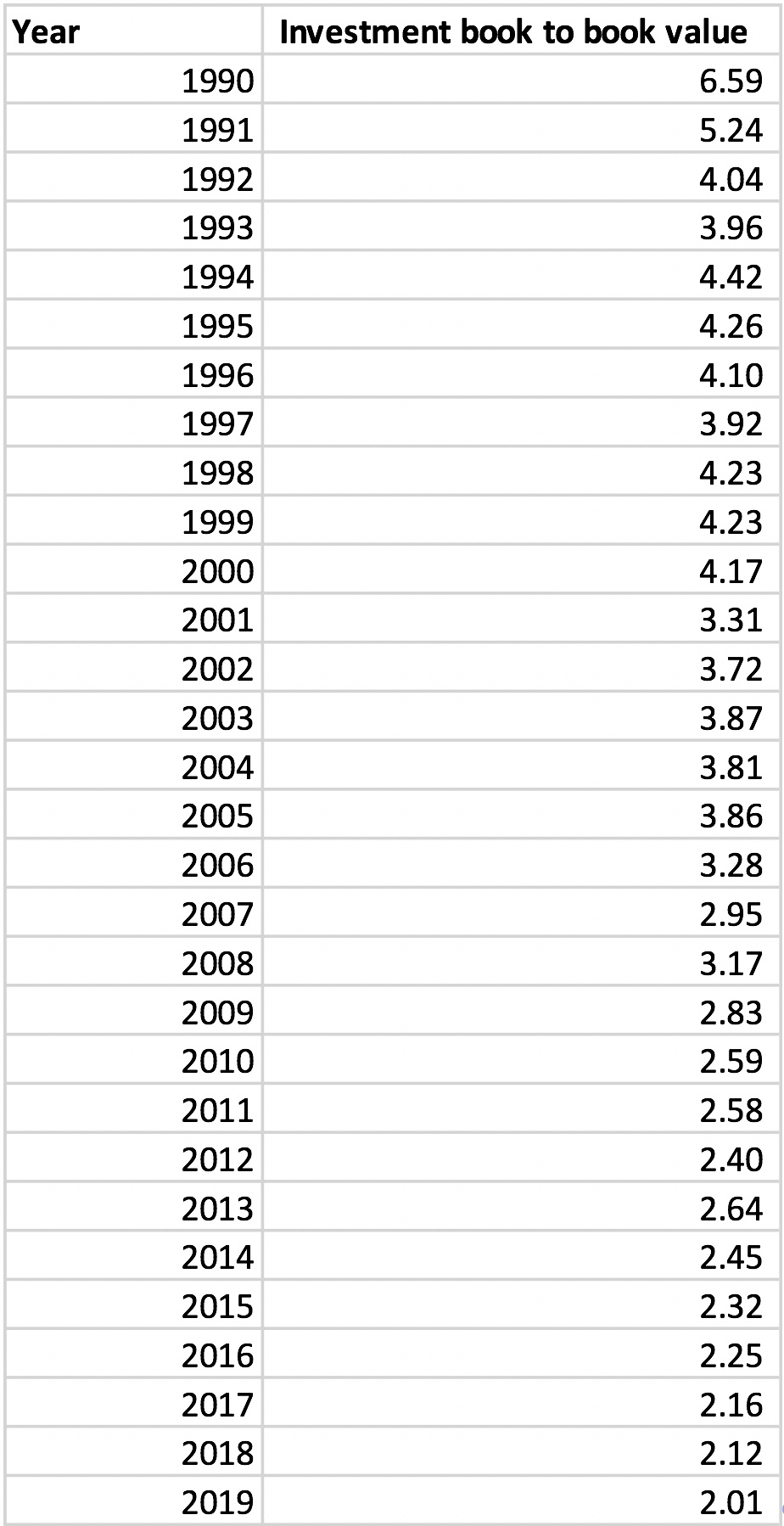

What is the Investment book to Book Value ratio?

For Markel this ratio is 2x while it is > 4x for ICICI Lombard

**What is the yield on Investment Book? How is it likely to change going forward?

Interest rates in India will likely continue to be higher than they will be across developed markets. Most likely > 2x of the developed market interest rates

How much of discretionary market building expenditure is assumed in the combined ratio?

Loss ratio is something no insurer can control. Opex ratio is something the insurers can control, for ICICI Lombard the discretionary component is 50% of PAT. This what businesses do when they have a long growth runway, they operate at lower PAT today to ensure they keep growth rates high for 10+ years. In a mature industry which is already efficient, this market development expenditure is much lower for obvious reasons.

What is the Net Premium to Gross Premium ratio?

This pretty much tells us how much underwriting risk is being assumed by the insurer. Lower the ratio, higher the reinsured component of the book, lower is the risk of a tail event hitting the insurer.

If ICICI Lombard is reinsuring away 80%+ of the tail risk book while holding on to the granular risk book, is the risk lower or higher compared to Markel?

Should one look at ICICI Lombard as a distribution setup or as an Insurer for the tail risk business?

For the same level of Book Value, ICICI Lombard books 2x the gross premium compared to Markel

For the same level of Book Value, ICICI Lombard is sitting on 2x the investment book of Markel

For the same level of Investment Book, ICICI Lombard is likely to do 2x+ the yield that Markel can do

ICICI Lombard can turn underwriting profits today if it wants to, it is instead trying to develop the market and capture market share rather than focus on maximizing profits in the short term

Shouldn’t these factors play a role in valuation if one were to compare P/BV across geographies? Is the comparison between Markel and ICICI Lombard on a standalone P/BV basis even fair given that the operating context is so different? Markel corporation is also a holding company with many underlying businesses including reinsurance. The product portfolio and the incumbent risks are much different compared to ICICI Lombard.

22 Likes

This can help you in understanding the valuation of insurers-

FLOAT AND INTRINSIC VALUATION OF INSURERS (30-03-20).pdf (1.7 MB)

For a likewise comparison, we should be looking at Markel in the 1990s to ICICI lombard today. For instance, Markel in 1995 wrote gross premiums of $402 mn on a book value of $213 mn (gross premium to book value ~ 1.9). So, its very similar to what ICICI Lombard does today. Another thing to keep in mind is that having a net written premium as a large number against book value is akin to having a large d/e i.e. it amplifies ROE in good times and loss reserves maybe found inadequate in bad times. Lets wait for one full economic cycle before trusting the underwriting performance of ICICI lombard.

Again you are comparing Markel today whereas you should be comparing Markel in the 1990s. Investment book to book value ratio for Markel was > 4 in the 1990s (similar to ICICI Lombard today).

Again, we have to look at Markel in the 1990s, their total returns on their investment books were 9-10%. The fixed income returns for Markel was 6-8% in the 1990s (details below).

Keeping higher expense ratio is akin to investing for future profits, I completely agree. However, it doesn’t change the fact that we should evaluate insurance companies on their book rather than profits because profits are dependent on future liabilities and nobody can assess what future liabilities will look like. Also, profits for insurance companies are very cyclical because they have to treat unrealized gains/losses on their investment books as acounting gains/losses in each quarterly report. Thats why I am comparing book values rather than profit trends.

Having a low net premium to gross premium ratio also takes away the float and makes it a brokerage operation. If you consider ICICI lombard as a distribution setup, then you also need to remove the effect of float.

Markel’s gross premium to book value was 2x in the 1990s.

Markel had an investment book to book value ratio of 4x during the 1990s, it came down to 3x during the 2000s and is now down to 2x.

Are you telling me ICICI lombard will make total investment returns of >10% by investing 85% of their book in fixed investments and the rest in equity? Markel managed to achieve very good returns in the 1990s (mentioned before in the post).

To conclude, I am not wrong in comparing Markel’s operations in the 1990s to ICICI Lombard today. Also, I am trying to give all the data points to support my arguments. I would love to know your thoughts!

Cheers

Harsh

17 Likes

I have read Berkshire, Markel and Fairfax annual reports since the start of their individual operations. So, I have a bit of an idea how floats work. Can you please look at my post above and point out what I am missing in my assessment?

1 Like

@harsh.beria93 - I broadly agree that the 90’s in the US market is where one needs to benchmark financialization stories in current India to. This holds across asset management & insurance.

Interestingly interest rates in the US in the 1990-2000 decade hovered between the 4-6% mark, it is only post 2000 that interest rates started dipping. So even on that front, India is right now in a similar ballpark range.

From an accounting stand point, differences could arise on two points -

-

Bond portfolio for insurers in India follows HTM and not MTM. Not sure how this is done in the US. Hence this smoothens out the interest rate/duration risk for insurers in India to a great extent, since 85%+ of the investment book is bonds the investment income trend also gets smoothened out

-

Customer acquisition costs have to captured as and when they are incurred in India, there is no concept of deferred acquisition cost as it there in the US. However this impacts mostly P&L and not the investment book, at most a minor factor unless one considers the cumulative 15 year effect of this on the book value

Coming to the data posted by you on the Investment to Book value ratio for Markel, the primary question to ponder over is why has this ratio dipped from 4x to 2x over the period? One can see steep resets in the years -

2001 (fall from 4.17 to 3.31) - WTC incident

2006 (fall from 3.86 to 3.28, then to 2.95 very next year) - Hurricane Katrina

From 2009 onward it has pretty much been a falling trend

If I assume a book value of 100 and an investment book of 400, at a 6% investment yield and nil underwriting profits the book value grows by almost 18%. For the ratio to fall steeply one these things needs to have happened -

-

A tail event that that depletes the investment book severely, this should also affect the combined ratio for the year and force a reduction in book value as well beyond a threshold. Given that Markel is into various kinds of insurance and that the US is well known for severe hurricanes/tornadoes that hit once in a while, was this the reason? Especially since Markel does reinsurance as well where one assumes much higher risks of underwriting tail events

-

Company goes on an acquisition spree and buys into businesses that skew the ratio to the lower side - either due to a different product portfolio or due to different underwriting economics. From the corporate history of Markel I can see that they have been acquisition heavy

-

Ability of company to charge premium rates is compromised for whatever reason, which is why the incremental addition to float lags behind the growth in book value. This can also explain why the GWP to Book Value has fallen. Increase competition may well have changed the economics from the mid 90’s onward

I think the sequence of events as to why the investment to book value ratio fell become important since that is one of the big factors why the P/B is much lower today was Markel than it was in the 90’s. If you have the data handy for this, this will be a very useful exercise and might answer a lot of questions. For ICICI Lombard the Investment Book to Book Value ratio has only been increasing over the 2010-2019 period (2.25x in 2010 to 4.1x in 2019). If this trend were to reverse, this will compromise the investment thesis in ICICI Lombard (at least for me) to a good extent.

I’ve started reading the history of the US Insurance market and will post here if I find these answers as to what changed in the market post 1995 that had changed the economics for worse.

As for expectations of investment yield for ICICI Lombard from here on, I’d probably run with a 6-7% number on the fixed income book over the medium term. Post tax this works out to the 4.75 % range which is what makes the ROE trend close to the 20% mark if one were to assume the investment book to book value ratio stays at 3.8x+

ICICI Lombard has a retention ratio (Net Premium to GWP) of 75% for the granular health book while it is 15-20% for the fire book. Motor book is managed at a retention ratio of close to 90%. This the management sees as a function of the tail risk in segment and is fairly logical. So ICICI Lombard works as a distribution setup only in fire and to some extent marine, but works as an insurer in the granular segments

6 Likes

Anyway earnings are not how insurance companies are valued. Earnings tend to be depressed during the early part of life cycle because of upfront investments. Thanks for clarifying the HTM aspect, however it doesn’t have much impact on book value.

Thats not the point I am trying to make. My point is that even when Markel was growing rapidly at 30+% per year, the maximum valuation they got was around 3 times book. Same was the case with Berkshire. Fairfax is the only exception which went into bubble territory in 2000 and cracked by 90% during the 2000-02 bear market. And we are talking about the best insurance companies in the world with very prudent underwriting practice, why should valuations be different for an Indian company?

Also, they acquired Terra Nova in 1999 which at that time was bigger than Markel and it took about 4 years to turn around their international operations business.

Thats because they started non-insurance acquisitions in 2005 (with AMF Bakery acquisition). Now, private ventures are not traded on stock market and their book value are not updated constantly. Markel uses EBITDA as a proxy to the enterprise value of their private venture undertakings.

You have missed one point, mean reversion of valuations. Insurance companies have been listed in the last 3-4 years, they haven’t seen even one market cycle. A simple P/B de-rating from 9.5 to 4 times can offset 5-years of 20% book value growth. Even HDFC bank trades at only 3-5 times P/B and gives 20%+ book value growth!

Its very simple mathematics for insurance companies: Lowering of interest rates translates into lower investment returns, hence lower growth in book value. Market pays for growth. Markel in their initial 10 years were compounding their book value by 25%+, not they are compounding at 10-12% (look at the last column in the figure below), hence cheaper valuations compared to their past.

All I am trying to say insurance companies being valued at 9-10 times book is not normal. Base rates of making returns equivalent to cost of capital at these multiples are low, doesn’t mean can’t happen.

8 Likes

The market may be discounting the next decade for ICICI Lomabrd, as it knows how the next decade is going to pan out. Maybe at that time in USA people weren’t sure how much wealth Markel would create in the future.

I guess its more about perception. If you had paid twice or even thrice in terms of book value for HDFC bank in 2002-05 you still would have made decent returns. Also the consistent returns from Markel shows us that the market did not value it appropriately in the first place.

PS- I do believe that PE is a better way to value ICICI Lomabrd

1 Like

So far I haven’t really commented on whether the current valuation is justified or not - neither in an absolute sense or in a comparative sense across other markets. That’s the one thing I am restricting myself from doing, am very happy to exchange views on quality of the business and how to value businesses in general.

That said, my preference on how to value businesses tends to be more towards considering a range of outcomes over the medium term. I find this much easier to do in a time series model since that allows me to express views on how the financials could change based on some good years and bad years. I have limitations in relying too much on P/B or P/E for this very reason, I find it very difficult to think of a scenarios when the peg is to what the current book value is or what this year’s earnings are. I might give higher weightage to these ratios if I believe that the past pretty much covers all possibilities that the future can offer - so that one can see what the mean range has been and where we are right now. Which is not the case for the business in question in my opinion.

As for the prime question - the current P/B seen by itself optically appears to be very high, especially when bench marked with the best in the business in the US during the 90’s.

But then, will we be guilty of being too micro focused without paying due attention to the macro picture? Gross Insurance Premium to GDP was in the range of 9.7% in the US when the 90’s began. Today India is still at 3%, maybe that is what the market is happily paying up for? I have no qualms in saying that I do not have a clear answer in my mind yet. One can see this across industries in India, there are many examples where the Indian arm of an MNC trades at 2 - 2.5x the valuation multiple given to the parent.

But this is where I start digressing into the macro aspects of investing, eventually this will need to translate into the micro in terms of growth rates and margins. I am increasingly finding this particular aspect tougher in taking investment decisions, the ability to translate views on the macro environment and scope that into taking micro decisions specific to a particular business.

15 Likes

I think looking at valuations as to whether they are high, low or fair in absolute terms is not very helpful.

Markets are a combination of Fundamentals + Perception. And trust me perception can keep valuations different from fundamentals for a very long time.

A better way to look at valuations is to ask whether the stock will re-rate, de-rate or stay the same in terms of valuations and what will be the factors for these to happen.

This allows you to avoid going into numbers game of say 80PE is high and 10PE is low. Plus, it prevents you from arguing with what the market is showing you.

Even though markets goes into another trip from time to time and arguing with what market is showing you can make tons of money. But that is very rare and difficult thing to do.

And frankly agreeing and understanding what markets is showing you can still help you make decent money over time.

3 Likes