Some reference point for precedent. Deal in 2017 happened at ~5.7x P/B if I have inferred it correctly from below article. Likes of PE fund of Warburg Pincus bought the stake. Again, not saying whether current valuation is cheap or expensive (it’s in the eyes of beholder).

And btw while this discussion is happening…from start of writing this thread to now, the valuation has increased from ~6x P/B to ~8.5x P/B

Yes for maintaining 1, varies per Insured tenor, approx 15%

Many infact, eg a few in 2008. Read Merger act.

Yes

Don’t know

Don’t know

I don’t track this insurance company, but one should give thought to risks, most assumptions in this thread is blue sky scenario.

Change in COC, big losses or fall in premium, low returns on float, losses on investment, more competition etc.

Insurance has no product differentiation, so one would need to be very sure how well the Float is invested and possibilities of same being done over long run ahead. Because if company invest badly, the whole insurance company will be in insolvent( if that coincides with UW losses or not maintaining 1) due to one Black swan. Think of it as a Fund which invest in Equity, Govt bonds, private companies debt.

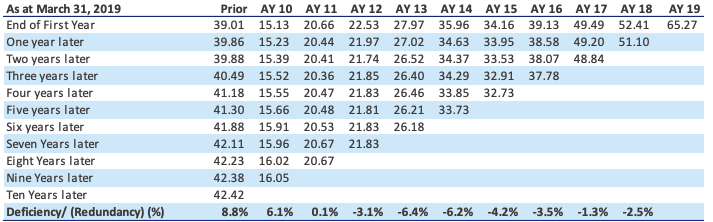

Excellent article, about time someone started a thread on this. One aspect which has not been covered is reserving triangles (for third party motor policies).

Though general insurance has typically short tail, Motor TP has a long tail due to vagaries of police department, courts, etc. If i am not mistaken, ICICI Lombard has been disclosing the reserving triangle for the last 3-4 years (among the only player to disclose this). Combined ratio gets impacted due to IBNR and IBENR (claims incurred but not reported and not enough reported). An analysis of reserving triangle indicates that they have been more conservative over the last 6-7 years.

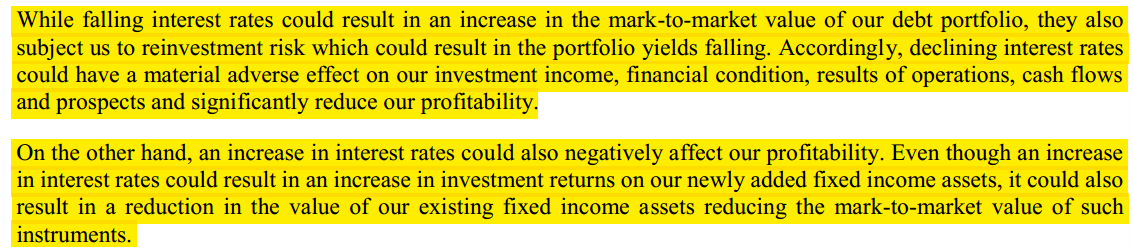

Some Risks highlighted From the Prospectus, which may be happening right now

Changes in prevailing interest rates could materially affect our investment returns

While falling interest rates could result in an increase in the mark-to-market value of our debt portfolio, they also subject us to reinvestment risk which could result in the portfolio yields falling.

Accordingly, declining interest rates could have a material adverse effect on our investment income, financial condition, results of operations, cash flows and prospects and significantly reduce our profitability

Our Business may be affected by

o prevailing income conditions among Indian consumers and Indian corporates;

o prevailing regional or global economic conditions, including in India’s principal export markets;

o any downgrading of India’s debt rating by a domestic or international rating agency financial instability in financial markets;

Though this should not materially impact the insurance companies but it does have the capability to leave the policy holder with a bad taste. Third party approval process in India in my personal experience is not very friendly. There are lot of queries and initially the TPA are mostly reluctant. With this boundation of 2 hrs things are bound to get more difficult.

Regards

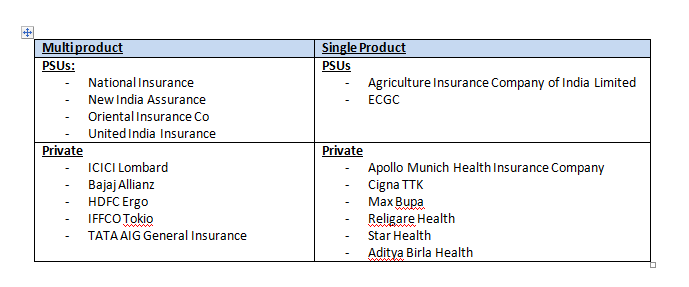

Need insights on why some players have chosen to focus only on Health Insurance instead of being Multi Product Insurer. Ironically, this is the space where ICICI is not as strong.

Why does it make sense to focus on one product alone

Many of these are hospital chains that have seen synergy in venturing into health insurance. Apollo, Max, Religare, Cigna TTK (Manipal Group) all have hospital businesses within the group / promoters. So they may not have interest in other insurance verticals.

Most PE investments have gone into standalone health insurers over the past few years

Apollo Munich is now part of HDFC Ergo

Health Insurance is the only pure play B2C segment, in all other segments you either have large buying centers or you have strong channel partners (Motor Insurance)

Come to your own conclusions. Taking a timeline approach to how an industry evolved over time gives insights that usual business analysis cannot

Yes, bond portfolios are HTM and not MTM though an insurer can manage the portfolio actively. Lower interest rates tend to lower investment income if they persist for a long enough period of time.

ICICI Lombard has the largest investment book among all the private insurers at approx 25,000 Cr as of date. With lower interest rates, the yield on investment book will trend lower but not proportionately since legacy book is already deployed at 7%+. Incremental float gets invested at say 6% but this only drops the investment income marginally, it is not a linear equation.

The discretionary total across the Motor and Health lines of business at 600 Cr for FY19 is more than 2.5% of the investment book. Though any reduction here can affect medium term growth, this expense item offers a cushion to manage yearly P&L if push comes to shove

Which is why @zygo23554 we would need breakup of legacy investment book deployed at 7%.

if say bulk of it is getting matured in next 1-2 years, and reinvestment rates are trending lower (today 6, maybe tomorrow 5.5% etc) , your entire revenue projection will go for a toss.

Again, coming back to Health Insurance - I agree with your thesis on channel partners, but wouldnt channel partners be also required in Health Insurance.

Come to think of it, how would u sell Health Insurance

Through Agents (Online/Offiline) - If I have tapped into these, why dont I sell an Auto Insurance also through this. Maybe answer would be something tied up to repairs and claims.

Through Corporate Tie ups - again, this would require legwork, so why not sell Fire Insurance etc to same corporate

Through Hospitals - How many big chains can u tie up with ?

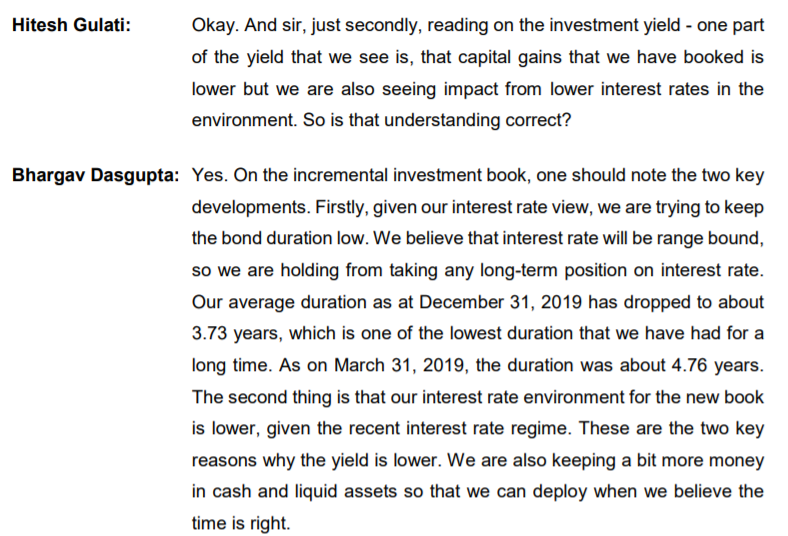

Q3 FY18 Conf call - modified duration of the bond portfolio as of date is 4.8 years

As of March 31, 2019 - Mod duration was 4.76 years

Q3 FY20 Conf call - Mod duration is 3.73 years

Back calculating from MF data, at a mod duration of 3.7 years the YTM for an 80%+ AAA portfolio is likely to be in the range of 6.7 - 6.8%. IDFC Bond Fund Medium Term plan I believe is a very good approximation of the kind of bond portfolio that ICICI Lombard is holding.

Hence the inference that the current yield on bond portfolio is likely to be 7% and that the average maturity of the bond portfolio is most likely 5 - 5.5 years

From the Q3 FY20 presentation - Corporate Bonds 50%, G-Sec 31% and Equity 11%

Overall takeaway is that they manage bond portfolio actively though accounting gives them the leeway of HTM instead of MTM. They are also likely to increase equity proportion if the market level looks attractive enough.

Health insurance segment is by far the most profitable segment with the minimum tail risks. So any new player who does not have a legacy asset insurance book is unlikely to focus on segments which calls for aggressive pricing at higher tail risks. They can but they are unlikely to.

Motor calls for channel partners too but one deals with concentrated buying centers there. Motor dealers wield a lot of influence in the OEM market (insurer has to get empanelled with OEM to sell through their dealer network) and also to some extent in the renewal market. A lot of motor insurance renewals again happens through the same dealer who services the vehicle, which is why IRDA brought the Motor Insurance Service Provider regulations into place in 2018.

Within health insurance the B2B segment where insurers offer health cover to employees of large organizations is again a price sensitive segment. Once again this is a segment where you have concentrated buying centers. Smaller corporates, SME and individual insurance buying are highly profitable segments with minimum tail risks. Channel partners are needed but the balance of power is in more in favour of the insurers.

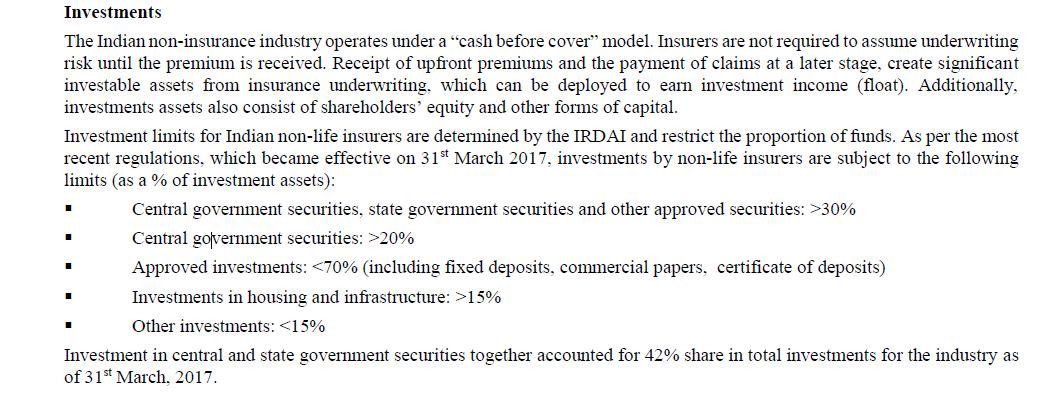

Investment limits for non-life insurers are determined by the IRDAI & restrict the proportion of funds

Govt Securities

Atleast 30%

Approved investments (including fixed deposits, commercial papers, certificate of deposits)

Less than 70%

Investments in housing and infrastructure

Greater than 15%

Other investments (Equity etc)

Less than 15%

ICICI Lombard Prospectus says

Since fiscal 2004, our listed equity portfolio has returned an annualised total return of 30.8%, as compared to an annualised return of 17.5% on the benchmark S&P NIFTY index.

Our equity portfolio outperformed the S&P NIFTY index in all but one fiscal year

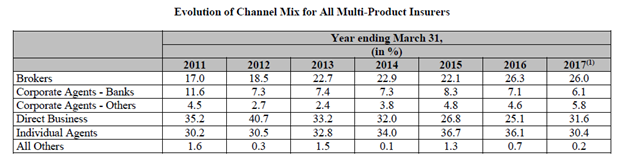

Balance of Power seems to be shifting from Banks to Brokers if we see from overall point of view, but if we look at just private insurers the picture is different.

Here Bank share has marginally gone up and ofcourse Broker share has gone up. Direct Business is going down a lot. This basically would mean that Public Banks have not been as successful .

Brokers and Direct Business are the dominant force anyways.

Maximum Commission that can be paid to brokers is somewhere around 15%

Does this mean that which ever way the interest rate moves, ICICI Lombard is going to loose? since the stock of investments will always be greater than than the fresh inflows that they can deploy?