Insurance Cos definitely seem to have been through all cycles with most starting from 2001 around. The investors in Insurance Cos might not have gone through up and down cycle.

1 Like

Big Structural Risks to the story are -

-

Lowering of Interest Rates - Cant imagine why this would go up in India/world over the next few years. This will suppress their ROEs going forward. This is the One and Biggest risk for me (especially at these valuations)

-

General Economic Recession - If people insure less stock, purchase less vehicles then clearly we can see growth coming down. Atleast ICICI is valued as a growth stock and hence, the valuations might be impacted.

-

The advent of Online Insurers (Acko etc) - Though these guys are burning money and shall probably continue to do so, these guys will hamper profitability in near term

3 Likes

My point was about valuations and not business performance.

It will be very useful if you can share how you think about the future of this business, and how Indian insurance businesses can be (or cannot be) different from global insurance businesses (be it general, life, or catastrophy). Is there real evidence somewhere in the world where this thesis has played out, or is it simply too much liquidity chasing too few opportunities?

Your point is that there is a long runway and India is an underpenetrated market. Well, this holds true for almost everything in India.

A company is valued as the sum of its future cash flows, so to get higher future cash flows, a company should either grow faster or have a longer runway. For Insurance businesses, the best Indian insurance companies have a ROE ~ 20%. Assuming a 20% dividend distribution their sustainable growth will be capped at 16%. Higher growth will require equity dilution. To understand growth runway, the best thing to do is probably look at the past. What is the base rate of a financial company growing at 16% for 20 years while maintaining ROE of 20%? I do not know the answer, but it surely is < 16% (based on simple probability theory; given that nifty decadal churn is ~40% and nifty long term growth is 12-15%).

You are not the only one, I face it all the time. On top of everything, equity valuations are completely dependent on interest rates which is another macro variable very hard to forecast. However, higher interest rates are good for general insurance companies.

5 Likes

One factor that you might have missed is pricing of risk. General insurance is kind of a commodity, where the lowest cost provider (or the most aggressive underwriter) will get maximum growth and set the industry pricing. I have gone through annual reports of a lot of global insurance companies, most of them complain about pricing of risk. Typically, risk pricing follows a cycle: after a few years of no major catastrophe, insurance prices fall. Then a major event occurs which leads to repricing increasing insurance prices and more sustainable future growth.

3 Likes

There is no perfect answer to choosing one between Philip Phisher (priority to quality) and Benjamin Graham (priority to valuation) investment styles. Both schools of thought have their own relevance. This is why investment is an art, not science. Therefore, the right answer could be finding a midway path between ‘Quality’ and ‘Valuation’ i.e. trying to find value in growth stocks.

Several investment gurus these days prefer to stick to ‘Philip Fisher’ style as this gives them privilege to remain right for greater part of their investment journey also translating into higher inflows into their strategies, however we cannot rule out old ways of picking stocks at the right valuation. Ultimate question is ‘Who has the patience of waiting for the right valuation and also the courage to buy when everything seems down and out i.e. in current scenario several quality midcaps and small caps’

Presenting text from Warren Buffet’s 1982 letter to shareholders: For the investors, a too-high purchase price for the stocks of an excellent company can undo the effects of a subsequent decade of favourable business developments.

Leaving to the wisdom of participants to choose between the two.

To take a comparative view, one needs to find a global peer that fits the following criteria -

Underwriting granular risks rather than tail risks (Health/auto rather than property/reinsurance)

Access to a population of this size (even after discounting the bottom 70% who may not be able to afford insurance anytime soon), health Insurance segment in India is at 40,000 Cr premium means less than 8 Cr people are insured.

Access to a market that can grow at 15% over a 15 year time frame

The average business hardly insures business risks beyond the usual categories. One sees higher penetration of categories like E&O policies only in export oriented businesses

Minimal penetration of even basic products like house insurance

Laughably low premium amounts (probably due to PSU insurance pricing all these years)

My sense is a pure play auto/health insurer in a South East Asian country might offer the best comparison. Comparing to US insurers might not be fruitful, P&C insurance premium from 2010 to 2019 in the US is almost flat.

This is still work in progress for me, this is not an easy view to build and will need a lot of reading and comparing.

That is the interesting part. If one draws up a cash flow projection for a period of 10 years and works with a 13-14% GDPI growth assumption at 18-20% pre dividend ROE % & an exit P/B of around 3, the CMP does not look expensive. At this growth rate company may not need equity dilution, anything more than 15-16% will call for equity dilution to shore up the solvency margin. Now a P/B of 3 by itself may not be cheap, but that is a 60% discount to the current multiple.

The other aspect is that my baseline growth of a financialization business (not financials) is close to the 15% range over the next decade or so. I cannot think of too many industries where one has visibility of that kind of growth at a favorable industry structure and at an ROE of around 20% assuming nothing fancy. For all the high quality narrative surrounding FMCG stocks, none of them can even come close to a 15% growth rate from here over that tenure though their ROE’s maybe much higher.

I more or less take it as a given that there is too much liquidity chasing the few widely acknowledged quality stocks in India. Bulk of the valuation risk comes from here, one can only keep this to a level but avoiding this risk appears very difficult given the operating environment today.

I find interest rates the easier variable to model for, given where we are. The tougher decision is to decide the tenure of the view/analysis to base decisions off, this impacts valuation view much more for a specific business. If one models for 10 years time frame, a business that can grow at 12-13% and manage an ROE of 20% does not deserve to trade at a P/E of anything more than 30. For this time frame approx 35-40% of the intrinsic value still depends on the TV one accords to the business which is yet another guesstimate at best. Stretch this period out to 20 years and the same assumptions make CMP look much more reasonable, so if one truly has a 20 year view to a business - the decision looks much more simpler though the risk of overpaying still persists.

In India, we also tend to underweight the importance of discount rates when it comes to valuation. P/E of 20 when interest rate is at 9% is very different from P/E of 20 when interest rate is 5%. The average multiple accorded to a high quality business in India is much higher after 2014 than the period before for this reason, the cost of capital premium is very real. We tend to look at Sensex returns only from mid 1990’s till date when interest rates were much higher than they will be over the next 10 years.

While lower interest rates aren’t the best news for Insurance businesses, there is a trade off due to the lower discounting rate used in valuation.

5 Likes

If we assume that AUM of the company will neither grow, nor decline, In that scenario, the valuation in a very simplistic manner should be equal to AUM. As you get to hold this capital forever. Money is money, as long as there is no cost to it. Am i thinking right?

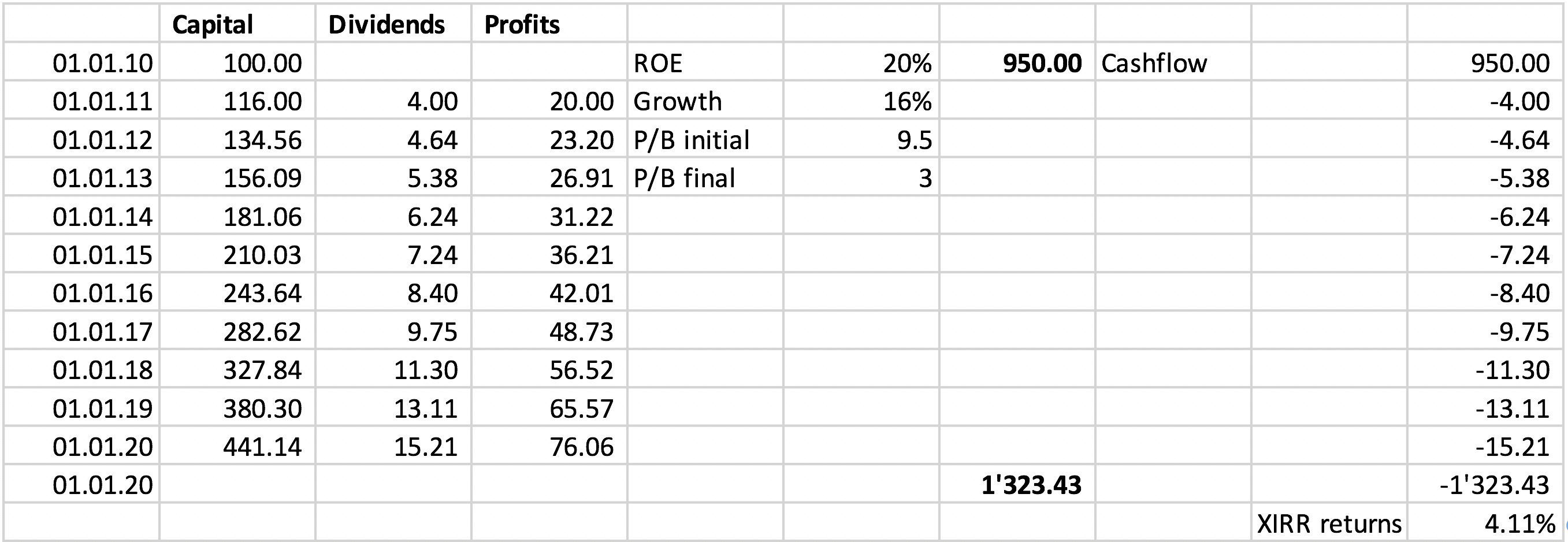

Are you sure about this? Here are the results for a 20% ROE, 16% growth, 9.5 times entry multiple (current P/B is 9.9) and an exit multiple of 3. The returns are 4.11% (see computation below). Are we getting compensated for risk?

Again base rates! Financial businesses are easy to grow, but very difficult to grow profitably. We don’t have past evidence of high sequential ROEs for any Indian financial company (the only exception in India is HDFC, and exceptions do not make the rule).

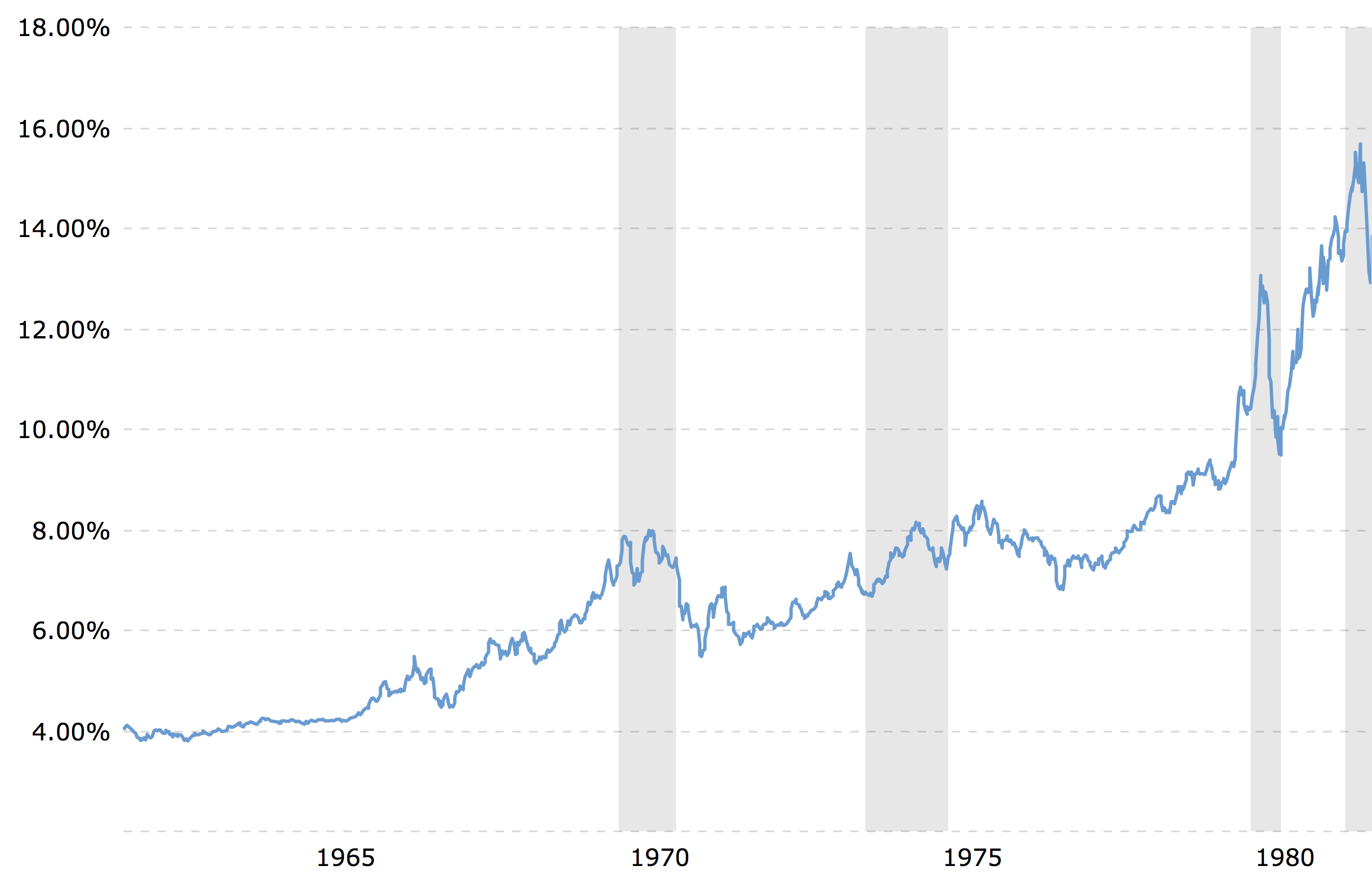

Lets look at history, 10-year treasury rates in the US moved from 4% in 1962 to ~16% in 1981. What happened to PE ratios? They went down from 20 to 7. What were S&P returns during these 2 decades (really long term)? 4% and -1% if adjusted for inflation. So much for interest rates! Is this likely to repeat? I don’t know! Can this happen? Yes! You can reproduce the charts on www.macrotrends.net

Stretch it out for 30 years, today’s price is a bargain. Over the very long term, stock price returns converge to ROE of the business if it can redeploy the profits at the same incremental ROE. The most critical part is returns on incremental capital.

Three other things happened after 2014, 1) mutual funds got a ton of money and for some reason they want to be 100% invested at all times, 2) growth in Indian corporates vanished and in absence of growth, investors seek predictability of profits bidding up prices of companies with relatively stable margins (hence predictable profitability), and 3) global interest rates went close to zero, pension funds need to generate 8% returns to fulfill their commitments, they are forced to invest in riskier assets to generate those returns.

All insurance companies go bankrupt if interest rates sustain below 2%. And this is not a theoretical exercise but has actually happened. Anyone interested can look at price charts of the largest insurance companies in the world, they peaked in 2000 when interest rates peaked and most of them haven’t got back to those levels (eg: AIG, Allianz, AXA, China life insurance).

No! The AUM of an insurance company does not belong to its shareholders, it belongs to its policy holders. Shareholders are only entitled to the shareholder equity + reserves (adjusted for any future losses)

I have loved this discussion so far because it has made me think a lot. For HDFC life, I think there is a separate thread. In a nutshell, I don’t know have any unique insights. We will know about underwriting quality and adequacy of loss reserves when the books are stress tested.

I think its been covered somewhere before in this thread, the main difference is the duration of insurance liability, its lower for general insurance companies than life insurance companies.

Buffett made his big money at 50% IRR during his early partnership days (1951-1960) (link), he later adopted quality because thats scalable. Instead of quality investing, Phil Fisher was a proponent of growth at a reasonable price and scuttlebutt. Growth and not quality is valued at a premium as growth means more future cashflows whereas quality without growth means higher current dividends. For instance, look at Castrol India, its very high quality (80%+ ROCE) but lacks growth. As a result, market penalized it (by derating the company). So, its growth that attracts higher valuations and not simply quality.

3 Likes

At NWP growth of 13-14% an exit multiple of 60% from entry level gives me an expected return of close to the 7% mark. Pre dividend ROE trends in the 18-20% range since I am running with the assumption of nil underwriting profits over the period with almost all of the PAT accruing due to investment income. Effectively Book Value grows at around 2-3% higher per annum than the premium growth. I guess once we work with the same precise numbers our return expectations cannot be very different arithmetically even if we approach this from different points (give or take 100 bps at the max)

As for real world expectations, the following can change the scenario materially -

Investment Book growth rate has been much higher than growth in Premiums or Profits. 35-40% of the NWP gets added to the investment book every year. In insurance cash flows and investment book growth should outpace PAT growth and eventually enhance PAT growth rate if the granularity of the risks assumed are preserved

What discount rate does one use for a float business? If one works with the thesis that the cost of float for an insurance company is the operating cost of running the business, as the scale goes up this cost only goes down from current levels. The WACC then becomes much lower than what one would normally use, even for a high quality business. I am tending towards the view that the WACC for a good insurer can be a good 200-300 bps lower than that for a high quality FMCG play.

Optimization of Opex over time can lead to underwriting profits and hence much higher ROE. Refer my earlier posts on the extent of discretionary market building expenditure built into the current cost model. This can surprise differently at some point of time, at a PAT base of 1250 Cr the discretionary expenses are more than 300 Cr

Customer acquisition costs can reduce significantly over time once again affecting ROE. Someone who already has health insurance and house insurance is more likely to buy travel insurance at minimal customer acquisition cost, operating leverage due to cross sell cannot be captured easily in an arithmetic driven valuation model.

The qualitative assessment then ends up being - are there enough levers to mitigate a higher initial price than warranted? The challenge also lies in reflexivity, if the ROE ends up being 30% at a 12% NWP growth 10 years down the line, why would the exit multiple be 60% lower?

In a few businesses it may be more important to participate and see how things evolve over a period of time rather than sit by the sidelines due to over valuation. Of course at a high enough entry price I am pretty much pricing myself out of the market but it does not seem to be such a clear cut case to me here. There are many widely acknowledged high quality businesses I would not touch since they do not offer even half the number of levers on offer here.

Once again, HDFC Bank or HDFC Ltd are financials which carry leverage and balance sheet risks by design. A financialization business does not carry balance sheet risks, nor needs incremental capital to scale up beyond a point. I can manage 5,00,000 Cr AUM with the same team that manages 3,00,000 Cr today. If anything the incremental return on capital is outrageously high for a financialization business, will never be so for a lender since one needs to have capital to lend in the first place.

If I can get 15% return from an FD I’d sell off all equity and park in an FD instead. In such a situation I’d generate alpha through better expense management rather than focus on higher returns. India is exactly the reverse of this, we are coming from 15%+ interest rates to interest rates in the range of 4-6%. No wonder P/E for businesses that can grow at healthy rates over long periods of time has trended up.

One can at best take a medium term view on interest rates, calibrate as you go along. 3 years down the line if the repo rate crosses 8%, it’s back to the drawing board for me. For this very reason I spend a lot of time tracking what’s going on in fixed income markets. I cannot predict but I can calibrate well enough.

This in a nutshell is why I like AMC and Insurance businesses. They offer one of the highest rates on incremental capital at a healthy enough growth rate over the medium term. That said I am not yet willing to look 20 years into the future, I hence model for a max period of 10 years. The long term is a series of medium terms,

3 Likes

One negative could be competition growing faster, HDFC Ego, Go Digiti(Fairfax JV), and Bajaj Finserv have all gained market share over the last one year, ICICI Lombard has just been able to maintain market share.

I understand, legally the float AUM belongs to policy holders, but notionally as long as there are no underwriting losses and GDPI continues to grow, AUM becomes sort of permanent capital for shareholders, just valuing the company on book value, misses the value of the AUM.

Without hampering the essence of beautiful conversation on insurance business, just want to add that I prefer quality insurers and lenders over AMCs.

Although, AMCs don’t possess balance sheet risks to the tune of lenders, but they are subject to a much bigger risk i.e. regulatory risk. The prime source of returns in AMCs i.e. expense ratio is a regulated metric. Any potential interventions by SEBI could send lofty valuations lower and revalue future cash flows for the sponsor. Understandably, expense ratio cuts will be gradual in nature but overhangs are here to stay.

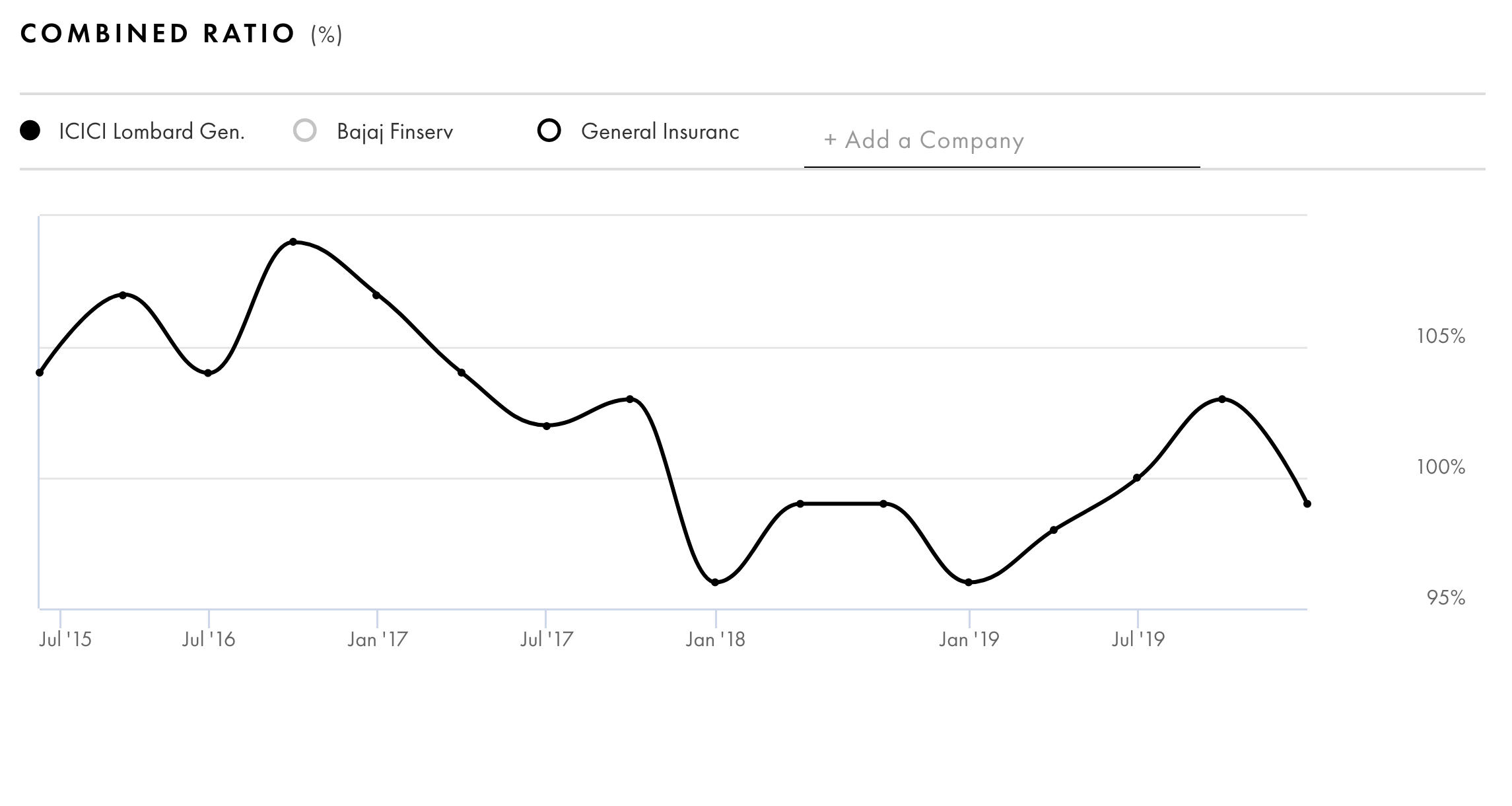

Cost of float depends on underwriting profits/losses plus operating costs. For example, if combined ratio is >100%, it means that the insurer is paying money to generate the float and if its <100%, they are getting paid to hold the float. Here are the combined ratio (taken from tijori). It clearly highlights that there is a cost to float i.e. company is paying money to have the float.

Is a 30% ROE a reasonable assumption? Given the nature of this product, its a commodity. High ROEs invite competition and in India, all the large financials are cut throat. I think the more relevant thing to ask is the source of competitive advantage for a given insurance company. In this business, there are three sources of advantage: (1) distribution network, (2) underwriting process, and (3) operating costs.

- Distribution network: Insurers with a banking fraternity tend to have huge scale advantages

- Underwriting: Mostly a function of industry dynamics, i.e. the cheapest price provider will end up defining the pricing trends

- Operating costs: This is the only aspect which an insurer can control.

Really a 10 times P/B is not clear cut? Anyway, lets not harp on this, for every buyer there is a seller and vice versa.

There is a difference between asset managers and risk underwriters. What you are referring to are AMC businesses and does not apply to insurance companies as they are taking balance sheet risk.

@rupeshtatiya - Have you also looked at general insurers?

3 Likes

(Not quoting the post since it becomes too long given my tendency to write walls of text)

Cost of Float

Loss Ratio - depends on the segment of risks one is insuring. This varies across insurers - HDFD Ergo is at 76.35%, Bajaj Allianz general is at 68.60%. By changing the proportion of business segments, this changes since the loss ratio varies across segments and also depends on how seasoned the book is in segments like motor TP

Opex ratio - Again changes based on the segments. HDFC Ergo is at 22.40% and Bajaj Allianz is at 28.10%. The extent of money spent on marketing and distribution impacts this heavily. An insurer with a higher proportion of B2B book will a spend lower % on the channel

If a considerable chunk of the opex is discretionary, the cost of capital can fall to that extent over time. There is a B2C element to some of the business segments that the company is into and this makes a big difference over time. A good chunk of the sales & marketing spends do not scale with growth in revenue for a consumer business, BTL expenses (that are usually % of sales) also come down over time as the volume of business done through the channel increases. This is one of the most important sources of how a consumer business increases margins and return ratios over time.

The opex ratio for the company can fall whenever the company decides that they need to fall, this will be subject to competitive forces but the company has a lot of leeway in my assessment.

Distribution - In general insurance there is no great advantage in having a banking parentage whereas in Life insurance this matters big time. The fastest growing general insurers in India are the standalone health insurers who have no banking parent. Reason being life insurance even today is more of a savings product in India, which is why the banca channel is so important. There is no savings component in general insurance, the presence of a banking parent does not matter much when the contract is of a 1 year tenure. The presence of a well known corporate house as the parent gives comfort no doubt but the absence of it is not a deal breaker in general insurance.

The control over distribution channel instead matters more. Is the channel captive or are we selling through an open architecture where other products can compete? One does not need much of a distribution channel if the focus is on B2B segment, a direct sales force gets the job done. The trade off is that the book then becomes a high tail risk and lower pricing power book .

More importantly, who holds the power in the OEM distributor relationship? Over a period of time as competition increases this is what determines who gets majority of the profit pool in an industry. Since the IRDA regulations pretty much cap commission payouts for each segment, any incentives over and above that are at the prerogative of the insurer.

Unless one does field work or has worked in the industry as a revenue facing person, how OEM distributor relationships work is rarely evaluated by investors.

Underwriting - Within compulsory segments like Motor the pricing guidance is given by the IRDA. In segments like Property insurance the pricing is set by the reinsurers more than the insurers.At the initial stages of growth, pricing is within a range for most players since everyone is competing in a growing market. It is only when we get to a stage where there are too many players fighting for the pie that players resort to price undercutting to win market share. Even in that situation, the large incumbent players have an advantage for obvious reasons since they can work at lower prices and not bleed out (this is why the 20% ROE assumption comes in, else the company can work at 25% ROE today). This will emerge over a period of time and one needs to track the developments, no point being very definitive about this right now since we have a long way to go yet.

Operating costs Already covered in the above points. These will trend down as a % of NEP over time with scale since the discretionary element is considerable. See the Opex breakup of the motor and health segments for the company and the data will pretty much tell you the entire story.

Valuation - ICICI Lombard is not the only general insurance player listed in India. GIC and New India Assurance are listed as well and they trade at 1.2 - 1.4 times BV, no change from global valuations here eh?

However, as businesses these three are way different from one another. The market maybe very optimistic on ICICI Lombard right now but the market is discerning on who deserves to trade at a higher valuation.

I’d rather invert and ask myself - why is Lombard getting priced this way compared to the other two? Clearly the market is not in love with “general insurance” as a theme going by the valuation of the other two. If all general insurers were trading at 9 times BV, there really isn’t much to talk about, is it?

Balance sheet risk in financialization - The order of increasing balance sheet risk in my mind is this - AMC --> general insurer with granular risks --> general insurer with tail risks --> reinsurer --> Life insurer with low protection component & low defined benefits book --> life insurers with higher proportion of protection & defined benefits book

Form which angle does it look like I do not appreciate the differences between asset managers & risk underwriters?

Every point I am making is very specific to ICICI Lombard as a business and not a generic comment on the general insurer category. I see Lombard and GIC as very different businesses that deserve to trade a very different valuations. My unit of evaluation continues to be ICICI Lombard as a business and then as an investment, there is limited utility to doing comparative exercises beyond a point. The market is discerning even when it comes to valuation of life insurers, you have one trading at 4.5 time IEV while there is another trading at 2.4 and they come from the same pedigree.

5 Likes

@zygo23554 I have been following you on HDFC AMC and ICICI Lombard forums. I must say, you have an amazing understanding of both AMC and Insurance business. Regarding balance sheet risk , do you mean “AMC” has the least risk and “life insurers with higher proportion of protection & defined benefits book” has the maximum risk.

1 Like

thanks for all your insights.

Are you talking about defined benefit pension schemes like group gratuity?

One of the reasons, could be for the years prior to 2010, the company was not setting loss reserves conservatively and probably deficiency. Towards IPO, they probably started setting reserves conservatively and you can see reserves redundancy.

Please suggest a good book to read on US Insurance market?

1 Like

2 Likes