Life Insurance products have a saving element in it and not general insurance. Investments backing unit linked products can have as much as 50% equities in it. I would’nt get into any of sort of comparison with life insurance companies.

Jotting down my thoughts on some questions posed by @rupeshtatiya

How has Bajaj Allianz general been faring so far? Don’t they make underwriting profits?

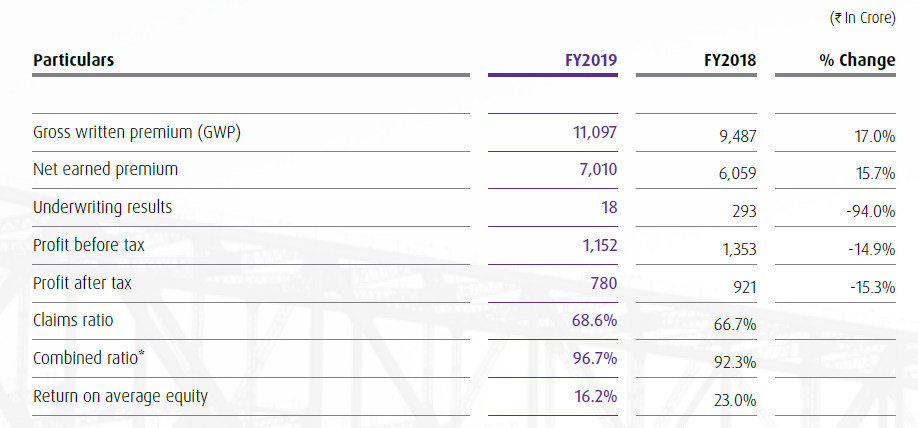

From their 2019 annual report -

They have made underwriting profits for FY2018 and 2019. In fact they have a claim ratio that is way lower than what ICICI Lombard has, logically this can only be an outcome of the product portfolio…

| Portfolio (GWP) | HDFC Ergo | Bajaj Allianz | ICICI GI |

|---|---|---|---|

| Motor | 34% | 49% | 45% |

| Health + PA | 22% | 26% | 19% |

| Others | 20% | 11% | 19% |

| Rural & Agri | 24% | 15% | 17% |

It is obvious that the proportion of GDPI from Motor and Health (taken together) for Bajaj Allianz General is much higher than the other two, maybe that explains why ICICI Lombard is spending a lot of resourcing in those two segments. To source motor insurance, an insurer needs to get empanelled with the OEM as one of the vendors. This is where Bajaj Allianz may have an obvious advantage due to the group parentage, commendable that ICICI Lombard does higher volumes than Bajaj Allianz in the motor segment. Coming to the other line Health, the absolute numbers are more or less the same for both ICICI Lombard and Bajaj Allianz. Once again logically thinking the B2C component of health should be more profitable than the B2B segment (where group health covers are given to large organization’s employees) though the claim ratio should not vary much - from the accounts this more or less gets confirmed. ICICI Lombard has net claims of 1400 Cr from Health + PA while Bajaj Allianz had ~1450 Cr. The difference appears to be coming from the claim ratio within the Motor segment - ICICI Lombard has 3477 Cr GDPI from OD and 3042 from TP while for Bajaj Allianz it is 2102 Cr from OD while TP is 2754 Cr.

From the ICICI Lombard conf calls I remember that motor TP liability always hits with a lag (over 5-7 years) while OD hits immediately. Extending this logic, it is possible that though Bajaj Allianz is running at lower claim ratio in motor segment, over a period of time this ratio might actually trend up given the higher proportion of TP premiums. This is just a logical inference and will need to be confirmed over time. If so, then the relatively high underwriting efficiency that Bajaj Allianz shows is more due to product mix than any other operational edge.

Other data points to compare Bajaj Allianz -

| Parameter | HDFC Ergo | Bajaj Allianz |

|---|---|---|

| Gross Written Premium (Cr) | 8,722 | 11,097 |

| Reinsurance (Cr) | 4,350 | 3,323 |

| Net Written Premium (Cr) | 4,372 | 7,774 |

| Net Earned Premium (Cr) | 3,810 | 7,010 |

| Claims (Net) | 2,909 | 4,810 |

| Total Expenses | 1,171 | 1,807 |

| Investment Income - Policy | 566 | 1,134 |

| Investment Income - Shareholder | 171 | |

| Loss Ratio | 76.35% | 68.60% |

| Expense Ratio | 22.40% | 28.10% |

| Combined Ratio | 98.75% | 96.70% |

| No of Policies (Cr) | 0.85 | 2 |

| Market Share | 5.10% | 6.89% |

| PBT (Cr) | 636 | 1,152 |

| PAT (Cr) | 383 | 780 |

| Investment Assets (Cr) | 9,104 | 17,237 |

| Investment Yield (%) | 8.10% | 6.58% |

| Investments to Book | 4.59 | 3.39 |

Investment Leverage ratio for Bajaj Allianz at 3.39x is much lower than the 4.18 that ICICI Lombard does

Suggestions welcome on if there is a better way of viewing the available data to see why Bajaj Allianz has better underwriting numbers

Consistent underwriting profit is a source of differentiation. Can the industry get there in some years through better product mix/innovation?

Agree, it is more a question of how the industry and competition evolves to force players into optimizing underwriting efficiency and not just focus on how to grow business. This will be a work in progress question for at least 5 more years

The trends that clearly stand out are -

-

B2C lines of business (health, motor) is more profitable than the B2B lines of business (Fire, Marine)

-

Motor TP by virtue of being a long term contract (3 years and 5 years for 4W and 2W) offers the highest float though the possible liability some years down the line is much higher. Over here the players can choose their product mix too based on the tradeoffs. CV TP gives higher float but the claims can be very large, opposite in case of owner driven PV

-

Private insurers taking market share away from public insurers, specifically in motor. The below chart says it all -

Public Insurer Market Share in Motor Insurance (%) - Source: Public domain

Interesting link - PSU insurance firms cry foul: Private sector insurers taking market with ‘unfair practices’ | The Financial Express

Over the medium term looks like it will be a market share game for private insurers where the first objective is to win higher business within the bounds of risk framework defined rather than optimize too much on underwriting efficiency. Why? Because they can afford to. This is a market that can keep growing at double digits over the long term, much easier to compete in a growing market than a shrinking market.

As for innovation, this has been my experience in the financial services industry - what one innovates today, others copy tomorrow. There is no great advantage emerging from product innovation, advantages are more likely to emerge from distribution, channel efficiency, scale of operations and strong parentage rather than product innovation. The mutual fund industry operates in a similar way, there is no great difference in product offerings across the larger names - at most proportions may vary.

In an industry like General Insurance, my objective as an investor is to participate over the medium/long term while ensuring that the price I am paying is not too high. We will likely see multiple players who are successful over the long run…

13 Likes

Hi,

While a lot of emphasis has been given on how great this business is, some more effort should be put into explaining why valuations are justifiable even at this price.

Some more questions from my side

-

do they invest in equities too. If yes, what has been the performance. If No, then do regulations limit them.

-

Insurance as a culture hasn’t taken off in India. 50% of General Insurance premiums is due to govt mandated insurance. Why or what do you think will change this.

-

How come ICICI Gen Insurance is ahead than Hdfc etc , especially because ICICI as a group has always followed the leader, but here it seems it itself is one of the leader. Why so. Is the management quite different here. Who are the key guys who made a difference.

-

What has been the underwriting skills of Lombard globally

2 Likes

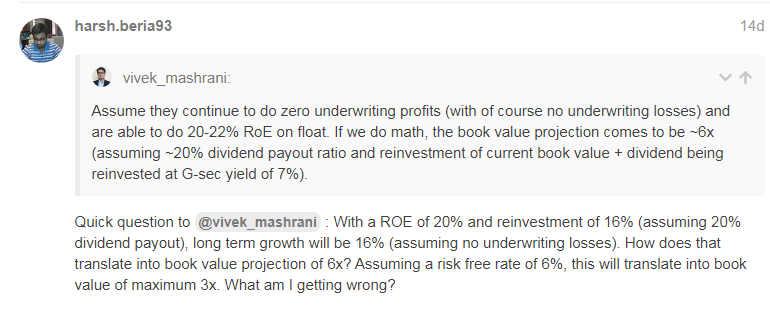

@ashwinidamani - As @zygo23554 rightly mentioned that currently they are making ~20-22% RoE just from the float + small underwriting profits.

Assume they continue to do zero underwriting profits (with of course no underwriting losses) and are able to do 20-22% RoE on float. If we do math, the book value projection comes to be ~6x (assuming ~20% dividend payout ratio and reinvestment of current book value + dividend being reinvested at G-sec yield of 7%). This is again very simplistic way of ball-park valuation ignoring some minor factors like reserves, investment yield fluctuations etc.

On other questions,

-

Since general insurance is short tail, they can’t afford to have large allocations to equities. Currently, they have ~15% equity allocation. Reason is mainly asset liability management. They need to have visibility of cashflows in 1-2 year basis. Again, investments in debt securities provides them greater visibility and comfort in terms of competitive pricing

-

Key drivers are formalization of economy which can give boost to travel and health insurance from employers + more education around these products. Motor is anyways now compulsory by law (and which is major chunk) + there will be market share shift from public sector players + penetration of apps which will push such product (so internet penetration will add to ease of access)

-

ICICI has very strong distribution network, good parentage + very robust digital platform. Again @zygo23554 can kindly add if he has more views on this.

4 Likes

Quick question to @vivek_mashrani : With a ROE of 20% and reinvestment of 16% (assuming 20% dividend payout), long term growth will be 16% (assuming no underwriting losses). How does that translate into book value projection of 6x? Assuming a risk free rate of 6%, this will translate into book value of maximum 3x. What am I getting wrong?

1 Like

ICICI group was a pioneer in many ways, the opinion we have of the group starting from 2009 (no prizes for guessing what changed) kind of colors the perception we have of the group. ICICI bank taught the banking world how to structure construction finance deals as an example, they were also the first to offer a 3 in 1 product for someone who wants to invest into the markets. ICICI Securities is way ahead of HDFC Securities, so General Insurance is not the only area where ICICI group is ahead of HDFC group. As an IT salesman, there was an unwritten rule that any new product would first need to be accepted by the ICICI Bank technology team before the industry accepted that.

Coming to the management team -

- Bhargav Dasgupta – Has been MD & CEO of company since 2009, has been a career ICICI group employee since early 90’s and has worked with ICICI Bank in various roles across project finance, international banking, technology and strategy

- Gopal Balachandran – CFO, has been with company since 2002. Has worked with ICICI group in roles across financial reporting, taxation, risk management

- Alok Agarwal – ED & CMO, has been with company since 2011 and with ICICI group since early 90’s

- Sanjeev Mantri – ED & CMO, has been with ICICI group since 2003 and with company since 2015. Has been a career banker with exposure across multiple businesses

This is unlike other subsidiaries of ICICI Bank where there is a transfer of people from ICICI Bank to run separate businesses. For e.g. Anup Bagchi was CEO at ISec before he became ED at ICICI Bank, Shilpa Kumar was in Corporate Markets team at bank before being posted as CEO at ISec, Vijay Chandok was heading International Banking at bank before he was made CEO of Isec. The general insurance management has spent a long time at the helm and actually understand the business and industry quite well.

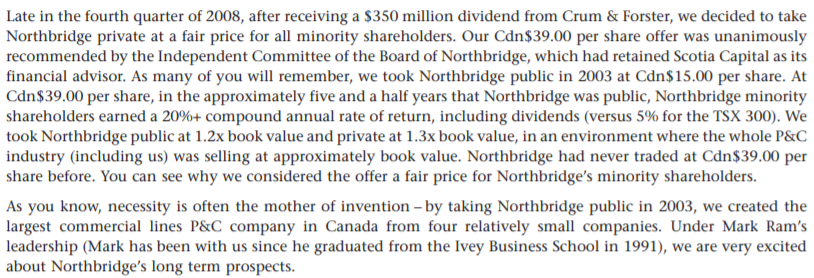

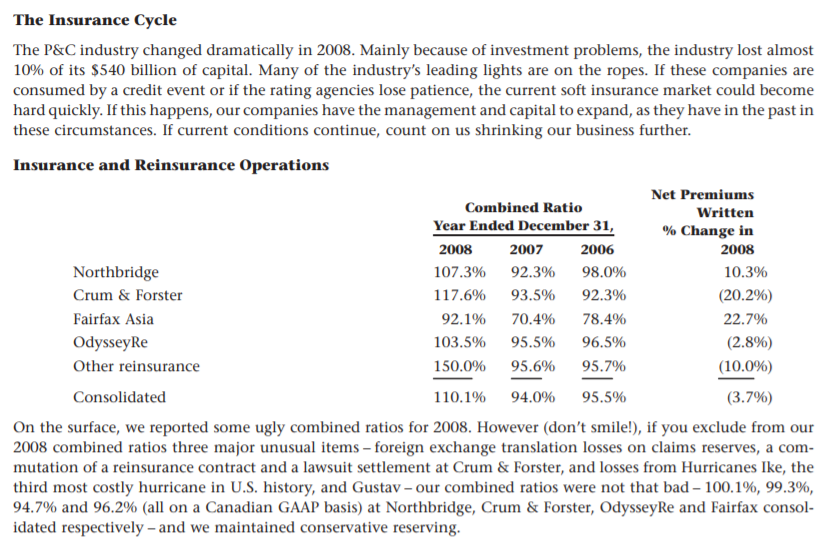

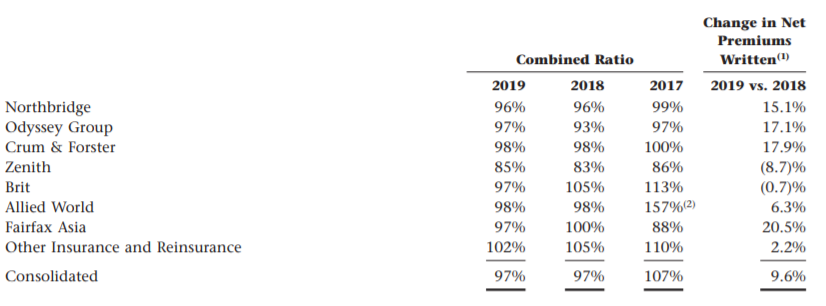

Lombard Canada Ltd is an interesting story by itself. This was the property and casualty insurance subsidiary of Fairfax holdings, was later rebranded Northbridge Insurance, taken public by Fairfax in 2003 and then taken private in 2009. From Fairfax 2009 annual report

From their 2019 annual report

Looks consistent over the years, of course their portfolio is a subset of what ICICI Lombard does today.

14 Likes

Can you post your calculation on excel, with BV projection for 10 years + terminal value. Add dividend. And discount this back to today? Assume starting BV as 100 for simplicity. Thanks.

Great response. Thanks for these detailed inputs.

I still have to work my head around valuations.

2 Likes

You don’t need a DCF for this. Assume you have a fixed deposit in a bank which gives you 6% CAGR (we call this risk free return). Now any business which earns returns that are greater than risk free rate will be more valuable than its tangible book value. A business which generates a ROE of 18% can be valued at P/B ~ 18/6 ~ 3 times. Thats a very simple heuristic to understand the valuation for a business.

This makes sense only for finance companies and businesses that don’t have a lot of intangible assets on their balance sheets. One of the most successful insurance business (BRK) earns a ROIC ~ 10% (long term growth ~ 10%) and trades at 1 P/B.

5 Likes

Sure, though here majority of the earnings are re-invested + growth opportunity which changes the context.

Anyways, valuation has been very subjective topic. If you are comfortable with 3x BV i.e. ~INR 390 TTM or ~INR 450 Fwd multiple, you can probably wait bit more. You never know in such market corrections you might get lucky ![]() All the best.

All the best.

1 Like

I find this very difficult to digest.

ROE and BV are related , but their relation is not linear.

A company with higher roe can compound wealth significantly in the long run. This is why companies like GRUH, BAJFin & SBI cards are valued at PB ratios which deceptively look high.

THB i don’t find the PB ratio quite useful while valuing companies. You just look at the ratio and ignore growth, franchise quality, management, business model etc.

PE is a better ratio for ICICI Lombard as the earnings are more or less predictable in the long run (short term would be volatile)

One thing to be kept in mind is that the earnings are a conservative estimate as the customer acquisition cost is front loaded in insurance.

Also the main game here is float & ICICI lombard has the highest inv leverage.

1 Like

This is late cycle talk i.e. when things have gone up for a long time, we are unwilling to look at times when things trade at appropriate multiples. I love this quote from Kenneth Andrade (article)

You start justifying price to book, when price to book becomes expensive, you start justifying price to earnings and the next cycle is price-earnings to growth.

Valuations are subjective, this thread is a very nice compilation of the business dynamics of insurance sector. Let’s try not to destroy it with our own assessment of valuations.

4 Likes

Without getting into a discussion on what valuation is appropriate, I am more interested in how to value a general insurance company. This way we focus on ground up, first principles which can make the downstream steps rather obvious.

An insurer is surely different from a bank, there is minimal leverage and much lesser balance sheet risk. What we have is the possibility that a small premium can result in a huge outflow due to a claim and that the claim can occur anytime before the end of the annual contract. Sometimes the actual payoff may happen 2-3 years down the line since the investigation and evaluation of the claim can take years together. It is this mismatch in terms of timing that leads to growth of the investment book over a period of time. Also the investment yield is on the Investment Book, not on the Net Worth of the company (book value).

A general insurer is also very different from a life insurer for the simple reason that profitable underwriting for a life insurer can only be measured over the complete life of a contract, for a general insurer it can be measured annually since the contract is for 1 year. This is why PAT does not matter much for a life insurer, we look at Embedded Value since that is the PV of the existing book. The accounting mismatch the makes life insurance complicated is not present in general insurance to a large extent

General Insurance does have an accounting mismatch in the sense that customer acquisition cost is front loaded and captured in the accounting period while premium and commission are accounted on an accrual basis. Motor TP is multi year to a good extent, so are some health insurance policies. If this hypothesis is true, non discretionary Opex % should trend down over time. It is the discretionary channel development expenses that keep opex % steady. This is like a Relaxo that can sell at a 10% premium if it wants to but doesn’t to keep competition at bay and ensure the business is tougher to enter and run for a new entrant who does not have the scale.

Why cannot one use a simple DCF based framework to value a general insurer? It is simple to draw up projections for the next 10 years basis assumptions of loss ratio, combined ratio, growth in investment book and investment yield.

Why does the book value of an insurer matter much? This is a business that may not need too much incremental capital beyond a scale, there is no leverage involved where net worth needs to be levered. The PBT (assuming underwriting profits are nil) is the investment yield on the Investment Book, not the yield on the Book Value. Won’t P/B trend higher over time for a business that generates good profitability but keeps paying out healthy dividends?

Interested in getting views on this, once the most appropriate way of valuing a general insurer becomes apparent the rest becomes easy.

16 Likes

One simple way to value a company on the basis of Book value is:

P/BV = (ROE - g) / (CoE - g)

where,

ROE = Return on Equity

CoE = Cost of (Equity) Capital

g = Long Term Growth Rate

This is generally used for valuing Banks as they are valued on BV (and not on EPS).

This is one stage model, but it considers all the variables that matters.

Reasonable P/B expands with:

High ROE

High g

Low CoE (or required return from the investor)

Example: With expected ROE = 18%, g = 10%, CoE = 12%,

P/BV = (18 - 10) / (12 - 10) = 4

This model is highly sensitive to the variable. e.g. if CoE is increased from 12% to 14%, then reasonable P/BV crashes from 4 to 2.

But I find this model extremely useful for the firms with very stable ROE, g and CoE (e.g HDFC Bank where ROE remains around 18-21%)

1 Like

Yes and No.

Bajaj Finance is a lending firm and hence should be valued on BV multiples. But Bajaj Finance is in a high growth phase (north of 30% g and would slow down to more stable g and ROE after say 7-10 years).

The limitation of this model is that it is one stage (and not two stage, with one for high ROE & g, and second with lower ROE & g).

Hence if you could plug a long term avg. ROE or g in this model it could be applied.

But if you think Bajaj Finance g & ROE will be very different across two stages (and hence averaging not reasonable) then this model can’t be applied directly, though there is still a way to apply. You extend the current BV to BV of 10th year:

BV(10) = BV(0) * Power((1+ROE),10).

P/BV(10) = (ROE - g) / (CoE - g)

where ROE and g will be long term ROE and G after 10 years, till eternity.

Now you discount P/BV(10) to P/BV(0).

ps: Sorry, I think this discussion on P/BV is actually deviating from purpose of this thread (ICICI Lombard analysis). It’s just that BV multiple came in discussion on valuation earlier on thread so wanted to share one more perspective on how to look at P/BV.

3 Likes

@zygo23554 Completely agree with your views. For an insurance company its the float (investments) which earns the profit and it does not belong to company(share holders). Hence IMO, valuations should ideally be based on quality of float ( how much leverage the float gives to equity and its growth rate) rather than book value or there may be another way of valuing this float.

Till there are no underwriting losses, this float is free rather has negative cost of carry. If there are underwriting losses, this float is just like debt.

I am not a finance guy and rather novice on this subject. Please correct me if I am lagging in understanding…

1 Like

- since Inception, ICICI Bank had management control and NOT Lombard. Gopal, Head - Investments, from Fairfax was leading investments till 2 years ago. Looking at global UW performance of Lombard does not help.

Great Question. Took me some time to understand it, but now that I understood, I realised the beauty of your question

couple of questions…Maybe @zygo23554 can answer.

-

Just like there is CAR in Banks, there must be some ratios in Insurance. Any idea what that is for Gen Insurance.

-

What are the restrictions (if any) on using Float money and also restrictions on using own money

-

Which are the biggest Gen insurers that have failed and why.

-

If Interest rate goes down (like it has currently), doesnt a General Insurer earn less in years ahead. May be there could be some gains on existing bond yields, but longer term ROE comes down na ?

-

Does Insurance Co have to give breakup of Maturity of various investments it holds

-

Do we also have an answer as to how much ICICI Lombard Auto Policy is sold with the vehicle purchase itself and how much is sold after 1 year through Non Auto Dealer route. This is because if customer will now buy 5 year policy upfront, then the winners will be guys selling at dealer level

5 Likes

Well in a DCF, what will u constitute the cost of equity for ICICI. Especially considering float calculations…

A fact explained very nicely below from the blog insuranceinvestor.wordpress.com

Also, I feel this reply was pure Gold

5 Likes