ITC is acquiring stake of up to 33.42% in Delectable Technologies Pvt. Ltd, which operates the Azgo app and vending machines that sell snacks and other fast-moving consumer goods.

ITC will pay up to Rs 7.50 crore ($1.04 million) in four tranches over a period of 12 months for the stake.

The deal will strengthen the presence of its FMCG products in the emerging distribution channel of vending machines.

Bengaluru-based Azgo, earlier known as goSnacker, provides Internet of Things-enabled vending machines that are set up in offices and apartment complexes.

Users can connect to the vending machines, order snacks and make payments via the Azgo app and later pick snacks from the machine. The startup has around 150 vending machines across Bengaluru.

This looks like an excellent move. This will allow ITC to expand its reach to thousands of corporate offices across all Metros, push newly launched products (Like Fabelle) and at the same time gauge the response and preferences of consumers first hand.

ITC is undervalued considering debt free status and consistent free cash flow genertaion. It has ROCE of 34%. They understand niche and know how to scale up. ITC at its prime was most prefferd employer and I still believe current management have the value system ingrained in them.

Matter of time when fmcg starts adding to bottom line as more and more operating leverage comes in to play as they scale up more.

They entering all the new segments with significant market size …rice , milk etc that too has big market locally .

When we bet on hul, we bet on the mnc pedigree and parent. When on dabur or Marico we bet on the integrity of burmans or mariwala, same goes for godrej. Wanted to understand whom are we betting on when we chose ITC…who are the real long term promoters…the management is answerable to whom for long term vision and results…same for institutions like Larsen…these are completely institution owned companies with no promoters…is that a good thing or bad in long run…what is the focus of management and direction…is it a medium term vision to give exit to some owners or very long term wealth creation…who is going to benefit most of ITC or say Larsen grow manifold from here…i am aware gov own significant stake but they will dilute…so will others…who is next generation of promoters…there is no Ambani or godrej legacy…neither hul or p&g link to developed nations hunger for indian growth…how they became so big corporates and who will drive the next big leg? At least for Larsen group companies, we have clear target statements from mr Naik and how they are achieving them with deadlines…couldnt find a Naik man or such targeted vision for ITC. Any insights and thoughts most welcome!

Disc. Hold tracking position in ITC. Thinking of adding more but above thoughts keep stopping me…

ITC : Long term Shareholder is BAT in addition to large financial institution

ITC employees ( Mid , Senior & Top) own decent amount of ESOPs - and have a strong reason to drive long term stock performance .

ITC finance team is pretty demanding and tends to demand that most commercial business drive return higher 10% ROCE . ITC had long 10/15 years of investment cycle in creating new brands , categories building integrated supply chain . It is possible one of few companies that invested in building new categories and made them into reasonable success in last 10 years …

It converted many of rental offices / employee housing/ factories / warehouses in to owned properties ( in era when commercial rentals are going up by 10% and most FMCG sales growing less than 10% - This will be important expenses management )

Now it is time to harvest … It is trying to cut down dead woods like lifestyle business , drive profitability in FMCG business … Lets see what is real value that has been created …

Did any one see their Latest range of products in shops around them ? Specially Juice tetra packs ( can’t recall the brand name ) , chocolates , pocket perfumes, Flavored Milk etc

Some one I am not able to find it in most shops that I have visited during last 5-6 months including food Bazar and small/mid sized mom and pop shops in Andheri West area.

Not sure if they have proper distribution channels established for all these products or not or may be shops not ok to keep it due to some reasons .

Would like to know observations from VP community too …please do mention area if you managed to find / could not find these products range in specific.

Ashirwad, Sunfeast noodles/biscuits , master chef are available at most places

Juice Tetra Pack is visible only in Summers - Brand name is B Natural popular flavour is Guava and Litchi - I see them more in hyd vs Mumbai - But you get them online on Reliance / Dmart etc

Chocolates : Fabelle gourmet varieties - you need to visit their five star hotels for feasting on them .

Deos - Engage has 10% Mks & is No2 / No 3 in India after Fogg ( 16% Mks ) - You can google its Mks - you will neilsen data

Flavoured Milk / Ghee - You may find them bangalore or Amazon site

Noddles Yippee is No 2 with Mks of 16% - 22% after Maggi

Atta : Ashirwaad is No1 with 35 % Mks

Sunfeast has around 15% overall Mks but has high Mks in Premium varieties

Is P/E of 15x for cigarette business alone justifiable by comparing with global developed country’s companies ? There is only 11% legitimate cigarette market in india. Will this 11% increase if govt take actions to curb illegal cigarettes ?

Even discarding the above point, locally, we have VST trades at 24x (RoE is 35%) and Godfrey at 18x (RoE is 10%) which are the other companies with ONLY cigarette business. why can’t we value at least 20x for this high profitability free cash flow (i guess RoCE is 400%) cigarette business ?

Cigarette = 20 x 12000 = 240000 Cr

cash = 30000 Cr

FMCG, Hotel, Paper, etc., = 25 x 2500 = 62500 Cr

Total = 332500 Cr

Is it not a conservative valuation.?

Disc: bought some shares of HUL today. Intend to buy more, if it corrects further.

Post the merger, GSK has expressed that they would look to liquidate all their holding in HUL which will be around 6%. That, to my mind is exerting some downward pressure on the stock.

A correction based on technical reasons in an otherwise sound business is what I crave for. I hope, this is one. That’s why the buying impulse.

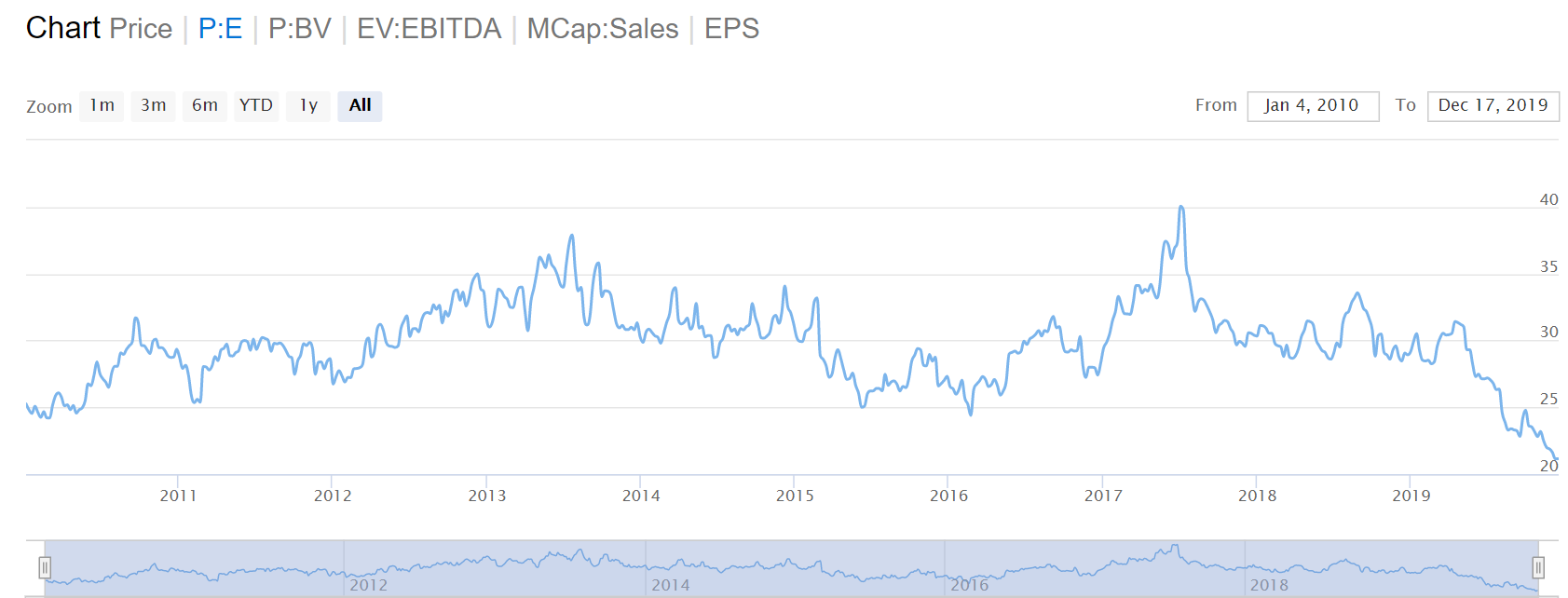

This is only the 3rd instance in the last 10 years, when the PE ratio for ITC has gone below 25 as shown in the chart. 28-32 is the range where the number has lied for the majority of this period.

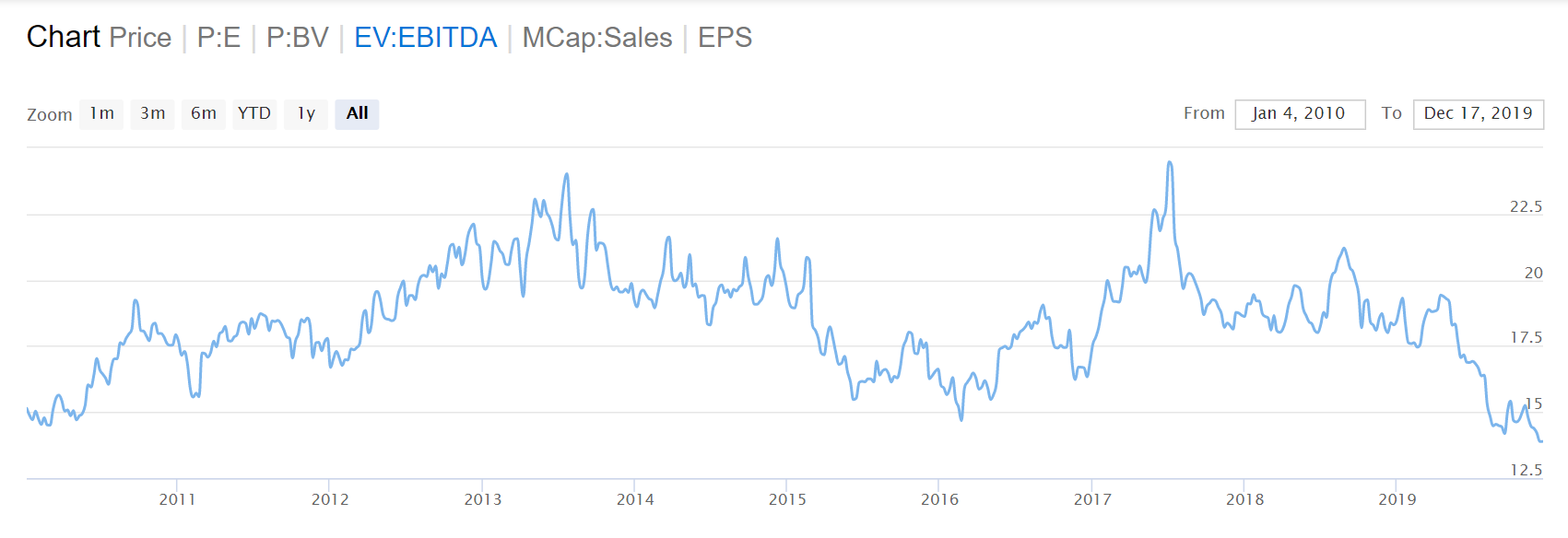

Similar this has happened when I look at the EV/EBITDA ratio, which has gone below 15 only on 3 occasions(3rd being current one). Here the ratio has lied in the range of 17.5-19.5 for majority of this period.

If I were to take the bottom of these 2 ranges and calculate the fair valuation for the stock, I get an upside of 31%(based on PE discount) and 26%(based on EV/EBITDA discount). Thus even from a conservative scenario, ITC’s price should be around Rs 300.

Good analysis Puneetc,

I have initiated Buy call two days back only at 235-237 range.

I strongly believe Valuations divergence won’t sustain much longer.

Revenue Mix of ITC improving on FMCG side.

Believe huge outperformence from the Stock

Market is more keen to Revenue Mix

FMCG never beat Profitability of Cigarette but give better Value & Volume Growth with stability.

May be in next 2-3-5 Years ITC may treated as FMCG major contrary to Cigarette major as of now

ITC is leader in two major segments, cigarettes and aashirvad aata. Bingo, sunfeast, fiama di wills, stationary products, agri products and even their hotels business are runner ups. The question is not of quality but branding and marketing. ITC brands lack awareness.

They already sold John Players and are in the process of winding down wills lifestyle.

Cigarettes is a different market. There are no real competitors to match the size of ITC.

Also, ITC has no presence outside of India in hotels or FMCG.

It will take a lot more effort for ITC to convert itself into a major FMCG company from tobacco.

Investors have realised this and this is reflected in its stock price.

Unilever on the other hand is a MNC. It has delivered hits after hits. Same goes for Colgate Palmolive, gillette and Nestle. These are all present in multiple geographic markets with strong brand names.

The real problem is probably the lack of marketing prowess at domestic FMCG companies who can skillfully take on these FMCG MNCs.