2 Likes

1 Like

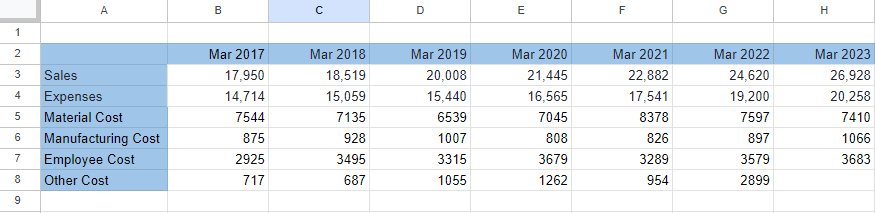

Looking at the above numbers. Since 2017 Sales has increased by over 50 percent i.e around 9000Cr while the Material Cost has remained the same, just around 200Cr addition to Manufacturing cost and around 700Cr addition to Employee cost.

What should one make out of this? Doesn’t these numbers say that HAL is more of an integrator/assembler than a manufacturer?

If that’s true, it’s a good business wrt return ratios but then the only moat that remains with HAL is that it is able to procure orders from the government.

1 Like

3 Likes

Defence ministry released its Fifth indigenization list of 98 items, to be procured by the armed forces under Atma Nirbhar Bharat.

Latest Order book position of all Defence stocks discussed

1 Like

HAL enters into a contract Supply of RD-33 Aero Engines for MiG-29 aircraft, for Rs approx 5,200 crores

1 Like

HAL published its FY24 Results today - a good set of numbers in line with expectations .

Revenue during the year jumped 13% to Rs 30,381 crore. The same stood at Rs 26,927 crore a year ago. It’s consolidated net profit increased 31% to Rs 7,621 crore crore as compared to Rs 5,828 crore of FY23.

Importantly, margins during the March quarter improved to 35 % as against 25.9 % a year ago.

Execution continues to remain a key parameter.

3 Likes

Phenomenal Investor Call Yesterday! Putting a few important pointers as I noted during the call

- Highest Revenues at 30238 Crores-13%

- Strong Pipeline.

- Manpower cost reduced to 23% from 2019 to 17% of revenue further reduction to 15% by next year. (My opinion is this means margins may be sustainable in this band)

- Overhead cost reduction from 8% to 3.5%.

- Reduction in inventory from 359 days in 2018 to 159 days now. Will not be reduced further.

Initiatives for growth

-

Capability and Capacity building.

-

New factory for LCA Tejas operational from October 24

-

Capex of 3000 crores per year for 5 years- total 15000 crores

-

IMRH and GE TOT deal require capex

-

50,000 ton hydraulic press launched

-

Self relaince and indigenious technologies needed to reduce need for foreign sources, Reduce licence production

-

4000 crores R&D for IMRH. 2000 Crores for Naval LCH

-

Tremendous oppurtunities for exports

-

15% PAT for R&D to enhance capabilities.

-

End to End Solution provider for Aeronautical solutions

-

Order Book is 94,000 crores. 12000 crores addition even after sales of 30000 crores. Engines-ALH, Navy Dornier upgrade.

-

Order book 47000 crores should materializes this year. 1.20 Lakh crores by next year even after sales.

-

Important is various lines of ALH, LCA MK-II and LCH etc total AON of 1.6 Lakh crores is done. Orders will flow in 18-24 months. This is over and above the 47000 crores order for FY-25

-

This will keep manufacturing lines occupied till 2032.

-

FY25 -deliver of LCA MK-1a and LUH

-

FY26 -HTT40, Civil Trainer

-

FY-27: Marine Helicopter, LCA MK_II, Medium role aircrafts.

-

Safran IMRH and GE TOT new engines in next few years.

Disclosure: Own in Family Accounts since last year.

9 Likes

HAL’s Aerospace division expanded to support production for Six LVM3 rockets per year as against its current capacity of only Two LVM 3 rockets.per year

As of the end of the 2023-24 fiscal year, the company’s order book stood in excess of ₹94,000 crore with additional major orders in FY25.

The company has forecast its EBITDA margin to be around 32% to 33% in the next two years.

The company said it has a robust order book and a very strong pipeline of orders. It added that it is confident of sustaining its FY24 growth momentum.

1 Like

will not move the needle for the company in terms of revenue or profit. Its a sub 2000 crore order book overall, I think.

Impact on HAL will be interms of whether stated defence orders come through and its engine JV and orders get completed. Only thing that is to be monitored.

Discl: No change in Holdings.

2 Likes

Agree, this LMV3 capacity expansion may not add significantly to its kitty.

But I see it as positive for a PSU company which is trendy And forward looking.

overall Order book goes on increasing and execution quality not bad for a PSU.

When I entered the stock @Rs 1200 a piece in 2022, I had a lot of hesitation, But after having entered the stock and after a little bit of research on Atma Nirbhar Bharat , i was excited to put more money in to it during its journey from 1200 to 1800… it went up to Rs 3800…and then there was a split 1:2 to bring it’s price back to 1900 and now the journey up to Rs 4700 ex split

I am proud to own this stock since then…no looking back as long as the order book , execution quality , and margins remain healthy.

Being a PSU stock, i keep getting good dividends irrespective of bear or bull market…The lesson is it pays off if one holds a quality stock for a long term without bothering in to short term volatility, QoQ sequential growth .

2 Likes

The company’s order backlog is (Rs 94000 crore at 3.1x FY24 revenue) and order pipeline remains robust.

Including this contract, management has been guiding for order inflows worth Rs 1.6-1.7 trillion (1.6 -1.7 lakh crore) in the next 2-3 years where the government has already provided approvals, as per ICICI Securities

1 Like

Are they the only bidder. Or will there be anyone else please

HAL is the only Company in india making LCH ad i believe the order is awarded under Atma Nirbhar Bharat.- Self reliant India

There’s no bidding here, Prachand is an HAL platform. 4 LSP units (2 each for IAF and Indian Army) were on user trials since almost a year.

4 Likes

HAL now more valued than NTPC & Tata Motors , Kotak Mahindra Bank as Market Cap.crosses 3.66 Lakh crore

Prachand IC engine indigenous content to increase from 45% to 60%

https://idrw.org/lch-prachand-ic-stuck-at-45-hal-plans-to-increase-it-further/