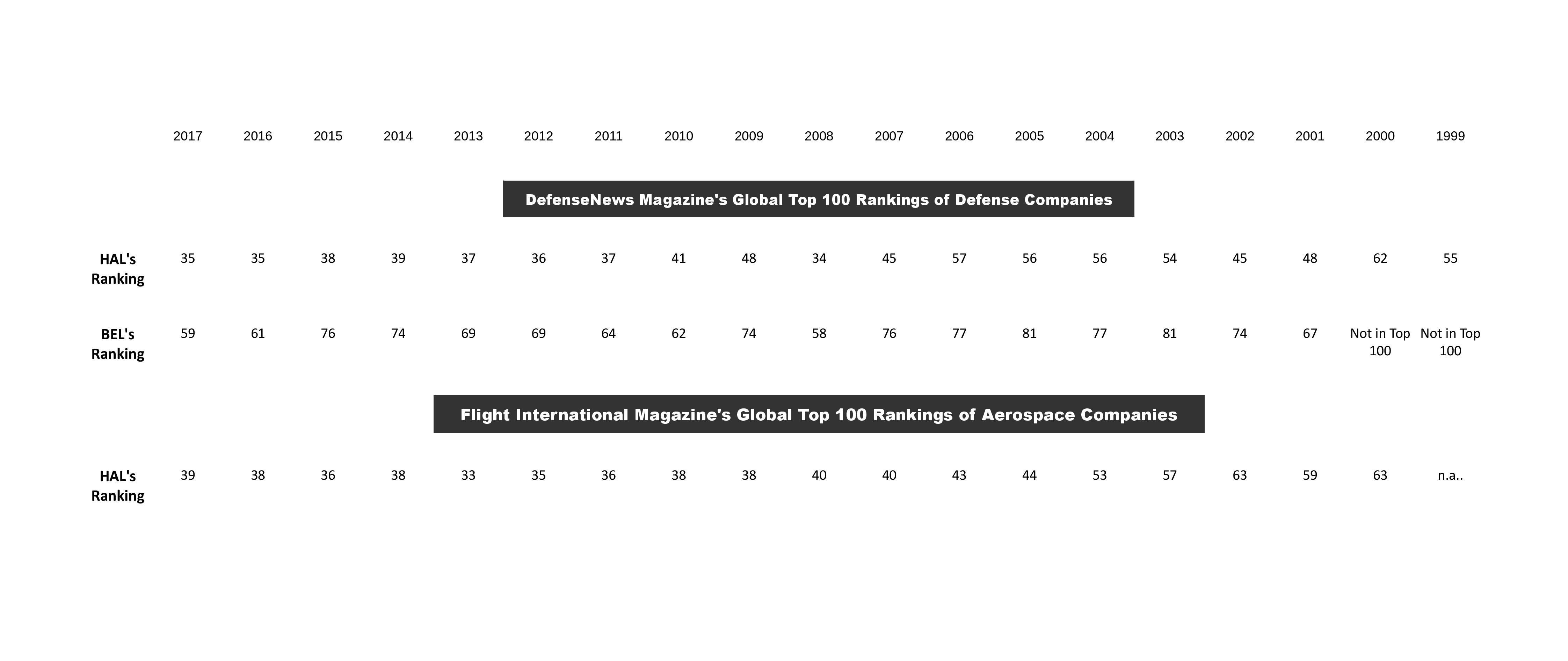

Hindustan Aeronautics Ltd. (HAL) is the Largest Aerospace company of India, one of the biggest Aerospace companies of Asia and amongst Top 50 Aerospace companies of the world. If we do a strict like-to-like comparison of companies that are present across the entire value chain and possess capability to offer end-to-end solutions starting from design of a flying platform to its manufacturing to its support – HAL is amongst the Top 20 companies of the world. Its worthwhile to note here the current and historical world ranking of HAL as mentioned by two leading industry publications viz., Defense News and Flight International. Here, we have also stated the ranking of Bharat Electronics Ltd. which is the only other company from India, apart from HAL, which finds mention in Top 100 global defense companies :

Will not go into much detail regarding the business of the company and its offerings as for that one can refer company’s RHP – link of which is provided below :

http://www.cmlinks.com/pub/dp/dp12030.pdf

Usually I don’t prefer investment in a PSU company as the biggest turn-off for me has always been the work culture followed and the government dictat overhang. However, despite these odds, why I got attracted towards this company as a good IO is because of the following reasons :

– Today, India counts itself amongst only seven countries in the world that have the capability to manufacture a fighter aircraft right from scratch i.e., design, develop and manufacture a fighter aircraft — HAL has been one of the major reason for this ;

– HAL’s positioning in Indian defense segment is indispensable and no competition can emerge for this company in forseeable future – any private player will need to spend decades and burn a huge amount of cash (even with support from a foreign player) to build even half of the vast infrastructure that HAL has built over last seven decades in terms of more than 2500 acres of land in possession in various parts of country, state-of-the-art machineries, experienced personnel with deep knowledge, huge library of flaws and shortcomings that are experienced by flying platforms during actual use in Indian conditions and ways to overcome them, etc.

– Its therefore no surprise that :

75 % of all flying platforms in use today (fighter aircraft, trainer aircrafts, helicopters, transport fleet) by Indian Air Force (IAF) are supplied/supported by HAL,

66 % of all flying platforms in use today by Indian Navy are supplied/supported by HAL,

100 % of all flying platforms in use today by Indian Army are supplied/supported by HAL,

100 % of all flying platforms in use today by Indian Coast Guard are supplied/supported by HAL,

– Company has so far produced 4090 aircraft and 5005 Engines

– With such dominant positioning, there also exists exceptional financials’ track-record with :

23 Years’ CAGR in Revenues at 12.80 %,

24 Years’ Average RoE of 19.82 %

24 Years’ Average RoCE of 30.26 %,

24 Years’ Average EBITDA Margin of 11.48 % (with consistent profitable growth achieved each year over last 24 years),

24 Years’ Average PAT Margin of 12.68 % (with not a single loss posted in any fiscal over last 24 years),

13 Years’ EBITDA to Operating Cash Conversion at 51.46 %

24 Years’ cumulative total absolute R&D spend at whooping 13,902 cr.

24 Years’ Average Spend on R&D as % of Sales at 7.65 % (one of the highest in the industry),

24 Years’ Average Dividend Distribution as % of PAT at 24.65 % (with actual, as we can see from reported accounts, dividend payment track-record each year over last 24 years and management stated dividend payment track-record each year over last 40 years),

24 Years’ Average Debt/Equity of 0.19 (with current FY17 gross D/E of 0.07 and on net level cash surplus),

And

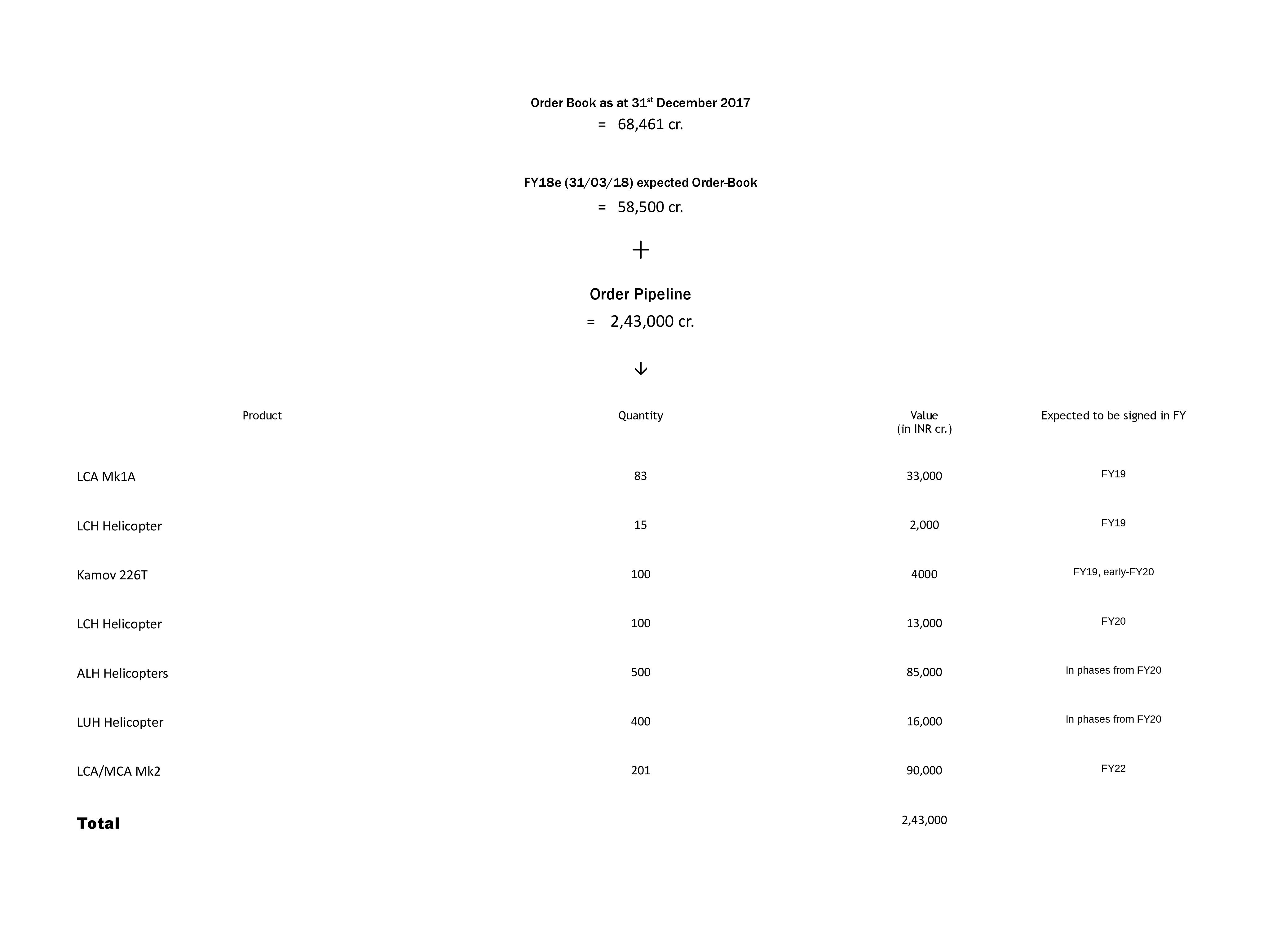

– Besides glorious past that we can see from above, future also looks promising with current FY18e order-book at 58,500 cr. (~3x FY18e Revenue) and expected order booking worth 2,43,000 cr. (~13x FY18e Revenue) over next four years,

– Apart from all these, its also macros which also seem to favour this company currently –

→ with Capital Outlay on Defense hovering around 23-24 % of total Defense Budget since last five years with a dire need to increase it to enable our forces to effectively tackle provoking neighbours,

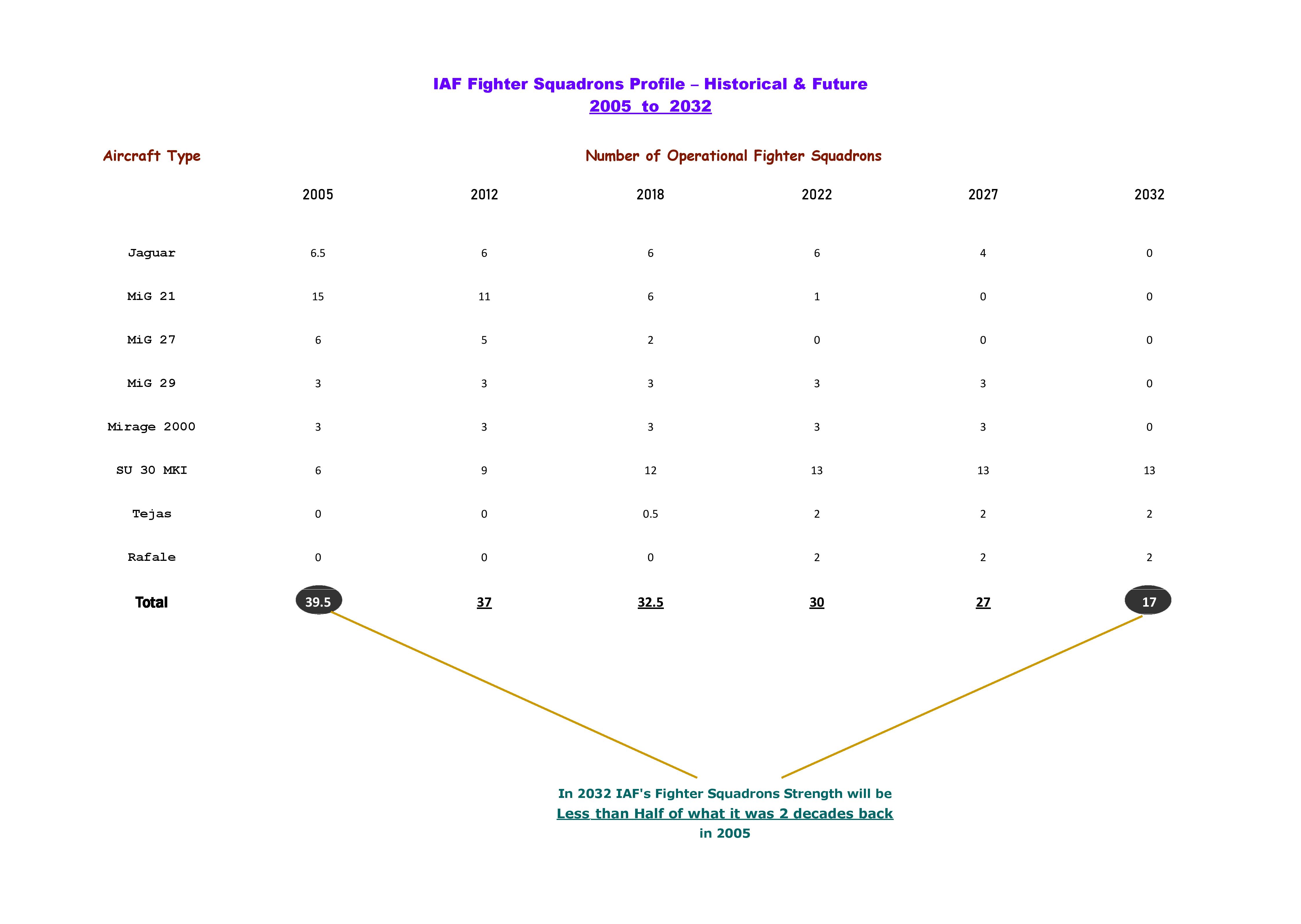

→ with ‘Aircraft & Aero Engine’ allocation, which constitutes major portion of Capital Outlay (average 35 %), requiring a significant uplift in near future to arrest the dwindling strength of Air Force (by 2025 with no new addition, fighter aircraft strength will fall to just 360 – just slight ahead of Egypt and Pakistan and 1/4th that of China) ----[it is interesting to note that if we map a trend of past 20 years then HAL revenue have remained at average 60 % of respective ‘Aircraft & Aero Engine’ allocation amount]

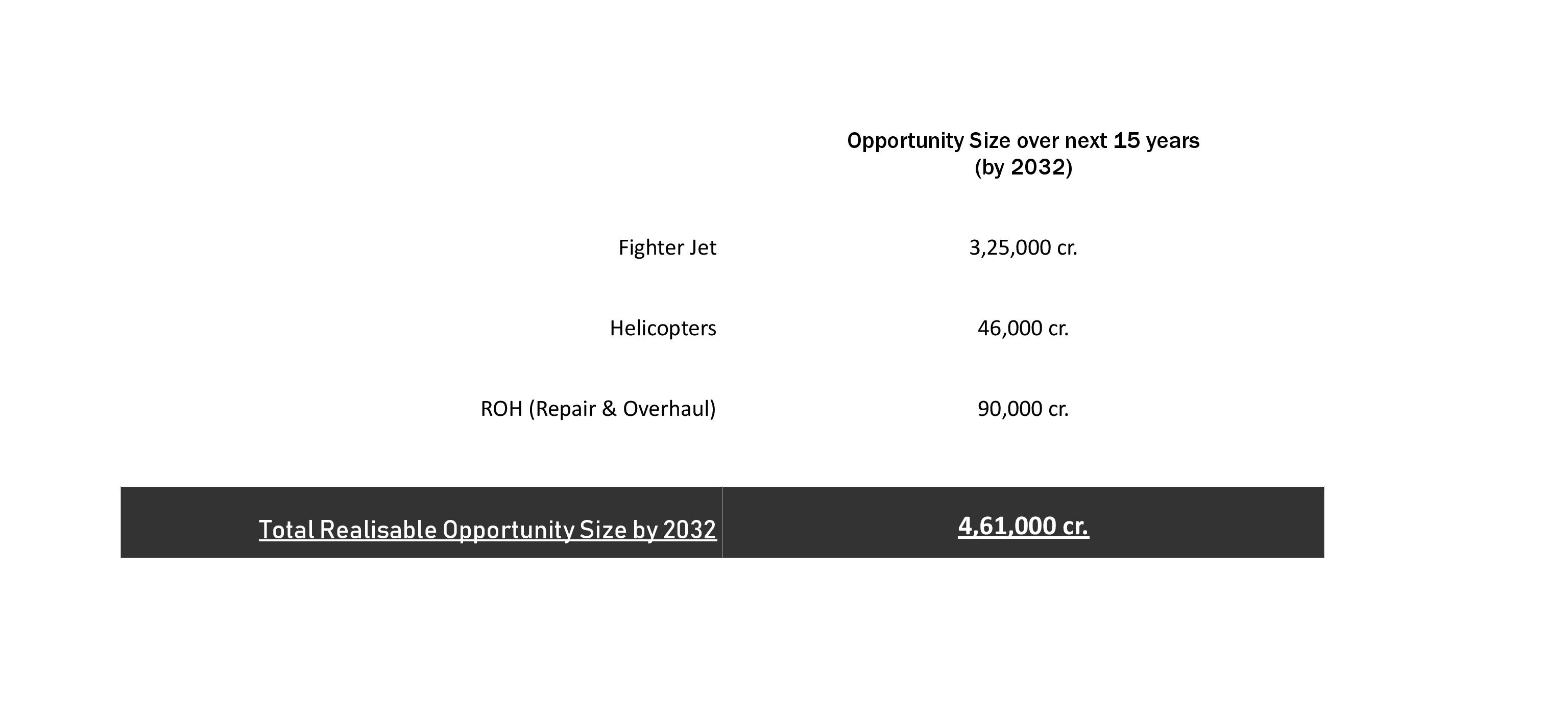

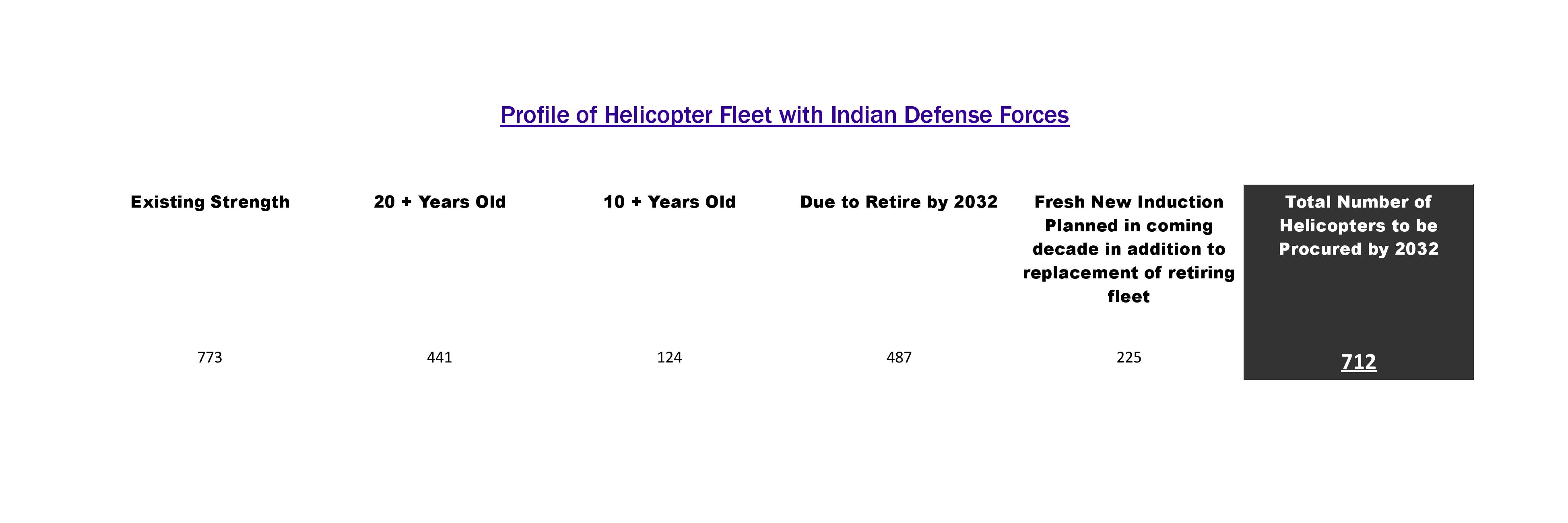

→ DProP-2018, draft of which is recently released, calls for significant increase in HAL flying platforms’ capacity, increasing level of indiginisation, exploring export opportunities as also overseas acquisition opportunities thereby making India amongst the top 5 countries in the world in Aerospace & Defense industries.

Link for DproP2018 :

Lastly,

– despite glorious past, promising future and favourable macros, HAL – one of the largest Aerospace & Defense companies of Asia – is trading at cheapest valuations as compared to global peers as well as Indian peers who are hardly 1/10th of its current scale of operations.

Let’s discuss in slight detail with statistics below :

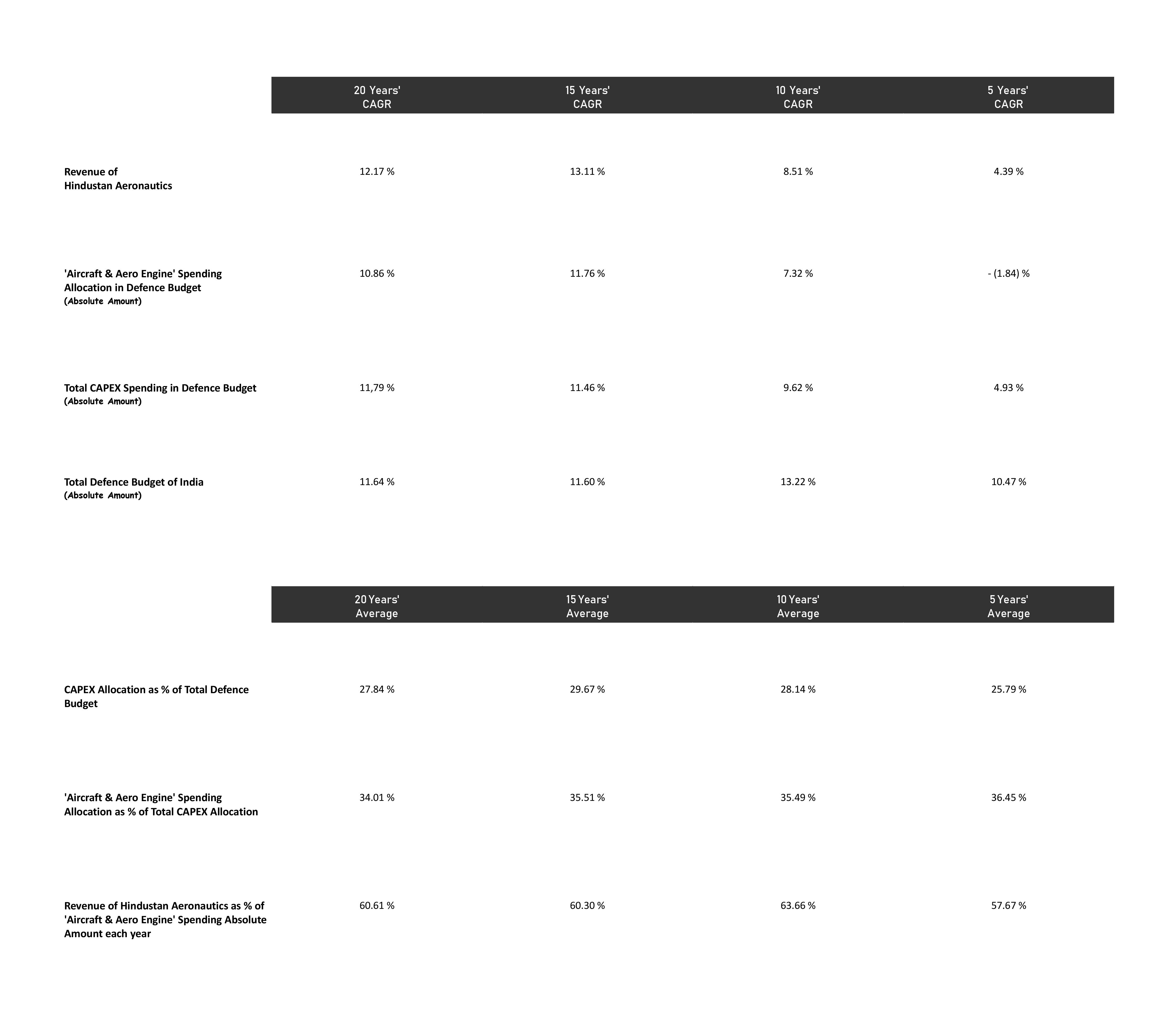

First Macros, – refer following table :

As can be seen from above :

– Overall Defence budget of India (including pensions) has grown at a healthy pace of 11.64 % (CAGR) over last 20 years as also 13.22 % and 10.47 % (CAGRs) over last 10 and 5 years respectively

– However, CAPEX spending has lost pace over last 5 years by growing at just 4.93 % (CAGR) which has severly dented our defence forces’ ability to effectively fight and win a two-front war (with Pakistan & China) in case war extends longer.

– ‘Aircraft & Aeroengine’ allocation which deals with purchase and support of flying platforms like fighter and trainer aircrafts, helicopters, etc. which has always been a major beneficiary of CAPEX spending (with 35 % + allocation) has infact exhibited negative CAGR over last 5 years. Because of this, today, our IAF stands at a critical juncture wherein if no steps are taken immediately, within 7 years, its stregth will dwindle by almost 40 % which will make it unfit to fight a two-front war effectively. Just refer the table below :

– Each Squadron consists of 18-20 fighter aircraft. Because of ageing fleet, 12 squadrons are up for retirement over coming 5-6 years (already IAF is using majority of these aircraft beyond their certified life). This effectively means a shortfall of 288 fighter aircraft (by 2025) projected as of today when Pakistan is increasing its AF fighter fleet substantially with support from China. Any substantial increase in any of the neighbours’ current projected strength (by 2025) will necessitate more addition.

– Do refer the first table again – as we can see, if we calculate HAL’s reported annual revenue with that respective fiscal’s Indian defence budget spending on ‘Aircraft & Aeroengines’, then, HAL revenue has on an average been 60 % of that.

– Also, although HAL is a direct beneficiary of increase in ‘Aircraft & Aeroengine’ spending, its revenue CAGR has outperformed ‘Aircraft & Aeroengine’ spending consistently over last 20 years.

Company- Specific financials & order-book :

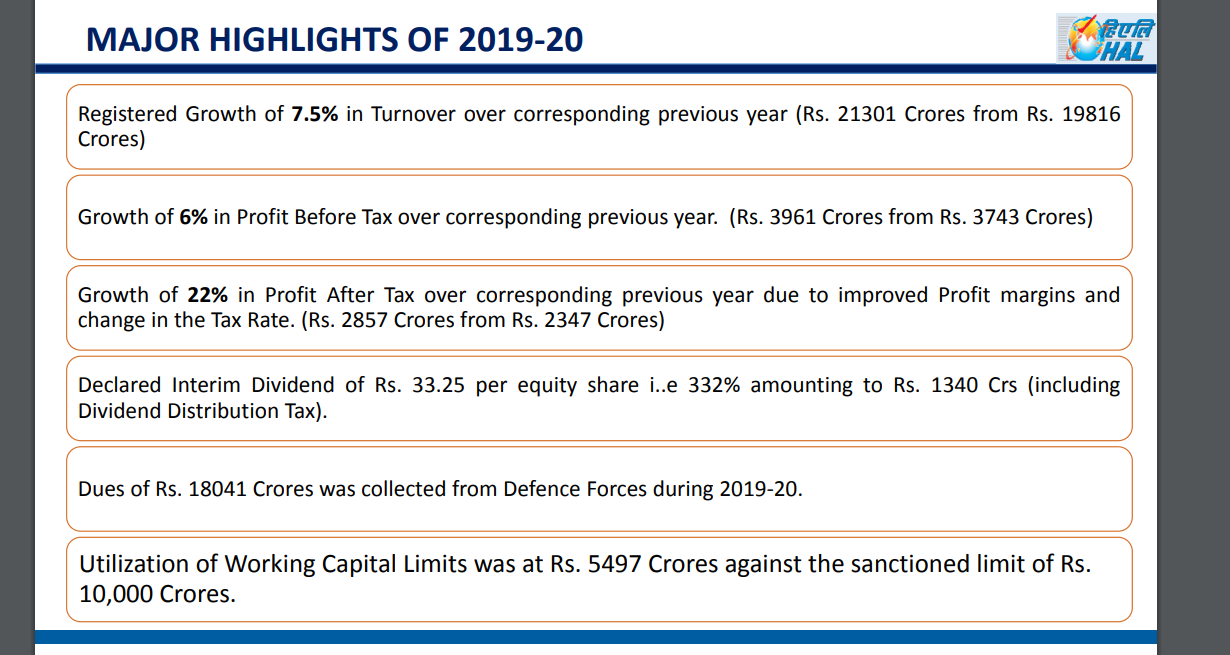

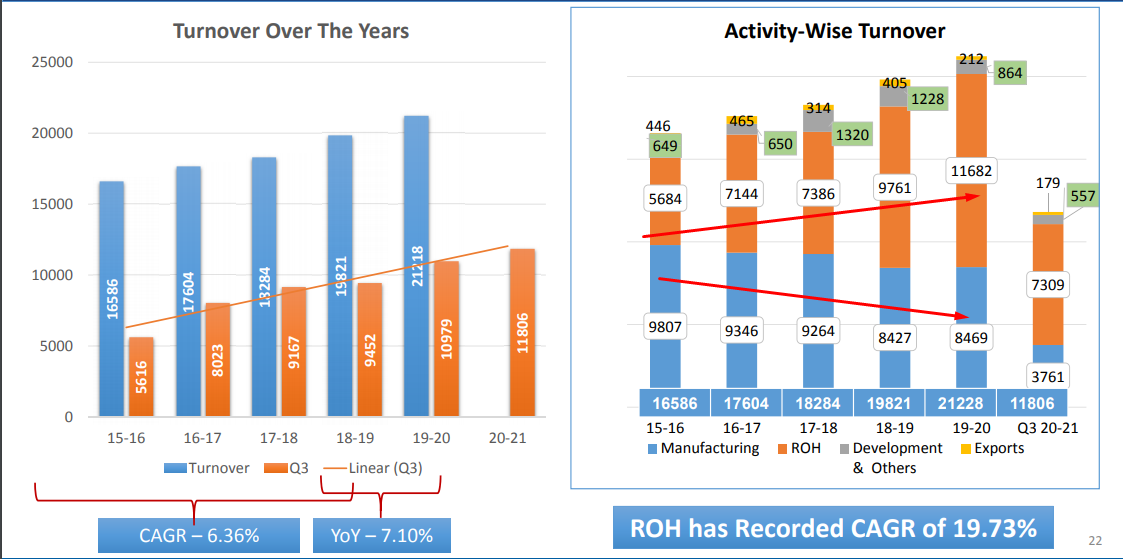

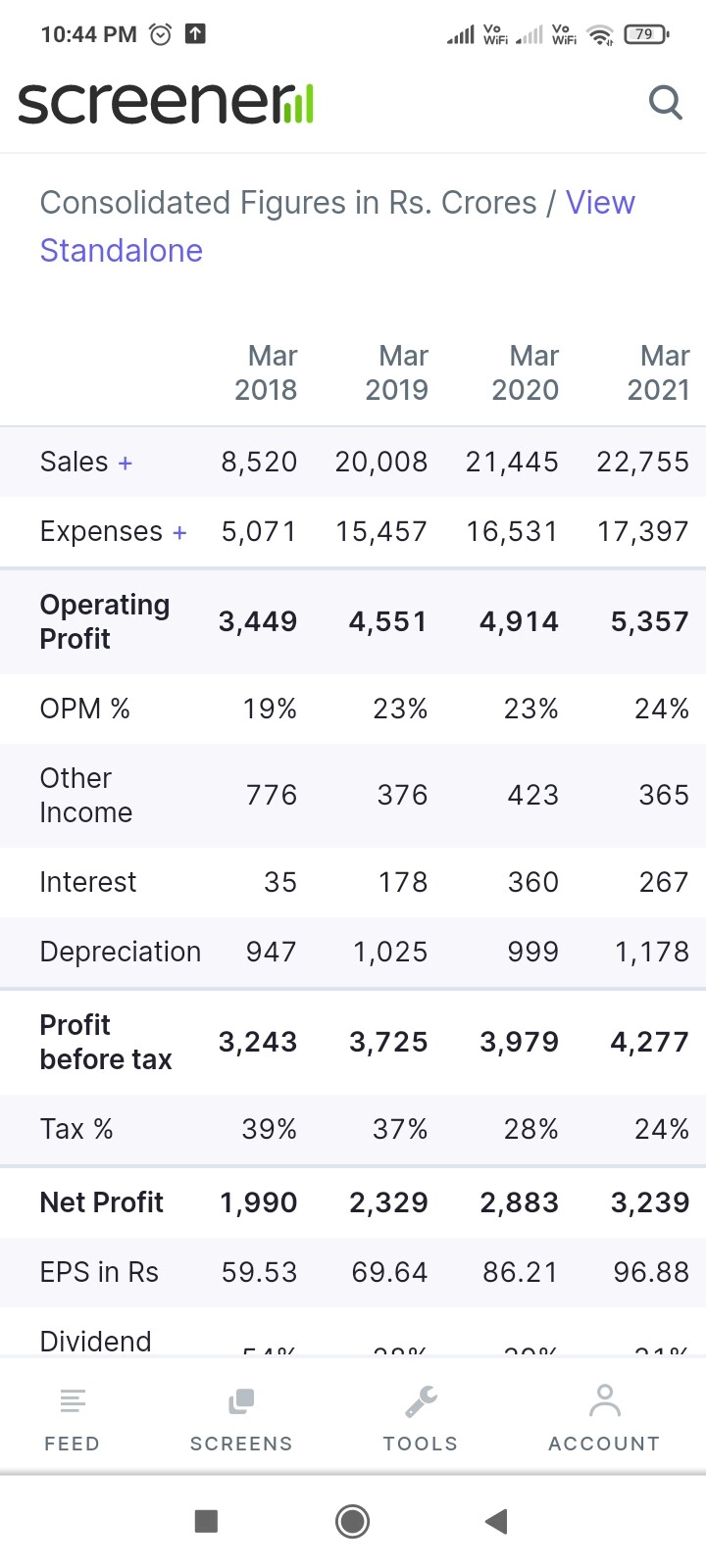

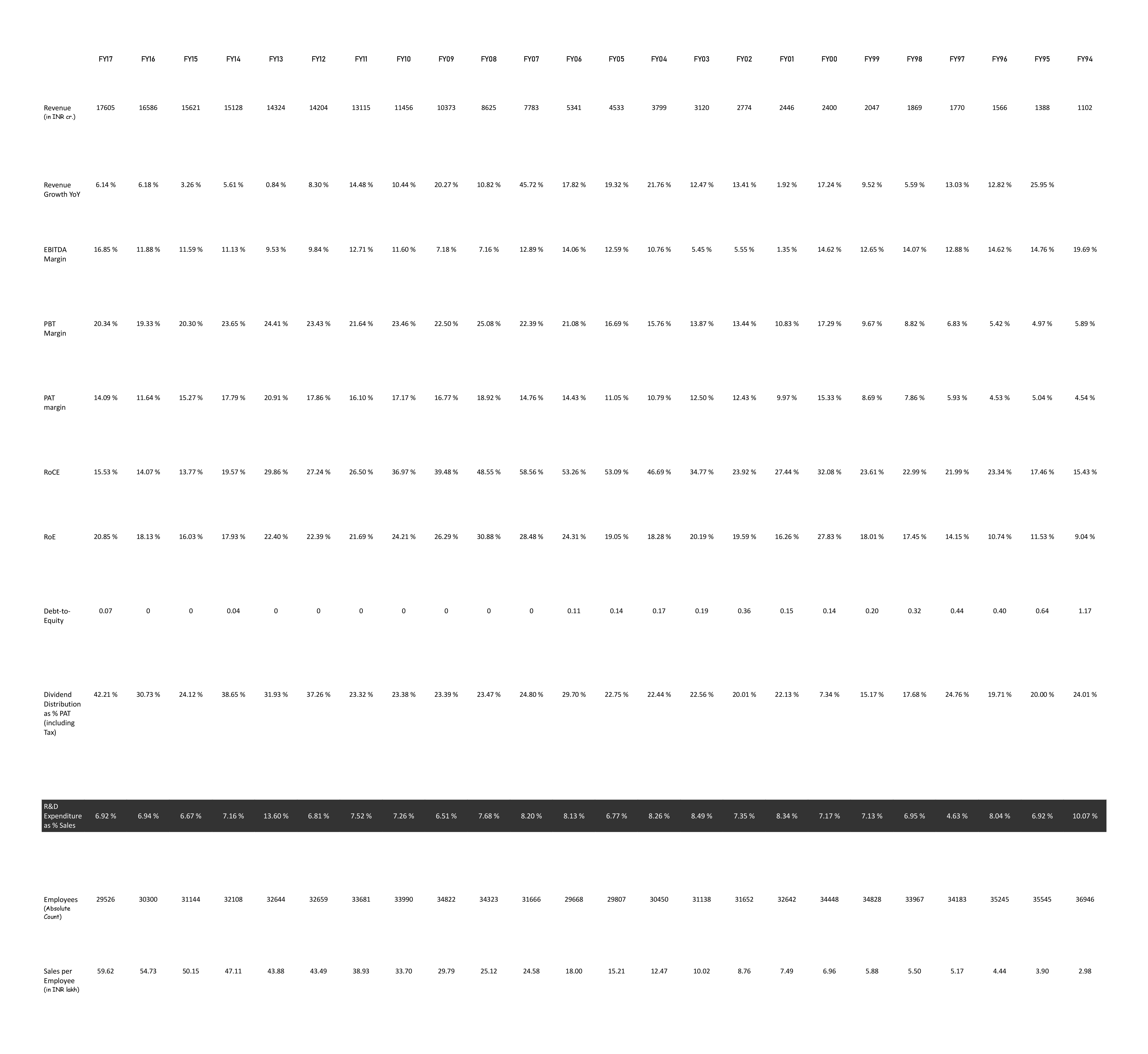

After discussing Macros, let’s shift our focus to company-specific discussion. First let’s refer financials over last 24 years in table below :

As we can see from above,

– HAL has grown its revenues each year over last 24 years although growth has been lumpy with some fiscals turning low single digit growth and some fiscals turning extremely healthy double digit growth. This is the nature of business and is consistent across most of the global peers we observe. This is because the product manufacture cycle is so long (around 6-10 years) and regulations for actual approval and delivery of products are so stringent that it takes time. Also, company follows an accounting policy wherein revenues are booked only when actual delivery of the product happens and not on percentage-work-completion basis.

– Company has been EBITDA positive each fiscal over last 24 years although margins vary from low single digit to low double digits with average coming at around 11 % on long-term-basis. Product-mix as well as delivery execution plays part in this as contracts stipulate penalty for delayed delivery and so provisions in a particular year can dent margins.

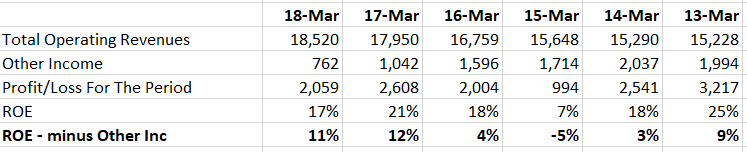

– HAL has been PBT & PAT level positive each fiscal over last 24 fiscals with last 12 years’ PBT margin consistently at 20 % + and last 12 years’ PAT margin consistently at 14 % + barring one odd fiscal. This is because of the huge cash company holds (and other income

it derives from it) because of advances given by customers (primarily defence forces) and milestone payments. This is a trend across all DPSUs which are involved in complex long-term projects and customer calculates product pricing while taking into acccount ‘Other Income’ that will be generated by HAL (or for that matter any DPSU) from the cash given as advance. Hence, this trend is likely to continue in future too although in short-term over coming one or two fiscals, if there is no fresh large order booking, level of ‘Other Income’ might come down as current order-book is approaching delivery dates.

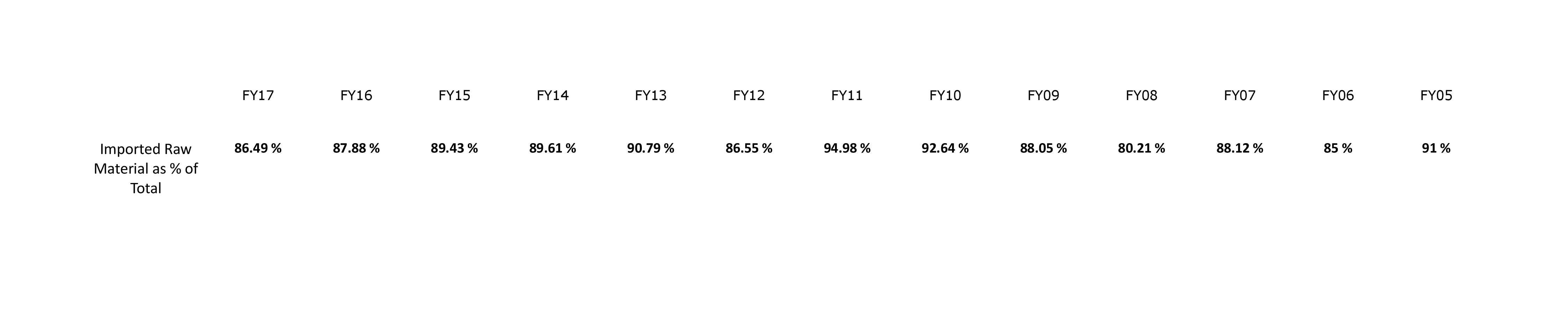

– R&D expenditure as % of sales has been almost consistent over last 24 years’ averaging out at around 7 % which is one of the highest in the industry.

Now, let’s turn our attention to order-book in table below :

As can be seen from above, company is sitting on a huge opportunity in terms of order bookings.

Valuation :

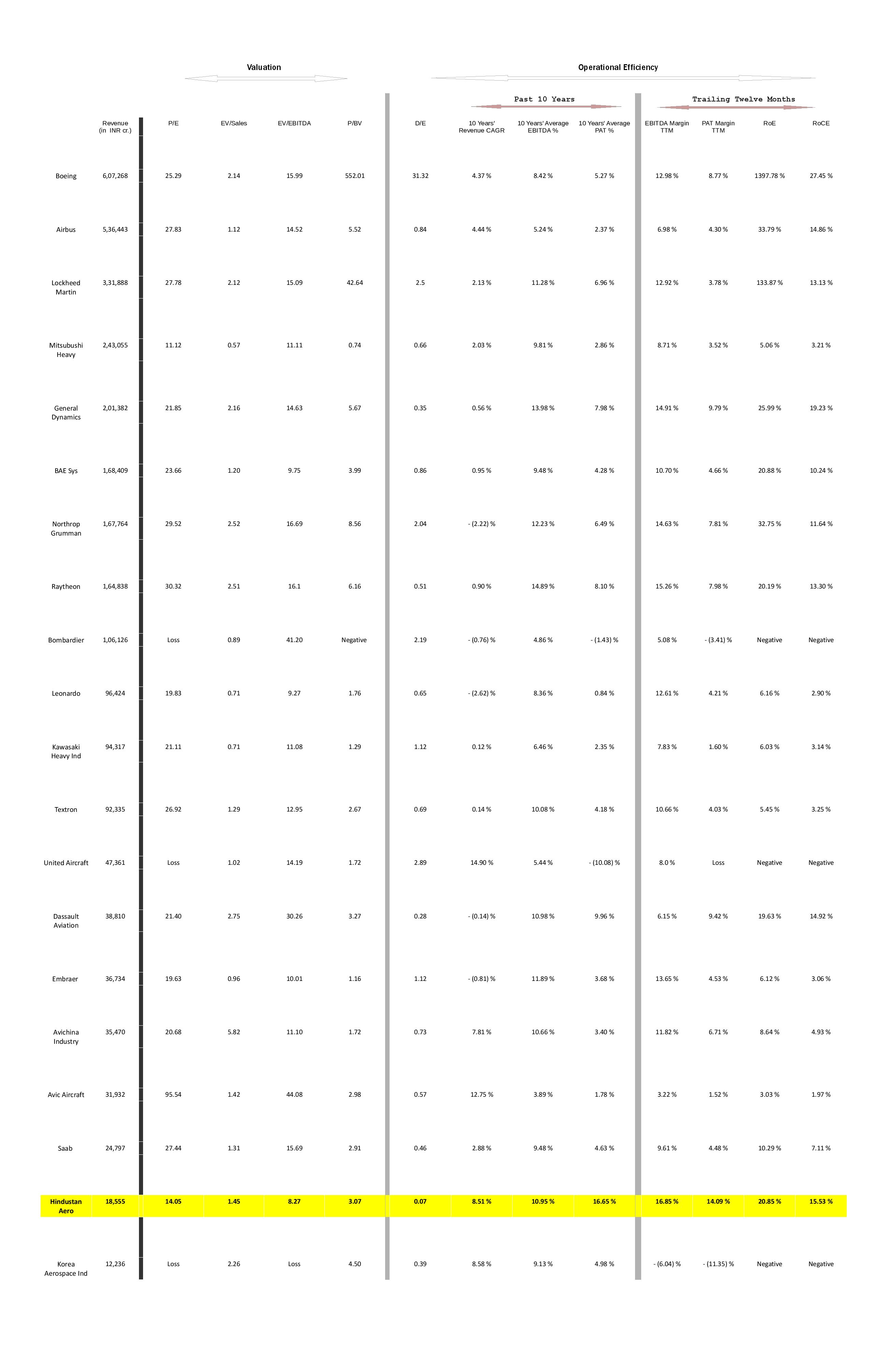

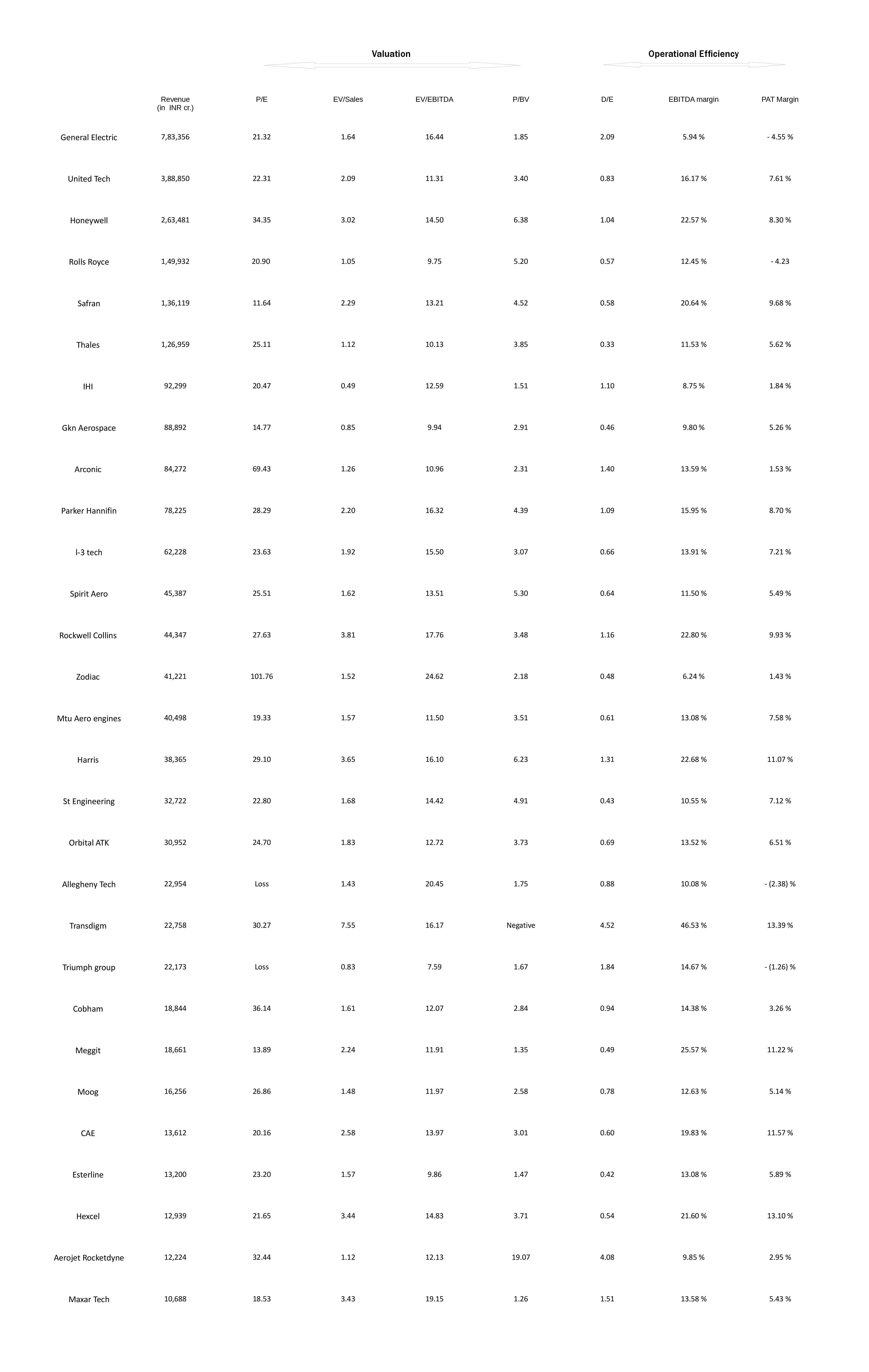

This is the most interesting aspect with regards to this company. Despite it being the largest defence PSU of India and one of the largest defence companies of Asia with many of its global as well as Indian peers inferior on varied and almost most of the financial parameters than HAL ; still, HAL today trades at relatively low valuations than most of them. Refer following table which gives an overview of almost all the l-t-l global peers of HAL :

– Revenues of all companies are stated in INR cr. with INR conversion rate of respective reported currency taken as at 31st March 2018.

– Many of the peers mentiioned above like Mitsubushi, Kawasaki, etc. have revenue streams other than defence/aircraft which contribute majorly to their financials ; however, we have sorted the companies based on the size of their overall operations and not by actual revenues coming from Aerospace & Defense segment.

– On 10 Years’ Revenue CAGR basis, only 3 companies have outperformed HAL and they are United Aircraft of Russia, Avic Aircraft of China and Korea Aerospace of South Korea. However, in terms of operational parameters, all these three companies are far more inferior than HAL whether we compare 10 Years’ Average EBITDA & PAT margin or RoE & RoCE.

– Another company that comes close to HAL’s 10 years’ revenue CAGR is Avichina Industry, again from China, but, here too, if we check operational paramters then its 10 Years’ EBITDA margin are almost similar but all other parameters inferior.

– Overall, evenif we leave aside consistent superior RoE & RoCE of HAL and only concentrate on business specific matrix like 10 Years’ Average EBITDA margin achieved and D/E aspect then HAL ,on the whole, turns out to be one of the best company amongst all peers except Raytheon who also has a portion of revenues coming from high-margin defence/commercial electronics segment.

Now, after looking at global l-t-l peers, let’s turn our attention to Indian peers — one fact here we need to note is that there are no listed (or for that matter unlisted) peers that can be compared to HAL since HAL is currently enjoying an almost monopoly in Aerospace segment related to defence and it only competes with global peers mentioned in above table for most of its contracts. Hence, what we did is we compared all prominent Indian listed entities which have some or major revenues coming from defence segment. We have divided our comparison in two parts – one Indian Private Sector companies and other Indian DPSUs for ease in reference. Refer following table :

– As can be seen from above, HAL enjoys consistently highest PAT margins and therefore highest RoE amongst all the companies – whether its Private sector or Public sector.

– Also, HAL is trading at one of the lowest valuations (on varied valuation multiples) as compared to both , private and public sector entities.

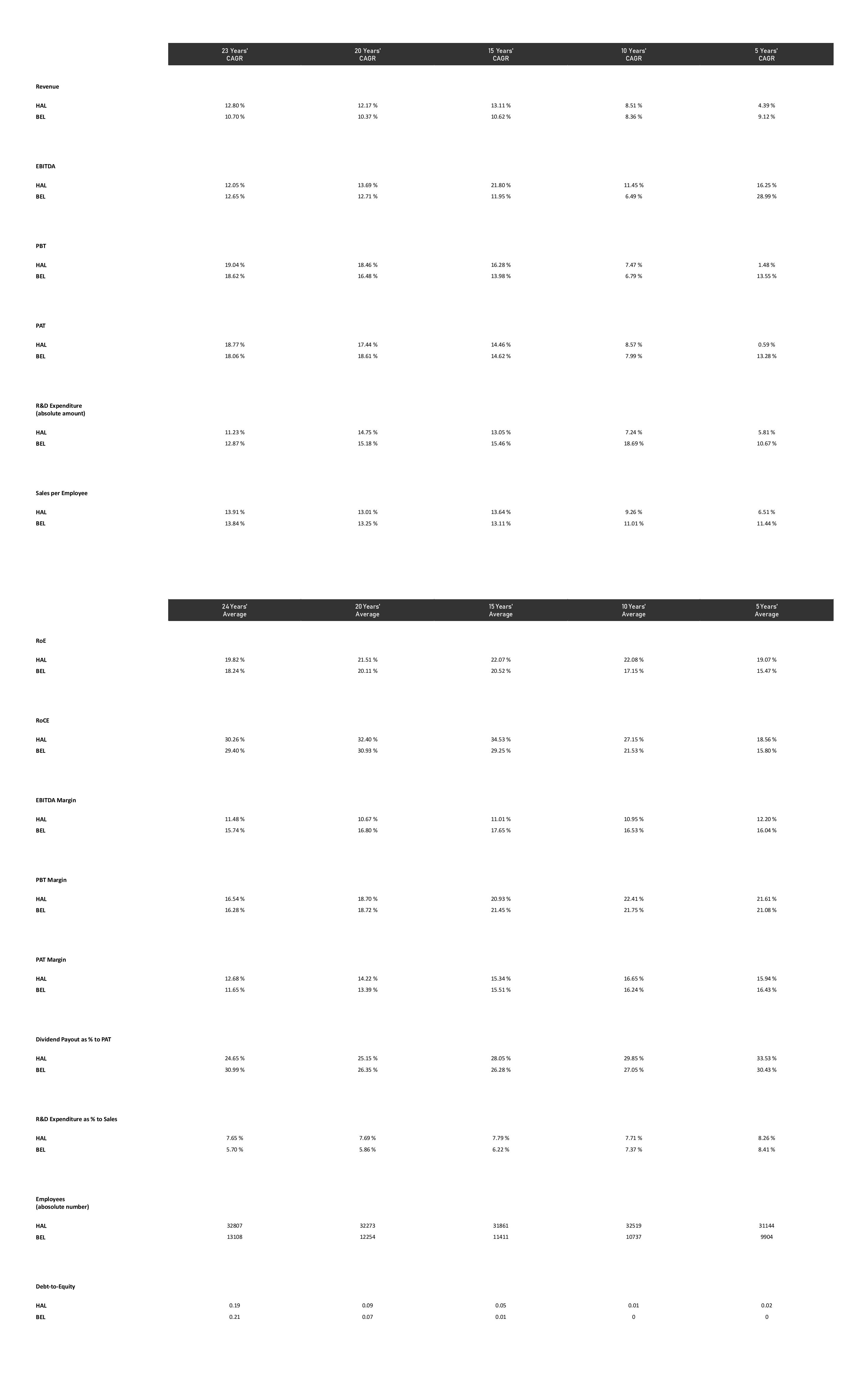

– Its only Bharat Electronics Ltd (BEL) , another defence PSU, which is as or more efficient than HAL and has the size of operations which are meaningful for comparison. Also, BEL is the only other entity which finds place amongst Top 100 defence companies of the world apart from HAL. So, what we did is we ran a detailed comparison of both, HAL & BEL on varied operational and business parameters across last 24 years to check whether BEL has outperformed HAL in any or many aspects. Refer following table where we have detailed 23, 20 ,15, 10 & 5 years’ CAGR of varied financial/operational parameters as also 24,20,15,10 & 5 years’ Average of varied paramters :

As can be seen from above,

– if we look at Revenue CAGR, BEL has outperformed HAL in last 5 years, however, on a long term basis, HAL has been an outperformer (this aspect will be more clearer in single-single 24 years’ YoY comparison detailed afterwards in next table).

– On absolute EBITDA CAGR front, again BEL & HAL are neck-to-neck on long term basis but in last 5 years BEL is a clear winner. However, here, if we look closely then, in two time-periods, viz., 15 Years CAGR & 10 Years’ CAGR, HAL outperformance has been significant, almost double that of BEL ; two things play part in this, first – its the actual period and its base which matters and second — the segment both the companies cater to, viz., defence, wherein once contract is booked its of larger value and has multi-year execution cycle and when major delivery periods of your order-book is there you wiill get operational efficiences and your EBITDA will get a boost and in other periods when the order is under execution it will be dull.

– Hence, these companies are best compared on a long-term basis and it is to be checked whether they are faltering on their traditional operational parameters like margins and all and here, both HAL and BEL are spot on as if we look at 24, 20, 15, 10 & 5 Years’ Average EBITDA margin of each, they are same with just a difference of 50-100 basis points here and there.

– Thus, what we here need to note is HAL’s business gives it an EBITDA margin of 11 % on a steady-state basis over long term whereas BEL is in a business which gives it an EBITDA margin of 16 % on a steady-state basis over long term — in some fiscal periods HAL & BEL’s margins will shoot up 200-500 basis points from steady-state and in some periods it will shoot down to a similar extent based on the delivery of the orders but on a steady-state if we will look in hindsight, it will not deviate from steady-state.

– If we look at PBT & PAT CAGRs the story is almost similar as explained above wherein BEL has outperformed HAL in last 5 years but both are neck-to-neck in Average PBT & PAT Margins achieved. Here, one intersting thing to note is the disappearance of margin difference of 500 basis points that is otherwise existent in EBITDA, with HAL PBT & PAT margins being similar to BEL in all periods whether you look at 24, 20, 15, 10 or 5 Years’ Average. This is because customer counts in its product pricing the benefits that HAL or BEL are going to derive from the cash advance they give at the time of placing the order.

– R&D Expenditure – if we look at ‘absolute amount spent’ CAGR then BEL seems to be outperforming HAL in almost all periods but, here again if we look at average of ‘R&D expenditure as % of Sales’ HAL seems to be more consistent with BEL only increasing its spend over last 5 years to come close to HAL but HAL consistently spending higher amount w.r.t. Revenues.

– HAL RoE and RoCE have consistently been superior to BEL whether you compare any period.

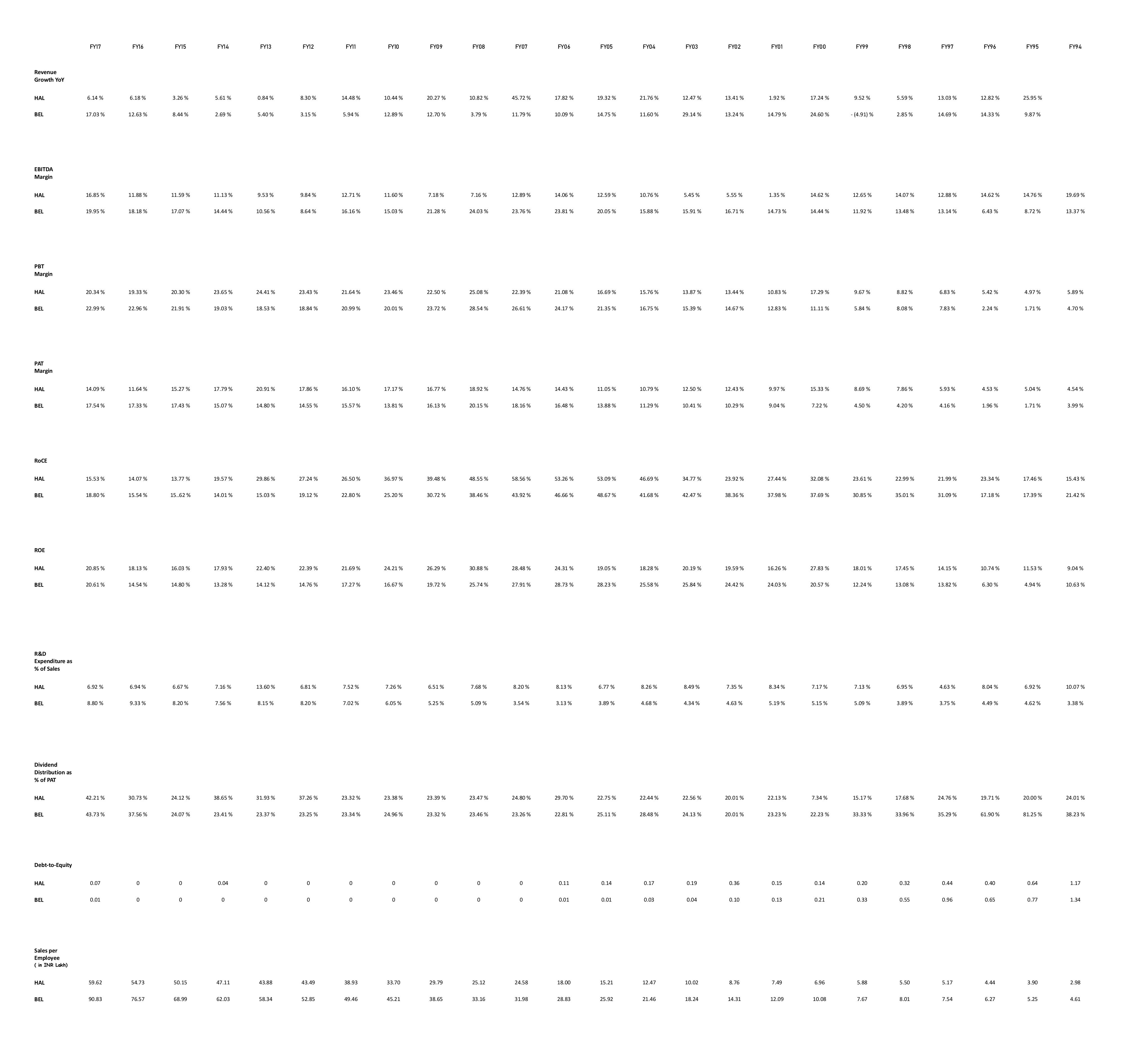

Now, after having looked at overall CAGRs and Averages of time periods combine, let’s have a look at each year’s actual numbers singularly of both the companies to get a better picture and correct ourselves if we are wrong somewhere. Refer table below :

As can be seen from above table,

– If we look at pure YoY Revenue growth achieved each year by respective companies then HAL has outperformed BEL in 13 out of past 23 years – its last 3 years where BEL has consistently outperformed HAL . Also, both the companies have registered a double digit YoY revenue growth in 14 fiscals out of 23 fiscals with HAL achieving single digit growth in 9 fiscals whereas BEL achieveing single digit growth in 8 fiscals and negative YoY growth in one fiscal.

– Both the companies have experienced high volatility in EBITDA margins, however, PBT & PAT margins of both the companies has been relatively more stable and has shown gradual improvement.

– HAL’s RoCE has been better than BEL in 13 years out of past 24 years – with BEL’s RoCE better in last 3 fiscals viz., FY15, FY16 & FY17.

– HAL’s RoE has been better than BEL in 17 years out of past 24 years – with HAL’s RoE consistently better in last 11 fiscals from FY07 to FY17.

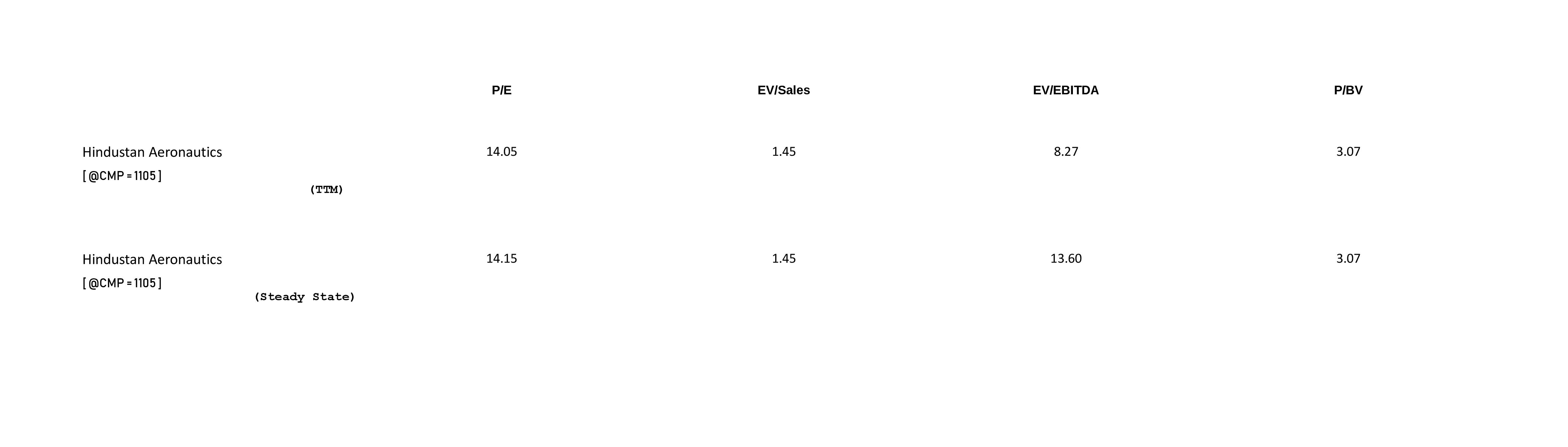

So, now, to conclude our discussion, let’s have a look at the valuations at which HAL is trading at present and then move on to discuss negative aspects. Refer following table :

– Here, we have arrived at valuation multiples by taking two base figures – one TTM (FY17) figures and second steady-state figures as the business is such that its better to value it on a steady-state basis.

– On steady-state basis EBITDA margin is assumed at 11 % whereas PAT is assumed at 14.50 %.

– Key thing to note here is that although current order-book and its delivery schedules ensure steady ~20,000 cr. revenue p.a. for next three fiscals but, benefits of expansions of capacities that are undertaken on LCA and Helicopter divisions to be commissioned in coming two fiscals as well as robust future order pipeline are not taken into consideration while assuming steady-state figures.

Lastly, now, since we have already arrived at HAL valuation both on TTM and steady-state basis, its better to see where HAL is pitched against Top 50 Defence & Aerospace companies of the world in terms of valuations. In addition to l-t-l global peers given in table before, below we have covered almost all the other prominent publicly traded Defence & Aerospace companies that find mention in world’s Top 50. Many companies’ scale of operations is smaller than HAL since HAL is amongst Top 40 in the world :

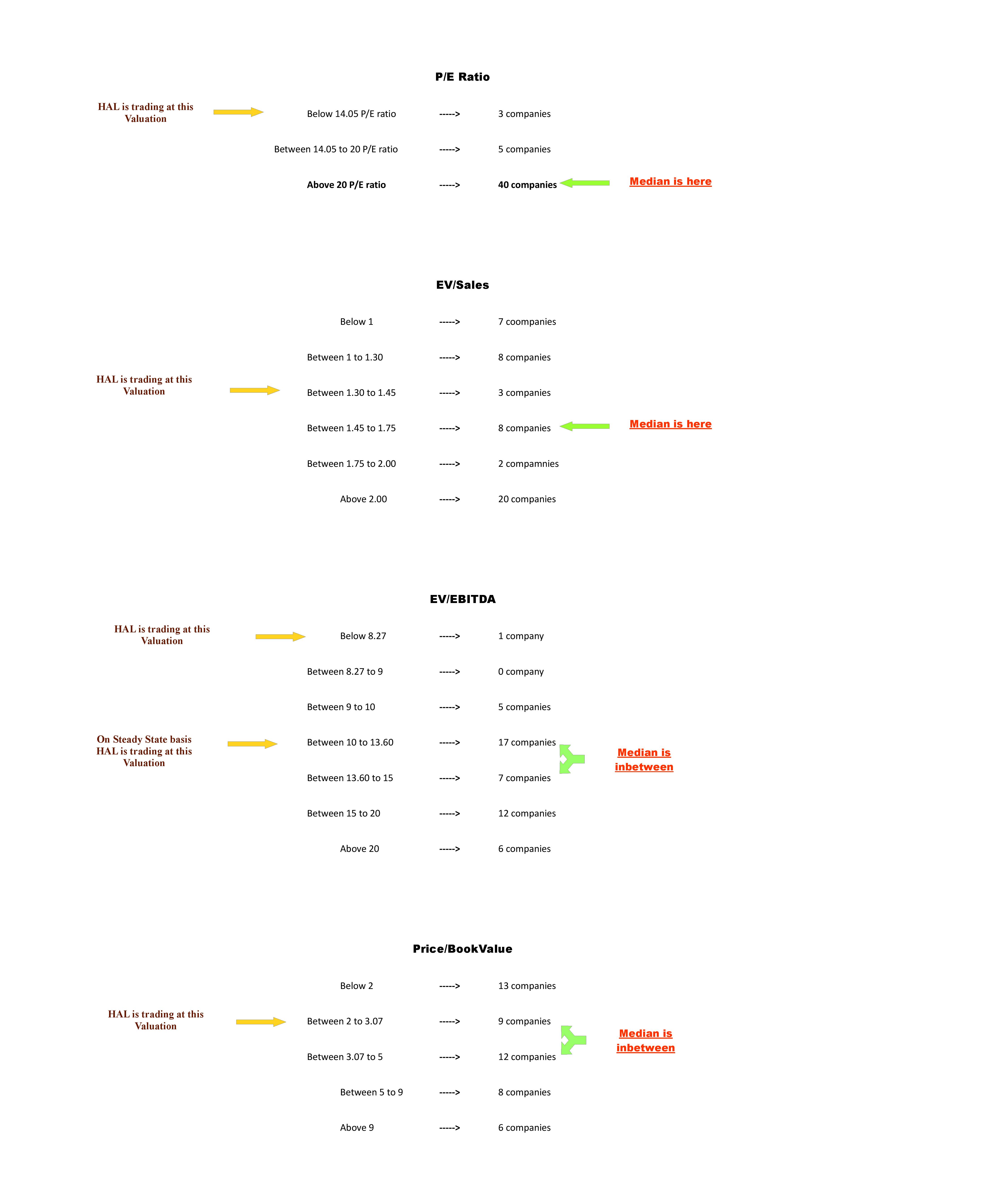

Having covered above (in two tables) the world’s Top 50, let’s summarise the valuation multiples and arrive at a median and see where HAL is placed at in the matrix. Here, we have chosen not to just arrive at plain averages of valuation multiples since averages can give wrong picture in such comparison as if only 5 out of the 50 companies are trading at extremely exuberant valuations, then averages will move up. Refer following data :