Was not mentioned in concall.

Key business insights

-

HCG employs multidisciplinary approach for the disease diagnosis and treatment wherein specialists from multiple disciplines come together to accurately evaluate the patient information, standardize the treatment approach and create efficiencies that will eventually lead to effective disease management.

-

Recently acquired next generation sequence in genomics which is a high-end sequencer and in the process of acquiring circulating tumor cell platform.

-

Brought in high-end technology including Linear Accelerators and Positron Emission Tomography to Tier II and Tier III cities and towns.

-

Triesta Sciences, a unit of HCG is the stateof-the-art, one-stop solution for cancer diagnostics, genomics (next-generation sequencing-based diagnostics) biomarker and translational research, laboratory services and clinical research services. Based out of Bangalore, Triesta Sciences is an integration of laboratory services, research and development and clinical research with a focus on innovation, quality and accuracy for better diagnosis and prognosis of cancer. Triesta reference laboratory is the leading CAP & NABL accredited high-end oncology diagnostic laboratory service provider in the country offering a comprehensive range of routine to highly specialized diagnostic tests for hospitals, medical institutions within India and overseas.

-

Through a pioneering industry initiative, we have brought healthcare training and medical education to the Metaverse by publishing 200+ hours of virtual reality content across multiple subspecialties.

-

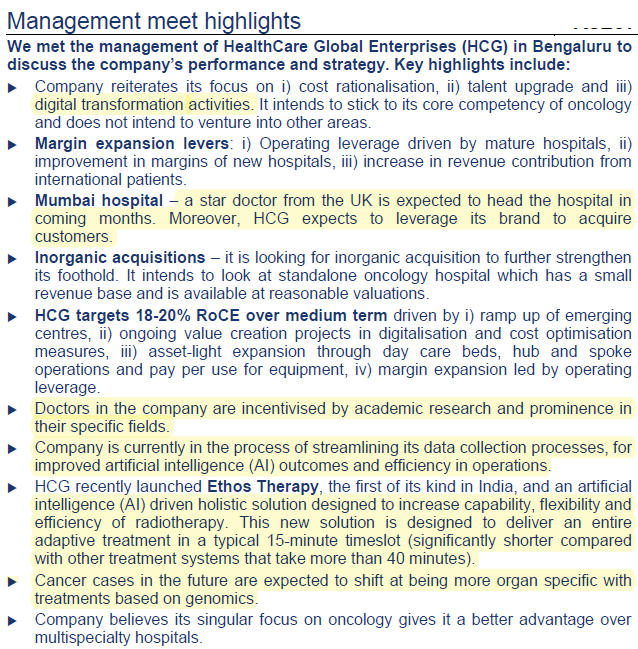

During the year under review, we have added over 40 oncologists, taking the total number of doctors in our team to over 450, which is the largest in the Oncology space in India

-

Post pandemic, we are seeing a rise in the number of patients covered by some form of insurance which augurs well for making cancer care more accessible and affordable for the community going forward

-

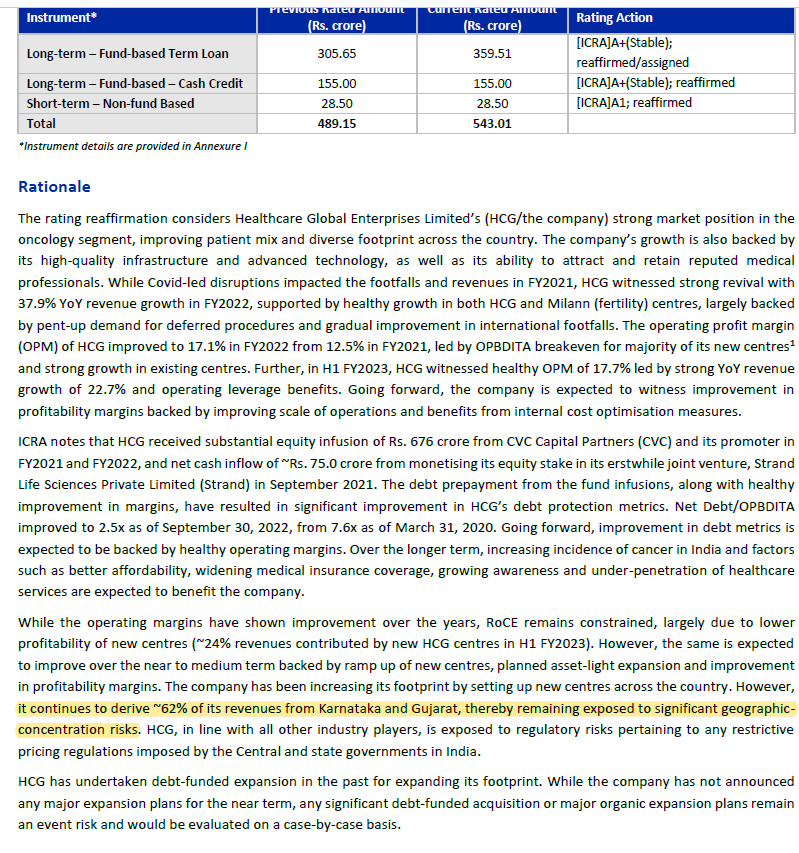

Coming to our financial performance for FY 22, our revenue from operations grew by 38% YoY to H 13,978 Mn, in comparison to H 10,134 Mn in FY21. With our focused efforts and local marketing activities, we have been able to grow our new centres revenues by 65% as compared to FY21. Revenues from existing centres grew by 31% on Y-o-Y basis. We reported robust year-on-year growth with an all-time record revenue across all four quarters of the financial year.

-

Our operating EBITDA grew from H 1,266 Mn in FY21 to H 2,380 Mn, registering a phenomenal

growth of 88% YoY. -

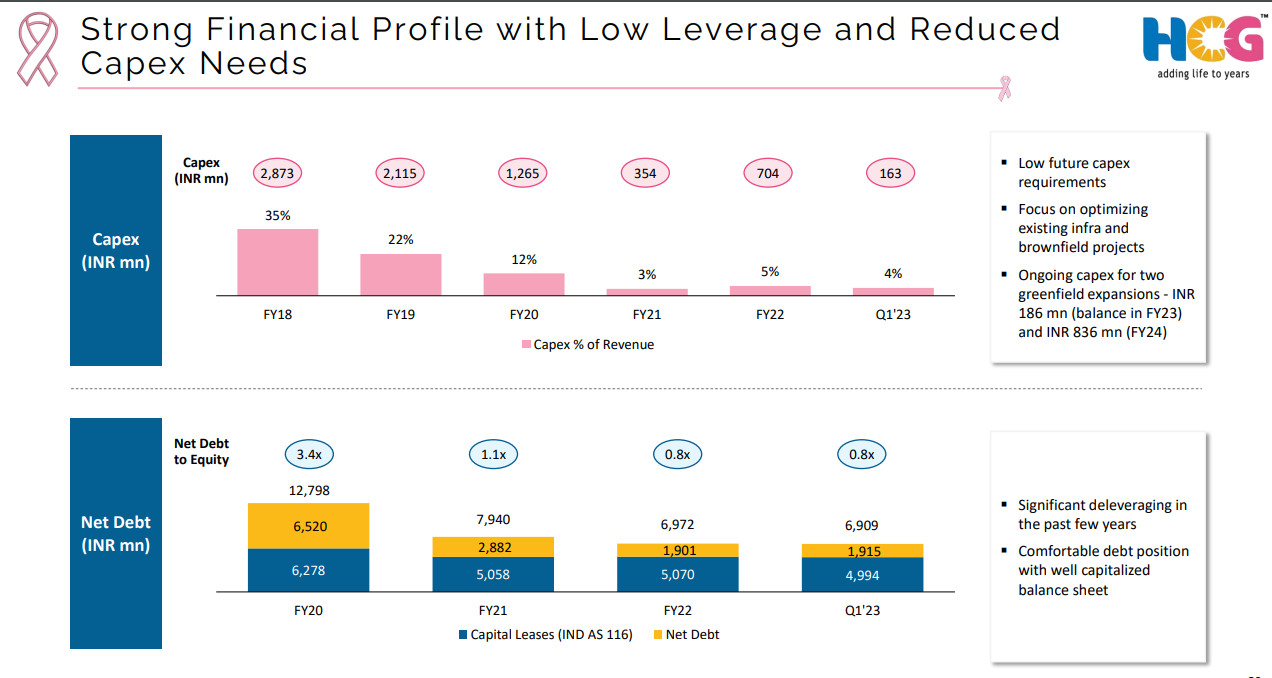

Profit of H 537 Mn, against a loss of H (1,935) Mn in the previous year. Alongside, we have also been working on strengthening our balance sheet and have been able to reduce our net debt from H 2,882 Mn as on March 31, 2021, to H 1,901 Mn as on March 31, 2022.

-

Largest player with Oncology focus in India with a cumulative operational bed capacity of 1,702 beds as on March 31, 2022. With 21 comprehensive cancer centres across 18 metro & non-metro cities

in India, we enjoy leadership position in 13 of those locations

19 Likes

2 Likes

Another listed entity is Rainbow Hospital in mother and childcare

1 Like

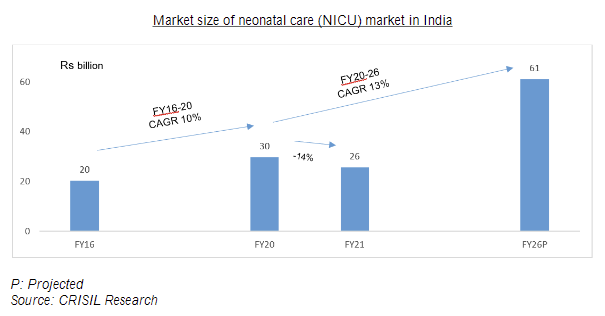

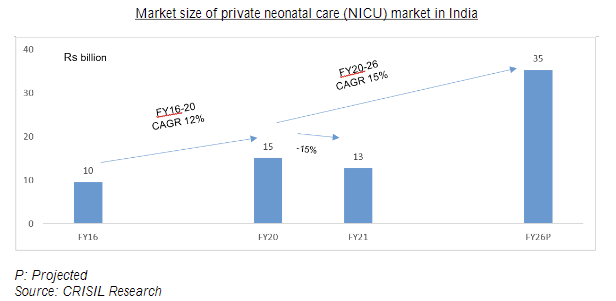

The “Ovum” acquisition might be good for HCG considering the CAGR in the Neonatal and Maternity market. Some of the data points I could find from Rainbow Hospital DRHP and investor ppts:

-

The Neonatal care (NICU) market is proposed to grow at a CAGR of 13% FY20-26.

-

Under the NICU market, the market share of Private hospitals is proposed to grow at a CAGR of 15%.

Thoughts on the proposed acquisition:

- It will be a good entry for HCG into Neonatal care, as it can be good revenue in the coming days for the company.

- Listed peers on NICU care are posting healthy margins, the same can be observed here also.

- In coming years we can see many such acquisitions happening in the hospital sector, which can improve the sector’s overall earning capacity.

Disc: Invested, biased.

8 Likes

does this also means HCG would become general hospital , not specialised cancer hospital? impact on valuation? margin? definitely revenue accretive

2 Likes

6 Likes

Hi @Rafi_Syed,

I recently started looking at HCG and the hospital industry in general to build a more investment oriented perspective towards these. Would it be possible for you to share this Equirus healthcare sector report with me so that I can gain a deeper insight into this sector?

Regards,

Rishabh

1 Like

I tried to search for the report you asked but instead I chanced upon a NITI aayog report that is very detailed and covers policies as well as healthcare sector opportunities. Attaching here for more people to benefit

https://www.niti.gov.in/sites/default/files/2021-03/InvestmentOpportunities_HealthcareSector_0.pdf

2 Likes

I believe the pre-tax cost of debt for HCG seems to be higher than the cost of equity. Could someone explain how does that make sense? Shouldn’t it be lower than the cost of equity?

@Deven I recall you closely track/invested in HCG. Could you please share your thoughts pust Q2!result. Thanks.

@Abhishek_Kumar_9 am not tracking it that closely q on q. The thesis am wroking is; for my business we are working with most hospitals. As such I may not have invested in any hospital except Apollo. As apollo has cg issues, I had not invested in any even we are working with them.

For HCG when I invested it was available sub 3k mkt cap. Main thesis is to trust in PE fund as HCG is in exclusive cancer care, and has opportunity to do much better than they are doing under Dr leadership. With cvc PE am batting on turnaround. It’s long term bat for me. Results are in line of expectation.

3 Likes

Prabhudas Lilladher analysis of Q2FY23 result

HCG’s consolidated post IND AS EBITDA grew healthy 21% YoY (4% QoQ) to Rs 747mn, in line with our estimates (Rs754mn). Adjusted for one time consulting (Rs50mn) and ESOP related charges (Rs12.9mn); was up by 28% YoY. Existing centers reported strong profitability with EBITDA growth of 30% YoY (4% QoQ) to Rs777mn, while new centers reported EBITDA at Rs 95mn (Rs 195mn in H1FY23). Margins improved by 10bps QoQ (25bps YoY) to 17.8% on cost rationalization initiatives. Margins adjusted for one off were at 19.3%.

.

HCG’s asset light approach with focus on partnering has made its business model – capital efficient and scalable. The company operates most of its Comprehensive Cancer Centre (CCC) on lease/rental basis with HCG investing only in equipment’s. Out of 25 HCG’s CCC, only four are on owned land. HCG is in a consolidation mode and given reducing capex intensity, we expect profitability to improve further.

7 Likes

Q2 Con Call highlights- 11 Nov 2022

- Introduced Ethos as a new technology COE in Banglore.

- One of the few centres in the world using this AI-based technology. It continues to probe and treat infected tumours using AI.

- Fellowship programme is top-rated, and students are willing to relocate to Tier 2/3 cities to learn.

- HCG and Milann’s revenue contribution is 96:4

- Mature centre revenue grew 19%, and emerging centres revenue grew by 26% YOY

- ARPOB- mature centre- 39684, emerging centres- 30,145. QOQ de growth in the emerging centre is due to a higher proportion of institutional business, which will come down in the future.

- Mature centre ROCE 24.8% and emerging centre ROCE 4%

- 5 Cr on consultancy- improve productivity and digital transformation. Both these initiatives shall help 100-150 EBITDA improvements next year. Have similar expenses in the H2 and this will disappear from next year.

- Hired Big Four firms to look into consulting on operational efficiencies, market dynamics, pricing, and labour productivity.

- When HCG open a new hospital, the first objective is to utilise different aspects of hostility. Hence we take the institutional business. This shall normalise going forward.

- Playbook for opening hospital

- Open hospital

- Drive football

- Boost occupancy (by the institutional business, for example)

- Higher utilisation across different segments

- How much time it takes to generate a margin of 15%?

Kolkata centre starred last year. Breakeven early next year, and then it will move to a margin upwards of 15% - Revenue split- Consultation and diagnostic- 20%, medical oncology(e,g Chemo)- 35%, radiation oncology 20%, surgical 25%.

- 13 centres are in non-metros- 11 out of them have #1 position in the market- lower operating costs, and serve the institutional business to drive up the volume. Hence our EBITDA are same for metros and non-metros. Unique business model. ROCE 15-24%.

- Ahmedabad, Bangalore- mature centres- 75,000 ARPOB. Baroda, Mumbai, Kolkata, around 50,000. Once they mature, their ARPOB will inch upwards to other mature centres.

- Six/Seven quarters ago, emerging centres were operating at -8% operating margin; today, they are operating at 10% operating margin.

- In the next 18/24 months, emerging centres PAT will be similar to mature centres (aspiration). This can result in a 300-400 point increase in profitability.

- For an 80-bed hospital- the cost per bed- metro is 65-70 lakhs, non-metro 55 - 60 lakhs

- Current tax rate is 35% and moving to 25%, possibly from next year.

- Focus in on Cancer super speciality. Some existing multi-speciality centres and moving them to super speciality.

- CVS PE fund owns 58%. Invested a couple of years back. No talk of exit yet

- On Maintenance contract- It seems asset-light model at the start. When the centre starts making money, partners like to do it themselves (e.g Apollo), so they are not looking into this. There is good opportunities in setting up dedicated Oncology centres. May be capital intensive at start but sustainable.

- ARPOB is a function of high-end work, complex work and a speciality mix.

Note: Invested. Special thanks and deep appreciation for @Worldlywiseinvestors for explaining hospital/HCG in details in his various videos.

19 Likes

, Rainbow (Single Specialty Hospitals)")

Congrts Harsh. Good indepth analysis.

I also liked your video on cement sector.

Gone through HCG video of this series and will go for last one as I get time.

Just to add or correct; PET CT will cost around Rs. 16,000 to 18,000 per scan, if not mistaken you mention total cost of 3 scans around 18K.

6 Likes

16th Dec22 --Healthcare Global Interview CNBC :

–Focusing on the margins, our margin now is in the range of 18/19% , mature centers are in the mid 20s and we expect the new centers to also ramp up to that level --so looking at margins in the region of low 20s as we move to FY24. Our goal is low 20s.

–Reasons we are achieving this is due to operational efficiencies in the system apart from the ramp up in new centers

–ROCE --In mature centers its at 20/22% & our COE has 25% ROCE. The new centers are ramping up particularly in Mumbai and Kolkata . Once these ramp up, we expect ROCE to be in mid-teens & going forward to 20%.

–International patients–contribute 5 to 6% overall contribution, its only restricted to big cities , the Bangalore center has 18% revenue contribution from international & its ramping up well, Mumbai, Kolkata & Ahmedabad are also ramping up. The margins in international is 10 to 12% higher than domestic.

–Looking at standalone oncology units for acquisitions --for us cash flow is very imp. we are generating 15/20Cr cash flow every month . So it puts in a strong position to have some strategy for growth . Its going to happen through M&A & apart from that we have some areas in different states and 3rd is we are investing in tech in existing centers. Robotics / AI / Genomics / circulating tumor cells --investing in present centers will give us good growth.

13 Likes

Recently started studying this business.

Some very layman questions based on quick scan of financials.

- There has been constant equity dilution historically. The size had doubled in just 7 years. Has management ever commented on this and have they actually walked the talk on this. Diluting existing shareholder wealth is never an investor friendly action unless they got it through high valuation QIPs which is not the case here (warrants).

- The debt has always been a bit high ~ 1.02 times. It has started reducing recently but is there any ballpark figure mgmt has guided considering no medium term capex and debt ~ 5xCFO.

- The sector/business seems to be capex cyclical in nature if one looks at net profit. Seem like peers like Fortis also display this tendency (although it is much more cyclical). Since we are not looking at much capex in medium term, is it fair to assume, the next 4-5 year cycle will be upturn one only ?

Would appreciate if anyone tracking this business can answer. Thanks.

@Rafi_Syed @KC1986 @Worldlywiseinvestors @arjunbadola

3 Likes