Q3 Con call highlights

-

Only 1% of the Indian population is covered for screening for different cancers. 2/3rd of cancer patients get diagnosed late at advanced stages of life.

-

Of the 480 comprehensive cancer centres in the country, around 40% are concentrated in the metro and state capital. HCG has 21 comprehensive cancer centre

-

HCG can provide the latest technology and treatments available across work and outcome compared to the leading institutions across the globe at a fraction of the cost, acknowledged by Harvard Business Case Study.

-

highest ever revenue in digital and international business

-

revenue split HCG: Milan- 96:04

-

Revenue from the emerging centre - 29% YOY growth. They are inching towards maturity

-

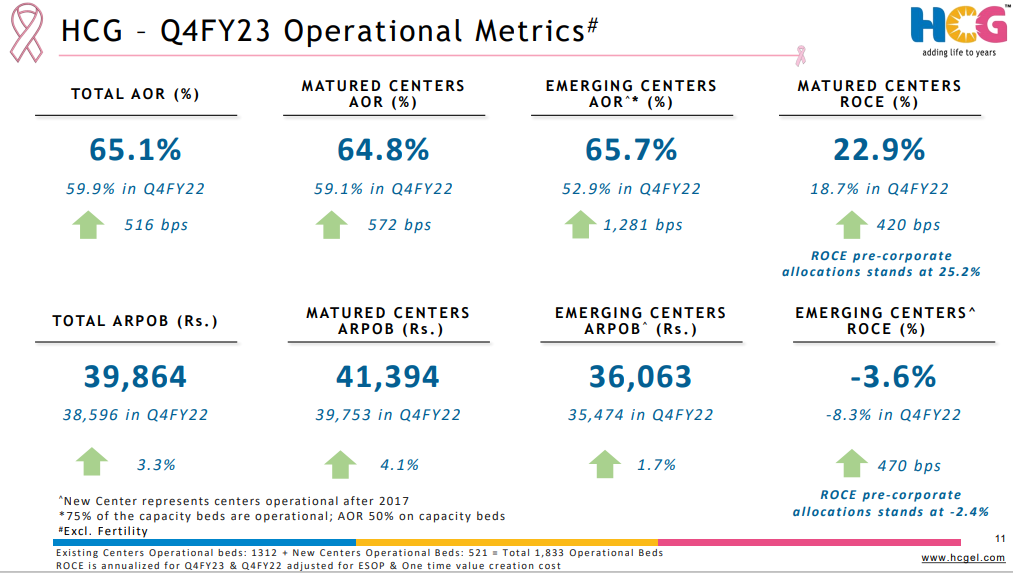

AOR company wise- 65 7%. Emerging centre- 71.9 and matured 63.2% (Is this correct)

-

ARPOB Rs 7k. emerging 30k and mature 40. emerging centres - Aiming for greater volume first and then target to improve the quality of the business.

-

Playbook for an emerging centre- Fill up the hospital first, optimize the payor mix- this will drive up the realization.

-

ROCE- matured centre 19.7 and emerging centre -5.3 for nine months.

-

Net debt 212cr

-

Ahmedabad capex 85 cr. Operation in Q1Fy25 (June 20 4). Banglore COE - 25cr Capex and operational by Q4-Fy24(March 2024)

-

Disproportionately investing in hiring clinical talent and building brands for emerging centres to drive scale/vol me. This is reflected in revenue growth for them. As utilization improves for the emerging centre, it, EBITA will improve.

-

Current quarter is the last quarter for consultancy charges (I guess it is 5 cr per quarter)

-

COE Banglore- Post IndAS EBITADA is 27-28%.

-

Lions’ share of mature beds will move towards 25% + EBITDA level within the next 2 years.

-

EBITADA without one-time charges is 19^% currently; this includes corporate c st. If you take out corporate cost, HCG is already in the low 0%. so they are confident of reaching 25% within the next two years. This means there will be high chance that HCG will have a 200-300 basis point improvement in EBITDA in the next 2 years (Thanks to Aditya Khemeca for extracting this most important information)

-

Invested 18 cr in solar ass ts and invested in high-end equipment and robotic surgery. As a result, despite profit, net debts have not been reduced.

-

Capex for 9 months- 96 cr

-

Da Vinci Robots- Pay-per-use model (first in kin ). This will help us drive this in tier 2/3 to ns. Robots is previse in treating patients, causing quicker recovery with fewer complications with fewer cosmetic scars.

-

Around 10-15 doctors (across HCG) are certified to use robots

-

Working with Da Vinci to create a new platform to improve the outcome even better.

-

70% occupancy for operating beds. If you take the installed bed, it is 6%. So the bed is not a constraint for growth. Also, chemo is daycare activity; radiation does not require ed. Only surgical patients who need overnight b ds. So HCG does not use beds as a constraint for growth. A bed is not the right parameter to measure growth for HCG as it is more and more outpatients.

-

Mumbai centre- Better payor mix and corporate-driven growth. So it is a better quality business giving better APRPOB, although it is showing less growth

-

Payor mix- 66-70% cash + insurance. Remaining corporate plus govt

-

Corporate client renewal is every two years. This will come for renewal next year, but it is centre to centre.

-

When occupancy reaches 75% levels, we start thinking about increasing the capacity. Only surgical speciality that requires impatient b s. HCG is converting a lot of impatient beds to daycare beds. On daycare beds, capacities can be increased by increasing the number of shifts. Hence bed is not a concern as one would think in a multi-speciality environment.

-

Jaipur is high occupancy and high capacity hospital even though it is part of an emerging centre

-

New Capex that will happen next year will be through internal accrual without additional debts.

-

Want to operationalize 203 beds over the next 18 months

-

Historically, presence outside the metro was larger. It was a mass market, low price, higher volume with govt scheme. Many emerging centres are in bigger cities (Mumbai/Kolkata), which will have better ARPOB. As emerging centre revenue goes up, APROB will start inching upwards

-

International business - already 1.5 to 1.6x of pre-covid. Q3 was the highest ever around 5% of revenue from international