CVC is the promoter of the company , so they bought the stake from the co-promoter (Dr. Ajai) which is a good thing in my opinion.

1 Like

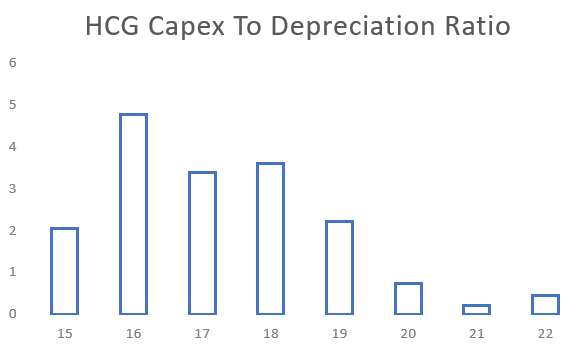

Capex to Depreciation ratio chart:

Depreciation can be used as a proxy for maintenance capex. Hence, the ratio of capex to depreciation indicates the proportion of growth capex to maintenance capex. A high ratio suggests that a higher proportion of the total capex is done for increasing supply

Disc- tracking position

7 Likes

This is expected to significantly reduce the turnaround time (for screening), standardise reporting quality and increase efficiency multi-fold. Further, this solution will enable pathologists to collaborate seamlessly across geographies thereby ensuring that every HCG centre will now get access to expertise across the network within seconds!

5 Likes

Reading through this company, did anyone have a view on Related Party Transactions that AR 2021 lists?

See, if the related party transaction is within limit of 10% of the total annualised consolidated profit of the company then it is not an issue. Approval of shareholders through special resolution is required if the related party transaction during a financial year exceeds this limit.

In above case, company’s turnover is 10,304 mn. Total transaction reported to related party is approx 208 mn which is less than that limit, So there is no issue as such. ![]()

1 Like

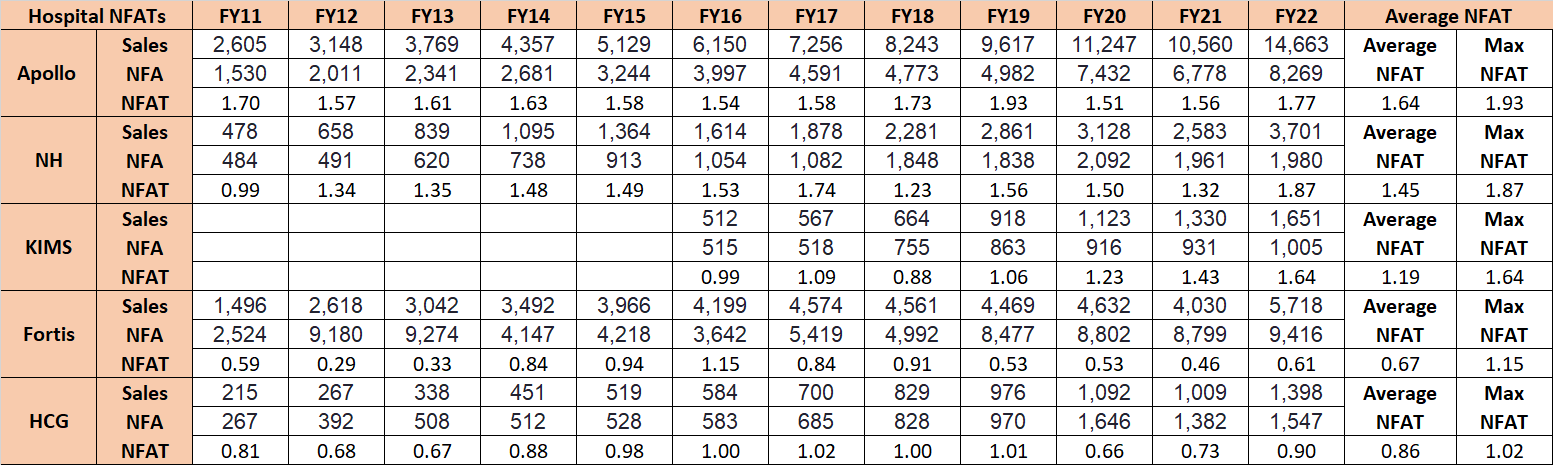

I was doing a comparison of net fixed asset turnover for listed hospital chains and this is what I found

Apollo and NH have superior NFATs in excess of 1.5x whereas HCG lags behind along with Fortis at below 0.9x. Since HCG is specialized on cancer care, it may have lower AORs (occupancy rates) than multispecialty hospitals but I guess with increased specialization their ARPOB should be superior, thus driving NFAT up?

Can any experts (Tagging @Worldlywiseinvestors) comment on future NFAT outlook for a specialty hospital like HCG? Is it likely to remain at 1x or below levels or is there scope to expand? Any insights on asset turns of specialty hospitals versus multispecialty hospitals? Asset turns is a key lever towards improving ROCE as HCG ROCE is still quite low.

6 Likes

I think the NFA for an oncology speciality hospital will be skewed because of cost of establishing radiation oncology facility which requires strict adherence to AERB rules.

Hence, comparison with multi speciality hospital can be misplaced.

1 Like

Dear all,

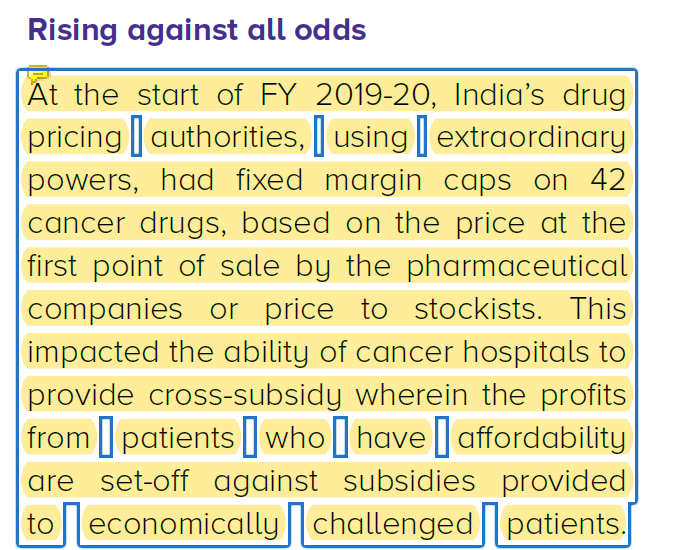

I am trying to understand how capping of cancer drug prices by regulator in 2019 affected hospitals. Found this note in FY 20 annual letter but I am unable to understand in what way price capping affected HCG.

Any guidance will help.

Thank you,

Mahesh

1 Like

A few things to consider while comparing fixed asset intensity of HCG vs others:

- Oncology focused hospitals are more capital intensive than multi specialty hospitals as the investment required in PET CT and linear accelerator itself can be to the tune of 20 cr. So, even if the land and structure is on lease model, the investment in equipment is far higher. The good thing is that higher investment limits the competition from small clinics which makes onco hospitals a viable business proposition in tier 2 cities that most multi specialty hospital chains have found a tough nut to crack.

- For HCG, the overall FA turnover is 0.9x but if you split that between turns of mature and new hospitals, the picture is not as bad. Mature hospitals have FA turns of 1.3-1.4x, while the new ones are still operating at 0.3-0.5x. This is increasing for both new and old hospitals and should drive ROCE increase going forward.

- Occupancy for oncology hospitals is not always the right metric to track. Chemo and radiation therapies contribute to a meaningful proportion of revenue and these are out-patient therapies. That implies the bed occupancy is low but the linear accelerator might be fully or optimally occupied.

- For the same reason, ARPOB might look artificially inflated for onco hospitals as the revenue captures OP treatment revenue without the bed being occupied. Numerator is higher with no corresponding increase in denominator.

19 Likes

Patho and pharma are important sources of profit for most hospitals. That’s why hospitals won’t allow outside medicine, you need to purchase from their own pharmacy while you were admitted.

The price cap was very severe for hospitals & pharmacies (which seems excellent for patients). For example decade back one tab named Femera from Novartis was costing Rs. 200/tablet which is now Rs. 42/tablet. Earlier some cancer patients may have required 1-5 lakhs of medicine every 6 months. They do PET CT, Dr prescribes medicine and many patients need to continue for a lifetime or till they cure completely.

Numbers are from memory, hence take them approximately.

Does anyone have revenue/profit share of patho, radio and pharmacy in the overall P&L of hospitals? if so please share.

5 Likes

These are regular ESOPs grant and not open market purchase

You may check details here(will delete this as doesn’t add value to thread)

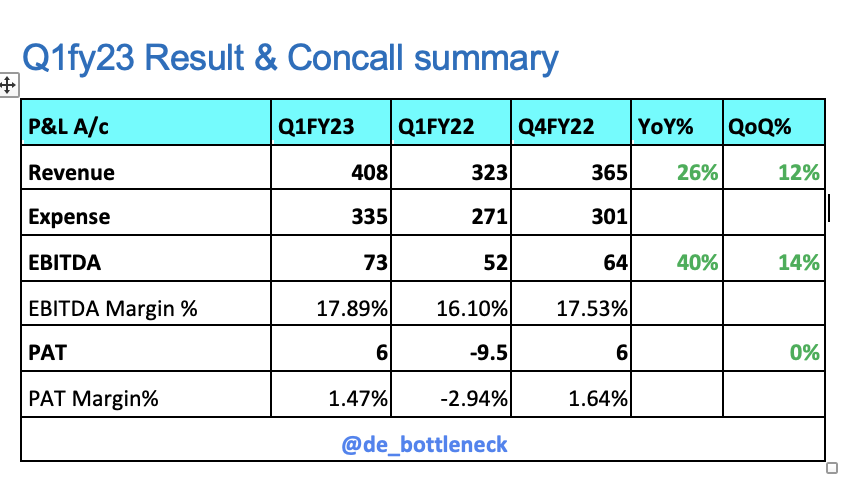

• Revenues for Q1 ‘23 stood at 408 crores as compared to 323 crores in Q1 FY22, a growth of 26%. Revenue split between HCG and Milann stood at 96% and 4% respectively for Q1 FY23.

• Revenues from oncology business grew by 35% on YOY basis to 343 crores and revenue from non-oncology business stood at 58 crores.

• Company AOR stood at 64.6% and AOR for existing versus new centres stood at 64% and 66.1% respectively. Higher Occupancy for new centres is due to only 70% of beds were operational in new centres.

• ARPOB on company level stood at Rs. 38,454 and our ARPOB from existing network stood at Rs. 40,606 and for new centres it stood at Rs.32,968.

• Working on 4 levers for growth - digitization, Cost optimization, growth in medical value travel business, inorganic acquisition.

• Jaipur grew by 263%, revenue from Ranchi grew by 112% and Mumbai grew by 53%. Bangalore centre of excellence grew by 37%. Milann business is also doing well. Revenues have increased by 43% in Q1 FY23 on YOY basis, our new registrations grew by 139%.New centers revenue growth in Milann stood at 70%.

• Management are confident of improving EBITDA margin by 100 to 200 bps over the next 12 to 18 months and profit-making company on a consistent basis from now onwards.

• International business is about 4%. But you would be happy to know that at our center of excellence in Bangalore it’s at 15% of top line and I think we’re just getting started.

• Net debt position excluding capital leases as on 30th June, 2022 stood at 191.5 crores compared to 293.7 crores on 30th June ‘21

• Total plan CAPEX for Ahmedabad is Rs. 85 crores expected date of operations being Q1 FY25 and for Bangalore COE is Rs. 25 crores expected date of operation being Q4 FY24.

• We have two of Mumbai centers as well as Kolkata centers which are greenfield centers for us. We are in process of ramping them up.

• One is an extension center in Whitefield for our center of excellence which is a greenfield project. Our Ahmedabad center of excellence has peaked out in terms of utilization. We are relocating in a newer site with an expanded capacity.

• Capacity of about 1,974 beds right now. We have opersonalised 1,737 beds.

• Maharashtra has only 10% growth because of covid income in base year.

• Tax rate is 34.5%.

• Going forward in the greenfield if we do will be less beds and more outpatient facility, day-care because the whole cancer care is moving towards that.

• Occupancy may increase up to 75%-80%. But more than occupancy the footfall will increase, and the radiation load will increase, the outpatient chemotherapy load will increase, our cost will increase.

• Successful implemented 3.3 MW solar plant at Bangalore facility.

10 Likes

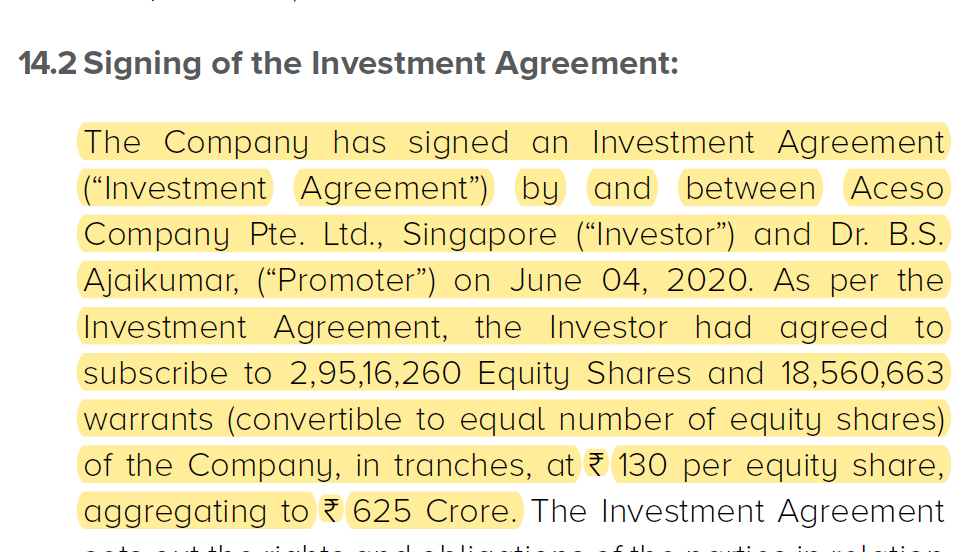

Hi all,

I have a naive question.

In 2020, Aceso (CVC) bought stake in HCG. They invested 625 crore as per FY 20 AR. From September 2020, the shareholding pattern shows that Aceso owns ~50% stake.

Does it mean that at the time of the deal, entire HCG business could have been valued at 1250 crore?

Tagging seniors here @sujay85 @Deven @Worldlywiseinvestors.

Thank you in advance,

Mahesh

2 Likes

That’s cortect. When they first bought one stock was somewhere between Rs 130. Which implies market cap would have been somewhere between 1600-1700 crores

6 Likes

Thanks @Worldlywiseinvestors.

CVC has already more than doubled their money in two years!

Not only that, CVC got the deal done at a valuation of 1250 crore (all the business) when it was trading at 1600 crores, discount of ~25%.

3 Likes

More on CVC:

CVC has about 9-10 investments in the healthcare field globally. One may find the name in the PPT of HCG (Slide 30).

Read the below article on how CVC transform businesses…

3 Likes

Not necessarily applicable to HCG. But many hospitals in their concalls have been talking about focusing on certain high margin segments.

6 Likes

as a small taxpayer I think regulation just for the sake of regulation is a bad notion (I’m not against regulation); a more prudent way should be that public healthcare infrastructure should be made more competitive through investments so that the citizen has a choice to choose between public or private; that’s how at least I perceive market economics.

4 Likes

HCG is relocating and expanding at Ahmedabad, also it is starting green field projects at Mumbai and Kolkata. Is there any information available that how they are going to fund these CAPEX?

1 Like