i think they are planning to become Asian paints in oncology by using technology and data. if they execute it to the full extent we can see tremendous growth.

Disc- tracking

i think they are planning to become Asian paints in oncology by using technology and data. if they execute it to the full extent we can see tremendous growth.

Disc- tracking

Shareholding Pattern

| Shareholder Category | % |

|---|---|

| Promoters | 71.02 |

| Institutions | 14.1 |

| Individual Share Holders with share capital in excess of 2 Lacs | 5.68 |

| Individual Share Holders with share capital up to 2 Lacs | 4.29 |

| Two Individual Investors | 2.41 |

| Others | 2.5 |

|  |

Promoter holding is increased by almost 3% at the end of dec quarter. Is this a good sign??

The increase in promoter holding is due to exercise of warrants due in Q3. So no real change in promoter holding as such.

Management interview.

looking for different point of view on q3fy22 results (positive or negative); personally, I feel numbers are good.

Hello Vivek,

Results are good; however, QT results can’t be over-emphasised either way. As far as direction is considered it’s on the right track as per my pov.

I have business in the healthcare segment hence have an idea of the functionality of hospitals. As such I may not have invested any hospital stock other than Apollo. Reasons for not investing in hospitals stock are like capital intensive/high cash business and Doctors are good as a profession but poor business people. Most hospitals in India is run or highly influenced by Doctor. Apollo has CG concerns hence I have no hospital stock in my PF 6 months ago.

I invested in HCG a couple of qtr back. Just to indicate my avg purchase price (256) is still higher than CMP (241); hence take my inclination towards HCG with a pinch of salt.

Due to my business engagement, I have a chance to visit HCG Bangalore and surely have an idea of HCG Ahmedabad (being located in A’bad). If you see HCG B – it’s like lots of low rise buildings. They built a top bridge to go from one unit to other. Similar HCG science city, Ahmedabad has small 3-4 buildings; there was some commercial unit in between the main canter and lab.

Mean to say they failed to visualise demand and failed to build sustainable infra. Difficult to get Accreditation like JCI – Joint commission international etc. Dr Ajaykumar is good professionally but like most Dr he is a poor businessman. When PE took over they first stopped further capex and decided to concentrate current business matrix. Hence I decided to invest as I find valuation attractive. Current market cap of 3300 cr; I find it cheap if I get the whole business of 27-30 units across India. Another reason is that cancer growth is higher (Unfortunately) and concentration in oncology will help in the acquisition of good Dr & Technology.

On the soft side; in Q2 earning call, Aditya Khemka asked most of the questions. In Q3 call there seems good interest from institutional.

Disc: Invested as indicated in the post.

Thanks for your Point of view; it’s really helpful I’m new to this sector and trying to understand the economics of this sector.

Hospital sector review and initiating coverage report on HCG by Prabhudas Lilladher

Thanks, @sujay85 for sending Prabhudas L report. Indeed it’s interesting to read, nothing to complain about.

Am just putting my thought process on brokerage reports or stock ideas by investor friends etc. for any company or sector.

As per PL report, the triggers are like

All these triggers seem old. Had that been useful in past? Let’s see…

Listing history of hospitals are not new, if that won’t be a useful trigger in past, so won’t be useful for the future – can assume safely.

Let’s see past performance on hospital stock price:

5 yrs performance as per screener in CAGR

Apollo 31%

Fortis 8%

NH 15%

Aster DM 2% (3 yrs)

HCG 0%

Hence aggregate return is lower than the index. Hence we can safely conclude that the old narrative proved false for a stock price.

Now let’s come to company-specific triggers.

Am able to give examples of only HCG (as I have not studied others).

The main trigger for HCG is an entry of CVC – PE player. They decided to stop the new Capex for time being and concentrate on existing centres.

Is this trigger working?

Seems yes,

How?

They stopped the development of a new hospital in NCR even they need to incur losses. They diverse some stake of non-core business as well.

2nd, In Ahmedabad they are building a new hospital from the ground as the existing centre is developed haphazardly (Ref my earlier post in the same thread). Seems CVC is walking the talk.

Due to this trigger, I took some allocation.

Now on stock pricing, is this story working?

Seems yes, HCG is down 13% from 52 weeks High which is resilient, much lower dropdown vs other small caps.

Just sharing my thought process, open to feedback. Thanks.

Disc: Invested in HCG and views are biased. Not Sebi registered and not a recommendation.

KYC में आज हम Healthcare Global के Management संग करेंगे चर्चा, कैसा है Company का कारोबार, Q4 में कैसा प्रदर्शन, Business Growth, Revenue और Income Growth पर Company के Chairman और CEO… Dr B S Ajaikumar संग विस्तार से चर्चा, देखें वीडियो

Q4 FY22 Concall Highlights

Existing centers EBITDA margin at 22%.

Existing centers recorded the healthy revenue growth of 15.6% in quarter 4 of FY22 on a Y-o-Y basis.

Karnataka region, Center of Excellence, performance in Q4 with revenue growth of 39.6% Y-o-Y and 25.8% operating EBITDA margin.

Bangalore Center of Excellence will be around 25-26% ROCE.

Ahmedabad will be around 30% ROCE.

Revenue expected to grow at 12% and it will all be EBITDA margin accretive going forward.

I also just recently checking hcg and there have a good business model though the p/e is too high at 76 and can u help me to understand that . Also balance sheet pf hcg is strong or at par with their peers like narayana and kims but the stock price isn’t moving for now whereas narayana , kims stock price is too high . Also i wanted to ask why market doesn’t seeing the opportunities in hcg.

PE seems to be high because the earnings of the company were negative last year. From this year the company has started to generate positive PAT.

However, better metric to look at is EV/EBITDA. By which we come to know that the valuations of HCG are cheap when compared to its peers.

Capex is all done waiting to See its fruits in coming Q’s

Hi all,

A few thoughts on the Capex annoucements made recently.

Radiant Hospital capex: Amount spent as per discloure is 16 crore which is 30% of PAT of FY 21-22. It can be considered Greenfield capex as HCG was not present in the city of Sambalpur (Odisha) till now. Although it has a cancer center in Cuttack in the state of Odisha. So there may be a brand recall.

Apart from this, discloure about expense details pertaining to other initiatives is not available. It would be interesting to see how much is the planned expenditure.

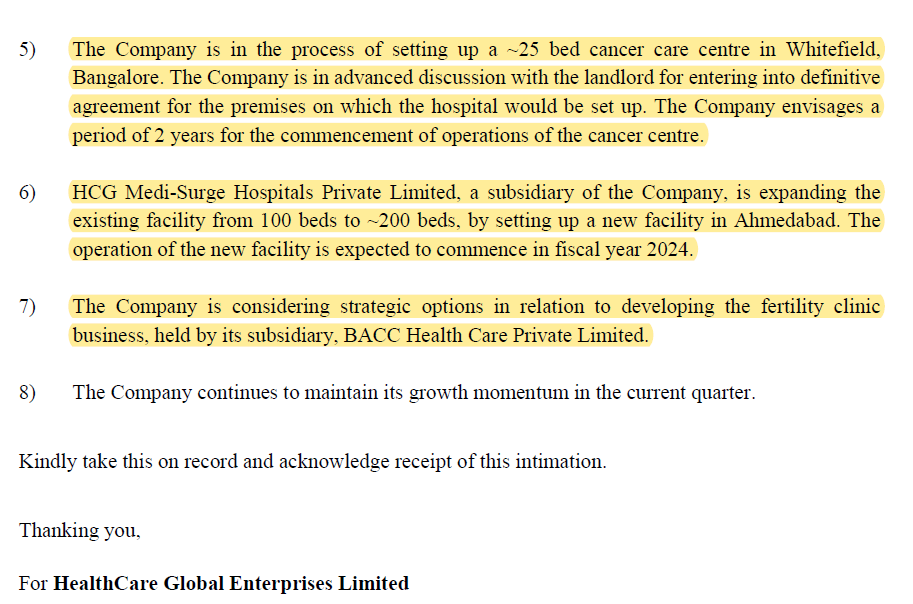

Initiatives include a stake acquisition in a cancer hospital in Nagpur (brownfield), new facility in Bangalore (greenfield, same city), facility expansion in Ahmedabad (probably greenfield, same city although I am not sure), a fertility clinic (no details about location disclosed).

They’ve launched operations and digital transformation programs with two consulting firms. Being from maangement consulting background, I know that consulting firms cost a lot of money. HCG being a relatively smaller firm, it would again be meaningful to see the expenditure versus the value consulting firms are able to bring in over time.

Waiting with bated breath to observe the next developments!

Disclosure - invested.

Ahmedabad (probably greenfield, same city although I am not sure) - yes it’s greenfield. It’s appro 2 km from the current facility. The construction is going on for a year. I believe they will shift the current operation of HCG cancer to the new centre. (While their multispeciality - HCG Medisurge will remain operational in its old location).

Due to radiation, they need to dig ground much bigger hence it typically takes more time to complete vs hospitals without radiation facilities (like 4 yrs vs 3 yrs).

Thank you @Deven for the clarity ![]()

Would you know the how much are the other capex initiatives worth?