Hello @Rafi_Syed - Thanks.

Just want to know, how you get conf call summary from Ishmohit @Worldlywiseinvestors.

Mean to say from other VP thread or Twitter or website etc.

Besides reduction in debt, am surprised by the EBITDA margin; it’s 18.5 % vs 16.5 % of industry leader - Apollo. Is this an old or recent trend?.

I just want to point out a few trends in oncology and HCG are following that trend and implementing it quite nicely. The only problem was the debt that they took in the growth phase…

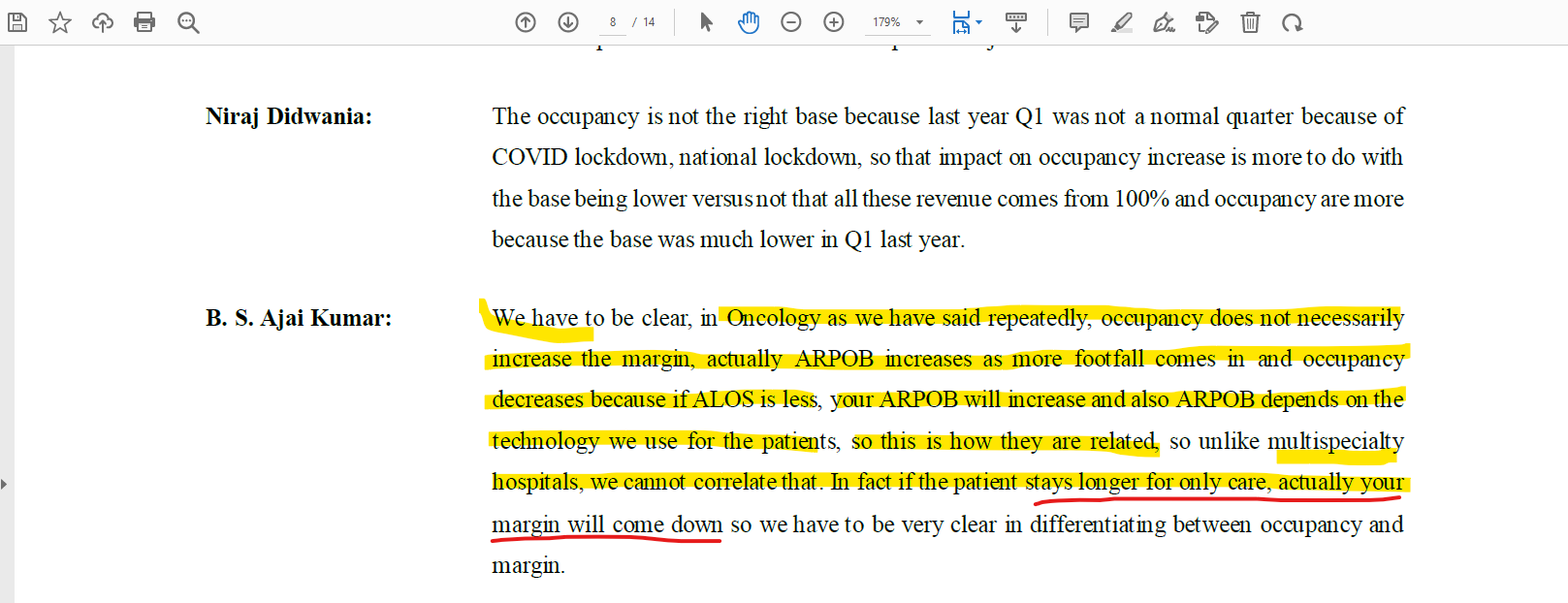

Oncology treatment is now predominantly outpatient based, most oncology treatments doesn’t need lengthy hospital stay - hence ALOS will continue to decrease. Bed occupancy also will decrease as a result. ARPOB is probably a better indicator

50% bed utilisation sounds bad but they will eventually figure out a way (I hope) to utilise the surplus bed space eventually (for eg co location/share the space with other medical/surgical or non-oncology specialists

Cancer patients will increase as the population ages - most cancer patients are living longer, and many cancers are curable

Most cancers can be treated in a small facility - massive hospitals are no longer required. HCG has created several such small hospital facilities in smaller cities. This is a huge advantage for them

They make more money from the patients who comes as a walk-in patient get the treatment done and leave. They don’t make much money in cancer care when a patient is admitted. This metric is useful for a multispecialty hospital. When it comes to cancer care the treatment is planned / scheduled over a period of time , patent has to visit the hospital for the treatment (like chemotherapy where patient have to visit multiple times for radiation ) . If it is a cyberknife surgery the treatment might be one-off .

Dr. Ajay in the latest concall was responding to Mr. Khemaka of InCred capital about modern therapies

Fututre treatments (Flash Therapy ) last only for seconds (40:35)

Yes, we do have to measure this metric of AROPB (Average Revenue per Occupied Bed, ALOS (Average Length of Stay) for the Multispeciality segment (they do have few ) but all in all this is not THE metric to track the performance in IMHO.

They still carry patient files from store to one building to another (experience from their main center in Blr) … I do not understand what data they are talking about … if they are collecting data and making use of it, it should reflect in publications. So basically we should look how many publications they are doing, how many of those refer to data?

From what I see, he has exercised the warrants now, but the warrants were allotted and 25% amount paid upfront in Jun 2020 at 130, which was almost equal to the share price at that time. So, don’t see any issues here. disc: Invested

we have to see at what period they injected the money and got the warrants ? Did they buy the warrant today or very recently ? Even QIP gives good discount (recently Yasho gave a discount of 35% to Mr Kacholia ) , we can’t compare the pricing with the retail ongoing price in the market when the company wants to raise huge capital. I may be wrong here, please correct me

Wouldn’t it would have been difficult for the company to get a rights issue sailed through in june 2020 when the markets were just starting to recover from the peak of pandemic drawdowns across all equity markets? And specially when their service offerings didn’t have clear visibility at that time for entire 2020.

Fully understand this sir, but the promoter doing this seemed very fishy. Especially, to a relatively new investor like me.

It may also be the case that in the recent years there has been a lot of criticism of usage of warrants by companies like Reliance Infra, that has created a prejudice towards the.

I had similar reservations regarding warrants in the past but it is an industry wide practice. Even companies with great corporate governance model use warrants to raise money from promoters e.g. Tata sons did it last year in Tata motors.

While raising money via warrants may sound fishy in case of share price rise, it will not feel so in case share price goes down. In a nutshell, in my experience, raising warrants has nothing to do with Corporate governance in the company.

Understood sir, but warrants do turn out to be an issue if it’s optional, right? So, in such cases if the share price goes down then the promoter has the option to not excercise the warrants? Or is it always compulsory?

Onchology is good margin and almost compulsory emotional spend for families

Naturally all Multi speciality hospital entering into it and enough trained surgical and medical oncologist available …they are eating up HCG share in onchology (slightly negative news , like other business onco market don’t expand)

The management is going to close the Capex except mainatenance Capex, since last 2 qtr(last qt was good due to internal transaction) . Centers are getting BE with increase of ARPOB 24% and AOR 53%. Moreover their margins increase due to growing cashflow, the topline will be good with respect to margin expansions with operating leverage.

Along with it the growing numbers of Cancer patients pacing by 12-14% from 5 years.