The reason for poor financial performance is merger

costs have gone up due to high cost deposits from HDFC and higher statutory reserve requirements. the solution is degrowth !! Management had thought they will get leeway from RBI but did not.

No operational gains are visible - while people are saying it will happen over time it may never happen at all !!

Technology wise, Service wise - competition is far better.

The bank is grappling with the merger and missing out on the growth opportunities which banks like ICICI are capturing. It may take a few years for the bank to come back and then too the return metrics may not be great. Will prefer to stay out and watch…

Personally, I bank with both ICICI and HDFC and find the implementation of net banking better with ICICI. However, my concern is about loans made today with banks and how many of these loans might end up as NPAs tomorrow. We can’t know for sure, but I hope HDFC performs like they have performed in the past and have made sensible decisions when underwriting loans.

Would it be correct to say that we are in that stage of the debt cycle when the loans are given out, bank loan books are growing? If yes, then we will have to wait when the debt cycle reverses from the present stage and some of these loans go bad.

Isn’t it better to invest when the sentiments are bad for a company? I am hoping HDFC Bank can figure out the issues in the future. Even if the bank takes a few years to do this, it shouldn’t matter for investing with a long-term perspective. It just gives us more time to increase our stake if we choose to.

Disclosure: Invested in both HDFC and ICICI. HDFC is more of a recent investment than ICICI.

The answer to this depends on an investor’s philosophy.

If you are a value investor, such negative sentiments will give you buy opportunities for longer time to buy a position in the stock in staggered manner.

But if you are momentum investor, then it is better to invest in stocks which are having tailwinds and are the favorites of the day. These stocks will give you immediate returns as long as the sector is in favor.

Stock which are not popular will be suitable only for investors who have patience and are ready to remain calm and remain convinced about the story.

No one knows whether any specific bank will perform better in future or not, but has to invest based on his/her own conviction without bothering much about the crowd. It is difficult to implement this philosophy but some investors have benefited in the past using value investment philosophy and will continue to do so in future.

Another approach is invest both in popular sectors & stocks and also in unpopular sectors & stocks from time to time. An investor can invest in both type of stocks if he/she believes in both philosophies. Probably I have used this mixed approach in the past 10-12 years and have at times invested in unpopular as well as popular stocks based on my own analysis.

For popular stocks, you need to buy at Fair Value to ensure that you are not overpaying for it, and Hope that they will be re-rated further by the Market based on their performance.

Stocks in this category were Defense stocks during 2022, IT stocks during 2020-21 and many more.

For unpopular stocks, you need to buy when margin of safety is high and those are undervalued as per your own analysis. No one can tell you whether it is undervalued or not but you need to take a call. Stocks in this category could be Coal India, NMDC, ITC during 2020-21 and Now today it could be few BFSI stocks & few Agrochemical and Chemical stocks.

I just thought of sharing my views based on my experience. Sometimes if you are lucky, both kind of stocks will perform over next 3-5 years!!

Note: I have not invested in all the stocks mentioned above. Those are only examples.

Indeed, these are high quality subsidaries that should grow at a PAT >15%. Currently, these contribute to about 5000Cr of the 68000 Cr PAT of HDFC (about 8%).

For sure, you cant buy earnings of this quality at a PE of 18-20 in the open market which is what HDFC sells for now.

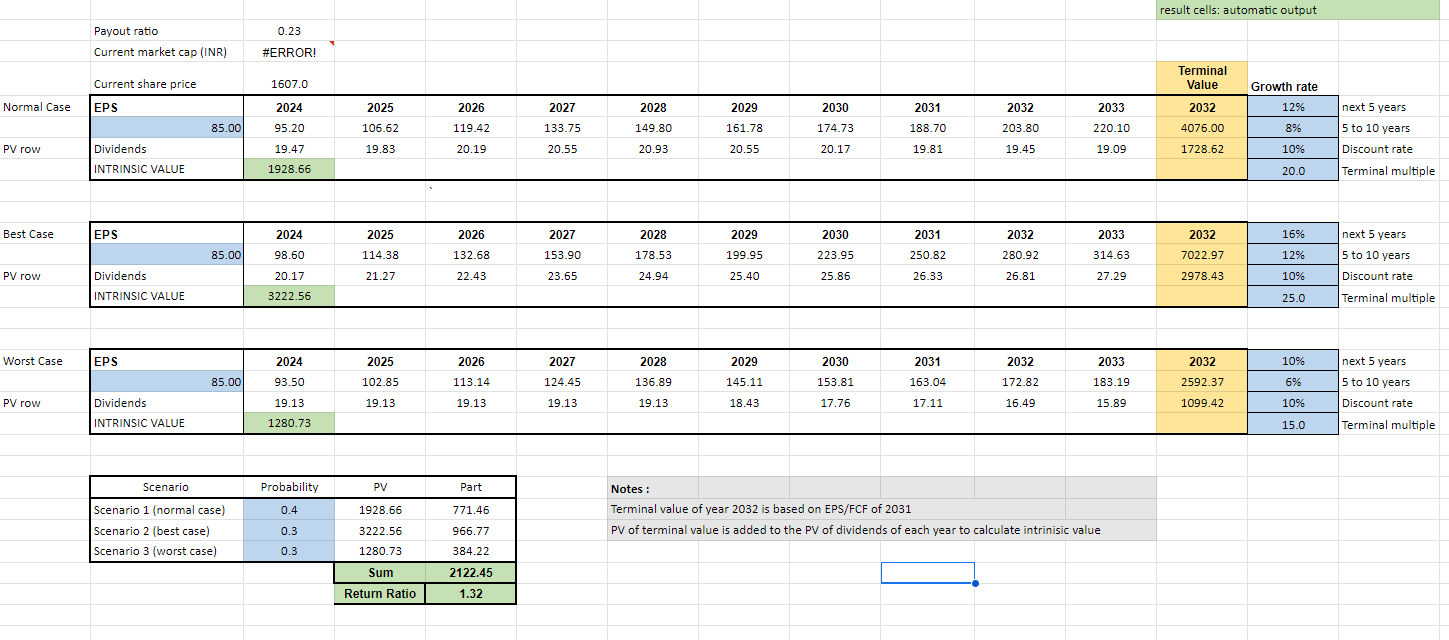

A light weight valuation of HDFC below. One should certainly make more than 10% going forward. Can be closer to 15% I think.

they are very complicated instrument’s

may include derivatives

credit risk default swaps

litigations etc

you cant realistically do analysis as there are many assumptions

Today, MSCI announcement was perceived negatively by market as expectation was that inflow will happen at one go vs actual inflows in 2 tranches, stock bled heavily today on the news. I believe, it’s a great pick at these levels for long term investment as interest rates start coming down both in India and US. Also, HDFC will get higher weight over couple of months, so expect staggered buying by passive funds. This should easily take the stock to 1800 levels in next 2 months. Any thoughts?

The credit to deposit ratio is a crucial metric that provides insights into the relationship between a bank’s loans (credit) and its deposits. In simple terms, it measures how much of a bank’s deposits are being lent out as loan]

Both of them will be deadly for the NIMs and growth. Also, with already such interest environment, and so much competition it’s very difficult for it to get more deposits and by reducing loan dispersal growth will take a hit.

This means that ICICI can grow its loan book much easily compared to HDFC bank.

The shear size of HDFC bank and the loan books of HDFC limited are few of the causes for the pain.

Thus is what I’ve understood till now.

In fact until RBI is stringent on the finance sector, pain might continue for longer even if the bank keeps performing what it’s been doing since long.

I had bought the stock at 1400 and sold it at 1700 . i don’t think hdfc as a great investment ,not only because it’s to big but because i have had a account and do love to use credit cards for rewards and it not common to see post about hdfc treating its customer badly even with good bank relations.

i think lower intrest rates will help the bank but still i fell the amount of deposit needed for this size is way to much and will take time to get sorted all the while peers are also available at same valuations .

Today’s share price is roughly same as the pre-merger price of Rs.1650 odd. Before the merger, HDFC Ltd held 25 % stake in HDFC Bank. So, the valuation of HDFC Ltd included the value of its holdings in HDFC Bank, which we can say was Rs.2.5 lac crore. That leaves the value of HDFC Ltd (ex-HDFC Bank) to Rs.2.7 lac crore. Add that to Rs.10 lac crore and you are at Rs. 12.7 lac crore, close to today’s valuation at an aggregate level.

But there is equity dilution to the extent of 35 %. To adjust to that, value of each share should be marked down by 25 %. (If 100 shares become 135, share price will adjust downwards by 25 % approx.)

Thirdly, HDFC Ltd was a worse business than HDFC Bank, so the merged entity will get lower discounting than before.

When you adjust to all this, today’s per share price should be much below pre-merger price of Rs.1650-odd. But then the broader market rally and the bank’s growth last one year helps it push up back to Rs.1650 perhaps. Today’s price doesn’t seem out of place.

First of all HDFC ltd actual market value was much higher than what it was getting due to holding company discount so 2.7 lakhs could be a depressed market value. Second since merger, bank has increased the book value by 20%. So it beats me as to why the current price of the bank should be the same as pre-merger.

Also you ignore the fact that premerger 1650 price was at 3.5 times book while current price is at 2.7 times book. At the same book value the price should be 2100. So currently market has already discounted all the bad that it sees in the merger.

The data that you have shared suggests that the issue is systemic and sooner or later other banks would also hit the wall w.r.t CD Ratio. HDFC Bank has merely acted as the canary of the mines due to its merger

Reminds me of Andrew Lo’s quote in the book - Adaptive Market “Government is a source of systemic risk”

Let me elaborate, in a country where the real inflation is way above the official one, tax on Fixed deposits or Recurring Deposits never made sense when the interest fetched by such instruments were too low.

In fact, taxing Recurring Deposits itself shows that RBI/FM is not aware of the utility of the product. Recurring Deposits are a form of compulsory savings and encourage individuals to save periodically. They do not earn the kind of interest as in FDs. By taxing them, you are effectively discouraging the public and telling them to go find some other avenues.

Why would anyone put their money in bank to allow the Govt to tax whatever peanuts (Interest minus Inflation) they got from their deposits.

By stating that Banks should think outside the box, RBI is merely passing the buck instead of suggesting correction in Taxation norms for such banking products.

RBI, Finance Ministry are at the moment disconnected from reality. Lets see how the things pan out.

Thank you all for your comments/posts/feedback. … this is what Valupickr forum is all about - all your thesis and anti-thesis related discussions in one page and it goes on …and on …enlightening all of us.

Due to the merger with HDFC ltd (which was a mortgage lender so didn’t take any deposits, correct me if I’m wrong), the CD ratio, Credit part of the lender was added while deposits didn’t grow hence the ratio jumped to above 100%. Another point to note is that there must be some loan structuring etc that might be happening since we don’t know if HDFC had the same standards as HDFC Bank when it comes to loan recovery, etc.

As I mentioned about the acceptable ratio previously which is around 80% and less, others won’t have this issue as they already are in the acceptable range.

So it’s basically the problem for HDFC Bank, not for others, as even if others grow their credit and deposit ~ equally, they won’t have the problem but for HDFC Bank at whatever growth they have, they have an added compulsion of making sure Credit < Deposit.

All in all, once this issue is sorted, we might see rerating.

This will pertain till RBI is tightening it’s noose. I personally think it’s good for them to have a tight noose to reduce slippage, etc since we’re moving into credit based society as consumerism/premiumization keeps on increasing. If you’ve observed the recent results of microfinance, you’ll notice that MFI is not at all healthy these days. Of course it may not be related to larger banks, but still we don’t know how big a picture that RBI is seeing.

Generally, NBFC’s have a high credit-to-deposit ratio because they don’t have SLR or CRR. So they lend a very large portion of their deposits, whereas when it comes to banks, it is not possible. So when a NBFC merges with a bank, the CD ratio generally increases for the bank. But in the case of HDFC Bank, it went above 100. So they have to slow down the gear of lending to 1 or 2 or shift the gear of deposit growth to 5 or 6. What is suspecious for me is: what is the reason for the hurry to merge HDFC with HDFC Bank soon after the pandemic? There were rumors that a large chunk of builder loan of HDFC is in verge of defaulting, so to tackle the situation, they have merged it with the HDFC Bank. I don’t know whether it is true or not. As a result of the merger, HDFC Bank shareholders who held the shares prior to the merger did not benefit significantly. The merger has actually had a bad impact on the shareholders, as the EPS has fallen now compared to pre-merger. I think the bad result of HDFC’s pandemic loan book is now affecting the shareholders of HDFC Bank as well.

You are right on most of the counts, but why should it get rerated? If it is no longer the same entity, investors should not expect the same multiple as before. That seems to be the collective wisdom of the market. My observation of last so many years is that the Mr. Market is generally right in pricing assets. Mispricing happens, but it gets corrected in a short period of time. Mispricing is more likely and may prevail for longer periods with smaller, less tracked, less liquid kind of stocks than with bigger ones due to technical factors. With a bank like HDFC Bank - literally the torchbearer of the India story - it is impossible that the market will misprice the asset for a year.

I don’t think it has anything to do with the pandemic. The chatter around HDFC Ltd - HDFC Bank merger has been around for a long time, may be for 10 years or more. But nothing came out of it. It had to wait for one particular event to take place, for the merger to move ahead. Once you identify the event, is will be easy to connect the dots. Think.