Hello Aarti,

how have you concluded that valuations are high? Also, would like to hear the reason behind saying that merger is not working out as planned within 3-4 months of merger.

4 Likes

No growth? I’m guessing that’s your thesis and not the reality

4 Likes

HDFC is growing in absolute profit but that is irrelevant to value of a share- what matters is per share earnings growth - it is flat for a year since merger

1 Like

I believe EPS CAGR for 3 years is a realistic tool to measure growth. YoY growth may have large variances. For HDFC bank the same is 13.5% and is fairly good keeping it’s size in view. If the long term ROE remains 16-17% then PBV of 2.75-3 is fairly valued with minimum downside risk within the asset class.

6 Likes

how about on PBT numbers… both YoY and QoQ… seems quite bad

there is some tax accounting so tax rate is low and hence PAT and EPS are better.

My notes on HDFC Bank based on my limited understanding of lending idustry:

Positives:

-

History of impeccable credit quality across multiple credit cycles. HDFC Bank has remained the best credit underwriter for more than two decades. Credit quality may continue to remain impeccable in the future. This is my assumption

-

Growth - Credit demand will continue to grow in the future, and only a few well managed banks will be able to take advantage of this tailwind in the future. All the profits can be deployed back to grow the business, creating a compounding machine.

-

Public Sector Banks - Even today, PSB’s have large chunk of deposits with them and the trend of business migration from PSB’s to Private banks will continue to work for a long time in future.

-

Cost of funds of large private banks is less than 5%. This is a huge advantage over other banks and financial institutions and extremely difficult to replicate.

-

Risk Taking - Because the cost of funds is low for banks, they do not need to chase high yields for risky lending. NIM of 4% is good enough to generate enough returns for them.

-

Regulatory Barrier - Banking is a regulated business with huge entry barriers. It’s extremely difficult to get a banking license from RBI.

-

Scale gives big private banks huge advantages. Their operational cost reduces a lot due to scale.

-

Consolidated industry - Though lending is a commodity business, the industry is consolidated with top 4 private banking players taking away huge market share.

Other positives :

- Reasonable valuation - After many years it is available at 2.5x book and 15 times earnings, cheapest in its history. It comes with HDFC AMC and Insurance business embedded inside, which provides further valuation comfort.

- Depressed Earnings - It currently has high cost of debt due to merger with HDFC. Cost of debt may decrease over time. NIM’s that are currently at 3.5% may inch up 4%+ as merger stabilizes. Profits may increase over time, even without growth in next couple of years.

Negatives:

- Size - It’s the largest market cap company , how much can it grow? Isn’t the company already too big to grow?

- Black Swan Event - The first industry to hit in a black swan event is lending and HDFC will have to take its share when negative events unfold. However, past shows that though during black swan events (Global Financial crisis, Covid etc), HDFC stock did suffer, but business/ credit quality was never a issue.

- Regulatory Axe - Business is highly sensitive to regulatory actions. Recent reference - Kotak being asked not to onboard new customers by RBI

- Nature of business - Lending in itself is extremely difficult business where profits of last many years can be wiped out in a single year. Quality of lending book is always opaque topic.

Past fundamental performance of HDFC may not be indication of the future, and my entire thesis rests on the past of HDFC.

Disclosure - Invested. I may sell anytime without informing the forum. I am a amature investor, not a SEBI Registered analyst.

21 Likes

HDFC bank traded at 4 times book because the profit growth and RoE were 20% in the past. But if an investor has to take a conservative estimate of book value increase of only Rs70 per share, then it leads to a profit growth of 0% and a decrease in RoE of at least 3% every year (15% in FY25, 12% in FY26 and so on).

BHEL was consistently delivering RoE of 20% and hence traded at P/B=9 till 2010 but then between 2016 and 2023, it traded at P/B of 0.6-0.9 when fundamentals changed.

So if HDFC bank profit growth is mid single digit and RoE is 10-12% (I am not of the view that HDFC bank will go this way in the next 10 yrs), then it will trade at 1.2-1.5 times book like Bank of America.

Hence such conservative estimate of EPS should also change the Price to book multiple assigned to the stock. It is mandatory for HDFC bank (or any other bank) to maintain a EPS growth rate of 10% to even trade at 2.5Xbook (assuming NPA remains same).

6 Likes

Article from 2015 -

Then the mcap was $750 billion and now $2796 billion

Obviously HDFC bank is not a global company like Apple, but India is a huge market in itself.

9 Likes

The growth in stock prices of any bank will be driven by the following:

1- Credit growth in economy

2- Bank’s ability to maintain or grow market share

3- Valuation adjustment

So you can see stock price appreciation for a bank should have nothing to do with its size. ICICI bank, despite its large market cap, is still the best performing bank, on the basis of stock price return, compared to any small-mid size bank (not including NBFC), over any time period. Conversely, you can have the stock price of a small-midsize cap bank do nothing for a long time, if they continue to lose market share or trade at above-mean valuations.

Coming to HDFC bank, they have been growing their book size at 20-22%, on an average, which is well above India’s historical credit growth (12-14%). It’s because of their operational efficiencies and gain in market share.

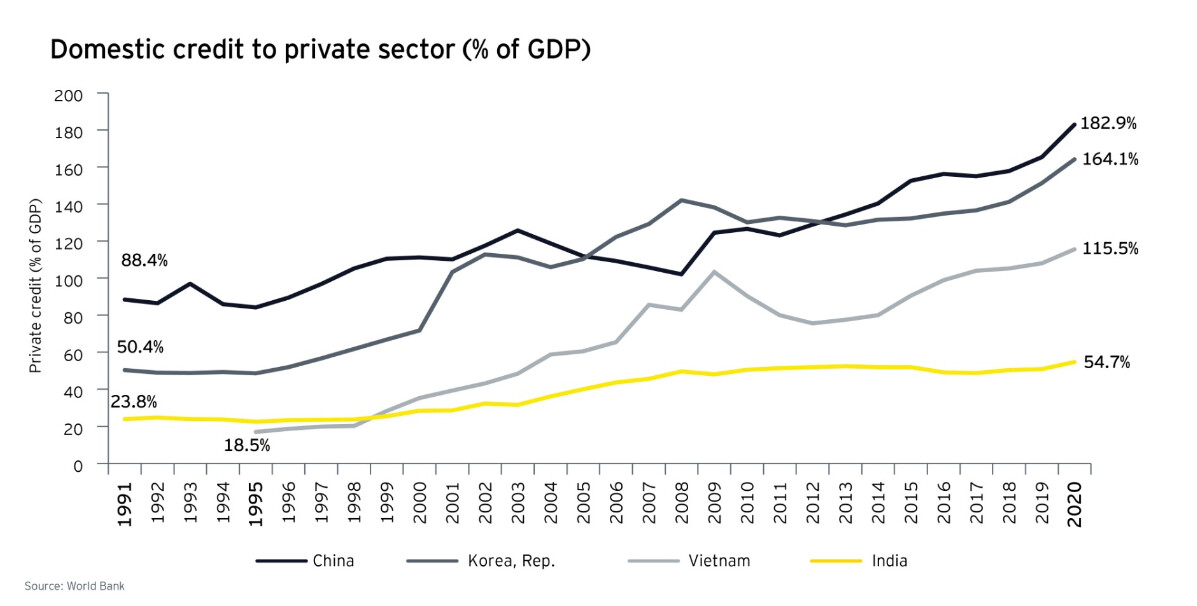

India’s credit to GDP is among the lowest in the world and as per many experts we are at the start of a credit boom (see the chart below).

So without getting into too much detailed analysis, big picture looks very promising for banks like HDFC. Even if HDFC can maintain their market share (which they will and even grow further), they should be able to grow their book at 16-18% (even with a large base) which should translate into the similar CAGR return on stock prices in the long run.

Valuation-based upside is just bonus.

Market cap is just a number. 15-20 years ago, we had very few companies trading at 1 lakh market cap and it was considered to be extremely large. Now we have close to 100 companies with more than 1 lakh market cap. And who knows what will happen in next 15-20 years.

20 Likes

banking surely has good future. but will all players make money?

HDFC Bank’s margins are too low to justify the valuation. Due to merger costs are high and no benefit to sales or operational efficiencies. This merger may go down as a one of the biggest corporate mistakes.

Disclosure - Exited.

3 Likes

Let the time be judge. Consensus view on merger synergy timelines are 3-4 quarters ahead so it’s too early to write it off.

In the meantime HDFC bank has been making money even after merger (isn’t it). Bank is run by smart people and I’ll trust them to figure out a way to make even more money.

Disc- Invested and adding more

17 Likes

Totally Agreed. I think pointing the merger as “the biggest mistake” to the biggest banking group of India is a little early. They have taken this decision with a vision. The base size is definitely bigger and Cost of funds might be higher for now but I guess when things are temporarily hurt, that’s the best time to acquire or buy them (in stock markets, businesses). I don’t expect it to give as high returns like a small-cap but for investors looking for valuation comfort in safe stocks in this continuously rising market, it is definitely one of the best candidate for now(or any other of the top 4 private sector banks for that matter).

Disc.- Invested. Rotated most of my profits to all top 4 private banks.

11 Likes

Today stock made all time high… scaling handsomely by 24% from the point of deep pessimism around the stock at the time of last post here.

Just another proof that banks need to and will participate in any bull run in Indian equity market. And quality banks like HDFC have been, are and will continue to remain compounding stories, a few setbacks here and there notwithstanding.

16 Likes

Wondering why there are no talks around the hot topic on the higher probability of $5 billion inflows into HDFC Bank in August MSCI India Index rebalancing… Experts opine that this might take the share price to more than 1800 levels. What are our members view?

2 Likes

Today I sold my holdings after 4 years and got returns as much as fixed deposit. The reason being simple was to free cash from such slow moving company. Decided after this stock becoming systemic to the India’s Banking and the growth (beyond GDP growth) will be not be what an aggressive investor should look. Elephants cant sprint.

For aggressive investors, this scrip is not the one they should look.

3 Likes

Well basically, this stock will move when we will have interest rate cut cycle. As you can see stock has not moved much, because since last couple of quarters, India (and other countries like US) have gradually increased interest rates. Thus no movement.

I also sold HDFC. But will enter when RBI will move ahead with interest rate cuts.

PS - not an investment advise. Just sharing my thoughts on why things are not moving.

5 Likes

Quite simply HDFC bank is a very solid company but may not be a great investment at this stage of its evolution.

Main reasons : Very large base + no particular USPs + well valued + well owned.

Just my opinion.

How can it become a great investment ? It needs to develop a strategy where it can dominate.

3 Likes

Given the kind of of run in the markets its the companies like HDFC Bank give stability to the PF.

2 Likes

HDFC is a bank which is a commodity business. Best banks are those which contain non-performing assets which HDFC Bank has done superbly over the years.

Universal banks in India need to have only one strategy, reduce the cost of funds while managing risk in loans book.

HDFC’s merger with the bank has increased its CD ratio >100% and it is putting pressure on the bank to increase its deposits at a time when there is a competition among the bank’s to garner deposits. Their timing is unfortunate. However, these are 2-3 quarter issues.

Private bank’s (and quality NBFCs such as Bajaj Fin) underperformance in last three years mean now they offer very good value in a very overvalued market. Their balance sheets have continued to grow, without increase in NPAs. They are well capitalised.

I think it is a time to get into these businesses (HDFC, Kotak, Bajaj etc), not out. Off course nobody knows when they will catch fancy of the market, they still remain great franchises available at fair prices.

Dis.- Invested in Kotak, HDFC Bank, Bajaj Fin

19 Likes

I wonder if the HDFC prices will start moving up once the FPI inflows go up again. That’s my guess as to why the prices are subdued now. However, I don’t expect a multi-bagger return. That said, I expect the return on HDFC shares to be better than the FD returns.

Disclosure: Invested

4 Likes