Good read on the state of Indian banks

https://x.com/TamalBandyo/status/1825368910842954046?ref_src=twsrc^google|twcamp^serp|twgr^tweet

Good read on the state of Indian banks

https://x.com/TamalBandyo/status/1825368910842954046?ref_src=twsrc^google|twcamp^serp|twgr^tweet

Stock price increase doesn’t have to come from just rerating. Earning growth is also an important factor and so far bank earnings haven’t slowed down.

Moreover, multiple rating has got nothing to do with asset mispricing. Mispricing is when market is not rewarding earning growths for a stock at the average sector valuation. Valuation rerating and derating are more driven by sector dynamics and collective wisdom, of the market participants, about the future of a sector.

Every sector goes through cyclicity in valuation ratings. Take IT sector in 2022 and 2023. All the stocks got badly derated and we saw the arguments from naysayers telling that IT story is done (with typical threadbare analysis of their valuations, business prospects etc). All IT stocks got beaten which doesn’t mean that market was mispricing them for 2 years. It’s just that market was pricing them at their earning growth on depressed sector valuation.

Market “collective wisdom” changed about IT sector in 2024 and started rerating the sector even though earnings still haven’t started to come through. I can provide similar data points for the other sectors. So “collective wisdom” of the market can be unpredictable and not something to be taken as permanent.

Coming to financial sector, all the private players (Kotak, Axis, Bajaj Fin, Indusind) have seen their multiples getting derated due to various external factors well summarized in this thread.

So when the rating cycle for banking industry turns and HDFC bank doesn’t benefit then it will make sense to analyze all the things wrong with the bank and pricing aspects. Before that making any predictions about stock prices is futile.

That’s already factored in stock price to book. Book value per share will go down with equity dilution. So current multiple of 2.7 times is after reduced book value.

RBI ruling regarding CDR applies to all the banks so yes it’s an argument to use if one is bearish on the entire banking sector but it doesn’t exclusively impact HDFC only.

With interest rate cuts banks will again go back to raising capital from the market. Big picture is that if we are bullish on Indian economy, banks need to participate in that growth. As investor we can’t lose breath over all micro-developments.

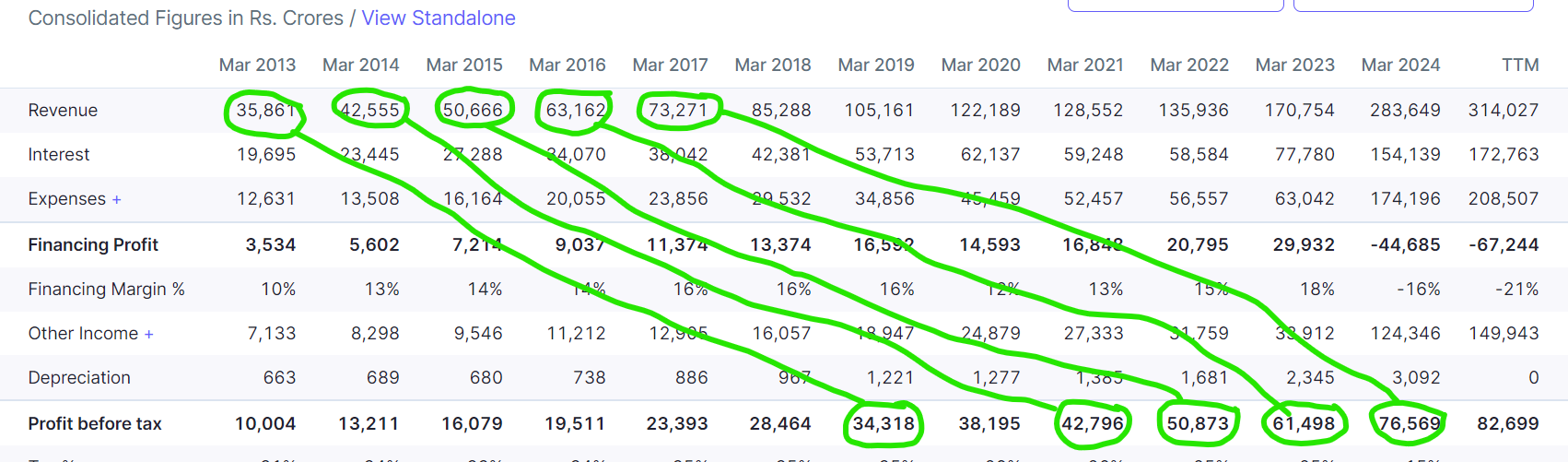

Interesting Revenue-PBT Pattern with a lag of 6-7 years.

Can this be repeated in future? Disc-Invested.

Oct-2019, Raamdeo Agrawal : One of the things is that credit intensity in the economy which is about 70 percent of the gross domestic product (GDP) – so Rs 200 lakh crore of our GDP, the outstanding credit must be about Rs 140-150 lakh crore. But world over what happens is the next $3 trillion will have a significantly higher credit intensity. So if the credit flow is not there, there is no GDP.

You can make it minus 100 percent and there is no GDP growth. That kind of thing. It is just one-to-one correlation. So it is a tower of credit. So my sense is that we will go to $3 trillion, we wrote about this trillion dollar economy in 2008. So we are watching it for the last ten years, it will go to $6 trillion and it will go to $12 trillion also, but let us talk about this $6 trillion and this will happen by 2026-2027.

When this happens, you will need about Rs 200-250 lakh crore of credit to be underwritten in next six-seven years.

That’s just coincidental because sales and profits have grown at the same % over the last 5-10 years. If sales and profits grow at different percentages it won’t hold true. Still nice observation though!

Thanx, I wanted to explain that if the bank continue to grow in similar pattern, the PBT in 2030 shall be 2.8L crs.

So what should be the share price in 2030?

I don’t believe people are still quoting this as a reason for the deposit slowdown.

Growth in bank deposits has been slow because RBI wants it to be slow.

That explanation doesn’t wash. After all, if the asset buyer’s bank balance is debited to pay for securities, the seller’s account is credited. The pie may get redistributed among lenders, and its composition may change. Still, money won’t leave the system, except at ATMs, and the use of cash in transactions is slowing.

In India, due to double-digit nominal GDP growth, the money supply must also grow at a corresponding pace, often in double-digits; if the growth in money supply fails to match this pace, it can lead to tightening financial conditions.” The term tightening financial conditions basically refers to the slowdown in deposit growth. So, why is RBI not creating money at as fast a pace as it was in the past? The answer might lie in the high inflation, which the central bank has been struggling to manage.

Above posts were quite interesting from the perspective of an investor in the private banking stocks.

The past 3 years have been quite different for the well known private banking stocks i.e. HDFC Bank and Kotak Bank.

This is after long time that, both these stocks have struggled to generate any meaningful returns due to various reasons.

May be, private banks need to come up with some flexible solutions like iWish Deposit from ICICI Bank, which allows the customer to deposit any amount flexibly into the iWish Recurring FD. More innovative products like this can probably increase the interest of customers to the deposits.

Also, high rate of unemployment which is almost at the peak after about 40 years, is not allowing many people to save and hence they are unable to invest more funds into deposits. Some of my retired friends have also told me that, they are unable to save now-a-days as their expenses have moved up rapidly after retirement, and hence they are not using deposit as a product as they used to use earlier.

People with lower salaries are also probably facing similar issues of Low savings.

Apart from the fact that, Central Bank is struggling to control inflation, some other data points also might be looked at to see Why deposit growth is tepid as compared to Loan book.

I may be wrong in my analysis, as I am not from pure Finance background.

It is definitely the reason for low and slow deposit growth.

There’s plenty of money in the system but deposit is not attractive compared to stock market.

"₹12-crore IPO of Resourceful Automobile, an SME company, which attracted bids worth ₹4,800 crore.

The ₹6,560-crore IPO of Bajaj Housing Finance set a new record, with subscriptions exceeding ₹3 lakh crore. The IPO was oversubscribed 63.61 times."

Post from another thread:

3.2 Lkh crore blocked in bank accounts towards Bajaj finance IPO size of 6600 crore- looks scary !

Source:

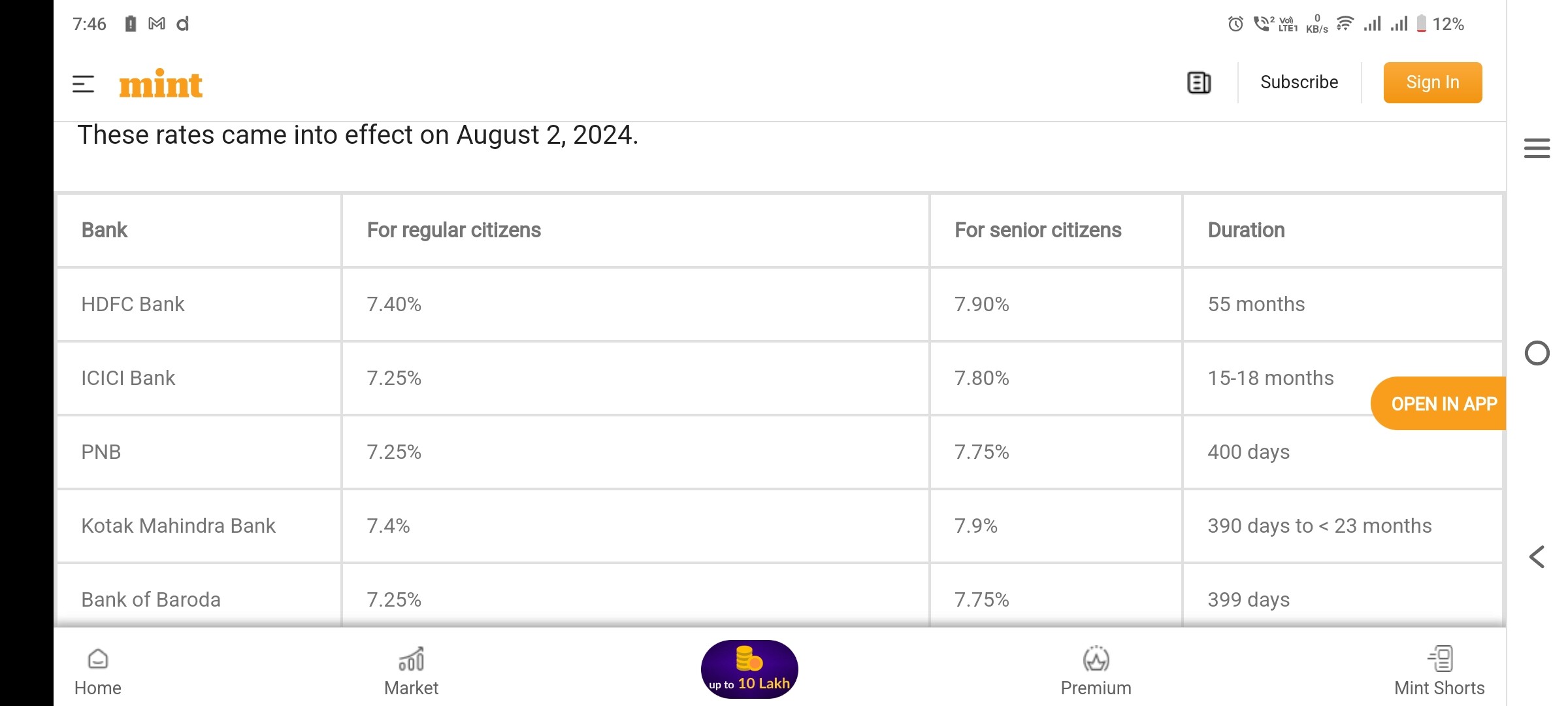

The bank FDs are not even yielding 8% pa interest. Over that, the interest is taxed at peak slab rate. For me it is 35%. So post tax, returns is 5.2% while the real inflation will be North of 7%. And there’s no deposit protection beyond 5 lakhs.

I don’t see any incentive in Bank FDs. Money will be better placed in nifty index fund which will give 12% cagr over long-term.

A patient investor in HDFC Bank and Kotak Mahindra Bank will be better rewarded than an FD holder in those banks. Also, we are at the peak of interest cycle and interest is bound to go down from here which will bring down the FD rates even further.

I think the point of the article was that all money in financial system remains with financial institutions such as banks until someone withdraws it as cash.

Even when it is invested in stocks, there is always a seller who will recieve the money in his bank account.

Similarly the money used for ipo applications also resides in bank account. So it is already with banks.

For loan book to grow, deposits need to grow and for that supply of money (rupees) need to increase.(domain of RBI).

I am trying to understand your post…

One side you said the money is going to equity market which is causing deposits to dry (I don’t agree), there are good articles shared above, the loans create deposit and RBI is sucking up liquidity.

Another side you pointed to post about 3 Lakh crores applied for IPO. Whats wrong in that? This money is sitting in bank accounts.

You are correct, but what you’re referring to is CASA, or current account and savings account deposits.

If you dive deeper into the issue of deposit wars, it’s not about CASA; it’s actually a war over term deposits or longer-term deposits. The so-called ‘FD’ (fixed deposit) isn’t as popular these days. Many financial influencers are actively discouraging it, and as a result, funds are flowing into alternative investments like equities.

Currently, term deposits are being replaced by CASA in the system. While CASA is a cheaper source of funds for banks, term deposits give banks the confidence to underwrite longer-term loans, such as home loans, commercial and industrial loans, and other large-scale lending. Banks can’t rely on CASA for such loans due to an entirely different issue: Asset-Liability Mismatch.

If the money is sitting in Bank accounts, why the banks are not getting deposits? Ironical isn’t it?

Banks have the deposit. The question is is about incremental deposit growth, not decline in deposit.

did HDFC Bank make a mistake by merging with HDFC Ltd?

Bajaj housing finance is trading at 6x P/Bx. May be euphoria.

The valuation after merger has dramatically shrunk for both HDFC companies.

According to this post, at 140 itself the PB ratio is 6.4.

At 165, the PB is 7.5.

yes so far.

I think, you are right. Even the traditional risk wary middle income customers in T2 and T3 towns are also now preferring the MF than FDs. Looks like HDFC is already trying to sell some of their loan portfolio. The Solution could be change in the tax treatment by government for FDs. In case of FD, you are taxed at slab and are forced to pay the tax every year when compared to Capital gains tax which are at a lower rate and you need to pay only when you capitalize it. The cash may be in the system with securities market but still FDs provide the banks with cheaper source with clear view of the liquidity requirement.

A similar argument was made by Debasis Basu of Moneylife

"A study done by Franklin Templeton Mutual Fund reveals that the AUM of mutual funds is 31.30% of the total bank deposits in India. This ratio was 24.20% a year ago.

This proportion has tripled in 10 years. In March 2014, the AUM of mutual funds was 10.70% of the total bank deposits in India."

Source: