HDFC Bank’s moat as the largest lender has gone nowhere. It has among the best lending practices. It is as solid as it was, say, a year ago. The valuations have become extremely attractive now.

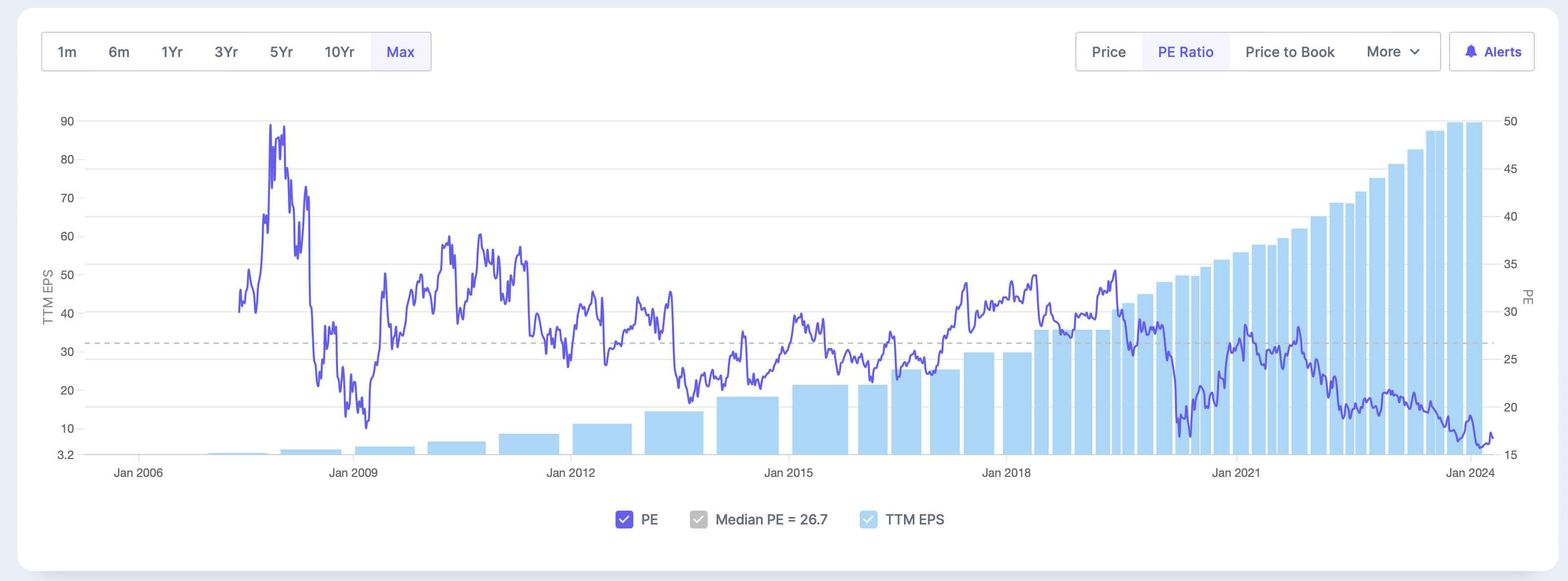

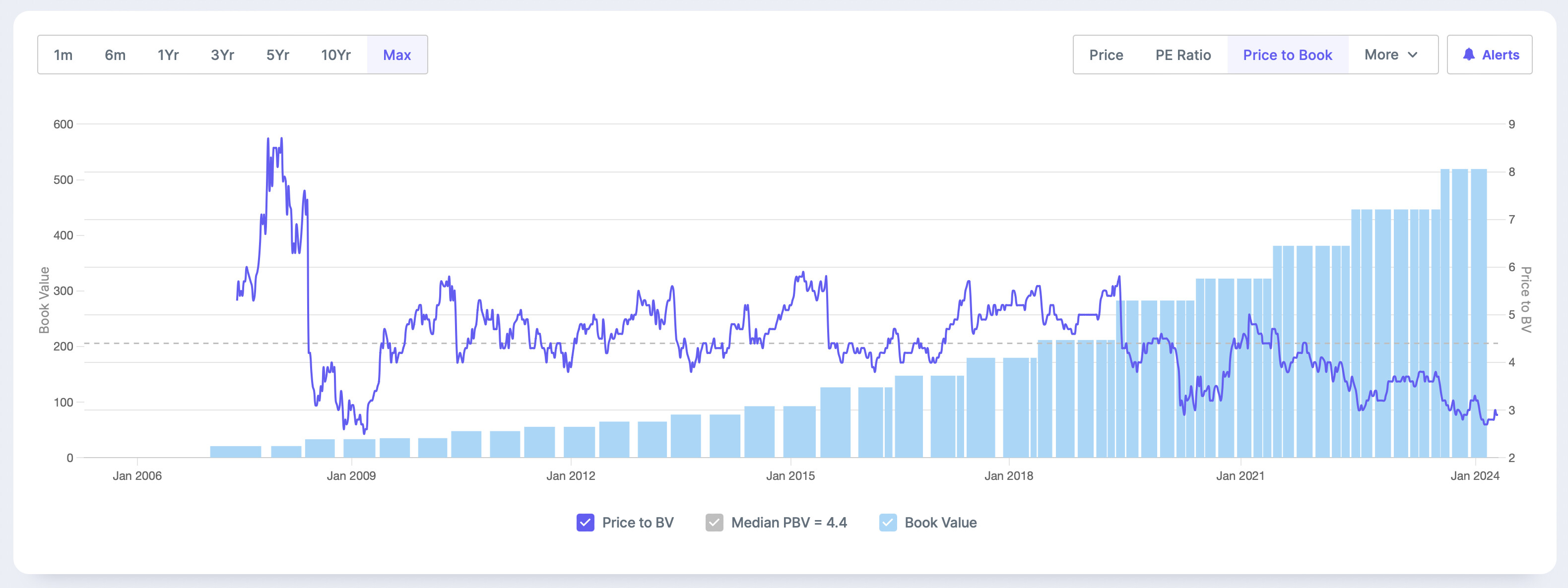

It is trading at the lowest P/E and P/B range in last many years’ history.

At present, it looks like a great investment opportunity, especially when adjusted for risk.

With the Indian economy set for decades-long growth, the largest private sector bank will have to go really wrong in their strategy to not grow. HDFC Bank’s history does not seem to suggest that. Rather, they’re the market leaders in many segments.

As economy picked up other cyclicals also became available for investment namely auto, infra, industrial, manufacturing and even pharma came out of downturn.

So exclusiveness premium which HDFC and FMCG enjoyed went down.

But absolute return investors should do their valuation analysis and take call.

Credit growth is what drives banking industry while deposits are fuel for them. Higher deposit growth means low capital cost for banks as they don’t have to tap financial markets for raising debt which comes at higher cost (e.g. 8-12% compared to 3-4% interest rate on savings account or 7% on FD accounts). This translates into higher net interest margin (NIIM). Finally asset quality of a bank shows their ability to recover their loans from the borrowers- less bad loans means less provisioning for NPA meaning better bottom-line.

HDFC bank of late has “disappointed” on all these metrics after the merger.

1- They inherited a lot of bad loans from the HDFC limited impacting asset quality

2- Net cost of deposit went up due to high cost of debt of HDFC limited, the latter being an NBFC

3- They have been conservative (and rightly so) in their lending (avoiding risky borrowing class) impacting credit growth

4- Slow deposit growth means they are attracting less deposits from Indian public raising questions on their ability to raise capital at low cost- having implications for NIIM

All the above will impact profit growth, ROE and ROA, the main determinants for a bank’s valuation.

Coming to valuations, HDFC and Kotak Bank have historically delivered superior performances on both ROE and ROA, compared to their peers, which drove up their valuations in the past, both trading at much above 3 times book for a very long time.

But now some of their peers are catching up on both ROE and ROA which has resulted in moderation in valuation premium for both and hence time correction in their stock prices. Investors are choosing to invest in cheap banking stocks (trading at marginally above their book value) with slightly lower ROE and ROA than HDFC and Kotak.

Valuation concerns for HDFC seem to have ebbed, with stock trading at somewhere 2.5 times book. But low valuations don’t automatically translate into higher stock prices; they only offer downside protection (depending on the quality of the stock). Investors invest based on what a company will deliver in the future and not what it has done in the past.

So no doubt HDFC bank is a high quality franchise and has a great track record of execution. But they need to deliver the results for stock to get rerated. Merger has proved to be an overhang and it will take some time before stock can find its mojo back.

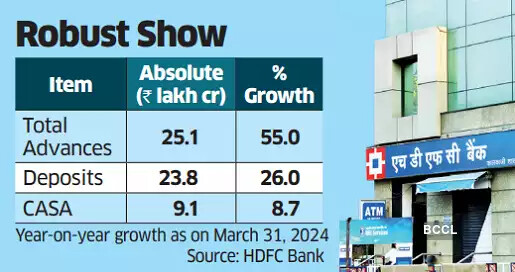

The CASA growth is the key metric to track going forward. Bank aims to have a total of 13,000 plus branches in the next three-five years. One needs to understand how much of these would aid low cost deposit growth. The March ending nos released by the bank show a jump but one needs to watch the trend

Disclosure: Invested from lower levels

It’s definitely a good news. Also I believe that NPA cycle is bottoming out in the banking industry so from here onwards market should start watching out for NPA trends. That’s where banks like HDFC and Kotak should do well given their strong risk underwriting.

HDFC bank is offering rates upto 8.05% on bulk deposits. Impressive growth in deposit but at what cost ??? Impact on NIM will be reflected in next quarter.

HDFC Bank share has tested the patience of investor over the past 3 years.

As we can see, due to merger with HDFC, there are some Builder loans which are putting stress.

NIM is also impacted due to the merger and may take another 4-5 quarters to stabilize. Till that time, investors will keep guessing and may have pessimistic views.

While other banks have done well to control their NPA(s), during past one year, the same may not be true going forward.

Though earlier premium valuations may not return back, but even with reasonable P/B, stock can hold due to moderate EPS growth and can sustain financial storms if they appear on horizon during 2024 due to geo political scenario.

Disc: Booked some profit before merger and now holding some position. This is my old holding since 2011.

I think right now is the best time to be invested in hdfc bank stock given the current valuations of the indian markets or even its peers.The markets are run on perception not long back there markets gave big companies like hul and hdfc bank and other large caps stock a higher valuation as these stock were considered to big to fall and the smallcaps and midcaps traded at significant discount as the perception was there is not much information known about the companies and are risky which soon changed to small/mid caps can grow faster.Not long back psu were given lower valuations as they worked for the nation not for the profit of shareholders and soon the perception changed of them being a monopoly .Now we don’t know when will this happen to hdfc but currently it trades at a significant discount then it ever has in the past.

No one can predict for how long the stock can trade for such a discount but let’s say it keeps on trading at price to book value of 2.5, which is the lowest it has ever been for the bank .The bank this year will 90 Rs as eps and i think it might give 20 rs given as dividend so it will add 70 rs to it’s book value eyery year and this figure is only going to increase every year as they have more money to loan out which is not borrowed and it is there own book value.But lets just stick to the most conservative estimate that the bank keeps on trading at price to book of 2.5 .which means that stock would have to appreciate by a minimum of 70*2.5=175rs every year to keep up the lowest valuations it has traded at.I know plenty of value investors has picked up the stock in the recent crash at 1400 levels so at a dividend of 20 rs and stock appriciation of 175 rs on 1400rs is almost 13 to 14% and it only going to increase every year,Tbh i am very happy to get 14% returns which are super safe.

Coming to the point of low deposit ratio i feel it is just a perception and soon it will change for me it is good thing as for a bank the deposits are it’s supply and the people who take out loans are there demand .With this logic the hdfc bank is currently at full capacity utilisation, which to me means sooner or later they have the the choice to charge higher interest but also choose better creditor with a better credit history and i am not even touching on the point that millennials take up more loan for there cars ,houses etc etc compared to Gen X.

disc: i am very optimistic about the stock and invested almost all of portfolio in it as i feel this is the next itc given the memes i have been seeing.

I think 12-14% annual stock appreciation should be a given from here on, even with just the index inflows and average profit growth. For those who are not looking for fireworks in their portfolio and happy with low risk, low returns, it’s a good bet.

In my opinion, the markets are digesting the merger. HDFC Ltd. had large holdings of housing loans, which had different dynamics from the traditional banking business of HDFC Bank. Therefore, the merger has caused some adjustments to NIM and other factors.

Having large institutional interest, HDFC Bank is also seeing some change of hands post-merger perhaps causing the current price pessimism.

HDFC Bank is a large stable blue-chip company, with no major imminent risks. It has a low beta in the industry.

No fireworks, profit slightly below expectations. Don’t think markets will be distributing sweets unless the management has a palatable explanation for the floating provision it has made.

Well, management made it clear why they increased provision. Bank inherited a lot of potentially bad loans from parent and increase in provision is a cautious move to protect balance sheet.

Overall, I won’t say it was a very disappointing result due to very low expectations this time around and there were some green shoots (e.g. beat on NIM). If there was to be a correction in stock tomorrow, it should be limited (as opposed to last time).

Merger is not working out as well as planned… has led to higher deposit costs and statutory deposits… financial performance will improve only after few years… operational performance will be good… but will not add to profits…

most likely to stagnate at lower levels for a year… at least.

I am thinking the slowdown has already begun. RBI trying to slow down loans, increased weightage, bank is openly admitting they’re struggling for liquidity, raised FD rates, cost of funds, suppressed NIM, increased NPA, everything will lead to the slowdown in growth or the stock will remain flat for a good time.

Very nicely explained,like the example of HDFC Bank , we have a similar candidate in Kotak Bank with somewhat similar EPS.

Provided banks in India maintain their premium valuation as compared to global standard.