The bank added 20k new employees and 500 branches in last quarter alone. The profit figure are very good after considering the expenses incurred for branch expansion and hiring. The stock has gone no where since 2020 but the profit is almost doubled.

7 Likes

there is a very cocentrated selling in hdfc & hdfc bank since november 2021 by FII’s. may be the fii’s dont want to merger to take place or something else. and the selling since the merger announcement is giving feel like march 2020. at that time also HDFC fell from 2400 to 1600 now it fell from 2900 to 2250 almost same. it’s moving like a small cap on steroids. i request experienced borders to give their valuable opinion on the price action of the hdfc and hdfc bank.

Nothing strange. HDFC is a company without any promoters (same league like ITC, L&T). The majority of the stake is held by FIIs. Whenever there is change in the macro economic environment (interest rate rise in the US market, better opportunities in the westerner world, forex fluctuations, etc.,), FIIs will tend to exit and move to other green pasteurs. As long as the fundamentals are intact and the long term growth looks positive, I would see these as good buying opportunities.

Disc: Invested in HDFC and adding more with every fall

9 Likes

Those mutual funds who are holding both hdfc twins will either sell or not buy hdfc twins further to avoid rule of10% of portfolio in single stock post demerger. Is this hypothesis correct? Can any senior member comment on above hypothesis and guide us further? Disclosure: Not having any position….but keenly watching.

I’m not a senior member. The rule says the total holding should not cross 10% due to buying more shares. If it crosses 10% due to share price rise or in this case due to merger, then that will not violate the 10% rule. So in our case the 10% rule is not applicable. Please correct me if I’m wrong.

6 Likes

Any idea how HDB Financial Services gets impacted by the merger? Most news seems to focus on subsidiaries HDFCLIFE and HDFCAMC and not much has been said about HDB. It was reported a while ago that HDFC Bank was seeking a buyer for strategic stake sale in HDB rather than an ipo. But other than that its been quiet in that front.

1 Like

Marcellus’ view on the mega merger.

…In this context of prudent capital allocation and fairness – the HDFC Ltd – HDFC Bank merger is a fitting finale to crown Deepak Parekh’s career as India’s smartest capital allocator. The combined entity will be value accretive for both sets of shareholders and it has ensured that the succession planning for HDFC Ltd. is taken care of.

4 Likes

Can anyone please explain how banks account for write offs? Is it accounted as a part of business expense or is it accounted in the cash flow statement?

As per my limited knowledge, write off is done against balance sheet.

Provisioning is done from Profit and loss statement. So there is a reserve of provision which gets money from pre provisioning operating profit .

Then later when required Non performing loans are written off at the expense of that reserve/provision. If the loans are written off and there is not enough provision then it will eat into bank’s equity. That will reduce share price since banks are valued in terms of PB ratio and the book value is nothing but the equity.

Suppose I have 30 rs (this is my equity) and I borrowed 70 rs at 0% interest to give a loan of 100 rs at 7% rate of interest. So I earn 7 rs at year end. As a prudent bank I have set aside 3 rs as provision from that 7 rs. So my net profit becomes 4 rs and after paying tax lets say I have left 3 rs which gets added to my equity. Now my equity becomes 33 Rs. Now next year also I give a loan of 103 rs but this time out of that 103 Rs lets say 1 Rs. becomes NPA and I can’t recover the money. Now since I’ve a provision of 4 rs so I can write off that 1 rs loan from my provision. Now lets say I have to write off 4 rs NPA. Then I have 3 rs provision and 1 more rs will be taken out of my equity of 33 rs and this will lead to provision becoming 0 and a loss of 1 rs.

8 Likes

if a bank has 1000 crore as NPA then it has to provide some provision against than npa amount. provisions vary based on the nature of loan. If the loan is a mortgage and it turned into npa they have to provide lets say 25% of the loan amount as provision for than loan. if loan is an unsecured one like personal loan credit card loan etc, then they have to make 100% provision against them. the provision amount will be shown as an expense. if loan becomes standard then they will write back the provision amount and the entire provision amount will be shown as profit.

as for write off , if there is no chance of recovering the loan then the bank will provide 100% provision for than loan and transfer the account to AUCA(advance under collection account). it means loan has been written off. by luck or any chance if any amount is recovered in the account subsequently then it will be shown as other income and will directly add to bottomline of P&L.

5 Likes

Thank you for your explanation and just to be clear the provisions are included under expenses that we find in the Income statement?

yes. they are included under expenses.

I think that revenue growth was only 10% and the fact that no dividend was issued this year seems to have turned the market bearish on HDFC Bank.

FII selling is the only reason for fall.

FII selling is the action…We need to find the reason behind this action

1 Like

That should be a separate thread, they are selling in many stocks, most owned stocks will get most impacted.

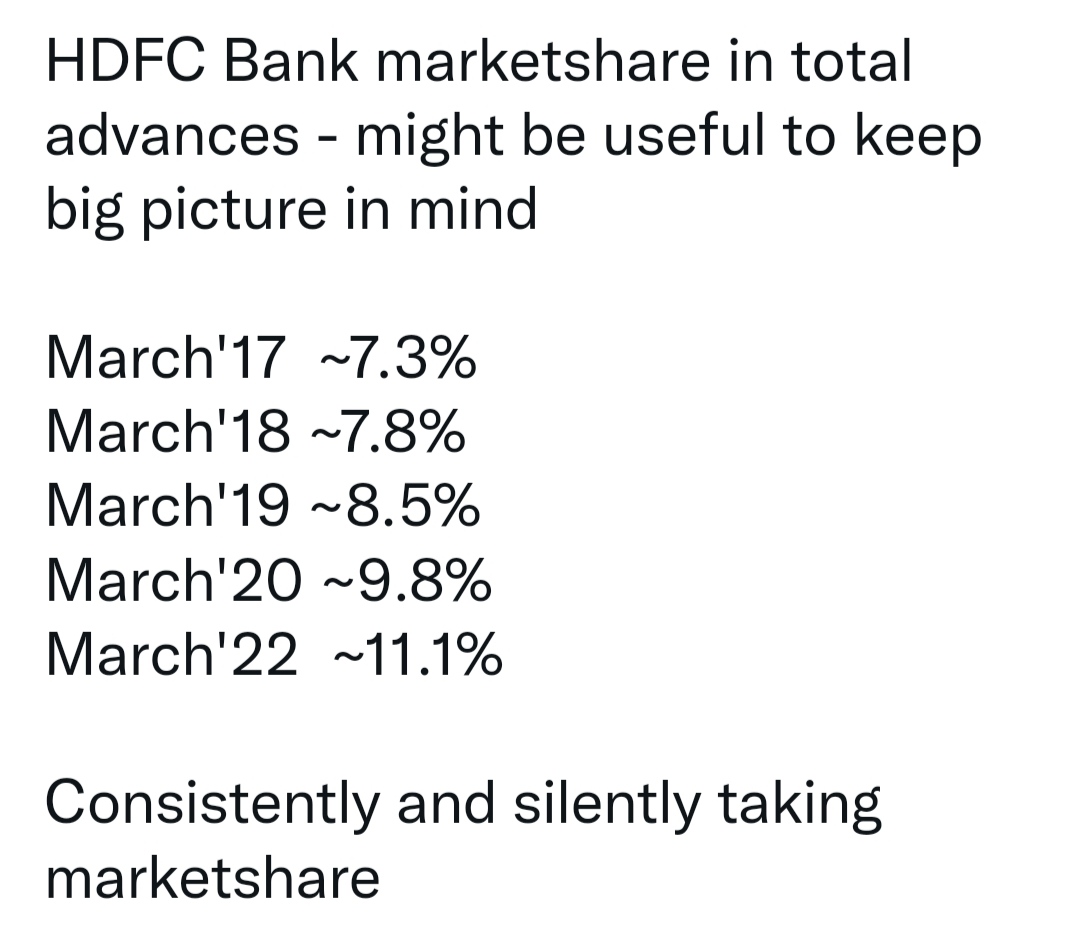

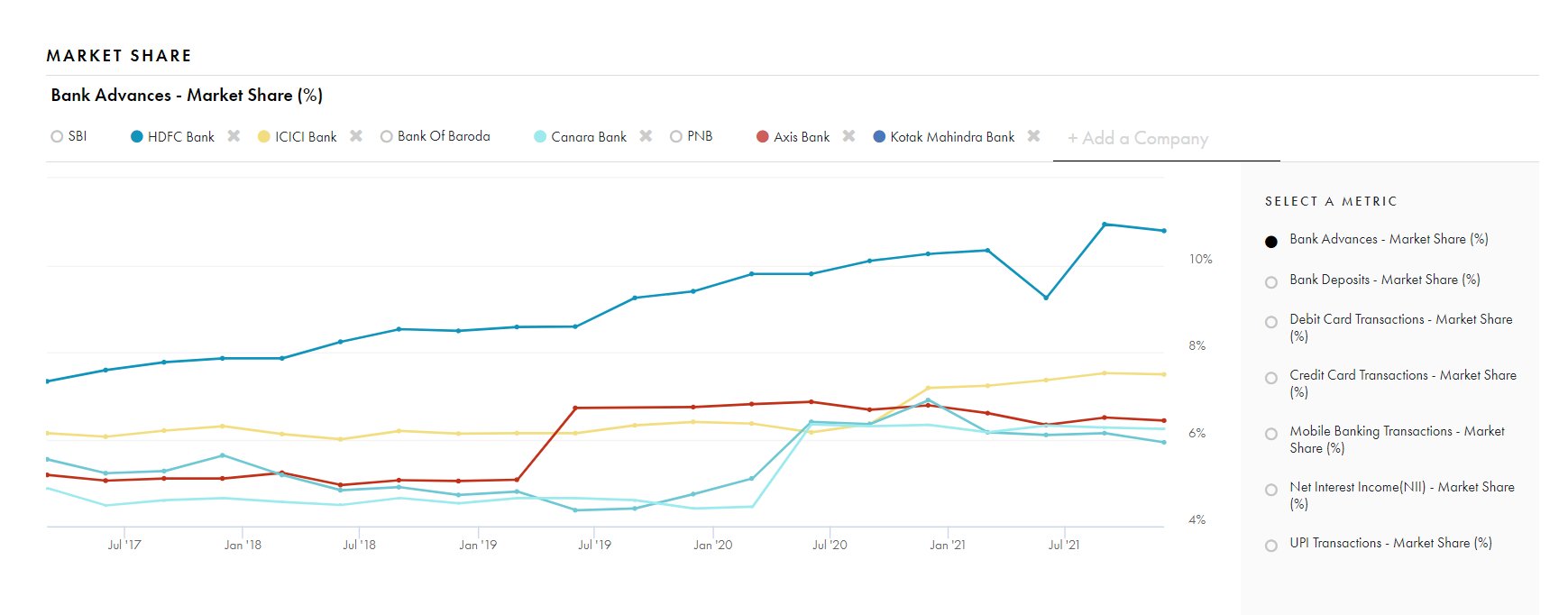

HDFC Bank has consistently gained market share on both sides of the balance sheet. Advances market share has shot up from 7% as of Mar-17 to 11.5% as of Mar-22. Similarly, deposits market share has improved from 6% as of Mar-17 to 9.5% as of Mar-22. No other bank has been able to clock market share gains on this magnitude over the past five years.

Source: Marcellus Newsletter

1 Like

I agree to this , FII selling can give us good companies at bargain prices. Do you a portal where we can track such activity

2 Likes

Can you or anyone with insights present more details on this? Will RBI stop such banks from giving any more advances and/or deposits if such an event happens?? Did SBI not have significant and bigger share earlier?

Have you taken into account the growth of the market itself? Also, the mix of corporate/retail etc. That HDFC Bank may play with while continuing to achieve 20% growth?

Also, what is the market share of largest bank in US, UK and China?

On one hand we need larger & stronger financial institutions to compete globally and have a strong global say & hold…while if any such caps are put, will that not be contradictory?

Lastly what stops HDFC Bank from again demerging it’s NBFC, housing finance and few other subsidiaries relevant to advances/deposits it may create in future …if the rules then demand it…just like how today the rules make a merger more preferable?

Insights/discussions welcome!

7 Likes