Does any one know what the tax implications would be if i hold HDFC shares and get bank shares. Would the tax be selling price - (purchase price * 42 / 25) ?

I don’t think there is any tax involved. No capital gains here.

HDFC Bank, HDFC merger seems to be a win-win deal

HDFC’s shareholders would get 42 shares of HDFC Bank for every 25 shares in HDFC. The merger is scheduled to take around 18 months to complete and is subject to a slew of regulatory approvals.

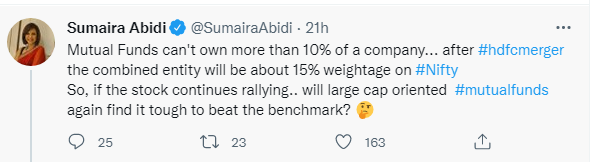

Pasting a tweet I saw

Sumaira Abidi is a well known face in MF circles

Question…will this trigger some selling? Every fund, worth the salt owns the HDFC twins and 10% limit will come into play? or am I reading it wrong?

Yes… but selling due to this 10% limit will happen only after merger is completed… they will even have around a year before merger consummation for doing that

and it would be compensated by FII buying since the the shares that hdfc owned will be cancelled.

Although, if the stock starts falling again because there are forced sellers, that would the best time to buy.

Would request senior boarders and other members to throw some light on the combined entity’s book, and what could be the possible range of how the market might value the combined entity in P/B multiples? Going forward what could be growth expectations of the combined entity?

Disc. Holding the stock.

Everything might be hard to value as now the overall book is way bigger and less diversified so it can be valued more or even less as the loan book is now more secure but also have less NIM even management also lists that so if we see these factors we may see some reduction in P/B by at least 10-15% so we can see around 3.5 times as a base case I really doubt it will fall below 3.2 after 5-6 months of merger.

If we think it over then both might grow at the same rate so we can assume around 20-22% of loan book increase in both of them if it takes around 14-16 months time right now both combined is around 12.4+5 lac cr loan book so after merger time we may see around 22-24 lac cr book at there merger.

If we look at tier 1 capital then it may be around 22% at least that is predicted by the market.

Note:-

if you are just looking at arbitrage as such a big deal with so many moving parts and also such high free float there is a very low chance of making much out of the arbitrage as the doubts of the merger and discount are so less than it’s better to look at the bigger picture then just look at the arbitrage.

What opportunity it can present is with higher loan book, deposits, and branch network they can now focus on bigger clients that may require a huge loan but due to their own policy of not giving out to much weightage to one borrower now with a sudden injection of around 40%+ in loan book this will make them way ahead of most of the other leaders and that can make the opportunity size to be even bigger and especially they can now look at even new sectors more aggressively like affordable housing where hdfc might play a role as their basic ticket size lower then hdfc bank.

I see now hdfc bank can easily focus on their main areas like personal lending ie credit cards and vehicle loans,etc and also have a booster shot to their home loan business as sbi was getting aggressive in this area but with hdfc in the picture they can have management that can easily make big leaps in there core area.

Just see the difference between hdfc bank and sbi in terms of loan to houses as a percentage of total loan this makes why hdfc might not be the best in the home loan and now can be better

I not really that senior and i am a HDFC share holder but this is how i see it

Post merger the core mcap will be 10 lakh crore. 8.5 lcr from the bank + 4.5 from hdfc - 21% (1.7 l cr) cross holding - 1.5 l cr subsidaries

And the joint profits of the bank will be 50k cr so core PE of 20

Not cheap but not expensive

I feel that the growth rates will have to come down to 15% eventually (nominal gdp + 2-3%) but i don’t see the valuations going down significantly. As the growth slows down the leverage will increase meaning lesser eps dilution and eventually higher dividend payouts which will act as a floor

Immediately there will be a cost of SLR, CRR and PSL but as the HDFC bonds mature and get replaced with CASA this will lead to a gradual profit growth over the next 7 years.

The tech spends will have to go up to integrate HDFC into the CBS and in general improve the bank’s capabilities. This will be offset by higher earnings on the excess liquidity they have as rates go up and a better growth environment in general for the next few years

But if you have the right expectations, that your investing in something that can deliver at max 13-15% CAGR + some dividends than i feel we’re in for a pleasant ride

- Not much change of large corporate governance issues

- Very likely to keep growing

- Less shocks in general

- High chances of slightly exceeding expectations

There will come a time where the bank starts to trade at premium prices and the broder markets will trade at a discount like 2017-19, that would be a good time to book profits and look for alpha.

Nicely explained.

One likely +ve surprise would be HDFC Bank’s ability to push the pedal harder on current HDFC subsidiaries - Insurance, Wealth management and Education loans. They are likely to outperform core lending biz.

There aren’t too many large caps to bet on India story with reasonable valuations. Even with moderate growth, it provides very good reward-risk combination.

Latest company presentation on merger

Going by this

If regulations permit adoption of an NOFHC structure, the banking business shall be carried out of a 100% wholly-owned subsidiary – thereby ring

fencing the banking activities in an unlisted entity regulated by the RBI

From interviews that i have seen the bank is interested in keeping the stakes in the life, amc and non life businesses, in that case a NOFHC seems like a likely option

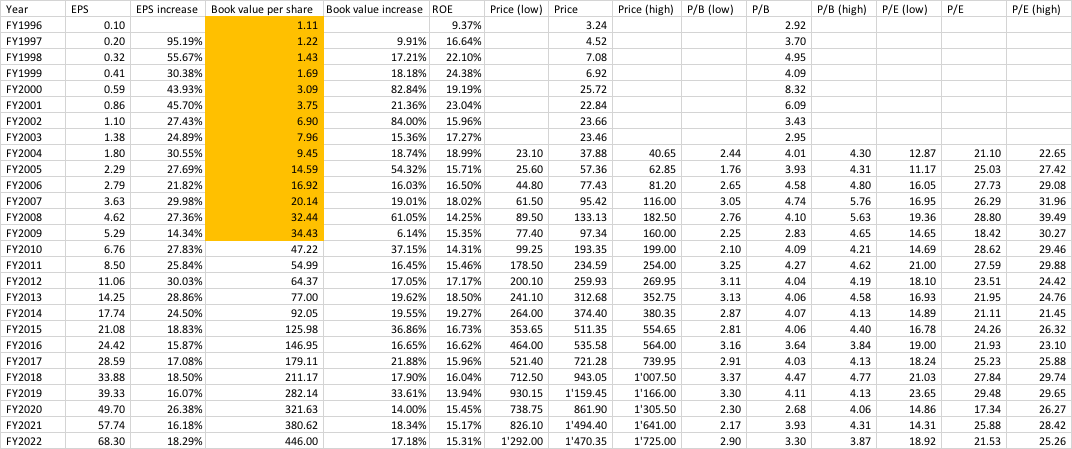

In FY22, EPS grew by 18% and book valu by 17.2%. The long term financials are summarized below.

At current stock price, trailing P/B ~ 3.28 and P/E ~ 21.45. Its a bit cheaper than same time last year, and at 10-15% discount to long term averages. What is impressive is EPS growth has kept chugging along at 15-20% over last 5-years when overall economy was relatively subdued.

Disclosure: Invested (position size here, no transactions in last 30 days)

new to hdfc bank, do they release investor presentations?

yes very small but precise.not named as presentation

Based on the results and the concall i think the results are good. An interesting thing that a lot of people are negative about is the low margin wholesale book has grown much faster than the retail book but as per the management

The cost to income on whole sale is in single digits and the credit cost it almost nill

and these are sticky longer term loans vs retail where there are higher margins but are typically much shorter tenure and the bank staff need to constantly run. My own guess is retail will organically pickup as the economy picks up but having secured longer tenure loans both on corporate and mortgage is good in the long term.

The high churn unsecured book of the bank is why i preferred investing in HDFC. I feel the bank is moving in the right direction for long term sustainable growth.

Also, it is just incredible how this bank has transformed from a pure retail bank to dipping its toes in wholesale in the early 2010’s to having 55% wholesale mix today. The next leg will be their entry into tier 2/3/4 cities. If they are successful not only will it help growth but it will also reduce the PSL costs.

I’m feeling very optimistic in the long term

plus they are expanding to Sub Urban and Rural (suru) locations. This was they are confident of doubling the book.

I live in a Tier 2/3 city in Punjab, HDFC opened a new branch recently(15-20 days back) and the new account addition rate is good.

They are adding 3-4 new accounts every day in this branch.