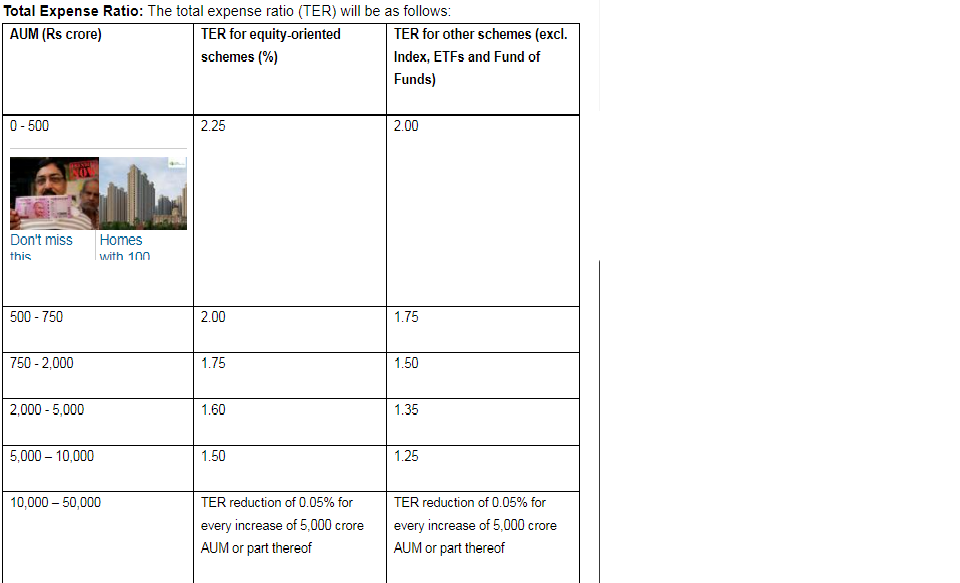

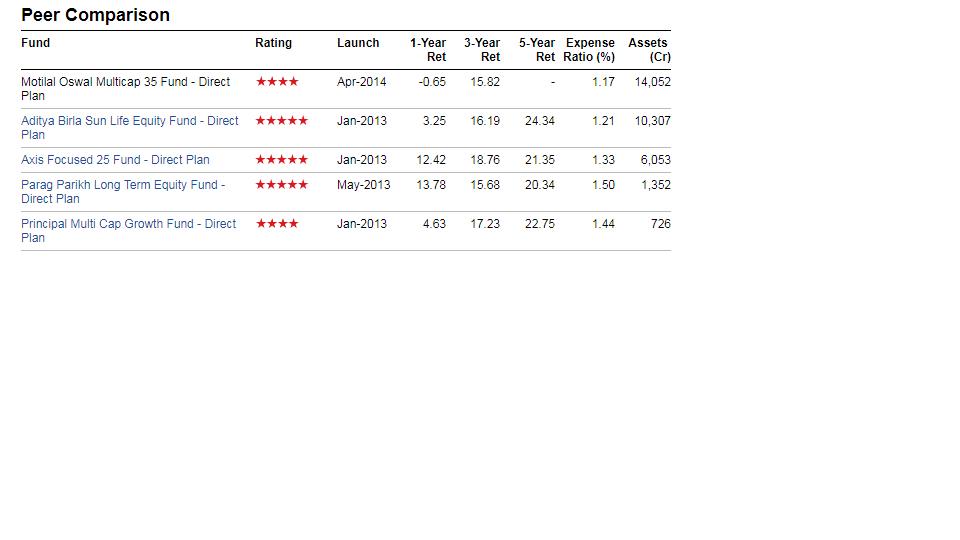

Above is SEBI’s new slab based on AUM and expense ratio of direct plans of some random schemes that I have taken from Morningstar, as you can see the ER for all the direct plans are already well below the new rates proposed by SEBI.

Mutual fund industry is a regulated business and SEBI has ensured limited competition (initially PSU, UTI then limited pvt players so on…). The drawback of this is SEBI will regulate the profits from this industry. The AMC which can differentiate from the crowd (read PMS, alternate investment funds) will win in long run. Expect more innovative products (riskier?) other than MFs going ahead or something plain vanilla (robo/quant/algo driven) so operational costs would come down drastically. Either way it is better for industry & investor in general and not end of road.

i have done a rough conservative valuation - which you can look at Valuation.xlsx (18.0 KB)

I have reached a conservative figure of Rs.1100 per share which would give you a 20% cagr return for a long time

As an equity investor, a bit disappointed that the regulation came just after IPO and not just before IPO…any thought by seniors on such news which often come after public money is invested? Thanks

3 Likes

@Investor_No_1 - This has been in the making for quite sometime. Even as recent as Aug 23rd, SEBI chairman was talking about regulating expense ratios. Please see this article (which was posted in this very thread)

Quoting from the article

Chairman Ajay Tyagi said on Thursday that capital market regulator is examining whether the high profitability of a few funds is because of the high total expense ratio — the fee that mutual funds charge investors to manage the schemes. It will also come out with a policy on close-ended schemes, he said.

“Is this concentration due to lack of adequate competition in the fund space? Are such disproportionately high profits due to high Total Expense Ratio (TERs), especially in equity funds …

This was when this scrip was trading between 1900-2000. There were adequate signs of manipulation to get rid of institutional holdings before the ruling came out. A few members including myself mentioned about expense ratios which could be regulated. In this case at least I don’t think the regulation came out of the left field. There were adequate signs. I didn’t expect it come out so soon though. I guess it was low-hanging fruit for SEBI to pick.

7 Likes

I will add that folks don’t realise that HDFC group is the ultimate insider when it comes to financial regulations in this country. It is beyond doubt that they knew this regulation coming and timed their IPO well. Now their employees timed their exit very well too. I was kind of surprised to see 1900+ on ok set of Q1 numbers.

1 Like

@zygo23554 had given advance warning of impending curbs on TER. He deserves applause for that. Those who heeded the warning and acted appropriately should be thankful to him.

About the situation now, it seems dust is settled on one part of the equation which is expense ratio. The other part of equation is how well the growth in AUM happens. If markets were to nosedive then there might be temporary hiccup in the growth curve but overall things should trend upwards over the longer term as there are a lot of people who vouch for wealth created by MFs.

As a business it has fantastic characteristics suitable for long term investment. With the recent correction and maybe some more to go it can be really interesting to look at.

24 Likes

Absolutely right. Warning signals were there and were explicitly raised in this thread. I am invested in it and my ownership bias did not let me accept that it will come so soon. Other point which is worrying now is what mentioned above in thread “… SEBI chairman spoke that he is worried about high concentration in MF industry where 4-5 players account for 70-80% of market”. Proposed TER also favors the small AUMs. This is not monopoly or duopoly…so not sure why SEBI is worried on this front.

1 Like

This is why a company like Google will not be born in India and even if it is, will not be raised to become a disproportionate giant. We will regulate the daylights out of these businesses until we normalise and stunt them to fit under our bell curves. Our socialist roots are still too strong for capitalism and open markets to thrive.

14 Likes

wrong comparison - Google is today is because of its innovation and customers as its focus. It was a disruptor and provided many services free … youtube, chrome, maps etc. In India the first motivation is to scam the customer by market dominance. Just look at HDFC AMC IPO, they wanted to provide a long term bribe to their own distributors by allotting stocks. SEBI is perfectly right to be alarmed by this kind of abuse of market dominance. Some of these bank promoted AMCs have undue advantage of captive distribution. This brings complacency as inflows are not exactly linked with performance which is not healthy for the overall market.

16 Likes

@sumi00 Valid points. Regulator should be there to stop these unethical/illegal practices and provide level playing field to all. Favoring small and putting additional constraints on Big ones actually goes against the customer. Customers are cheated by small as well as big players (more by small players actually per my experience)… it is just that big one come in news because they are envied the most. Let market dynamics decide who grows big and who remains small unless someone grows very big that it comes in CCI domain.

HDFC group stocks are valued as if they are most ethical in this country, while I don’t see any of it. They allotted shares to distributors in pre-IPO sale. I was also approached by my HDFC Securities rep to subscribe to HDFC AMC IPO. Blind disregard to any set of ethics here!!

1 Like

This I believe the regulators are already going after - this is based purely on my reading of how the regulators think and whatever limited understanding I have of how banks and AMC’s function.

Over the next few years RBI might want banks to focus on the savings and loans business than on generating third party products distribution business (MF, Insurance and the like). After the core banking wave where every single branch staff is converted into a profit center from being a service resource, the pressure on branch staff to sell all these third party financial products is huge. Banks which have traditionally been corporate lenders are focusing on generating more fee based income this way which is a segment where they have minimal skin in the game.

Walk into an large bank branch and you will see them trying to sell their AMC products, ideally they should have an open architecture (the way most wealth management firms function) but the undue advantage that AMC houses like HDFC and ICICI on this have on this aspect are just too huge. This advantage which they have historically enjoyed will most likely be curbed/restricted going forward. No idea on the timelines for this but one could safely assume this will materialize at some point of time over the next 2-5 years time.

Banking has always been a license driven business till the license grant process was made on tap recently, one can already see signs of this segment getting more democratized/open. It is a real tragedy if the bank parentage were to give undue advantage to some AMC’s as well for too long a period.

One can see the regulator directives given to some banks recently on the tenure of their CEO’s, we must get ready for more active financial regulators here on who appear happy to take on the big behemoths when needed and discipline them if needed ![]()

Disclaimer: The above post is an opinion, please read and judge accordingly

8 Likes

Currently banks are selling products of not just their group companies but also others’. One example is HDFC Bank distributes not just insurance products from HDFC LIFE but also products from other insurance companies.

Also, why should RBI / SEBI influence group company interactions. In open market, such things are perfectly fine. What regulator can do is probably set some targets for selling such products from non group companies as well. Also, such captive distribution is not done free of charge. If HDFC Bank sells insurance & mutual fund products from HDFC LIFE & HDFC AMC, they will charge them both for such activities. As HDFC Bank itself is a listed company and would want to increase their own profitability, would they really charge less for HDFC AMC to sell their products compared to charges on other company products? That would not be taken well by the shareholders of HDFC Bank.

The recent changes in TER by SEBI, does it cover only the MF part of business OR does it cover new businesses like PMS, AIF etc? If not covered, I think AMCs will not focus on more such businesses to maintain / increase profitability, where the fees are also higher

Let me give you practical scenarios -

-

The proportion of XYZ AMC products sold by XYZ bank is 50% higher compared to the next largest selling AMC with the bank - which has an equal amount of AUM as XYZ AMC. Does that sound right and normal?

-

You have a combination of upfront + trail commission paid by all AMC’s to the distributor - which say is XYZ bank again. But internally all bank officials are told that to meet their targets and qualify for whatever sales contests are running, business sourced from XYZ AMC should be at least 50% of the total business sourced

-

At the end of the FY just before closing the books, XYZ AMC decides to pay XYZ bank a one time marketing charge which is different from the commission already paid. This number for XYZ bank is way higher than what is paid to any other distributor

Globally large AMC’s like FT have been around for a very long time in India, yet struggle to cross 1,00,000 Cr in AUM. Their funds perform equally well and they pay similar commissions as well ![]()

Come to your own conclusions

6 Likes

Please see my comments below.

While it is easy to keep this discussion going, we are starting to digress from the core purpose here.

Look at it this way - the question we are trying to answer in the context of this discussion is - What is the probability of HDFC AMC further being hit by regulatory moves?

In my opinion the probability is medium to high whereas in your book it might be low to medium. I think HDFC AMC will get both by SEBI (due to further action on expense ratios at a later point of time) and RBI (if they direct banks to move all third party product business out of the branch infra into a separate entity which will be regulated as an advisory entity) while you may accord a much lower probability to that scenario.

The key point in investing is to think of all scenarios, estimate probabilities and buffer for that. So let’s estimate our probabilities, quantify the impact to the extent possible and and move on

7 Likes

I am not sure why you think it is arguing. I am merely stating my views and that is what this forum is about.

Good luck.

1 Like

All said and done, HDFC AMC cannot trade at these market cap of 30000 crores. I dont think there will be any

further pruning of expense ratio for a long time. Mutual funds may change their business model. Nothing is going to happen by this SEBI order except that it is a short term dampener. This will still trade at premium…

1 Like