Yes, possibly true. Such instances provide opportunity to buy at lower levels. My only concern is general market conditions.

1 Like

Its simple stock picking/advisory business with no capital requirements and very high return ratios, look at the sales nos and profit nos. as percentage of sales.

In the last decade from 2008 lows, we saw how people are moving towards equity…and SIP are increasing …so in future as the economy grows the people will invest in equity through MFs.

Opportunity size is huge for long term investors and HDFC is the most trusted financial brand of the country, it will trade at premium valuations whether u like it not…

1 Like

well, HDFC group is known for its business continuity, consistent growth, and focus on generating profits for its shareholders – some people may refers it as business ethics, though on the moral ethics side do do not stand the ground. There are plenty of examples of that – see how their Bank employees push you for ULIPs and Insurance plans, search how HDFC AMC settles the front running case etc.

At the same time, no other institution will be able to clear the ethical test though.

Many in the market are under the impression that post 2014 migration to equity as savings is a secular irreversible change unrelated to market direction.

However this article indicates otherwise. If there is some truth to it, AMC investors need to stay prepared for a substantial correction during prolonged market downturn.

Disc. No position in HDFC AMC. Recently created tracking position in Reliance Nippon.

1 Like

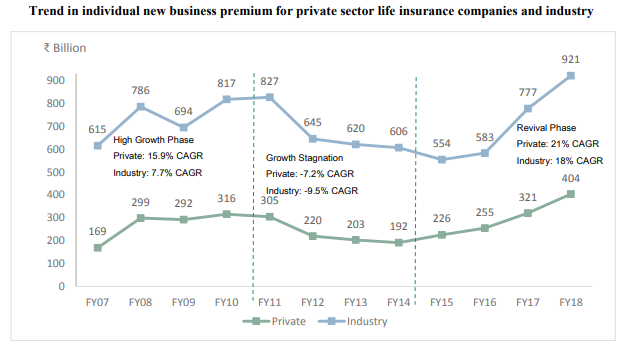

Let us see what has happened in the Life insurance industry after some regulatory interventions.

IRDAI had issued fresh guidelines on FY11 for ULIPs like minimum five years lock in, sum assured should be atleast 110% of the premium, rationalization of the charges, etc. and this is what which happened:

Source: PNB Metlife DRHP

As we see that there will be some short term (3-4 years) issues and then possibly back to normal. These days ULIPs have improved a lot as a product, thanks to IRDAI!

Now IRDAI is expected to issue fresh guidelines for traditional policies. HDFC Life’s MD was the chairperson in that committee and life insurers are themselves welcoming the changes which will make the policies attractive for customers.

I feel shareholders should be happy about all this changes which will increase the returns of the unitholders and in turn should look to invest in mutual funds.

10 Likes

Well said. When Google entered search engine market, it was the eleventh player.

Is there any possibility that low TER will lead to more inflow in MF by public and ultimately more profit to AMC ?

1 Like

Happened to BSE/NSE with STT in early 2000’s. Happened with disproportionate CTT to MCX in 2013. Happening to HDFC AMC in 2018. Really dont understand what the benefit of tinkering with free markets is???

This act by SEBI should be enough to rerate the Asset Management Industry. While the profits of AMC’s will continue to rise disproportionately as AMC’s continue to increase, the risk of constant regulation should definitely be accounted for in the valuation. Perhaps a year or 2 will pass and people will forget about it but this risk will hang over the company like a silent sword for perpetuity.

The company is in a sense a better version (a significantly better one at that) of a regulated utility. Im not saying it should be valued at 10-15 times like a utility (it still has high operating leverage and minimal capital requirement) but Im not even sure whether 40 times trailing earnings provides for enough margin of safety now. How do you account for the risk of a similar event such as this in the future in ones models? What will SEBI think is a “fair” profitability for the MF industry.

2 Likes

I think we are making too much hue and cry about SEBI intervention. Give it sometime and the dust would settle down with not too much impact in the long run… broadly I believe TER reduction would lead to 2 changes which would nullify or reduce the impact in the medium term:

-

Cost reduction at AMC - changes to be visible in next 1 to 2 years (this would reduce the impact by half)

(i) AMC would increase the % of direct plans (% has been increasing and with technlogy they can reach out to more customers)

(ii) Commissions paid to brokers and other marketing cost would be curtailed by AMCs -

Increase in revenue - Medium term increase in revenue to offset current losses (3 to 5 years)

(i) Reduction in charges would lead to mutual funds gaining more popularity with the public - larger asset pool to charge fees on (More Revenue in medium term)

(ii) more PMS & AIF structures which do not have fees restriction such as those seen in Mutual Funds

2 Likes

Quick question - i see a lot of people commenting about them moving to direct from regular plan. Could you kindly elaborate how that will help them to increase profitability? My understanding was that generally the difference between direct and regular plan is what the distributor makes? However, the net realisation for HDFC is the same in both cases for HDFC. Does the same TER cap apply for both regular and direct schemes. In that case it would be easy to reduce difference between direct and regular and cut down on distributor margins. Could someone kindly clarify?

Also, I would imagine marketing costs can be cut even today - SEBI intervention or no SEBI intervention - its just that they spend that money for a reason and simply cutting them might have its own consequences?

I agree that more PMS and AIF structures will pop up but we must remember that there are hefty minimums for both and consists of only part of the market.

Not sure however whether reduction of TER’s will really make more people jump into equity. I understand that fee reduction has only happened in equity. Would a person really jump from FD for example just because fee has been reduced by 0.42%?

1 Like

My views are based on my own experience and judgement since I have been in the distribution space for some time. So please see this post as a view and not as a fact that has to be taken in black and white

Logically what you are saying should be right but ground reality is different. A lot of schemes have a 50 bps differential between the regular and direct plans, but the commission paid out to distributors can be higher/lower than this. Hence the net realization is different for the AMC on the direct and regular plans. Large distributors generally manage to negotiate better terms for the AMC, as a rule direct plan AUM is more sticky and more profitable for the AMC since the incremental marketing/customer retention effort is not high as long as performance is good.

PMS and AIF gives the flexibility to charge higher expense ratios but these structures also mean higher distributor payouts. Upfront commissions to the extent of 4-6% are not unheard of in PMS/AIF, so the AMC is actually cash flow and profitability negative on this line of business in the first 2 years. PMS and AIF put together would probably be between 1,20,000 and 1,50,000 Cr but growing at 30%+

The average person on the street does not understand what financial products are, leave alone understanding TER and taking a call based on that. We should not be guilt of intellectualizing this too much, money will come into equity either due to a long term habit that gets ingrained into people or because the recent performance has been good. Right now we are seeing a shift in India where the weight-age given to the first factor is increasing, second factor will always be in play no matter how developed an economy becomes.

One more point that needs to be considered - as you have concentrated buying centers (for example large wealth managers and large DIY portals like icici direct, now paytm money) garnering more AUM, how will the power balance change between the OEM (AMC) and the distributor? This I think will emerge only over time, but for the time being I am tending towards the AMC economics looking better than distributor economics.

14 Likes

@Zygo - thanks for giving your insights and adding to my thoughts.

I would like to clarify that when I said reduction in TER would help in increasing the popularity of Mutual Funds - I agree with you that the average man on the street does not understand TER and would not invest in Mutual funds based on lower TER - my point was any reduction in AMC costs directly improves the returns for the end investors and this helps mutual funds to get more investors in the medium to long run (something like what happened with Ulips)

Further one more point we have been missing is that SEBI has mandated brokerage commissions to have trail fee model which means fees won’t be paid upfront (larger distributors were able to negotiate higher commissions at better payment terms and if you see Mr.Deepak Parikh’s speech in AMFI he talks about various inducements which AMCs use to lure brokers such as multiple foreign jaunts all this would now be curtailed) and this would align Mutual funds and Distributor Interest (Distributor would get paid if client sticks around) and cash flow for an AMC would be straight lined

With regards to larger mutual fund distributors like Paytm / ICICI Direct having more negotiation power - I think they are able to reach out to more customers via online medium which has a lower cost compared to other distributor models so they may be able to thrive in a lower fees model set by SEBI. Further I would like to add here that costs of AMC Direct Plans follow a J Curve - you need to spend an X amount to maintain your online presence - but that spend need not increase dramatically to reach out to more clients (the spends spread out on larger client numbers) and automatically improves profitability

1 Like

Hello all.

Everyone is saying that slab wise reduction in TER will benefit funds with smaller AUM. There is an argument contrary to this theory.

Suppose there is HDFC Top 100 Fund with large AUM and TER of 1.10% and another say Motilal Fund having small AUM and TER of 2%.

As a young, tech savvy and price conscious investor, which scheme will i choose ?

Now Motilal Fund realizes that it cannot compete with HDFC Top 100 Fund with a very high TER, so it also reduces its TER to be in line with HDFC Top 100 Fund TER. (Like Jio effect)

Will the small get bigger or the gap between the small and big get bigger.

What about all the Corporate Funds - wont they get higher incentive to shift towards larger AUM funds? I have worked in a BSE 30 company which has nearly Rs 10,000 Cr in current investments in a mixture of bonds, debt Mutual Funds and commercial paper. I can tell you from the info that I have gathered is these investments are ultra price conscious.

3 Likes

smaller funds can expend more which means they could spend on marketing, distribution, employees to attract more funds and retain more profits hopefully. Larger funds have to pass on the scale benefits to the investors so it means they would have to rely on their past performance. From investors of AMCs point of view smaller AUMs (Motilal, Edelweiss etc) make more sense than having large AUM like HDFC. THe next one to two years will be years of consolidation for large AMCs while smaller AMCs should continue to attract larger flows provided they show returns.

Corporate funds generally come via direct plans and have direct negotiation with AMC mgmt. A typical risk averse corporate will allocates funds based on existing AUM.

One question to everyone here - do MF investors look at expense ratio while choosing a fund? And I don’t mean the difference between direct and indirect plans of same MF. That’s a no brainer for any savvy investor but would you choose say HDFC over Motilal if Motilal charges higher expense? I think people look at last 1, 2, 5 and 10 year return or go by brand names rather than look at expense ratio.

As the opening post on this thread said - [quote=“Yogesh_s, post:1, topic:18943”]

Invisible Revenue - I couldn’t find a better name for this but the mutual fund customers do not even realize how much they are paying to the AMC. This is perhaps one the few industries where customers aren’t even aware of what they are paying. This is a truly win-win situation. Customers get a higher return on their investments than all other alternatives they have and AMC gets revenue without even sending a bill to the customer.

[/quote]

Yes, fair point. One category of investors would not even be aware of the expense ratios.

Now suppose both HDFC and Motilal have Fund managers of equal competence, Motilal would realise that it’s investor returns post recovery of expense ratio would be lower. They may want to retain that high charge. My personal opinion is that they would at least reduce by some amount.

I agree that in reality, for investors decision making - the competence of Fund managers matters far more.

Many times , my office colleagues asked me to suggest some good mutual funds. And most of them don’t even know how to look for the returns and on what basis one should select mutual funds and they did not have any idea like what is regular plan and what is direct plan. I have noticed this with 5-10 peoples and all were same, They are not at all concerned about expense ratios etc, Companies and sebi are trying to increase investor awareness and financial literacy but I feels more than 90% Indian population is financially illiterate.This is my personal experience.

1 Like

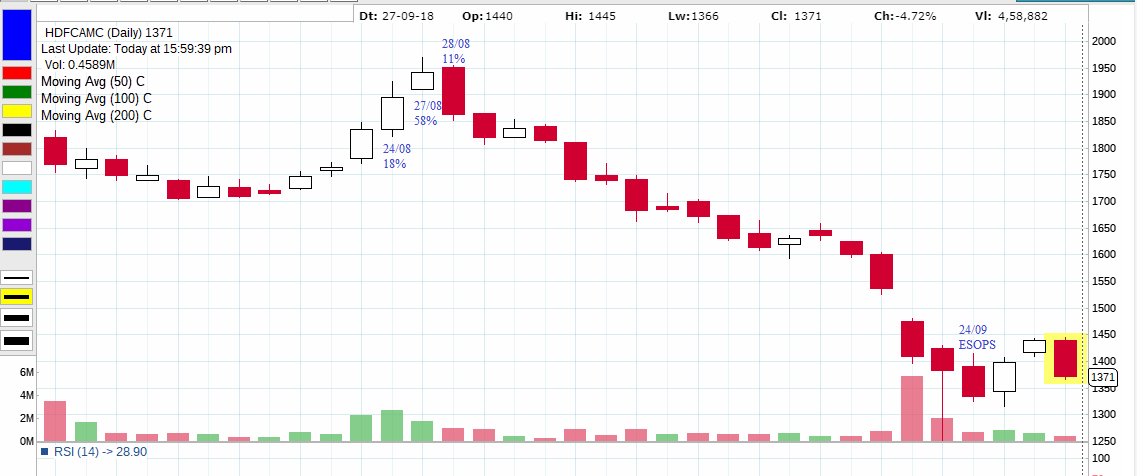

Hi

Was going through the insider trade disclosures just to recheck the sale of shares by designated persons. Roughly 6.7 lakh shares were sold in the market till 19th sep by a total of 31 guys.

Interestingly 121 odd Crores worth of shares (out of 128 crs) were sold by designated persons on 24, 27, 28 Aug which is almost 86% of the total shares sold by them. This was the peak of this stock.

Then on 24th Sep 2.8L shares have been allotted as ESOPs to 50 odd employees which is the bottom so far since listing.

Rgds

Deepak

5 Likes

Thanks @deevee, Good observation

Is it a case of corporate mis-governance.

seems like they are gaining from gullible retail individual investors.