Its a good graph showing the performance of different fund managers… However, it is also important to note that the managers managing the old funds may show better long term returns as it was generally easier to generate alpha in old times… For the last 5-6 years generating alpha has become more difficult as it is evident from the fact that most of the funds have founf it difficult to beat their benchmarks. this is specially true for large cap funds. Hence, it is a possibility that newer and their fund managers may actually be performing better than their older counterparts in recent times, for example PPFAS equity fund and its manager Rajiv Thakkar. On the other hand funds like quantum have failed to beat their benchmark on a time scale of 5-7 years… Srinivasan and Prashant Jain may be having a superior performance on a longer time scale because funds managed by them have a long history and it was easier to generate returns… That picture has changed a lot in recent times specially after introduction of fund classification system of SEBI…

Its not always about fund performance that counts. Most of the times distributors sells fund based on who would give him more income. HDFC AMC, HDFC Life has MOAT wrt huge banking networks. Similar is the case with SBI MF and SBI Life. Apart from online purchase, majority of the customers acquisition comes from banking network and distributors.

In my opinion, its the banking network that plays major role for HDFC AMC and SBI MF.

Then one also have to consider the size of the fund.

As it will be very difficult to generate alpha when the fund size increases.

These guys managing big size funds and have seen multiple market cycles and still leading.

A deep dive into Kotak Bank led me to learn about AMC businesses. In order to do so, I have extensively benefitted from this thread. Thanks to @zygo23554 for brilliant work on this story.

My notes on this story:

1- The business has few characteristics that stand out:

- Recurring Revenue

- Long Runway

- Proven Management

- Strong Financials

- High ROE

- Low Capex

- Diversified Customer Base

- Strong B/S

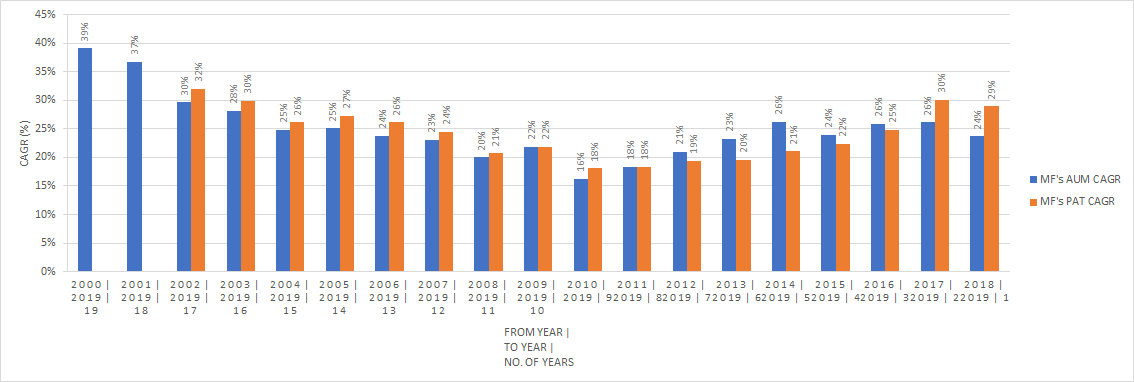

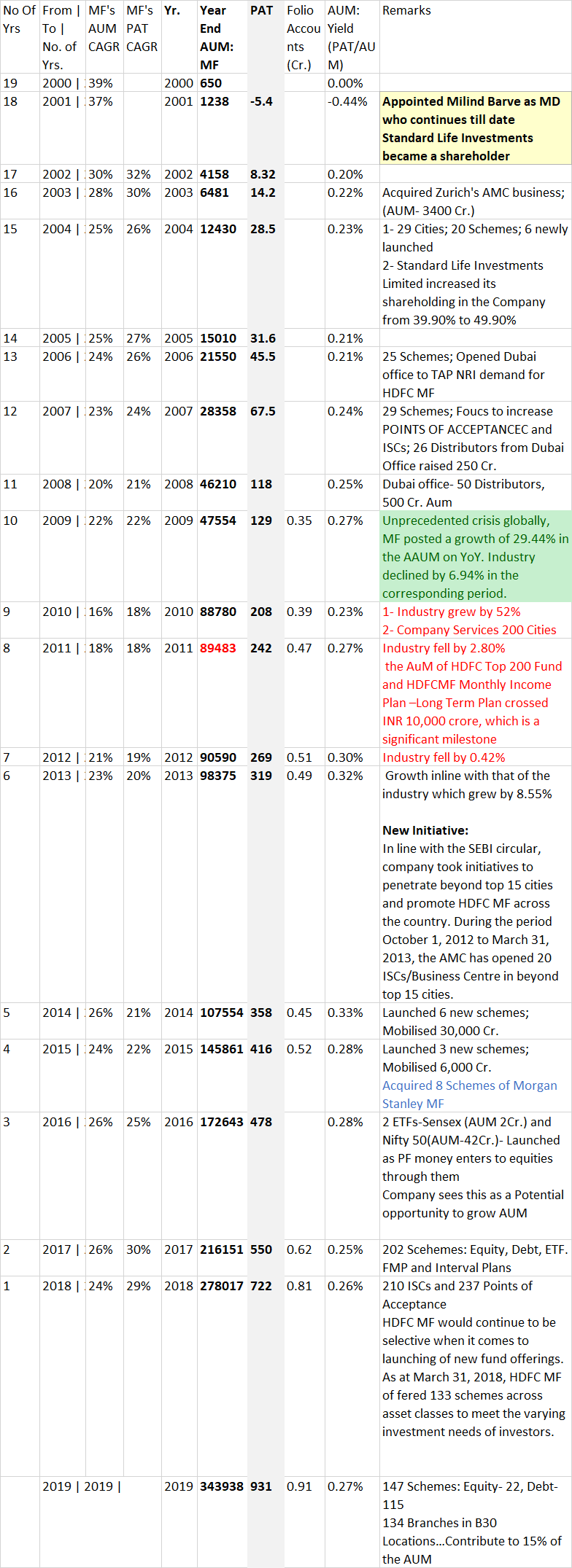

2- As evident from below snapshot, HDFC AMC knows how to grow it’s AMC and PAT as FYs keep changing. For instance, for a period of 14 Years from 2005 till 2019, it’s AUM and PAT grew by a CAGR of 25% and 27% respectively.

3- What’s the reason for such growth?

On seeing its evolution (shown in below snapshot) over the last 20 years, a few things caught my attention:

- Increasing the Network- Outlets and Cities- to engage customers

- Product Diversification

- Regular Launching of new schemes

- Financial Strength to Buyout the players who are willing to move on

- Same jockey at the helm from 2001

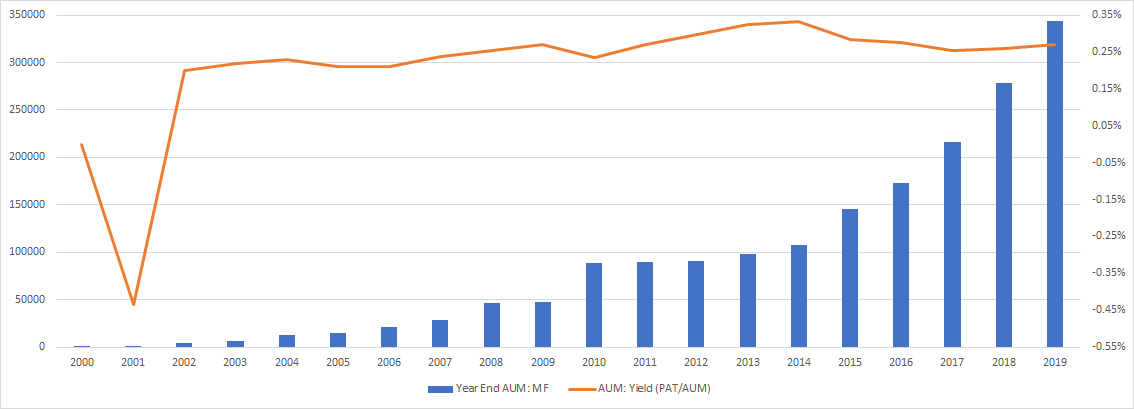

4- The yield on AUM (PAT/AUM) trends around 0.3% - shown below:

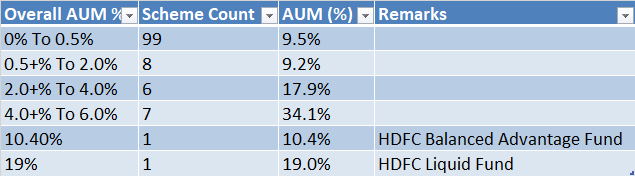

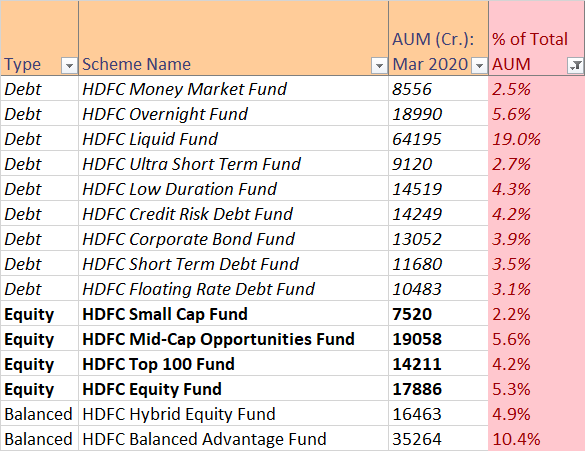

5- Although the AMC has 120+ schemes, only 15 schemes represent 80+% of the AUM .Two schemes among these 15 carry a weightage of 10 % (HDFC Balanced Advantage Fund) and 19% (HDFC Liquid Fund). Knowing their expense ratios and monitoring their progress should give a rough estimate of Revenue and PAT. Details are as below:

Few questions, if anyone can answer: Trust that @zygo23554 would share his experience:

-

What ensures customers stickiness in this business?

-

What are the differentiating factors among AMCs to incentivize the IFAs and National Distributors?

-

Having a bank as part of the group does benefit in this business as evident from the size of HDFC, ICICI, and SBI AMCs. What makes ADITYA Birla and Nippon special to be among the biggies?

Disclosure: No Investment.

In the short term, the slowing economy, job losses and pay cuts etc., will lead to lower AUMs, lesser profits and maybe even losses. But this instance may inculcate in a generation the importance of savings like nothing else.

Disclosure - Invested since Oct 18

Interesting comparison of total AMC AUM of India and US companies AUM

It shows size of opportunity

@pkk123 good data point

My arguments

We all know indian must have more unaccounted wealth in form of gold, farmlands, real-estate then your data suggest

according to your data 1% wealth shift is around 2000 billions USD which is more than enough opportunity for AMC business

Financialization of savings and unofficial to officially income is really a trend I am expecting

Thanks

-

Customer stickiness - Long term track record, perceived safety of the investment house (among investors & the distributor channel), technology & tools to keep pace with the times

-

Commissions are more or less in the same range now, one won’t see too high a difference across players. From the distributor point of view one thing matters - if he recommends a Mirae fund and it does not perform well it is on the IFA, if he recommends an HDFC AMC fund and it does not perform well it is on Prashant Jain. Distributor has a fiduciary responsibility and behaves accordingly, not much upside if the funds do well but relationship with investor goes for a toss if the funds under perform. This is probably why we still see a lot of equity allocation to HDFC AMC equity funds though the performance has been nothing great in their flagship funds since 2013

-

Aditya Birla and Reliance started business since they were assured of a bare minimum AUM from their parents. It was only in 2010 I think that there was some limitation brought up in this regard, one can see that market share of Reliance AMC fell from 2010 onward due to this limitation. Strong parentage is a huge asset in any kind of financialization business - AMC, Insurance, Broking

Disclosure: Invested for self and customers, I am a SEBI registered IA

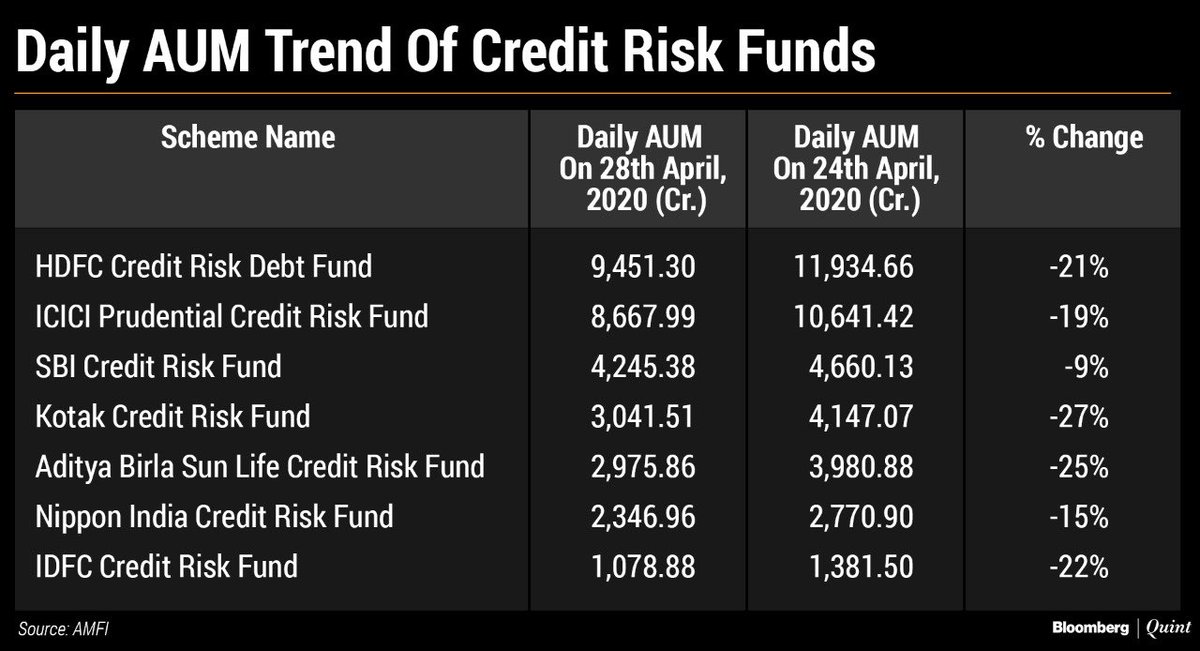

HDFC AMC is heading for tough times ahead as there major AUM was Debt and nowadays debt market is in deep trouble. Another thing that adds to problems to HDFC AMC is that its equity side has been doing very bad and none of schemes are able to make upto top 10 in past 5 year horizon. So both the above points are worrisome but HDFC has been big amount reach due to large branch network and IFA channels. Lets see how things emerge in next months

Thanks, Kedar.

How do you think about the aspect of ‘HOLD’ or ‘FOLD’ - continuing as an investor even though current valuation is not attractive for a ‘fresh’ or ‘additional’ position? How does it matter when the position was initiated as the goal is always to earn better than the opportunity cost?

In order to come in the ballpark of the current Market Cap (54,000 Cr.), expectations from reverse DCF using FCF-Equity are :

- A growth rate of 13% for the upcoming 10 years and 8.5% for the subsequent 10 years.

- Expected Exit PE of 20 after 20 Years.

- Required Rate of Return of 10%.

I drive this decision off my framework of whether something is core or tactical in my assessment. For something that fits my decision of a core holding (business quality, long growth runway, management quality etc), the length of rope I would give for periodic overvaluation is much longer. So if a core holding trades 20% above what I think is a reasonable range, that does not constitute a sell trigger for me, I can never be agile enough to buy back my entire position. I would not extend the same courtesy to a holding which is tactical in nature in my assessment, I’d be happy to take some money off the table at a 20% over valuation.

So far I have been the kind of investor who makes money due to a good buy decision more than anything else. Hence this thinking/framework is optimized for my own preferences and behavior which I’ve tracked over the past 10 years or so. For someone else who is more agile this might work differently.

As for valuation, I’ve stopped commenting publicly on what valuation is appropriate - this is what can get IA’s into soup as per the regulations. As long as the valuation methodology is consistent enough over a period of time, it does enable investors to make decisions that are in line with their investment philosophy. The worst thing one can do is to base a buy decision on a reverse DCF and then sell based on optical PE over valuation. By construct a Free Cash Flow engine will look much more expensive on a PE basis, the valuation starts to look much more reasonable in a DCF. Also which valuation methodology to use for which business is a big decision - I might use a reverse DCF for HDFC AMC but not for an Aarti Industries.

Not sure if this long rant to a simple question helped ![]()

Hi @zygo23554, I very much appreciate all your insights on AMC and Insurance business, and I am sure other members of this forum find them equally useful too.

I have one query regarding AMC profits. How do AMCs in general (or HDFC AMC in particular) utilize their retained profits. Do they invest in one of their Mutual Funds, or can invest more freely such as PMS/Private Equity where restrictions are less than Mutual Funds. Or is it that they give substantial Dividends and hence left with minuscule retained profits that this becomes immaterial.

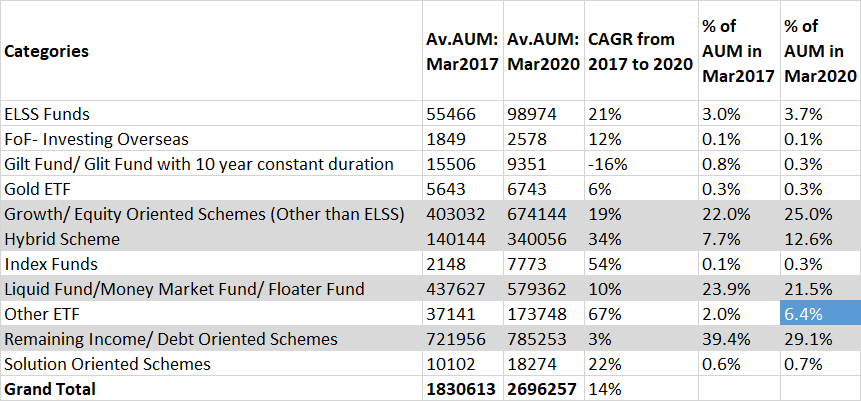

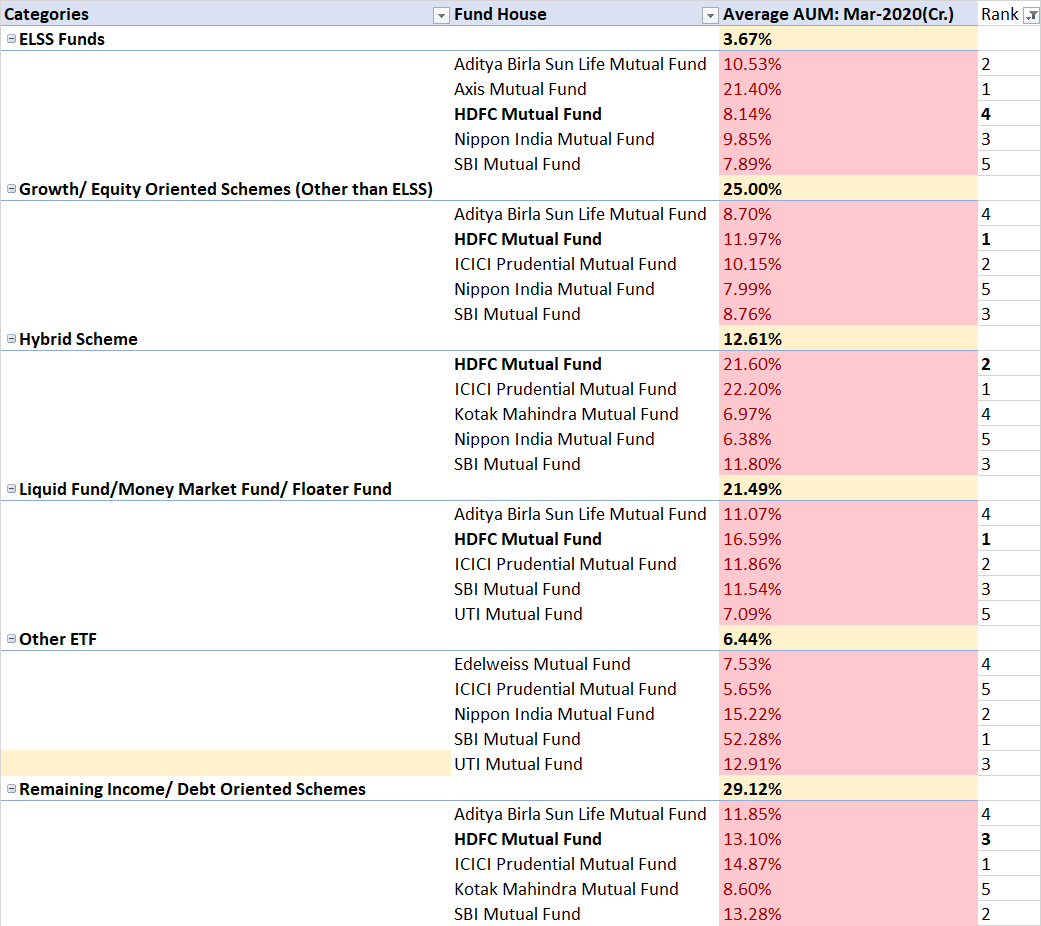

In 2017, 90% + of AAUM was under 4 major categories:

- Growth/ Equity Oriented Schemes (Other than ELSS) - 22%

- Hybrid Scheme - 7.7%

- Liquid Fund/Money Market Fund/ Floater Fund - 23.9%

- Remaining Income/ Debt Oriented Schemes - 39.4%

By 2020, the above 4 remained as the leader. However, growth in the ‘Other ETF’ category, which was small in 2017, is evident.

HDFC AMC remains either a leader or very close to the leader in most of the major categories. But, it does NOT show up on the podium in the case of the emerging category ‘Other ETF’. The same should be seen in the context that both SBI and UTI are mandated with EPFO money to invest in Equity Market only via the ETF route.

Thank for sharing

From where did you get category wise AUM break up, can you share the link please?

Source is available in this thread at:

All Asset Management companies have seen huge interest from investors,resulting in a sharp spurt in valuations. But some degree of research is also required to understand the uncertainty around sustainability of the only source of profits i.e. Expense Ratio which is a regulated metric. Imposing caps on expense ratio by the regulator only leave volume power with the companies to increase profitability. Whether, SEBI will take steps to reduce expense ratio in future, have to be seen.

Good Luck

Based on the above discussion, my learning is that leaders in the business are defined by distribution muscle and brand value. Returns are secondary factor in nature.

Q. Given the influx of new wealth management platforms like groww, paytm money etc, also conversion of brokers to fee based advisors, is the distribution muscle of hdfc AMC likely to take a hit?