On the contrary, I think the commission by HDFC AMC is amongst the lowest because of which generally distributors push other AMCs. So this may overall be beneficial.

Above is basis my understanding basis inputs from RMs of a bank. Need to validate further

Looks like HDFC AMC has come back to no.1 position by AUM. SBI’s month end AUM has come down a little MoM (as per AMFI) and HDFC AMC’s month end AUM has gone up considerably MoM (higher by 30K at the least) as per their statutory disclosures in their own website. Details should be visible in AMFI website in a few days. Liquid fund AUM has gone up well and there is a decent increase in the Equity funds AUM as well

Check the Monthly portfolio of Schemes for April. It will show the month end AUM and not average AUM I guess. You have to download the XL file and s up the AUM of all their funds.

Can someone explain how the accounting for Essel ncd works? What is the difference here in Other income & Other expense>

From Presentation-

The Company holds certain Non Convertible Debentures (NCDs) that are secured by a

pledge of listed equity shares. These NCDs are classified as financial assets at fair value

through profit and loss. Hence, any changes in their fair value on the reporting date is

reflected as a part of ‘Other Income’. In case where a fall in their value results in the

aggregate fair value of financial assets measured through profit and loss turning negative,

the aggregate amount is shown as ‘Other Expenses’.

On fair valuation of the said NCDs as at March 31, 2020, the unrealized loss recognized in

the results for the year ended March 31, 2020 stands at ₹1,203.60 mm as compared to

₹251.07 mm for the nine months ended December 31, 2019. As a result of this, the

changes in fair value of all financial assets measured through profit and loss for the year

ended March 31, 2020, in aggregate amounted to negative ₹33.95 mm which has been

shown as a component of Other Expenses. The carrying value of these NCDs as at March

31, 2020 was ₹294.21 mm. The value of the collateral as at March 31, 2020 is ₹358.78 mm.

Accounting has been done based IND-AS (indian version of IFRS) followed by all companies. HDFC AMC’s primary business is managing assets so any other business’s profits/ loss will go other income / other expenses as it not regular course of business. You can DM for more clarification on this accounting doubt

This is wrt HDFC AMC OFS and off-topic so this can be moved to another thread if required, but I believe this can help a lot of retail investors understand how OFS works to help us in the future issuances of companies.

The HDFC AMC OFS which concluded yesterday, had a floor price of Rs. 2362 with 10% shares earmarked for retail as per SEBI norms. That is 12 lac shares for retail out of 1.2 crore total on offer for sale.

I applied in the retail category and made a bid at the floor price itself 2362 (not the cut-off / market order).

The retail portion of the OFS went undersubscribed at 0.82x i.e. 9,87,191 shares bid. Now my understanding is - whomsoever bid for the OFS at >= 2362 i.e. floor price should get the allotment as the total retail portion itself is undersubscribed. However, I’ve not been given allotment because as per the NSE site, retail allotment price is Rs. 2386.1. But at that price 2386.1 or above - retail demand is much lesser than 12 lac shares (5-7 lac shares only out of the 12 lac)

So my question is - how is there a 10% reservation for retail if the retail category was undersubscribed and within that anyone who bid between 2362 and 2386 was denied the allotment?

The cut-off price for retail got decided previous day as 2386.1 (basis the general category bid, I think) which was available on NSE website yesterday.

As per SEBI rule any bid below that will be rejected - also was mentioned.

Some of the online brokerages have option where the cut-off price automatically populates to this price decided previous day.

In OFS , the first offer is given to non retail and the price is discovered on that basis .In case the demand by non retail is at higher price, the floor price gets converted to minimum discovered price for retail which may be higher than floor price. Floor price loses its relevance subsequently. Once the retail subscription is rec’d, the retail allotment price is again discovered and that price may still be higher than minimum price for retail if demand is higher than retail share.In case the demand is lower than retail allocated share, the allotment to retail would be done at minimum discovered price and balance shares are allotted to left out non retail at discovered price. A similar thing happened in D mart last ofs wherein the retail allotment price was almost 200/_ higher than non retail.For any further clarification , you could directly write to me.

Rgds

Thanks for sharing, believe he mentioned that for short term there may not be much expected but from long term there is value.

Few points to consider

There has been articles around lot of demat ac in last few months- equity as asset class is getting traction.

April, may mf equity inflows have not been disappointing, if anything resilient

AUM from March end to april end got better and June end should hopefully see same trend if indexes hold.

With inflows stable( if not growing) and cost reducing for AMC in qtr, margins should improve

With lockdown easing new SIP registration should pick some pace - looking forward to see it fully digitized

6 savings and financial discipline is visible in masses as a behavior changed due to current risk scenarios- FD might be getting a larger share now but will find ways to equity too eventually.

This is one of growth story with super long runaway, now much reasonable valuations and asset light play - linked to financialization theme. Add to it mgmt quality. See all aspects of a steady compounder.

HDFC AMC Annual Report 2020 Notes

Management Discussion & Analysis Report is a very good read on current economic situation in India and effects of Covid on economy in medium term. It also provides good insights into the current valuations of Indian equity markets and near term risks and opportunities. Mutual Fund Industry Insights highlights the growing trend of individual investor participation in the mutual funds industry. Management has repeatedly emphasised on the vast distribution network and different product offerings as the key reasons for company’s success.

Revenue from operations comprises investment management fees from the Mutual Fund and portfolio management services and advisory fees. This increased from 1,915.18 Crore in FY 18-19 to 2,003.25 Crore in FY 19-20, due to an increase in investment management fee by 3.69% from 1,895.39 Crore in FY 18-19 to 1,965.28 Crore in FY 19-20. This increase was led by an increase in the Annual Average AUM of Mutual Fund schemes. Subsequent to the regulatory change in October 2018 referred to earlier, commission and certain other expenses related to the schemes of the Mutual fund which were earlier borne by the Company are now borne in the books of the schemes of the Mutual Fund which has had some effect in reducing the investment management fee. These regulatory changes were effective only for a part of FY 18-19 but for full period of FY 19-20. Hence, the growth rate of Investment Management Fees for the FY 19-20 was more subdued than that for FY 18-19.

Fees and commission comprises primarily of commissions paid to distributors. They relate to sale of our mutual fund schemes, PMS and advisory mandates. Our Fees and Commission expenses decreased by 91.31% from 240.26 Crore in FY 18-19 to 20.89 Crore in FY 19-20, mainly on account of a decrease in commission expenses on sale of mutual fund schemes. Due to the regulatory changes mentioned above, no commission was paid by the Company on sale of mutual fund schemes from October 22, 2018 and the amounts charged relate to commissions paid to distributors on PMS and advisory mandates as well as some amortization of commissions paid in the past on sale of mutual fund schemes.

On adoption of Ind AS 116 - Leases, the expenditure on rent of premises has shifted from other expenses to depreciation on Right of Use Asset and finance cost on Lease Liability. This has resulted in reduction of rent expenses from 38.50 Crore in FY 18-19 to 0.29 Crore in FY 19-20. Taking into effect of leases Operating Margins increased from 66% to 76% yoy.

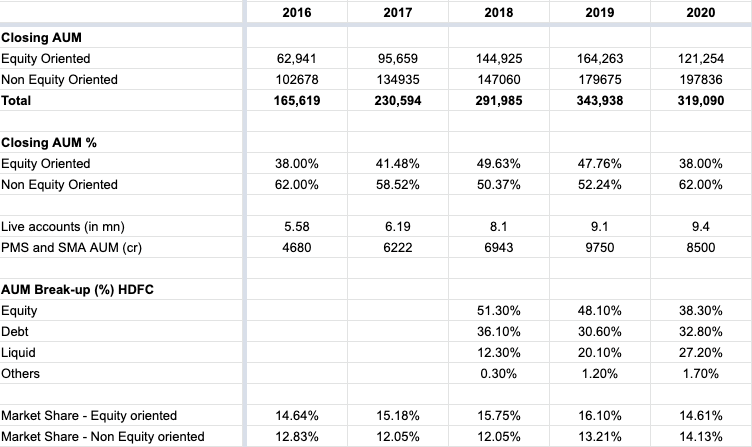

Equity-oriented schemes constituted 38% of our total AUM as of March 31, 2020.

Our fixed income schemes constituted 60% of our total AUM as of March 31, 2020.

Our investment philosophy for equity-oriented investments is based on the belief that over time stock prices reflect their intrinsic values. Our research efforts are predominantly focussed on bottom up research keeping in mind the economic outlook and macro-economic conditions. The focus of research effort is on understanding the businesses, key drivers and understanding the risks taking into account both quantitative (growth prospects, key variables, analysis of P&L statements, Balance Sheet and cash flows etc.) and qualitative (management quality, corporate governance, track record, competitive advantage, feedback from dealers, customers & experts etc.) factors.

Investments in fixed income securities are guided by our investment philosophy of Safety, Liquidity and Returns (SLR), generally in that order. Given the limited liquidity of fixed income markets in India, especially in difficult times, we believe focus on liquidity, especially in open ended schemes is of paramount importance.

Other than HDFC FMP 1100D April 2019 (1), a closed-ended fund, no new scheme was launched during the financial year.

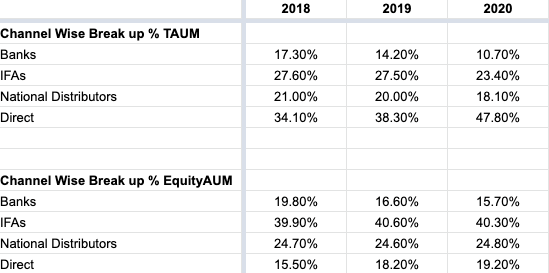

Our strong distribution reach is one of the major drivers of our growth. During the year, we continued to enhance our footprint. We constantly strive to identify and establish our presence in cities with growth potential.

Chairman’s Message

My view on the mutual fund industry’s growth story remains unchanged. I believe Covid has shed further light on the importance of household savings. Mutual funds will remain important and relevant in the savings and investment landscape. HDFC AMC is well positioned to leverage the opportunity offered by the market. Your company has nearly 20 years of investment management experience and over the years it has laid a strong foundation of diversified offerings, cutting-edge digital platforms and has built a widespread distribution network.

MD’s Message

Over the years, we have been heavily investing our resources towards building our current IT systems and digital platforms, which formed the pillars on which we continued to operate seamlessly even from remote locations.

Electronic transactions have been dominating our total transactions volume share even before the lockdown, and this has helped us to manage all our transactions through these channels.

As we continue to reopen our branches, we’ve learnt to utilise these efficient modes of communication and transaction even more, as many crises usually make systems more robust and less fragile.

Our closing AUM grew by 7% during the first three quarters from 3.44 Lakh Crore in March 2019 to 3.69 Lakh Crore in December 2019 but ended the year at ` 3.19 Lakh Crore due to the pandemic and its impact on equity markets.

Although the industry AUM, including our own, has seen a decline in the last quarter despite net positive flows into the industry, Mutual Funds continue to be the optimal savings vehicle. The last 5 years industry CAGR as of March 31, 2020 is still an impressive 15.5%, as Mutual Funds continue to penetrate the hinterlands.

Our market share remained stable at 14.3% in total AUM and 14.7% in actively managed equity-oriented AUM.

Our unique investor count stands at 56 Lakh as against the total of 2.08 Crore in the industry, so well over one out of every four mutual fund investors have invested with us.

Success Stories of year in Digitisation

Transaction volumes on our inhouse platform grew 17%.

Almost 50% of direct transactions are on inhouse digital platform and the balance is divided between physical and aggregator platforms.

Mobile-to-web ratio had increased with every third digital transaction being on mobile.

More than one new investor onboarded every two minutes on our online platform last year.

There is a lumpsum/SIP booked every minute on our platforms.

Inflows into domestic equity oriented mutual funds moderated to US$ 9.5 billion, compared to previous year (US$ 17 bn). Inflows were supported by steady Systematic Investment plans (SIPs), averaging ~US$ 1.2 billion per month during the year.

Post the fall in March 2020, Indian equity markets are trading at attractive valuations with Indian market capitalisation to GDP below 60% (based on 2022 GDP estimates) as of end-May 2020. Further, one year rolling forward price to book value of NIFTY 50 is also trading significantly below its long term average. Thus, while GDP growth is likely to be impacted significantly in near term, in view of the prevailing valuations, our medium term outlook on equities is positive.

Long Tenure SIP Book

Over 5 years: 81%

Over 10 years: 69%

Mutual Fund Industry Insights

The Mutual Fund industry’s closing AUM as of March 31, 2020 fell by 6% to 22.3 Lakh Crore as against a closing AUM of 23.8 Lakh Crore as of March 31, 2019. During this period, the equity oriented AUM fell from 10.2 Lakh Crore to 8.3 Lakh Crore while the non-equity oriented AUM grew from 13.6 Lakh Crore to 14.0 Lakh Crore. As can be seen from above, the fall in overall AUM can be attributed to the fall in equity oriented AUM, which fell by 19% due to the fall in market, primarily in the month of March 2020.

The MAAUM of individual investors in the industry has reached ` 12.9 Lakh Crore in March 2020 and has recorded a growth of 18.2% since March 2015. The number of individual folios have increased from 4.14 Crore to 8.93 Crore in this period.

The monthly SIP flows grew 2.8 times from April 2016, to ` 8,641 Crore in March 2020. The number of SIP transactions processed in March 2020 was 3.12 Crore as compared to 1.01 Crore in April 2016.

Non equity AUM increasing majorly led by Liquid schemes. Equity AUM fell majorly bcoz of market crash in march 2020. Company gaining market share in non equity segment.