In M&A world deals happen at 5-6%. Also, the AUM is underlining AUM which won’t get any new customers due to the old brand. Only growth of the portfolio… say around 7-8% is there.

So, HDFC’s customer stickiness and brand deserve a premium. Also, there is a premium for future growth (An increase in the number of customers).

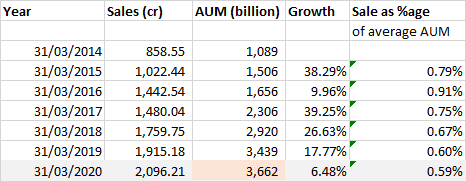

- I have assumed 13% increase in sales in H2 and around Rs 3800 Billion AUM

AUM can increase in 2 ways.

- New Customers

- Increase in value of old investments (increase in old customers money)

So, assuming an 8-9% increase in old investment value (debt is around 55%) and even with a 10-12% (9% y-o-y as per presentation) increase in new customers, I have assumed around 20% AUM growth going forward (which is again on a higher side considering recent trends).

Historically also, HDFC AMC’s AUM Growth is around 22% CAGR and net sales (excl. other income) are growing at a lesser pace. Even if we assume that there won’t be a further reduction on expenses charged to unitholders, the %age increase in the sales should be around the same as the %age increase in AUM.

With current profit/EBITDA ratios, I hardly see any swift upside in margins. The expenses won’t rise much, so the addition of say Rs 200 cr of sale, should see PAT rise by Rs 130 cr. In the overall scheme of things, this should improve the PAT margin by around 0.6% for a few years.

Now, coming to EPS, this increase in PAT margin can be ignored as ESOPs will dilute the EPS to around this extent. With a 20% increase in sales, the expected CAGR of EPS should be around 20% assuming all get well with the markets.

I am not very comfortable holding a company at PEG of 3, mcap to sales of 35 etc as the margin of safety is just not there and the margin of error is huge. I think better alternatives may be available as per one’s assumptions of growth, risk and investment horizon.

Basically I concur with zygo23554

That is one way to look at valuations. Comparative valuations look good during up-moves, but when the whole market corrects… which happens during every market cycle… only fundamentals related to your own company can give comfort.