Interview of CEO of AMFI

His industry SIP target 9000 cr per month

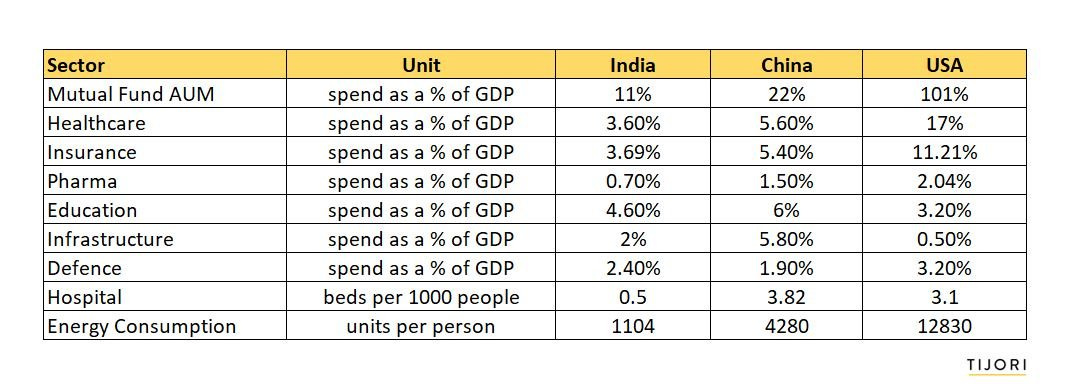

All data suggest big opportunity in MF industry

Thanks

Ashit

Interview of CEO of AMFI

His industry SIP target 9000 cr per month

All data suggest big opportunity in MF industry

Thanks

Ashit

New report of Boston consulting group and AMFI

Says , Individual Equity investor are increasing and they noted four characteristics that define the mutual fund investor base—metro, middle-aged, men and moneyed. However, it identified future industry growth in segments other than these, namely, millennials, women, people living outside big cities and those in the middle income or the “lower affluent" segment.

I think gradually financialization of savings is taking place

Thanks

Ashit

SIP in August at 8231 CR

Equity mutual funds saw the second highest level of net inflows to the tune of Rs 9,152 crore in the last 10 months.

Flow in Mutual fund really compensating FII selling More people are accepting Equity as serious class of assset for weath creation even in gloomy economic environment

Interview of CEO of AMFI says 3 lac SIP new folios are added in mouth of August

Thanks

Ashit

Fees will gradually come down with time ahead with the increase in AUM.

HDFC AMC already got around 500 Crores from ZEE / ESSEL group recently. Will they be getting the remaining amount by Sep 30?

Where do i get Equity AUM market share of all MF’s for the last 5 years?

Superb results 1HFY20 profits up 60 percent.

Since I have been posting very regularly on this thread, time for an update. I infer the following from the results of all three AMC’s

To revisit what SEBI did in October 2018 -

Effect of (2) and (3) are visible starting Q3 FY2019 and the base effect normalizes from Q3 FY20 onward. Effect of (1) is visible from Q1 FY20 onward and the base effect normalizes from Q1 FY21 onward

Which means the 50-60% increase in PAT seen across last 2 Q’s will start normalizing from Q3 onward. Q3 and Q4 will still show disproportionate PAT growth by 25-30% but from Q1 FY21 the PAT growth will depend on AUM growth and operating leverage that is inherent in the AMC business model. So if your expectation is that AUM grows at 15%, PAT might grow in the 17-20% range on a steady state basis.

It is very important to manage this pivot well as an investor, one needs to decide based on numbers and calculations rather than what stock price has done over past 1 year. Fear of Missing Out will push investors to load up at precisely the time when projections are most optimistic, do your math and decide the buy price accordingly.

I am still very excited about the business over the long term but the short term expectations now need to be managed in a calibrated manner.

Disclosure: Invested for self and customer portfolios

Agree with you but i like to highlight two points

1… this quarter tax cut advantage was around 35% it will be there and helping bottom line for long time

2…Other income … probably from there retain earnings is up 46% Q on Q and due to tax cut it will be increase and will help bottom line (some part of other income is from revaluation of NCD which is one time)

So i think this two points will be boosting bottom line

Thanks

Ashit

I have one question. What does HDFC AMC do with the Retained Earnings (after paying dividends). Do they invest back in one of their own funds or somewhere else. Thanks.

Concall highlights

The Marked Down Value of the NCDs is around Rs 27.5 Cr. The company will retain the current margin levels for the foreseeable future.

The company has seen more and more individual investors moving into direct plans. Almost 24% of gross flows are coming directly and the direct plan AUM is around 18% of the total book.

The company will maintain industry-level TERs and will not make any proactive moves to change it significantly.

The total surplus on the book has gone up 33% and thus the company was able to increase the yield on their book which led to the high other income figures.

The company is focussed on growing the retail business and continues to maintain its position as the market leader in the retail mutual funds’ space.

The share of higher-margin equity funds has gone down as the product has evolved and thus the growth in AUM is not necessarily reflected in revenue growth.

The management reiterated the market opportunity for mutual fund investment and penetration and they maintain that financial advisors shall remain important despite the rise in direct mutual fund investments.

The management believes that passive funds and ETFs have become the norm in western countries as actively managed funds have not been able to outperform passive indices while in India active managers have been able to provide superior outperformance above benchmarks. Thus passive funds are not as attractive returns wise. The cost of the currently available passive funds is also high as only the headline indices like Sensex and Nifty50 are represented and smaller and more specific benchmarks done have passive funds tracking them.

The management has maintained that investor education and financial product literacy is the primary medium for penetration and growth for the entire mutual fund industry.

For the company, the management has identified maintaining and developing SIP experience for retail customers as one of the key drivers of growth for the company. More than 79% of SIPs are of >5 years’ duration and more than 67% SIPS are of >10 years’ duration

Just to highlight a couple of points I’d covered in my VP presentation (VP Chintan Baithak Goa 2019 - Sector: Asset Management & Wealth Management) which I think are very relevant over the next 4-5 years -

The space of investment management is going to see a lot of entrepreneurship over the next few years. You will have junta like me branching out on their own and setting up boutique asset management business and on the other hand you will have the tech focused guys trying to crack the retail investing platform segment. Disruption is coming for sure but it is wealth managers who will bear the brunt initially (refer slide 23-25 in the ppt)

As tech platforms which enable direct plan investing for retail investors take off and start hitting respectable volumes, the power play will tilt more in favor of the AMC rather than the distributor, reason being investing will never be a winner takes all market either on the AMC side or on the distributor side. The inputs from HDFC AMC during the conf call indicate that retail users appear to be adopting the direct plan route more actively now

AMC disruption occurs only after the general public realizes the futility of chasing alpha and paying higher fees. This will occur only after people try out exotic strategies and realize that they don’t work in the long run, for this first the PMS and AIF bucket need to really take off (which has started). PMS & AIF are growing at 1.5X the MF growth rate since 2012, look at the growth in PMS AUM of Motilal Oswal to get a sense of this. I know some PMS players who have grown AUM by 10X between 2013 and 2019 even when the performance is just slightly better than the index

What does this mean for the investment thesis on AMC’s -

Higher proportion of direct plans means higher profitability in the long run since expense ratios right now are well below the TER cap (and can be increased whenever it is needed, see slide no 19). Direct plans also means lower customer acquisition costs - instead of distributor acquiring customers for the AMC and getting paid a % of AUM, AMC now does adverts, invests in digital channels and can spread this cost over a larger number of customers. Think how operating leverage plays out for a consumer brand, as scale goes up the advert expense does not scale in proportion hence margins trend up

All initiatives that are being taken by an AMC are either focused on increasing growth without increasing costs proportionately or to enhance customer stickiness over time through digital tools. This is what a growth mindset looks like compared to what distributors are doing (preservation mindset, cost optimization mindset). This is classical inferential reasoning based on behavioral models - more often than not we will be right when we take this approach

With the inclusion of HDFC AMC in the MSCI India index this will see some passive flows going forward.

This said, valuation is not within the comfort zone right now. I love the business but not sure I like the stock enough at CMP to be able to buy with conviction in one shot.

Disclaimer: I am a SEBI registered IA, hold this in personal portfolio and in customer portfolios. You may assume that my buy price is much lower than CMP. This only presents my views on the business and does not constitute investment advice

Just wanted to understand how does it help - getting added to the MSCI index?

And is there any other news around that we should be aware of?

The funds who follow MSCI index blindly buy in the company. Secondly, the company gets international investor’s visibility…

I don’t feel there is much upside from here (Market Cap to AUM at 20%).

aum = 366200 cr

mcap = 74,721 cr

Disc: Invested but sold out 70% position in past 2-3 weeks.

Thank you. How do we value AMC company?

The management has mentioned that they will maintain their operating margins to AUM at 0.4%. Now that the tax is at 26% approx, we can expect the net profit to be at around 0.30% of AUM.

For the HDFC brand name and management capabilities, if we give a PE of 50, then valuation of the company would be around 15% of AUM.

At the current AUM of roughly 3.8L crores, the valuation at 50 PE would come to 15% of 3.8L = 57,000 Crores , which translates to a share price of roughly 2850 rupees per share.

Additionally, as there is no real capex for this company, most of the profits will be distributed to shareholders as dividends. I would expect a FY20 full year dividend somewhere between Rs.35 to 40, which should be declared along with the next 2 quarter results.

I believe the dividend payout also has to be considered for valuing the company. Is this a fair measure of valuing the company?

Of course, we need to see how the AUM & it’s mix grows up, how the expense ratio (main income of AMC) moves down in increase to AUM etc for the future.

Good point on valuations. In fact if we consider new tax rate for full FY20, the net profits would be around 14-1500 cr. That’s around 0.4% of AUM.

Saw valuation comparison with Blackrock the other day. Blackrock makes 4 billion PAT on 3000 billion AUM. That’s 0.13% of AUM. I don’t think we can compare valuations using sole metric of Mcap / AUM and ignore all other facts.

HDFC AMC has potential to grow at 15% for long term. Have a look at current market, all such companies are trading above 50 PE. And market is valuing this one at par.

Disc - Holding since IPO