HCL appoints Siki Giunta to lead its Cloud Consulting and Offerings Strategy) continues to accelerate its #HCLCloudSmart journey; appoints Siki

Giunta to lead its Cloud Consulting and Offerings Strategy

HCL Technologies to Bring McLaren Health Care’s Digital Transformation

Vision to Life and Deliver Cost-Efficient Solutions

Noida, India, May 25, 2021 – HCL Technologies (HCL), a leading global technology company, was

selected by McLaren Health Care, a fully integrated health network committed to quality, evidencebased patient care and cost efficiency, to provide digital transformation, standup a global EMR

(Electronic Medical Record) Center of Excellence, and enable higher standards of service to members,

providers, and employees

July 2, 2021 - HCL and Fiskars Group announce a strategic partnership for Digital

Q1 FY 22 call highlights - focus on future performance

37% TCV( these are net new deals) growth YoY at $1.67B for Q1 22

Double digit rev growth of 10% they are confident in CC, rather than numerical guidance they believe TCV of new deals in every Qtr is a better color

They might be conservative on revenue growth at X but looks like they have more levers to deliver better on bottomline- probably 1.5X to 2X following are some facts/ observations

Supporting above facts are hiring plans - 14K freshers in FY21, planned 22K in FY22 - pyramiding to help margins and skill factory

Most lateral hires in Q1 are in Mode 2( digital) - higher growth areas

With 74% workforce vaccinated they are unlikely to be hit hard from disruption in future - one of the key issue in Q1 during second wave was their higher employee base in India NCR+Chennai (60% employees) were affected higher than other cities - one factor for relative low performance to peers as billing would have got affected

They have called out large deals mix of 8 in services and 4 in products- product deals are higher margins

Double digit growth for FY22 is having higher offshore components hence higher margins

On a medium term looks like their bet is paying off where product + services capabilities is helping them not only get larger deals but also synergy efficiency to create stickiness and better margins for Eng svc and Products at 25%( 30% rev) as opposed to App svc at 18% type ( 70% rev)- most of this quarter wins have 2 or more service lines

in general Demand is strong from Q3 is verticals like Life science etc but asset hevay vertical are also showing growth- hence Engg svc good performance QoQ

EU drop in QoQ revenue was acknowledged but confident of growth trajectory with regional leadership teams in place and good deal pipeline

Q4 TO Q1 flattish trend - Looks like they had a large deal win in 19-20 for $1.2B which each year has a on-site to offshore component playing out, hence some revenue loss, and skewing the revenue growth view - this is a flip side of large rebadging deals but should taper off

Bit disappointed as was keen to understand their product and platform growth plan deeper as that is a key differentiation from peer group and risky bet - however to some extent it is visible in large deal wins commentary

Services - 5%+ QoQ and 13%+ for 85% of biz( outside product & platform)

Net new bookings of $2.3B , 38% YoY growth ( highest among larger peers)

Attrition in mid range of peers.

Employee cost going up, hiring is strong 11K for this Qtr

75% dividend payout policy - 10/qtr at current run rate - close to 4% yield.

Lowlights

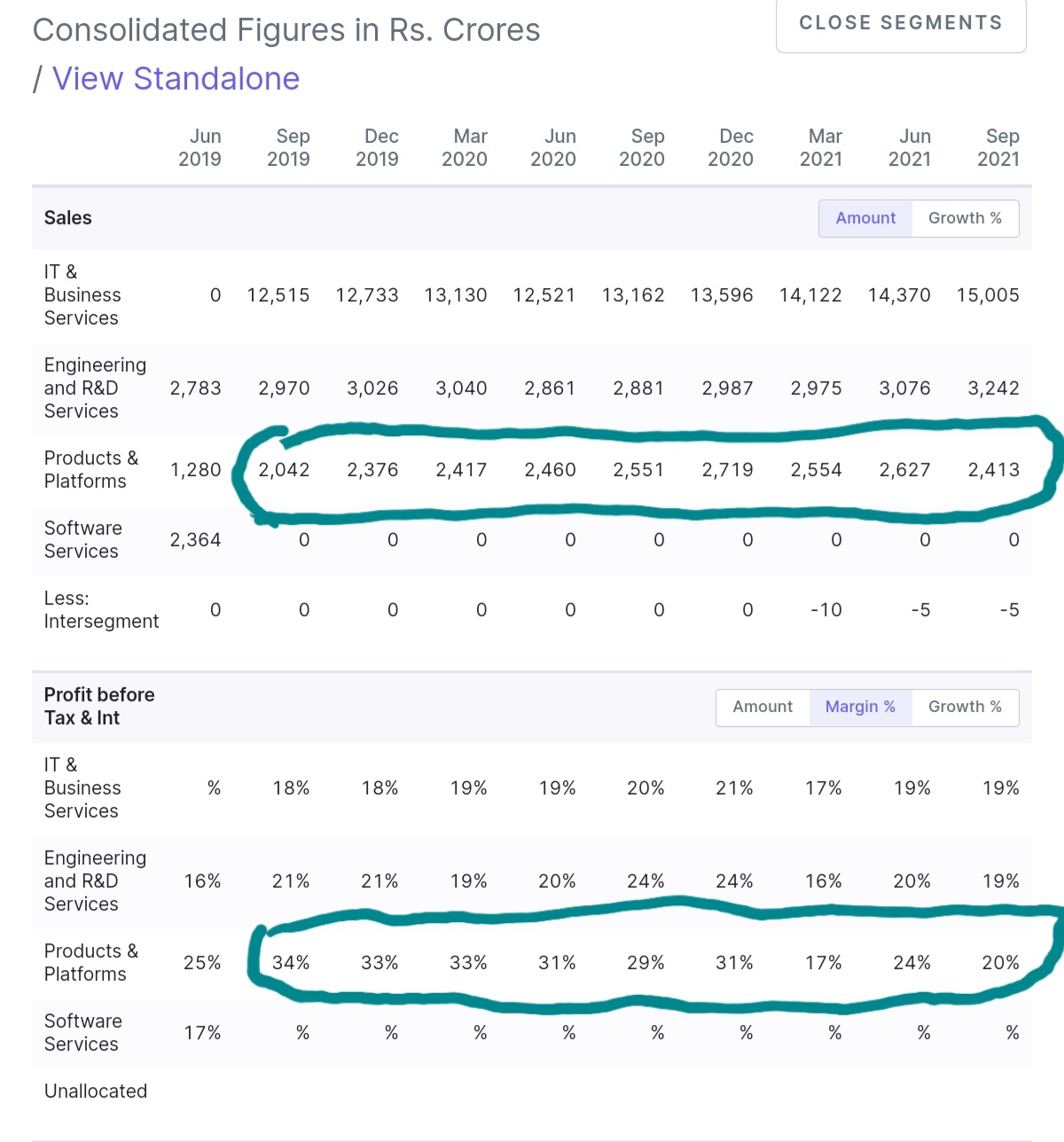

Product and Platform ( mid teen biz share) degrowth QoQ and YoY, drags performance as whole, still patchy and need to see commentary, however is a higher margin biz, Q3 is usually strongest- full year guidance lowered to flat for this biz

BFSI muted( high growth for other peers e.g. high teens for TCS) , drag by products and platforms renewal delays

HCL was first to give Bonus to larger workforce in Jan, has also come up with RSU plan for senior leaders

Given good growth numbers by larger peers and sector doing well, performance looks lagging. However consol guidance is maintained, new bookings are very strong supported by hiring , may underperform like TCS for short term.

Demand scenario is strong, they have solid new biz win, product&platforms are bit patchy but should compensate at annual levels, peers valuations discount may continue till P&P segment stabilize as more consistent - mgmt didn’t sound very confident here and lowered P&P guidance to flat for FY22.

My take is that services biz will grow inline with sector at healthy mid teen for FY 21( has done mid teen in H1), at current TTM they are at 50 EPS, given strong tailwinds for sector and demand visibility, they are well positioned for mid term for mid teen growth at consol. Midcap IT valuations are closer to FMCG and HCL at TTM EPS basis available at 25 PE. Product and Platform biz is different animal and performance is a question mark as of now though this was a differentiation investment thesis for many including self - will need to give it some more time and it may need some Org structure different from current to enable a better runs well as leadership front.

HCL vs TCS - some observations

For some reasons TCS approach to build organic IP/Solutions seems better placed and integrated to whole organizational strategy, one can see press releases for TCS and majority wins have some Solutions/IP elements, whereas when we go through HCL wins list and it seems services heavy though they have a dedicated P&P unit. If TCS were to decouple and report, they may actually outshine IMO.

Another aspect is TCS overall Employee cost have come down as revenue % per Rajesh interviews, HCL it as gone up despite doing right things - bonus, hikes etc., managing Attrition TCS beats entire industry hands down

Key monitorables

Mgmt has indicated Q3 to be strongest season for Product & Platforms- need to see if this delivers

Margins ( they are on lower band of guidance in H1)

Employee cost as % of revenues

Future capital allocation- though new policy of 75% dividend payouts limits any misadventure but at the same time shows scarcity of sound re-investment options( or sending a message to market?)

Reposting my comments on HCL FROM another thread for better context

HCL acquired legacy sunset products from IBM. The plan is to make them cloud. Native and resell them in their new version to customers

Among the acquired products is Lotus notes which is a really old mail server. They have lost some big customers on this in the recent past. I will not be surprised if this is causing the drag. My evidence on this is anecdotal.

That said they have a few other products like big fix and some security and deployment products which seem to be doing better.

Have they ever talked or been asked about demerger of products segment …any organisation restructuring vision for very long term?

Since which Q they changed this policy to 75% payout and what was it earlier? How does it compare with payout percentages of TCS, Infy, Wipro …and even midcaps like LTI, mphasis… probably that would give direction on whether dearth of opportunities is for everyone or hcl alone…also IMO 75% payout still leaves a decent amount for small/mid size acquisition…

I have an add-on question to above mentioned 75% dividend pay-out part. Why is the company not going for share buy-back like Wipro and Infy? Why are they paying dividend which is Taxable for most of the Investors?

Classic tale of Inorganic vs Organic, TCS chose Organic build up and HCL took inOrganic route - results are here for everyone to see, not judging but over long term These are Optionalities to move up the innovation curve and value chain, may not seem meaningful in short term but differentiators over long term. This is one sector where India dominance will continue for long time to come and supported by opportunity size expansion and acceleration with Covid - will continue to deliver wealth creation opportunity for investors with least risks.( not multi beggars but realistic 15%+ CAGR for long times in forseeeable future with good dividends, quality Corp governance)

I was checking on the Products basket that HCL bought from IBM and intend to reinvent them etc. Some thoughts - It is not easy to change the basic building block for particular product/platform…we cannot suddenly buy a Product from Legacy technology and reinvent itself in Digital avatar. If at all, then it will be a big project in itself, equivalent to building the product/platform from scratch…

Does HCL intend to use the existing client base for these products and mine them over next couple years which it takes to rebuild new upgrades of Legacy products into Digital?

Will those clients wait for this time period?

A small example - Lotus Notes…with Microsoft Teams (earlier Outlook)…Lotus was a lost game…reinventing and competing with such giants may take several years, if at all they can do that…Clients will certainly not wait if they have a gem of a product from the likes of Microsoft at reasonable costs…

Lotus was even used for Change management purpose (and not just communication)…now we have likes of JIRA and other SaaS products that work in fields of Team & Change management…unless HCL product basket from IBM or indigenous has such SaaS hits…the reinventing may not result in value we may expect…

Cyber security products - This again is a very specific field with specialist companies…not sure how IBM basket product fares here…

Overall, with initial checks, I see the Product turnaround to take several years (small ups and downs here and there would be there) but complete overhaul or the intention with which HCL took such a big step to buy IBM basket …the vision maybe very long term and execution as well…

Fortunately/Unfortunately for HCL…the IT world took a sharp & swift Digital turn at right very moment of this acquisition that the disruptions around may render these products and also reinventing capabilities a challenge…It also gives insights into the capabilities of top leadership to anticipate such changes and make acquisitions likevise…I maybe wrong if these products have strong Digital capabilities and I am unable to see them…

Disc: Tracking position initiated last Week. Not a buy/sell recommendation. Above views purely to understand the business and I can be completely wrong in my assessments/knowledge.

One question that I don’t understand is rather than going for rebranding legacy products which have high chances of failure why not invest in tech startups which are disrupting the existing players. companies like HCL are throwing up excess cash anyways. why not migrate to a naukri type model? please flag if the question is irrelevant

It would be good to read through AR to get a deeper perspective of HCL business segments, Employees focus, growth strategies ( Non US and Non EU), products & Platform

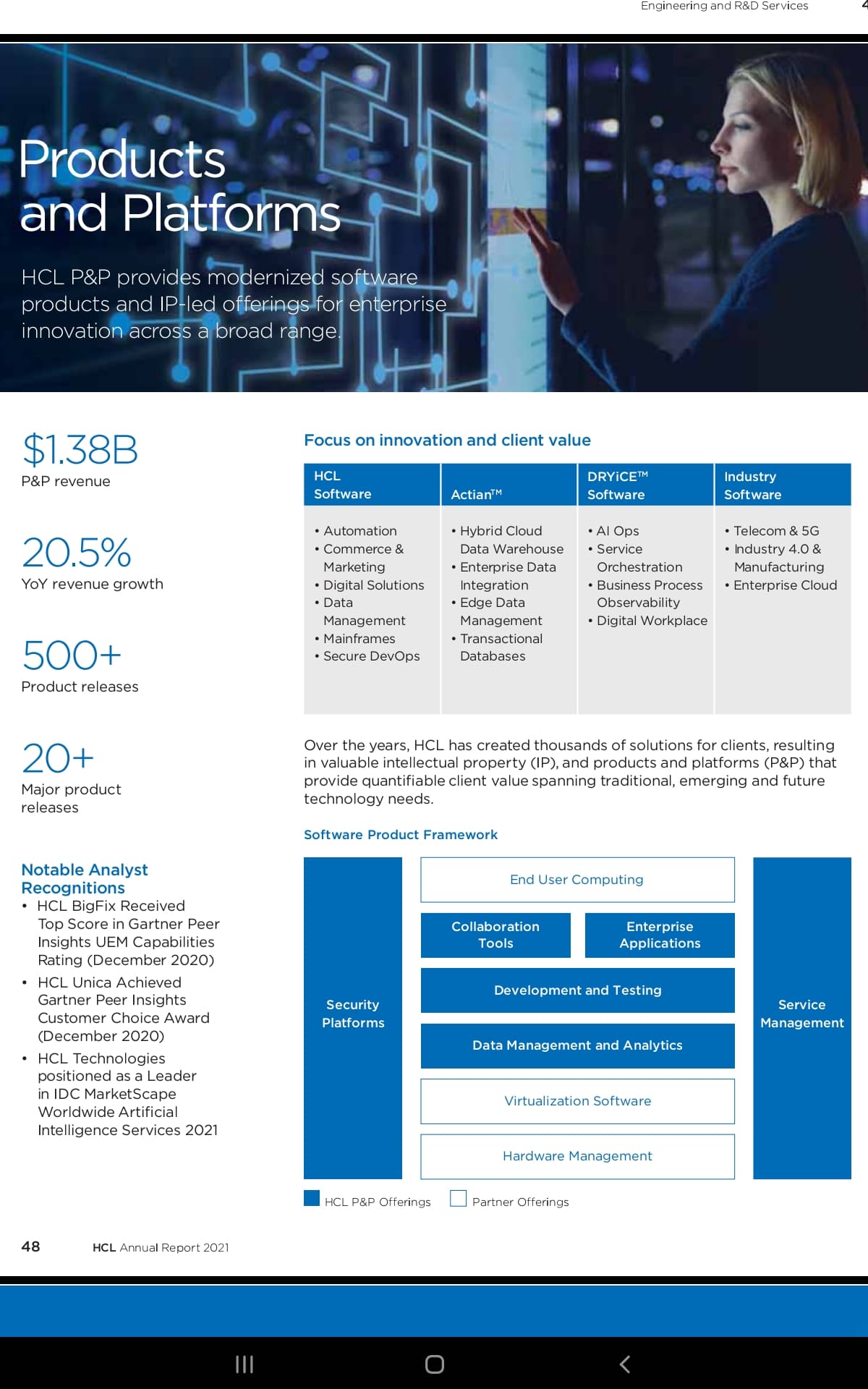

Here is summary on Products and Platform - they are quite relevant in current context, mgmt has been vocal about 25% of acquisition to be sunset and 75% being focus

On expected lines Q2 call was tilted towards P&P underperformance and as usual short term queries, some notes from same

Background - HCL has been long associated with IBM on 5 out of 7 products acquired in Mid 19, acquired them for $1.8B, idea was to win customer base, convert them into aaS offerings and ofcourse create IP and new high margins vertical which aligns to their Mode 3 offerings.

While revenues has been flattish on face value but it seems that sunset products were going down and other products were doing well to keep up - as per Q2 concall, this trend has reached towards growth curve from FY 23 onwards

Segments Margins have fallen post Corona else it was 30% margins business, understandably so as this has been the case for many product organization, again if we go by mgmt indicators on Q3 misees (on some deals delay being a blip as they moved to next Qtr )and resumption of growth from FY23 onwards - these should improve too.

If these were to revert to single digit growth trajectory and Services biz continues to deliver inline with industry trends, we can see a re rating in coming quarters- Q3 will be key as mgmt has indicated a good performance for P&P.( mgmt has emphasized seasonality in product biz hence YoY being better measurement, similar commentary from other products org like Intellect design as well)

Thanks for posting this. This helped contextualise products business current situation for me.

I had read their product portfolio in detail before I invested.

75 percent growth and 25 percent declining was known.

Covid probably accelerated the killing of declining products by customers because they were not cloud native.

Lotus notes - declining

Unica - has potential - it’s a digital campaign management tool . Depends on execution by HCL.

Big fix - secure devops- getting analyst recognitions. Probably trending upwards

HCL commerce - was higlighted as winning more customer licenses this quarter so assuming it is trended up

Couple of other products

One thing not known is the split within one time license sale and saas revenue run rate. If more saas sales are made the cost is upfront and revenue back ended.

Much needed step to get P&P on growth path, change starts with leadership , lost some precious time though

Nothing against Gentleman, he got 2 years to deliver, a legacy leader from IBM( which itself is epic of Legacy) is not your best bet when P&P has ambitions of SaaS transformation and GTM against Competetion in current digital era. Hope they pick wisely this time ideally someone with SaaS experience from new age organizations like Salesforce or Adobe etc.

Good thing for newcomer is that sunset products ( read baggage) are on their way out and his/her focus is on Products relevant to today’s digital context.

Though this would mean hiring+ settling down = atleast two quarters, anyways P&P being flat this year is factored in valuations.

This also indicates that there could be a spin off in med term if they can’t get it right next time either, it is an acknowledgement from top brass that problem exists and we will fix it one way or another. Hope it doesn’t get to it.

Any views on Q3 results? Results look flattish excluding deferred tax. Revenue growth is promising.

How is it placed in terms of valuation when we compare with TCS/Infosys? If I adjust Q4Fy21, PE comes out to be 27, where as TCS/Infosys trades at around 37PE. Dividend yield should be around 2.5% as they promised to distribute 75% of net income.

Going back to Q2 result analysis for outlook for Q3, HCL Tech has performed largely in-line on the following points. No out-performance. Given that employee cost is a key monitorable for all IT services companies so I think out-performance in its P&P division is needed for growth over peers.

Appears TCS and Infosys have relatively out-performed peers though not by much.