Find HCL tech on much awaited inflection point and Divergence from peers will be accentuated from FY 23 onwards, given their future strategy ( Demand side) and foundational blocks are now in place

- Highest QoQ revenue growth among peers, lead indicators of deal wins and hiring suggest brighter times ahead

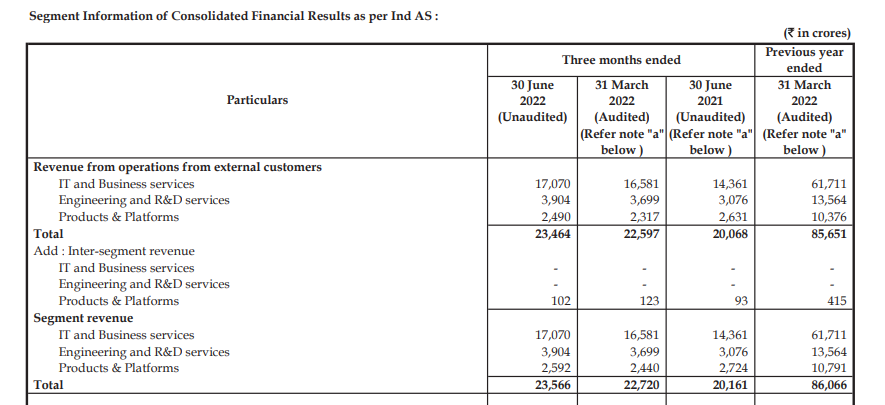

- P&P division overhang should alleviate which is also one reason of valuations discount, this division need to be seen differently from services both on revenue trend( more of YoY game) and margins trajectory ( higher end of 25%+ annual) than services. Also sunset products are pretty much out of way so no baggage, winners to drive clean performance going forward.

- Smart move to seperate ER&D and calling out focus “Futuristic” elements - mgmt presentation had Vijay kumar - AR+VR+Metaverse, silicon platforms-Semiconductors (hw and sw),industry 4.0 IoT, Med devices - remote mgmt and so on - listen Mr Vijay Kumar 21:00 onwards

- ER&D growth and margin profiles are higher than regular IT services

- Between ER&D and P&P - 35% type revenues are high margins and relatively sticky relationships and higher growth ( key strategy difference)

- Also in AR 21 - as part of Market growth strategy, focus is higher on Non US geo - results are visible as they are growing well in these geo

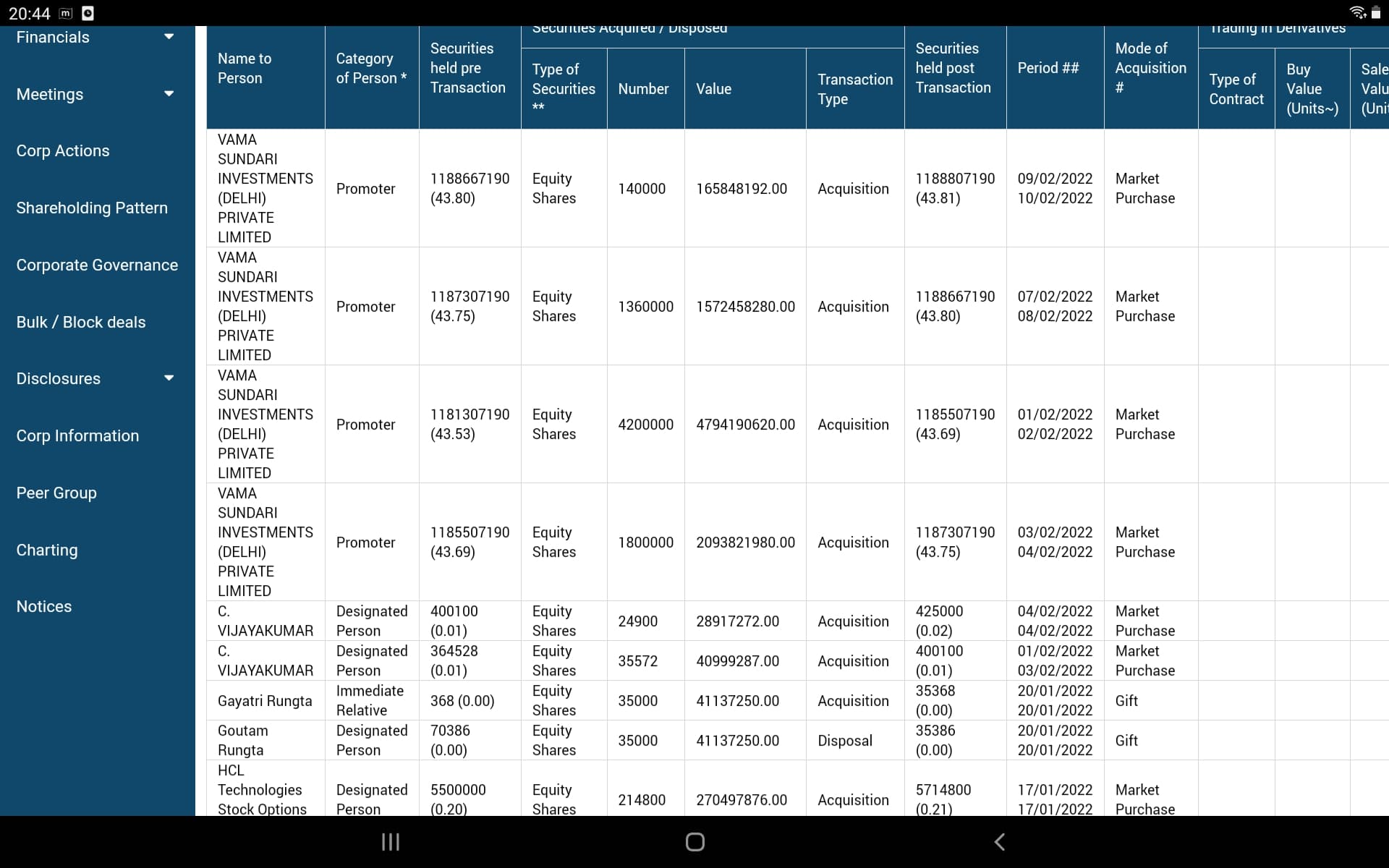

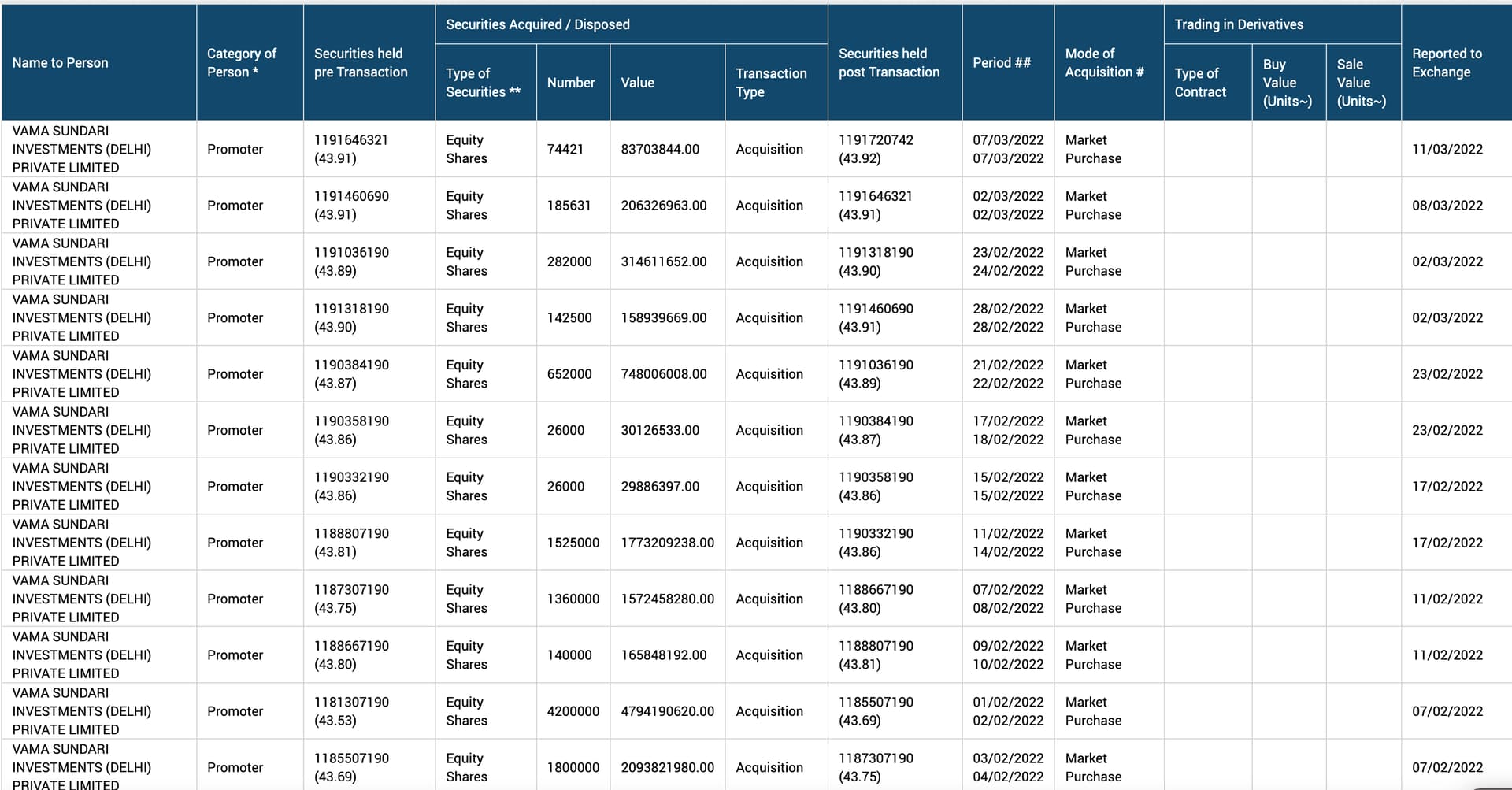

- Acquisition- selective inorganic growth continues with solid dividend payoutt( 3.5% yeild)

- Mgmt was candid about FY21 and 22 being investment heavy and hence margins on lower end of guidance - already negotiating higher pricing ( and higher T&M projects share) and fresher ratio going high should normalize it back in few quarters, Attrition is hitting them alike industry, though they are better off than most( except TCS). Happy to see them chasing growth and right investments.

All in all good quarter and FY 23 onwards see them narrowing valuations gap with TCS and Infy.

Proud to see world dominance by Indian IT services put together, middle class at scale they have built in last 20 years to indirectly drive India consumption growth, they continue to be a strong pillar of society at large and quality of employment opportunities they continue to provide to next generation at volumes that India needs.

Invested in IT as basket, HCL being Highest allocation