Promoters have bought 61 lacs from the open market…

N there is off market transaction from Kiran Nadar as well to the tune of 30K Odd…

Promoters have bought 61 lacs from the open market…

N there is off market transaction from Kiran Nadar as well to the tune of 30K Odd…

I am working for one of largest supply chain software provider and there will be major impact to service/support provider to product company like us. There will be either renegotiation of contracts or there can be termination of contract for the services we get.

I am seeing this trend with many product companies where they first try to shorten the budget by removing some dependencies.

Please factor in all these criteria when we try to invest in this counters. Problem can be bigger than highlighted above.

If a product company terminates the contract with a software service/support company,

It will be mainly in house model(if renegotiation of contract won’t work) till the business picks its pace.

Supply chain is one of the less impacted sector even during crisis. But the impact is so large in US that it forces some of the company to come up with new plan before they can think of real head count reductions.

HCL and Google Cloud Expand Partnership to Digitally

Transform Commerce

Bringing HCL Commerce to Google Cloud will enable businesses to maintain their investments in HCL’s

trusted Commerce platform while also taking advantage of the global reach, security, and elasticity of

Google Cloud

CRISIL Ratings reaffirmed for HCL

https://www.crisil.com/mnt/winshare/Ratings/RatingList/RatingDocs/HCL_Technologies_Limited_October_31_2020_RR.html

Exposure to intense competition in the IT industry ’ Company has to compete with Indian IT majors such as TCS, Infosys (rated CRISIL AAA/Stable/ A1+), Cognizant, and Wipro; and also global players such as IBM, Accenture, and DXC Technology. CRISIL believes that though HCL Technologies, with its diversified service and vertical mix along with deeper client mining, will continue to register healthy revenue growth over the medium term; albeit it will remain exposed to intense competition from its peers in the industry. CRISIL also believes that to leverage the opportunities arising in the global markets and cushion medium-term volatility, domestic IT companies will need to realign their cost structures and improve operating efficiencies and financial flexibility.

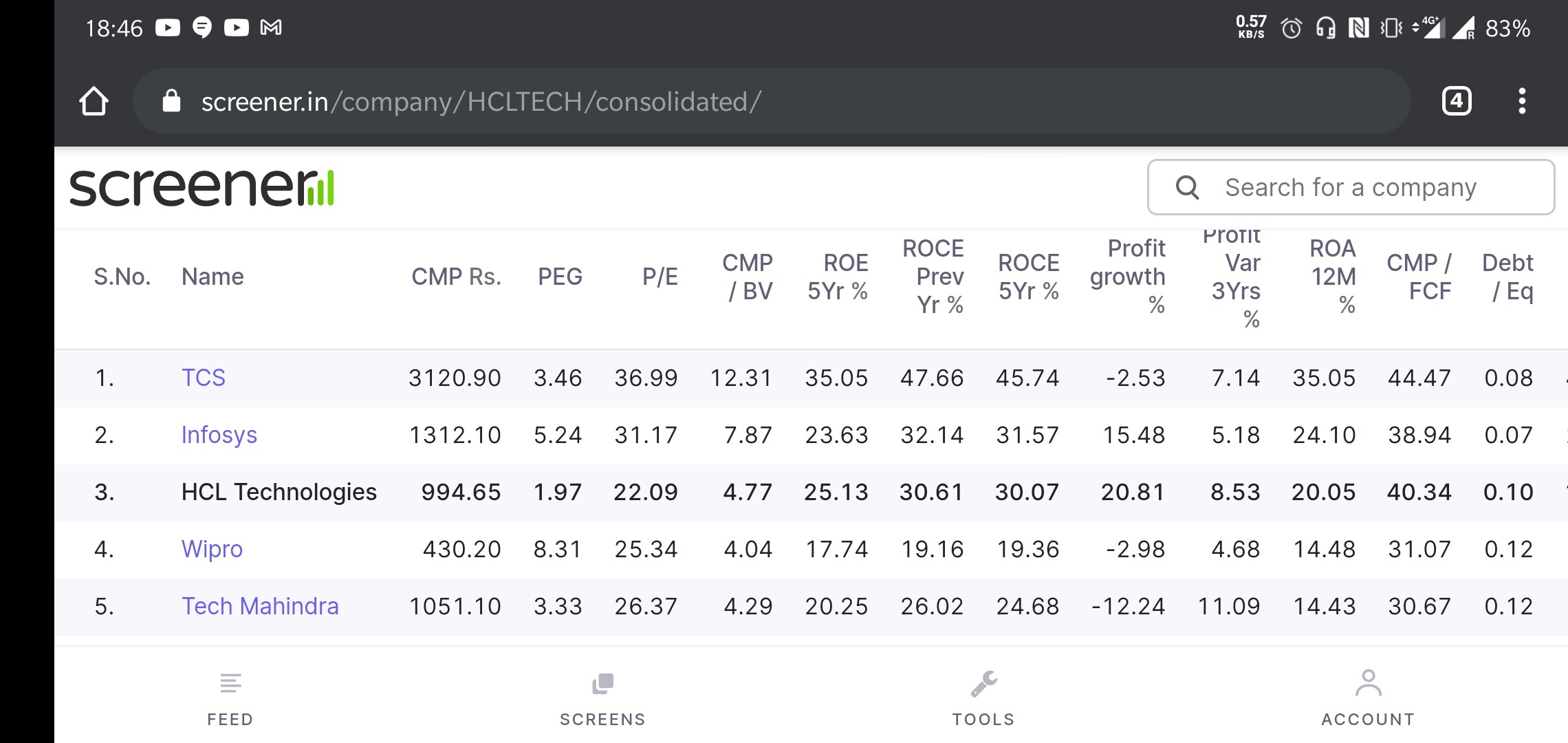

When one looks at Top 5 IT companies in India, HCL has the lowest PE ratio as well as lowest PEG ratio. Given that HCL has given highest profit and sales growth over last 5 years among big 4, it seems very odd to me. Even the margins are very close to Infy and much better than Wipro.

Is it bcoz of the IBM acquisition alone? Can someone please throw some light on this?

Hello @Sanjeev_Bansal good Question. I am invested in top 3 with highest allocation to HCL followed by Infy and TCS. I also tried to find the answer but couldn’t come across convincing one. But some thoughts…

Generally market gives higher PE to 1st and 2nd leader like banking or paint ind etc. However why HCL lags behind 4 & 5th player, don’t know. But we can take this as opportunity. Market is efficient at last and hope they may catch it soon - that’s what I think, have right to be wrong.

I myself in IT and have IT allocation more than 55% of my PF, I use various method to find efficiency of my holding IT companies. As we know HR is most important for IT companies. Hence besides general comparison I compare them per employee as well.

Below is the some statistics:

TCS: Revenue / Emp: ~ 3 Lakhs / Month &

Profit / Emp: 62000 / Month

Same for infy is 3.45 L and 69 K

Where as for HCL its 4 L and 83 K.

This is as per latest Q3 result and taken as appro for calculation purpose.

Disc: Not recommendation. Have interest hence my views are biased.

Even though i agree with your discrepancies, when we look at the Market returns HCL has outperformed rest over 10 year horizon and for rest of the term its more or less the same. With the growth and guidance they are giving for rest of the horizon we might outperform it peers. Personally i am very bullish on this stock and investing on every correction.

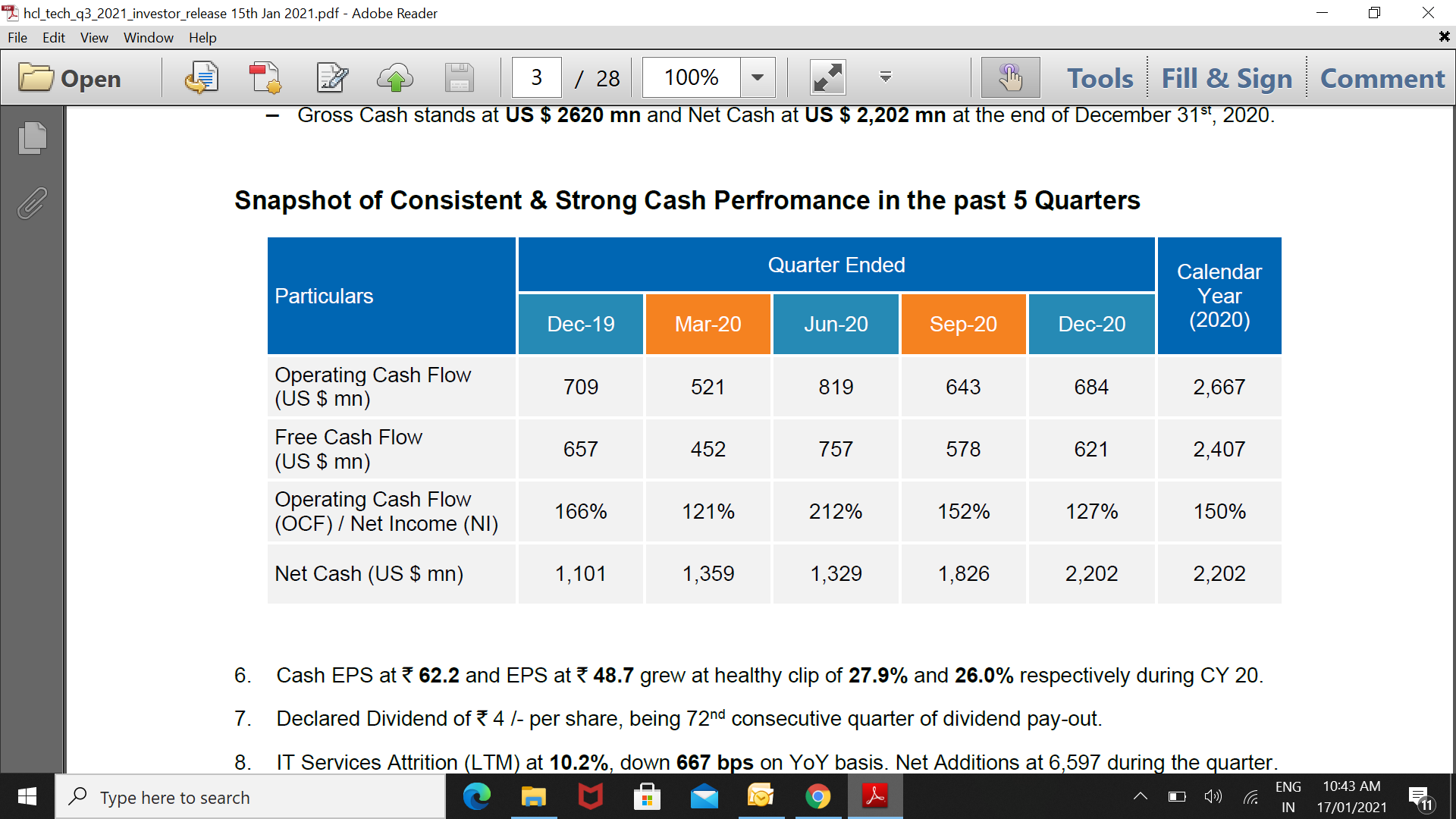

This is taken from recent Q3 result from HCL Tech.

I have question, if anyone can assist?!?..

How company consistently have higher cashflow than profit?

As in business say we calculate profit and book it in to account books. Than, as per terms of credit, we gets cash from clients. In most business cashflow will be equal or less than 100% Net Profit. If cash goes higher than profit, that means we taken advance from client, that will be equalised in coming Quarter or year.

Is this correct understanding or am I missing something?

Thanks in advance.

I guess you are missing impact of Depreciation and Amortization. It will be added back to Net income to calculate Operating Cash flow.

Whenever you acquire an asset, the impact is shown in Investing cash flow, hence Operating cash flow will always be higher compared to Net income by amount of Depreciation & Amortization (as long as you are getting paid by customer in cash as well).

HCL Tech has taken a slightly different path compared to traditional Indian IT companies which are more service oriented. HCL did a large acquisition from IBM products business a couple of years ago which the market disliked. Here are some interesting insights as to how the product business segment is performing (link):

Disclosure: Invested (position size here)

It is also dividend payout percentage. HCL shared lower percentage of profit with shareholders compared to tcs and Infosys for last 10 years.

@harsh.beria93 the 1.8 billion payout to ibm was supposed to be done over a time period. Any idea if it has been completed or some of it is still due in coming quarters ?

HCL Technologies Ltd. Concall Update

Revenue expected to grow in double digits in constant currency for FY’22. EBIT margin expected to be between 19.0% and 21.0% for FY’22. Management has indicated that around 100 bps of margin impact in FY22 will be on account of investment in new geography. The consensus EBIT margin expectation in FY22 21.2% as such will see some downgrade in earning or around 3-5%

• TCV is Strong -New Deal TCV hit an all-time high this quarter at US $ 3.1 B, increasing 49% YoY. For FY’21, New Deal TCV are US $ 7.3 B, which is 18% increase over FY’20

• CC QoQ came at 2.5% Dollar revenue came at $ 2695.9 Mn,(3% QoQ, 6% YoY)

• EBITDA Margin dipped by 224 bps QoQ and came at 25.9% which was impacted by Wage hike by (60)bps, Seasonal decline in revenue in BMp by (73 bps)Large no of fresher hiring by (61) bps and Forex by (21) bps

• Plans to hire 15000 entry level over the year in FY22

• On segmental front,

• IT and business Services – Grew by 5.2% QoQ. Going ahead this segment is Expected to have Strong growth with good demand from digital transformation deals

• Engineering and R&D Services – Grew by 0.4% QoQ. The growth impacted by covid in auto and aerospace. Going ahead , this segment is expected to Low single digit

• Products and platform -75% of this segment is expected to have got strong double digit growth in medium term . Remaining 25% is expected to have more of a sustain growth

• Adj. PAT came at Rs. 2962 Cr excluding bonus to employees of Rs.575cr.

Adjusted HCL’s EPS (excluding employee onetime bonus plan) is 47.9Rs in the fiscal year 2020-21.

I wonder why the company is trading with lower than 20 P/E compared with other competitors like TCS (~34 P/E), Infosys (~29 P/E), and Wipro (~26 P/E)?

(Top IT firms faced a drought of new clients in FY21 - The Hindu BusinessLine

hcl tech will have a major impact going forward…huge reduction in new client additions …very thankful for your ideas and comments …

This is the effect of pandemic and same is there in their revenue of FY 20-21.

However going forward the deal pipeline is strong. They are hiring more resources; Armed with big-ticket deals, IT majors report strong hiring in FY21 - The Hindu BusinessLine

For next couple of yrs the fight will be on hiring and maintaining resources. I run IT company and can see the effect in local hiring - candidate gets offer of 1.5 times plus of standard salary.