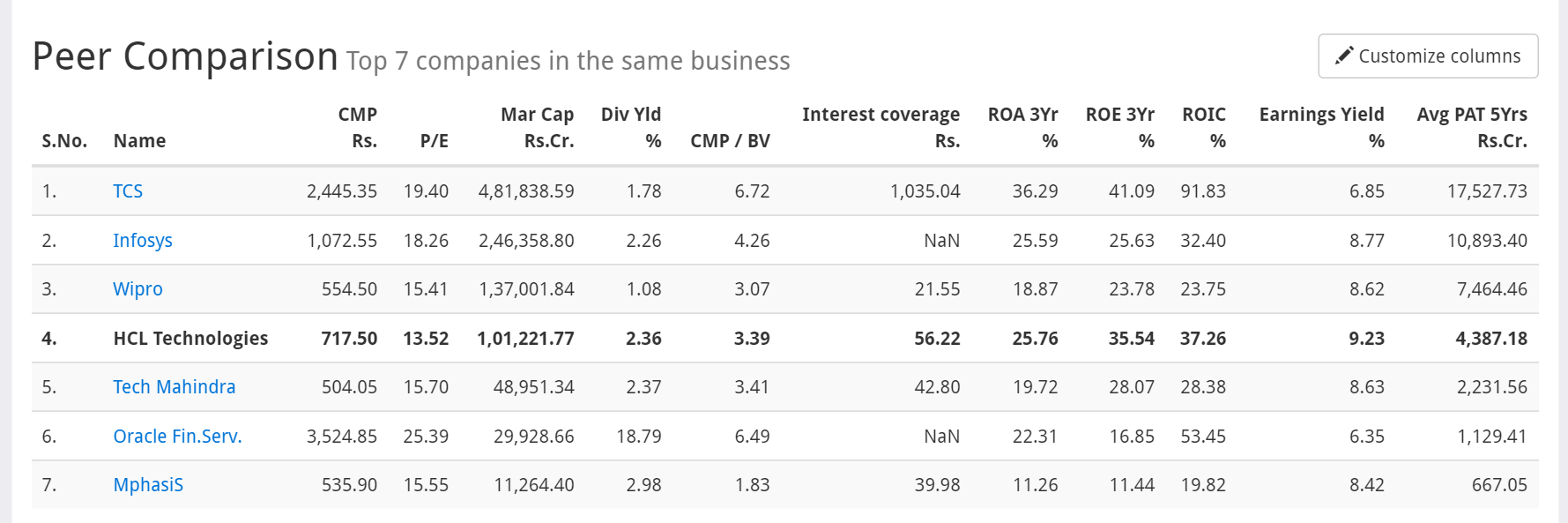

Want your views on HCL Tech. It’s trailing around its 52 weeks low and also it valued at low as compared to its peers. You can have a look to image below from Screener:

@aashish2137

It’s at its 52 weeks low due to low EBIT margins in recent quarters.

And don’t know whether it will fade away but its valuation is low as compared to others and also the merger will boost the profit.

All are estimations.

@Sowmay … I do not see any positive trigger in the near term for HCLTech or Indian IT sector as whole. It is trading at historical low valuations and can give a technical bounce but that is it. IT spending is reducing and generic IT service companies focusing on typical AMS type of work (which means all of Indian IT biggies) will face more pressure. They have grown big now so adapting to new technologies is not going to be easy and there is no clear direction emerging from any of these companies. US elections are near and that also may hurt sentiments negatively for Indian IT companies. Overall do not see good signs for coming few qtr.

Still as per my opinion, directly investing in HCL tech would not be a good decision. I heard many technical analysts that it may fall down more in coming 2-3 quarter.

Instead, it would be great to buy Geometrics. HCL tech merging with geometrics and every 43 shares of geo. will be equal to 10 HCL tech shares.

There an artibutory situation available. Read this thread to get more of their merger - HCL and Geometric merger. Can someone Please point out the Pros and Cons

But still, I’m worried about if the Price of HCL Tech will fall more or not? And I’m thinking to transfer all of my funds from HCL Tech to Geometric, Is it a great move?

Not only low EBIT margins @Sowmay…

IT Sheen has been fading away due to recent quarterly results showing lackluster growth …

Is Industry itself under presurre? main question is that…

Only thing which is acting positive is USD-INR rate… right now…

I’m surprised how people are engaging in a constructive discussion on this thread given that the opening post doesn’t fulfill the Valuepickr requirements for a company specific discussion.

Putting a screener screenshot and then mentioning the below is hardly the kind of information required to analyse the business prospects in any depth.

And then the title of the thread is asking for stock specific advice on buy/sell.

@Sowmay Request you to please go through the ValuePickr Forum guidelines before initiating a thread.

When we look at IT we should look at global majors including Accenture and Capgemini of the world.

Most companies trade at 15-20 multiples.

Proportion of software continues to increase in our lives. Amazing amount of software goes into even our cars/mobiles and so on. There will be occasional disruptions and Indian biggies have shown that they can evolve with times. Google and read “Software is eating the world”

Growth in software is < 5% but Indian companies have grown faster. They continue to take the market share away from others. They have continued to do so every year, every Q for last 30 odd years they have been around. These value migration is unstoppable.

Even Buffet has started appreciating software as a service rather than technology.

We don’t want to pay a premium for rosy consensus.

6 months back people had declared that Pharma is dead. Look at Biocon results today.

Switching from HCL to Geometric is good arbitrage. I have done that already

Behavior finance - we have all reasons to justify crowd momentum! Now crowd is focusing on MFI and we have all reason to justify historically PE as reasonable in spite of its inherent risk!

Strong company having robust cash flow, visible growth story, proven track record when bitten by crowd inappropriate justification, that’s right time to buy!

Before few months all were negative about Pharma and now again they are bullish!

Disc- invested in HCL Tech and adding 250 on every 50 rs drop in price!

Before starting the thread, I customized the ratios on screener to get the whole overview in short and then took that screenshot. Default ratios are some others.

Also, I assume the blog-post was enough to get everything you need to know.

You are right., we have all reasons to justify crowd momentum.

For some, this can be a a classic contrarian investment to make. But one has to be cautious, as a slide forever cannot be a contrarian pick.

I almost agree with you on almost all points such as “Strong company having robust cash flow, proven track record”., but only with an exception of “Visible growth story”.

Can you please tell me whats your idea of a visible growth story here ?

Right now the whole IT industry is on the verge of a major transformation wrt automation and cheaper infrastructure. This applies not only to service companies like Infosys, HCl etc. But also to major IT product vendors. The companies that adapt the quickest to the transformation will emerge stronger than earlier.

However at this stage it is too early to predict this as most of the new trends are in nascent stage of technology and the direction is not very clear. The story will play out in the next 1-2 years where in a close watch needs to be kept on individual companies.

Being in a senior position in one of the IT companies I can see that these topics are discussed daily since last 1 year.

Hence my strategy wrt IT stocks is to keep a close watch and enter only when I see a major shift in strategies.

@mukesh_gt Can you please post link which give complete report of CS, I would like to review on what parameters HCL Tech is better choice than its peers.

Disc- Invested in HCL Tech at 710 and would like add more on dips