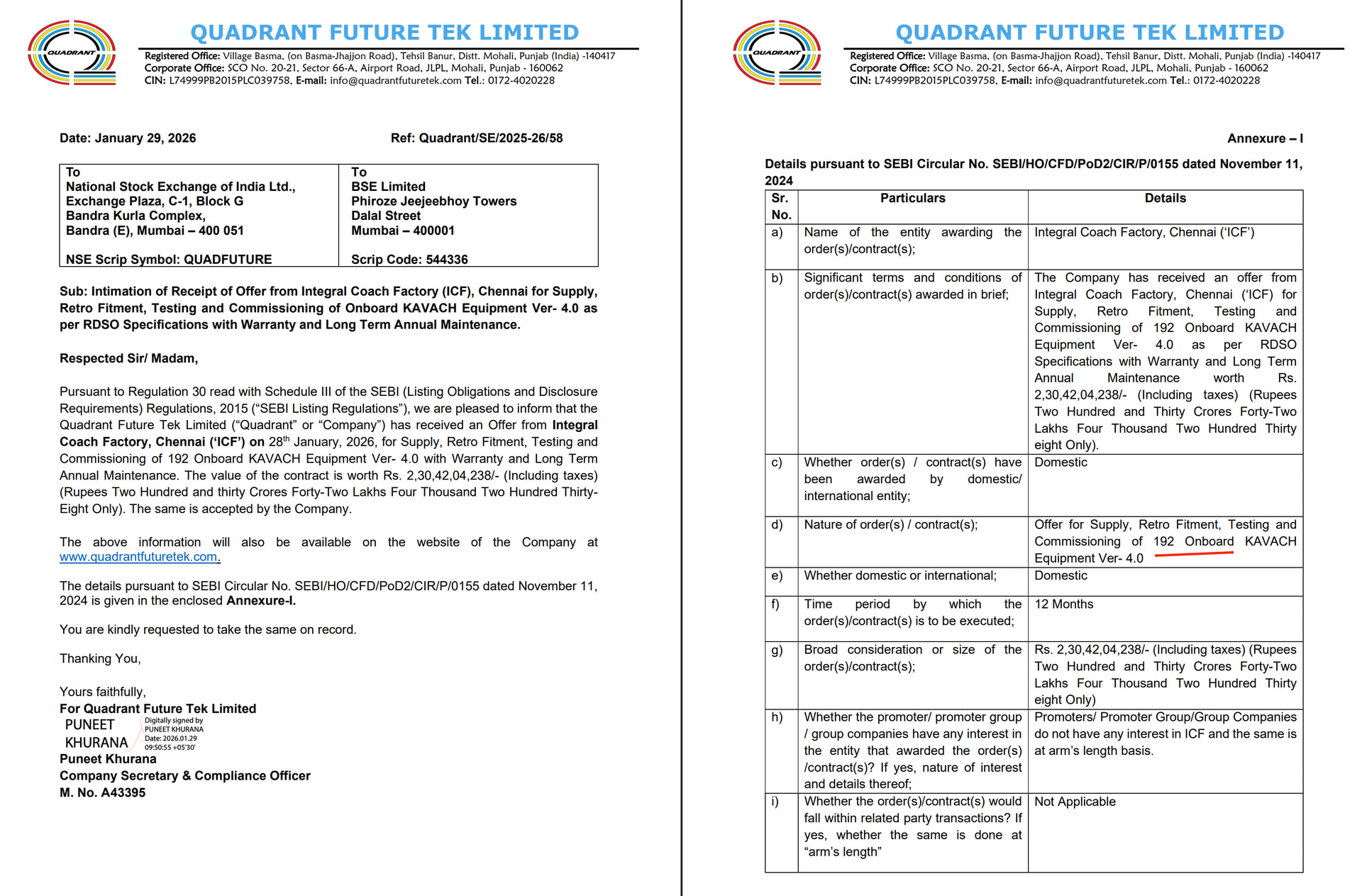

Quadrant gets ICF order but at very high rate of 1.2 Crore per unit.

9 Likes

Brilliant detail research by you ,thanks for sharing .Your finding and response to earlier post shows your detail orientation and profound insights you have on the subject matter .

Any insights on the opportunity size & margin ?Any insights which would be bigger market between 23mm/40mm/70mm/155 mm in India ? In fight with Pakistan recently which ones played a bigger role ?

6 Likes

155mm is distinct (from other lower calibre shells which are air defence ammunition, used in bursts, largely dumb) as they’re bigger, more lethal, have multiple options (effect on Target/attack the target as in laser guidance, loiter capable ) which make the fuze complex in tech terms.

155mm Guns are mainstay of long range artillery, hence their inventory and ammunition requirement is highest……and there seems to be a shortage of shells worldwide, lots of stocking/reserves build up is also anticipated

4 Likes

Yes, the per-unit rate is on the higher side, even after GST is included in the value.

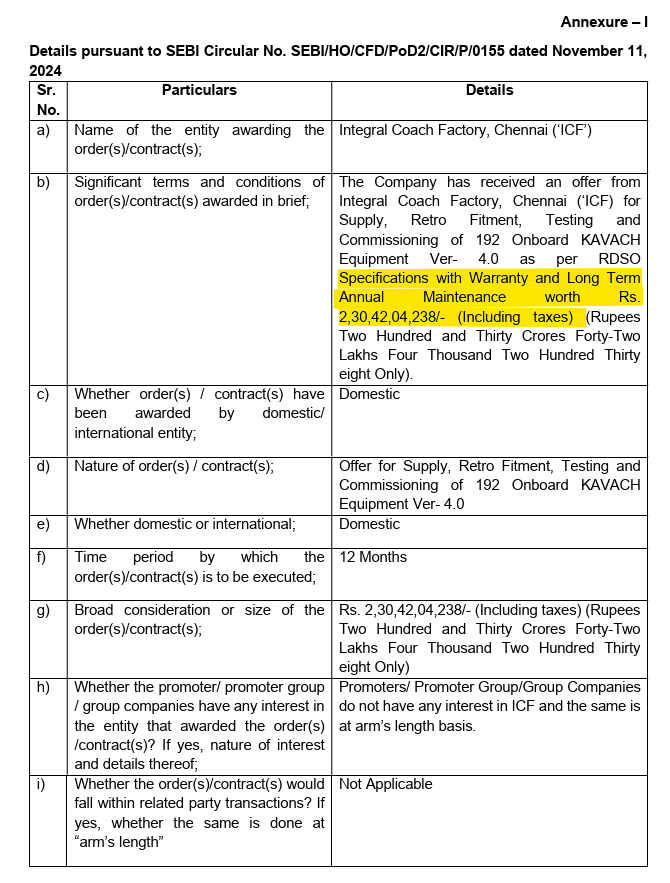

The ICF tender mentioned “retrofitment of Kavach in EMU/MEMU” which is technically different from the design of conventional locos. So some price variation is expected, however, a variance of this magnitude (~₹40 lakhs per unit) was not expected. It is possible that the final order value includes annual CAMC charges, which was mentioned in the tender document.

I think once HBL receives the order, which I think is very likely this time, the pricing will become clearer and more transparent.

4 Likes

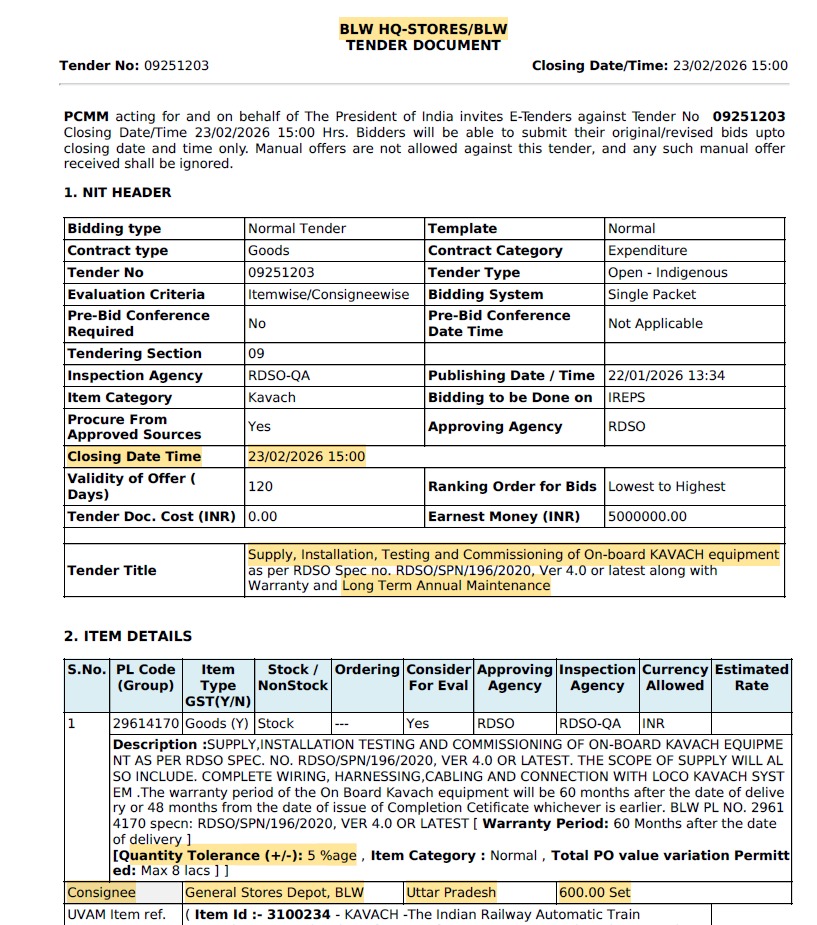

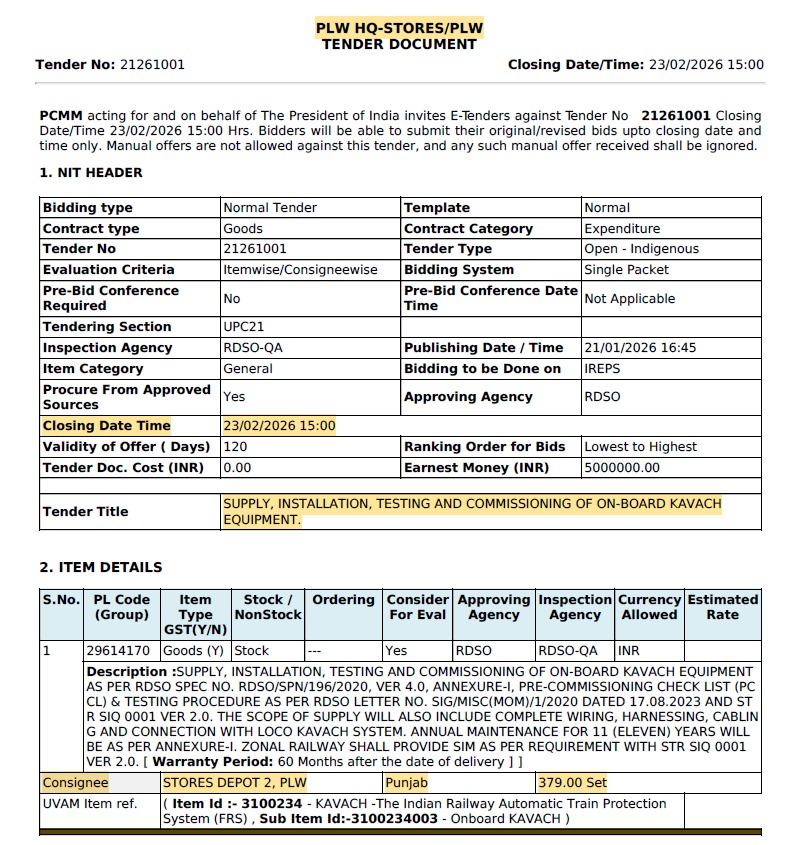

Kavach TAM update: Two new tenders floated by Railways (BLW & PLW)

Two fresh loco Kavach tenders have been floated recently:

- BLW tender: 600 loco units, ~₹480 crore

- PLW tender: 306 loco units, ~₹244 crore

(assuming a per-unit rate of ~₹0.80 crore for both)

While the individual tender sizes are smaller this time, at an aggregate level a meaningful incremental TAM is now visible.

In addition, two large tenders are yet to be fully finalised:

ICF: 2,400 sets Quadrant has already received an order, further allocations shall follow

BLW: 2,679 sets

Also, the backlog of ~7,000 loco units from the 2024 CLW order is yet to be retendered (I searched IREPS website and found no such tender from CLW).

Screenshots of the newly floated tenders are attached herewith.

10 Likes

GG tronics (CG Power company) wins order for 434 CR from CLW

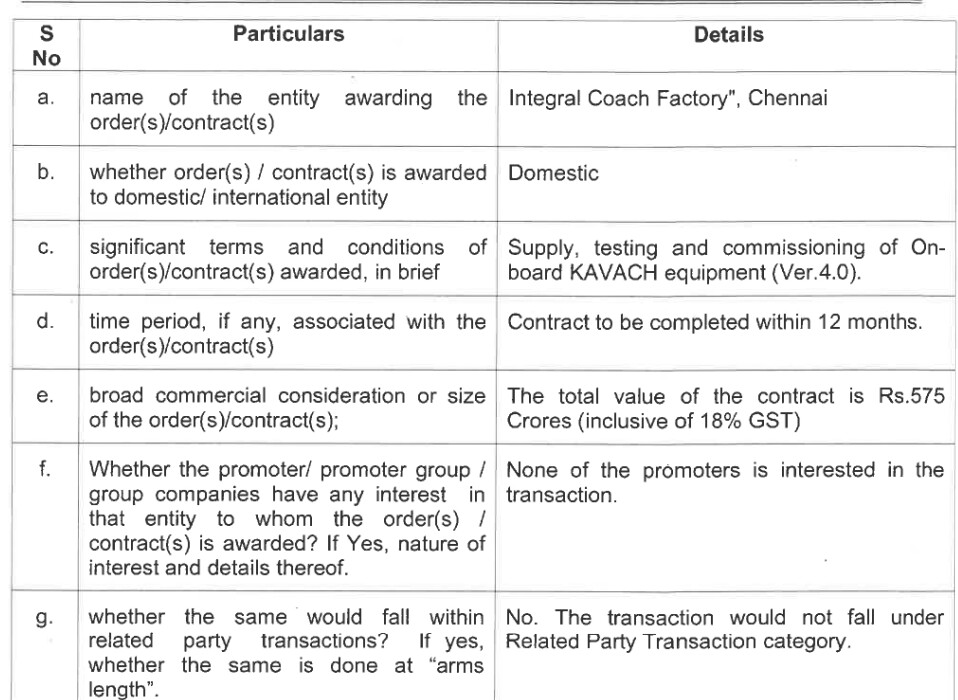

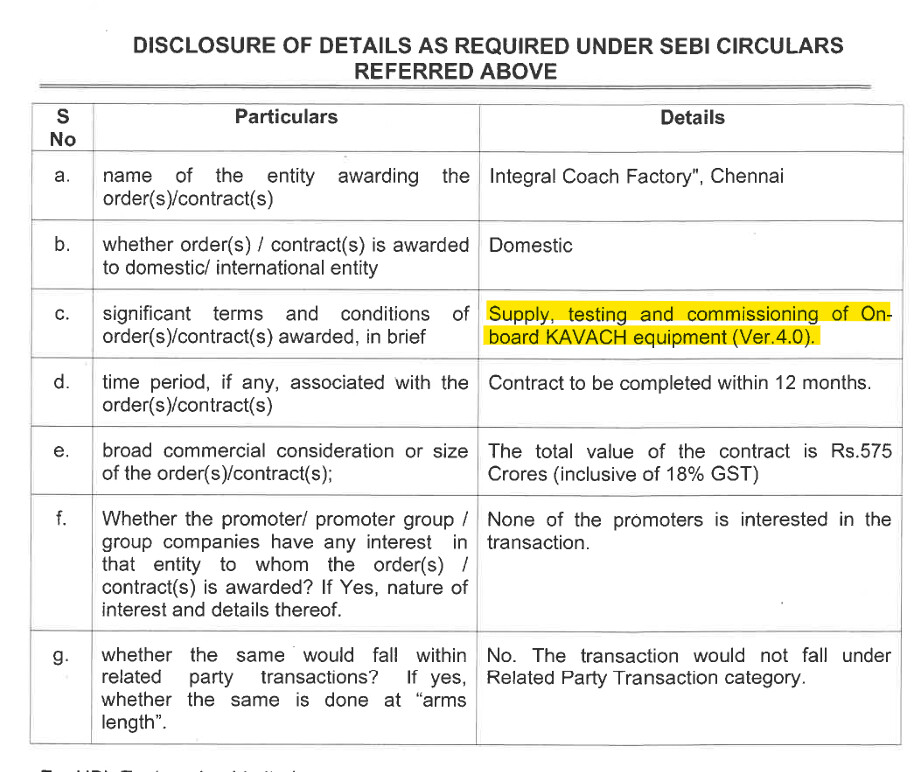

HBL got ICF, Chennai order of 575 crores (Incl GST) for Kavach 4.0 supply & commissioning.

Exchange filing here.

8 Likes

Assuming HBL’s pricing is same as quadrant’s (1.2 Cr per set incl GST), HBL’s share comes out to 575 / 1.2 = 480 sets out of the total 2400 sets. This is 20% of entire tender and also 25% of 1920 (80% reserved for approved vendors), which indicates that HBL was L2 or L3 in ICF tender. This also indicates that the tender has been split across L1, L2 and L3. Which means Kernex will get some allocation as well.

7 Likes

It beats me why HBL quoted so much high? We know that margin in Kavach is very high which was reflected in their Q2 figures. When competition is going up there was bound to be some reduction of margin. HBL management is efficient enough to know this. So it beats me why they made bid so aggressively. We expect to know the truth in a few days time during their Q3 conference call. Till then fingers crossed.

1 Like

I guess they can take this risk knowing their other business might scale up going ahead, or they might have other plans. Energy storage/defense is also an area where HBL has invested a lot, and they might have plans to scale that up as well. Too much reliance on Kavach can be devastating for a company or investors, as government orders and execution delays can be a challenge while evaluating a business. See what happened with Kernex last year. They were not able to execute the majority of their orders in the last 2-3 quarters because of pending approvals, and now, even though they have the orders, their execution capabilities will be tested. We can rest assure on the execution part from HBL.

8 Likes

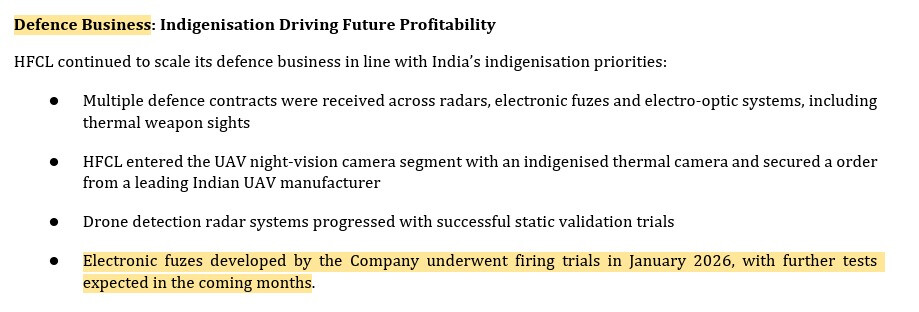

Update on Electronic Fuzes business by HFCL management:

Firing trials done in January 2026, and further tests expected in the coming months.

As per HBL management, they do not expect a significant contribution from fuzes before FY28.

3 Likes

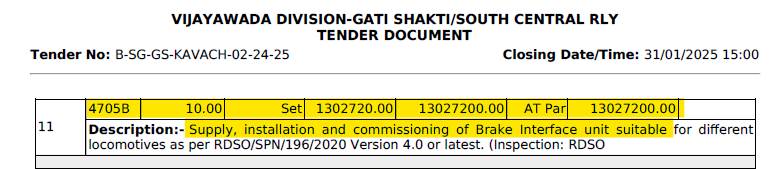

As pointed out by @faltooinvestor in the Kernex thread, HBL is one of the developmental vendors for Brake Interface Unit (BIU). BIU is one of the components of locomotive KAVACH.

Originally BIUs were manufactured by Faiveley Transport (French company with manufacturing plant in Tamil Nadu).

My question is: Is there a backdoor opportunity for HBL in the loco KAVACH tenders through BIUs? Will other vendors such as Kernex purchase BIUs from HBL?

Among all the listed vendors HBL is listed to have the largest capacity (1000 sets per annum). However this is dated info since HBL has been classified as a “developmental vendor” since 2022. If anyone has any insights on the pricing of BIUs, their share in each loco KAVACH installation etc. then please throw some light on this.

3 Likes

What if the Quadrant order include AMC spread across multiple years? If you see, HBL hasn’t mentioned anything about AMC inclusion in the contract vs Quadrant explicitly stating its inclusion? The non-mention of number of locos in HBL order has complicated the calculations to be honest.

3 Likes

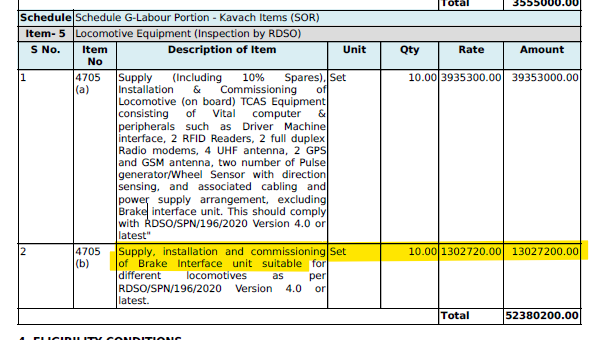

The price of supply, installation, and commissioning of one unit of BIU for loco is ~Rs. 13.03 lakhs. Below are the screenshots from the following tenders:

a. Gudur Jn (from center line towards BZA) - Vijayawada - (excluding Vijayawada)

section (HDN5 Route) of South Central Railway

b. Balharshah (from center line towards KZJ) - Kazipet Bypass - NWBH (excluding

Vijayawada) section (HDN5 Route) of South Central Railway

2 Likes

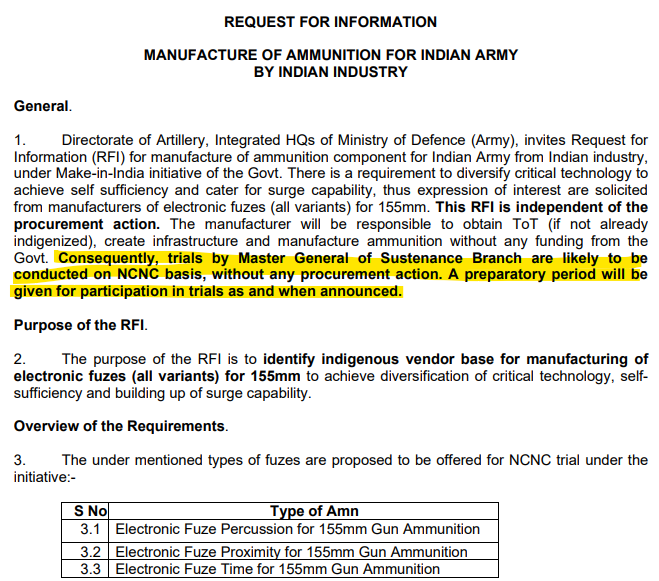

There was an RFI released in Nov 2025 for 155mm electronic fuzes. Indian Army Issues RFI for Indigenous Manufacturing of 155mm Electronic Fuzes Under Make in India - Indian Defence Research Wing

Trials were supposed to happen post the closure of RFI (closure date was in Dec 2025). Given the urgency because of Operation Sindoor, I would not be surprised if the trials would have happened in Jan 2026.

7 Likes

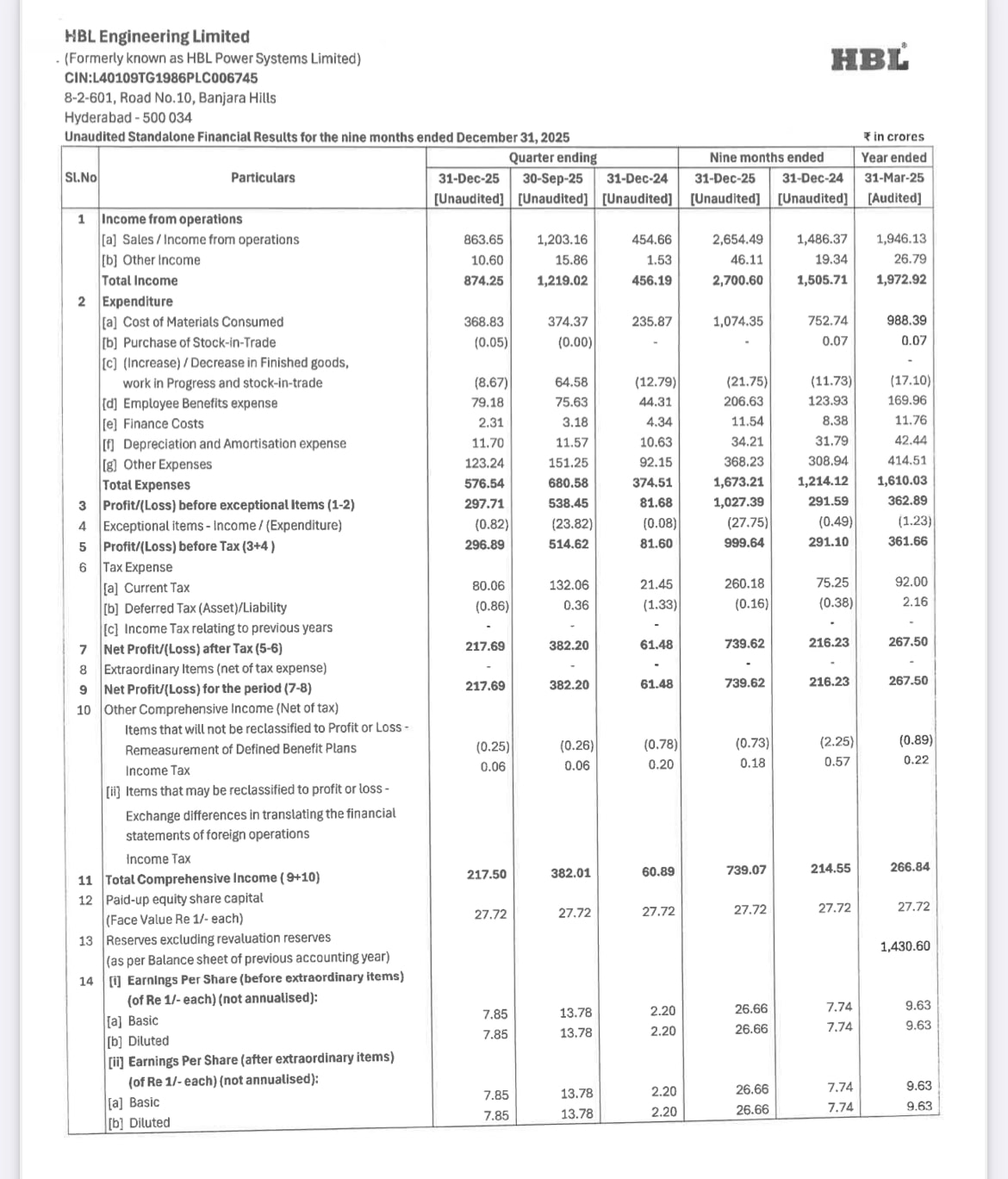

HBL announces Q3 results. Revenue 833 Cr, PAT 217 Cr. Good operating margin 33%. Dividend of Rs 2 per share. No projections for FY27 given.

HBL Q3FY26 Results.pdf (2.1 MB)

6 Likes

Numbers “largely” as expected.

Big growth YoY, quarterly dip was expected but honestly I was expecting close to ~1000 cr revenue as they had time to ramp up Trackside/ Stations kavach execution.

Well, what’s even more interesting than the Q3 result is the update on startup investments.

As indicated earlier, HBL is deploying surplus cash into two deep-tech startups:

- Yaaneendriya Pvt Ltd (Bengaluru)

- Xalten Systems Pvt Ltd (Kochi)

Yaaneendriya is an Indian sensor manufacturer focused on high-performance inertial solutions, GNSS, and AI-based autonomous systems.

Xalten Systems is working on innovative products in robotics, embedded systems, and sensor networks.

Will be interesting to see track these companies, along with HBL going forward:)

21 Likes

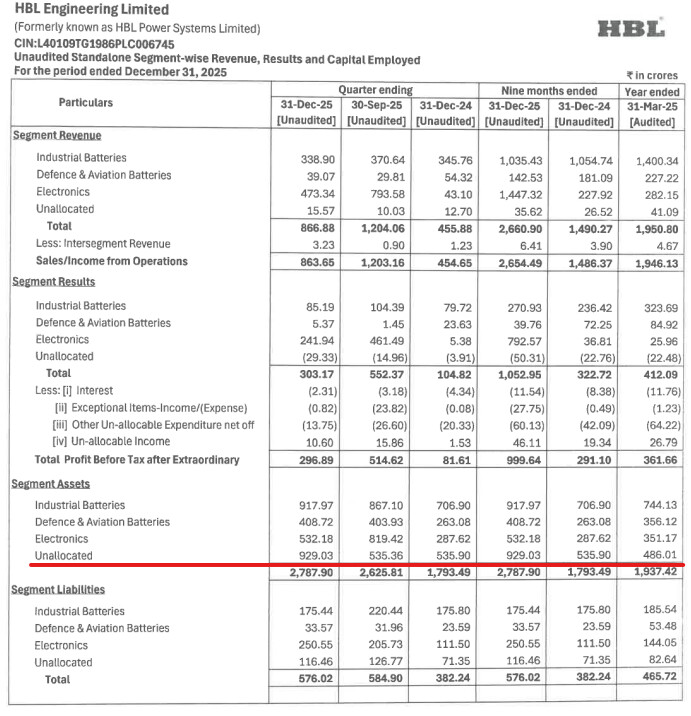

One observation regarding Dec results. HBL releases segment wise revenue, results and capital employed. Saw a sharp rise is assets under the category “Unallocated” by 400 Cr (almost 75% over the Sep’25 quarter and 100% increase over Mar’25 quarter).

As far as I understand the “Unallocated” category is for new product categories such e-trucks, electronic fuzes and other products for defence applications. Looks like something concrete is brewing and the management has not announced it yet. I have a strong suspicion that this is related to electronic fuzes. Employing 400Cr of additional capital cannot be just for R&D. Looks like they have received or anticipating a large order.

Channel information indicates that previously in 2025, HBL has supplied electronic fuzes for 40mm grenades to CRPF and 155mm electronic fuzes to a European country, both via MIL. Taken together the revenue from these 2 supplies could be around 10% of FY25 revenue. While not very significant, this would mean that HBL’s investment and patience has finally started paying off. Bigger things might be in store in FY27 and FY28.

22 Likes

It could be due to the realization of bumper profits from the last quarter, which were previously recorded as accounts receivable in the electronics segment. Those amounts have now been realized and shifted to cash and cash equivalents this quarter. You’ll also notice a corresponding decline in the electronics segment’s assets compared to last quarter. Just a calculated guess.

7 Likes

Another order for Kavach from Banaras Locomotive Works (BLW) worth Rs 800.36 crores

5 Likes