Electronic Fuzes for Dummies

For HBL investors electronic fuzes are often mentioned but rarely explained clearly. Yet, the fuze is one of the most critical, safety-sensitive, and value-dense components in any ammunition. I was speaking with @niraj the other day and between us we could write a series of 2-3 posts talking about the functioning, the market opportunity and the revenue potential for HBL in the coming years. So here goes the first post.

A note on nomenclature: It is spelled as “fuze” and is not to be mistaken for electrical “fuse”, which is a device which breaks an electrical circuit when a high current passes through it. “Fuze” is specifically used for a device which is used inside ammunition.

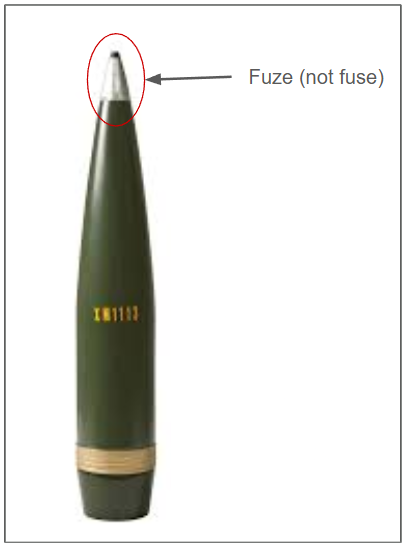

The fuze is almost always located at the top (nose) of any ammunition. Like in this picture of a 155mm artillery shell.

This post is structured into the following sections to build a clear, logical understanding:

-

What is the fire train?

-

Why is a Safety and Arming Device (SAD) required?

-

Mechanical SADs or mechanical fuze functioning

-

Problems with mechanical fuzes

-

Why electronic fuzes are better?

-

Critical items in electronic fuzes: the Micro-Electric Detonator (MED) and ampoule battery - what gives HBL the edge in this?

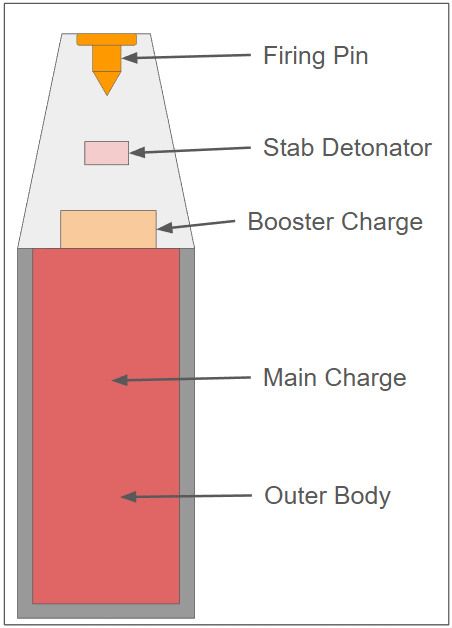

1. What is the fire train?

The fire train is the controlled energetic pathway that transfers initiation energy from the fuze to the main explosive charge.

Conceptually, it consists of:

-

Firing pin

-

Detonator

-

Booster charge

-

Main charge

“Charge” over here means explosive. It’s a term used in the defence industry. Here is an over-simplified image of a fire-train:

On impact with the target, the firing pin hits the stab detonator, which is an extremely sensitive explosive. It is sensitive to even tiny amounts of friction, force, impulse etc. So when the firing pin impinges on the stab detonator it immediately detonates and initiates the next explosive in line which is the booster charge which then initiates the main charge. The booster charge is required because the stab detonator in itself is not capable of initiating the main charge. All these elements together are referred to as the “fire train” and it is responsible for detonating the entire ammunition on impact with the target.

Like I mentioned above, the stab detonator is extremely sensitive to friction, impact or force. That is why it is called the “stab” detonator because you are literally stabbing it. If you were to take some of this in your hand and scratch it with your nails then it will detonate in your hand. Even an amount as small as 1 gram of this is sufficient for rupturing the hand and possibly taking off a couple of fingers. The other elements of the fire train - booster and main charge - are the exact opposite i.e. extremely insensitive. You could play hockey with balls made out of those or light them on fire and still nothing would happen. However when they detonate (when initiated by the stab detonator) they will create devastating consequences.

2. Why is a Safety and Arming Device (SAD) required?

Like we have understood above, the stab detonator is the weakest element of the fire-train. Now imagine these scenarios, what should happen to the ammunition if:

-

The vehicle carrying it meets with an accident, lets say a high speed head on collision with another vehicle

-

The personnel handling the ammunition accidentally drops it from his hand

-

There is a fire at the ammunition depot, where a large quantity of this ammunition is stored?

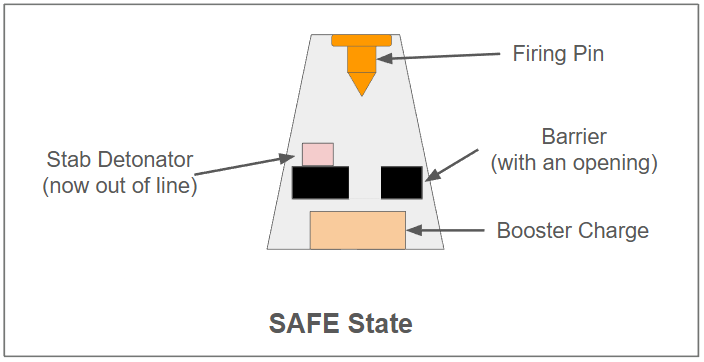

Should the ammunition detonate in these situations? The answer is NO. But the “stab detonator” in all likeli-hood will detonate under these conditions. This is where the safety and arming device (SAD) comes in. SAD is also referred to as “fuze”. We will use these terms interchangeably from here on. The key function of a fuze is:

The fire train must remain safe during storage, transport, and handling — and only become continuous under very specific, verified conditions.

Since the stab detonator is extremely sensitive it is not put inline with the firing pin and the booster. It is kept “out of line”, so that even if it accidentally detonates the rest of the ammunition remains safe. Usually the booster charge and the stab detonator are separated by a metal barrier. The barrier has a small opening and the stab detonator is initially away from the opening. This is called the “SAFE” state.

When very specific, verified conditions of ammunition launch are detected then and only then is the stab detonator brought in line with the firing pin and the booster charge. In this state if the firing pin impinges on it then the ammunition detonates. This state is called as the “ARMED” state. And so these devices are called “Safety and Arming Devices”.

So what are these very specific, verified conditions? The answer is it depends on the ammunition. But for ammunition such as 155mm artillery shell these conditions are “shock” and “spin”. When these ammunition are fired from a gun they go from being stationary to a speed of around 900 m/s in a fraction of a second. The entire ammunition experiences a great amount of jerk or shock. Also when it comes out of the barrel it is spinning at an extremely high rate, around 15,000 RPM!

The job of the fuze is to detect the shock and spin, only if they are experienced simultaneously and of a certain magnitude then “ARM” itself.

3. Mechanical SADs or Fuzes

Historically, SADs were implemented using purely mechanical means, such as:

These systems rely on physical forces generated during launch to:

-

Remove safety blocks

-

Align explosive elements

-

Enable the fire train

Mechanical fuzes dominated for decades because they were:

Many are still in service today. You can watch this video to understand more:

4. Problems with Mechanical Fuzes

While proven, mechanical fuzes have structural limitations that become more visible in modern warfare and procurement environments:

a) Limited Precision and Repeatability

Mechanical systems are sensitive to:

This leads to performance scatter, which militaries increasingly dislike.

b) Constrained Functionality

Adding features such as:

c) Safety Scalability Issues

As safety standards tighten, achieving multiple independent safety barriers using only mechanical elements becomes bulky, heavy, and expensive.

d) Obsolescence Risk

Mechanical designs are harder to upgrade once fielded. Every upgrade or re-design requires thorough testing in all kinds of conditions and this results in long procurement cycles.

5. Why Electronic Fuzes Can Solve These Problems

Electronic fuzes replace many mechanical decision-making elements with sensing, logic, and controlled actuation.

a) Deterministic Safety Logic

Electronic systems can require multiple independent conditions to be satisfied before arming — not just a single physical event. This dramatically improves safety assurance.

b) Multi-Function Capability

A single electronic fuze design can support:

-

Point detonation (on impact)

-

Delay post impact (if you want the ammunition to detonate after penetrating a bunker)

-

Proximity (detonate in close to the target where a direct hit may not be achievable. E.g. in anti-aircraft or anti-drone ammunition)

-

Time-based functions

This creates platform reuse, a major commercial advantage.

c) Environmental Robustness

Electronics allow compensation for:

-

Temperature

-

Launch profiles

-

Storage aging

Result: more consistent battlefield performance.

d) Upgrade and Differentiation Potential

Software-driven logic allows:

This is where margins and long-term contracts often come from.

6. Critical Items in Electronic Fuzes - Where HBL has an edge

Two components largely define the credibility and technical depth of an electronic fuze manufacturer.

Micro-Electric Detonator (MED)

In electronic fuzes instead of the “firing pin” + “stab detonator” combo you have the MED. It is the interface between electronics and booster charge. It is basically a detonator which initiates on giving an electrical input (voltage/current).

Its importance lies in:

-

Extremely high reliability requirements

-

Tight control over sensitivity

-

Immunity to stray energy, electromagnetic interference, and ESD (static electricity)

-

Consistent output over long storage life

Few companies master this well — which creates defensible competitive moats. HBL has successfully developed its own MED.

Ampoule Battery

Electronic fuzes require power — but only after launch. Ampoule batteries play an important role in this. They have the following characteristics:

-

Remain inert during storage

-

Activate only under launch conditions

-

Provide reliable power for milliseconds to seconds

Their value is not in energy capacity, but in:

In-house ampoule battery capability is a very high barrier for entry.

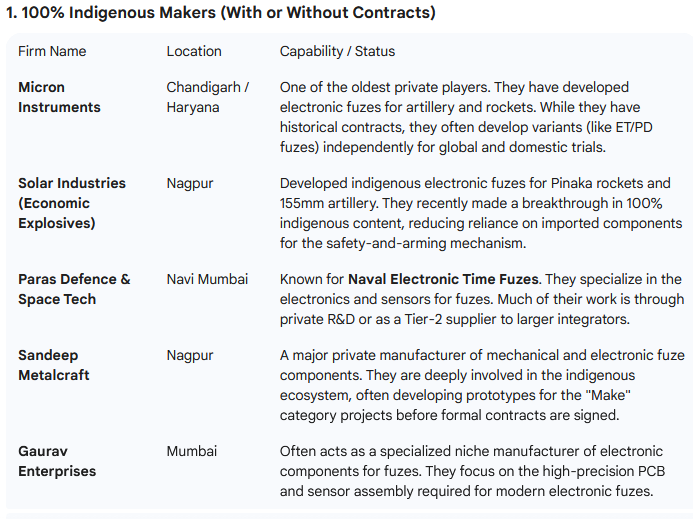

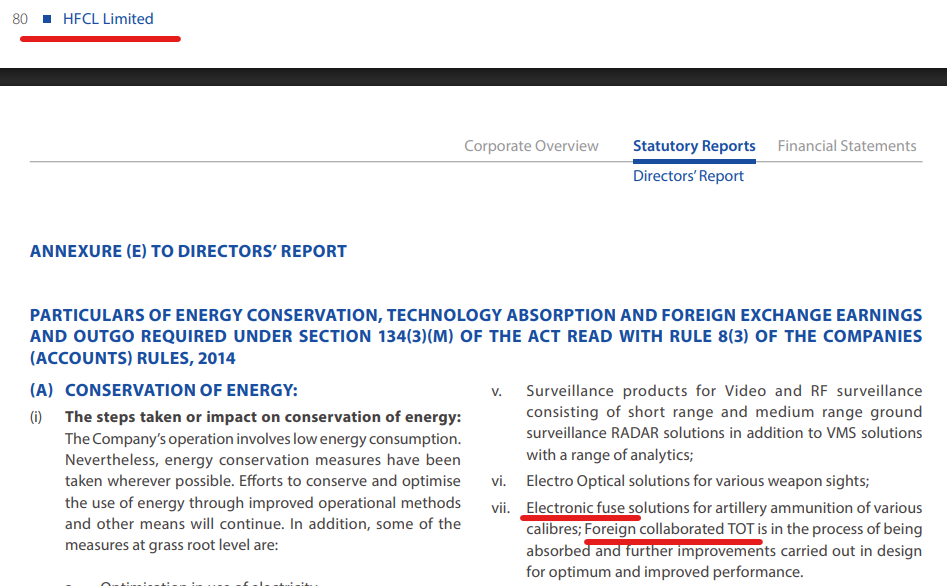

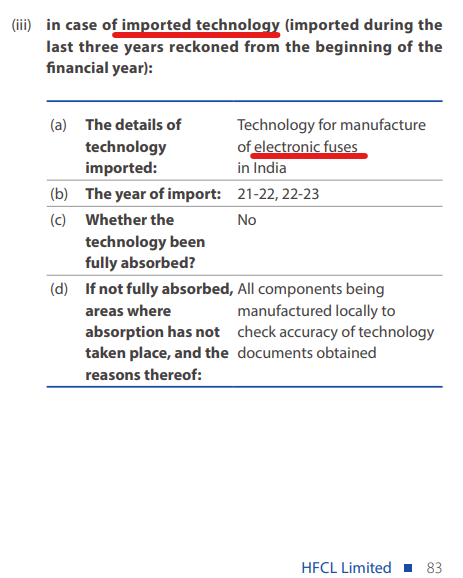

Very few companies supply these 2 components on a stand-alone basis. If you manufacture these 2 then you may as well manufacture the entire fuze. In my knowledge there is only 1 South Korean company which supplied the ampoule battery as a standalone item. And a handful of companies across the world which supply the MED as a standalone item. Having indigenized these 2 components, HBL stands out in the electronic fuze game it is the only Indian company with 100% indigenization.

Over to @niraj to talk about the market potential and potential revenues from electronic fuzes.