I went ahead and did a Capital Structure analysis for Hatsun. Here’s the file: Hatsun Capital Structure.xlsx (91.0 KB)

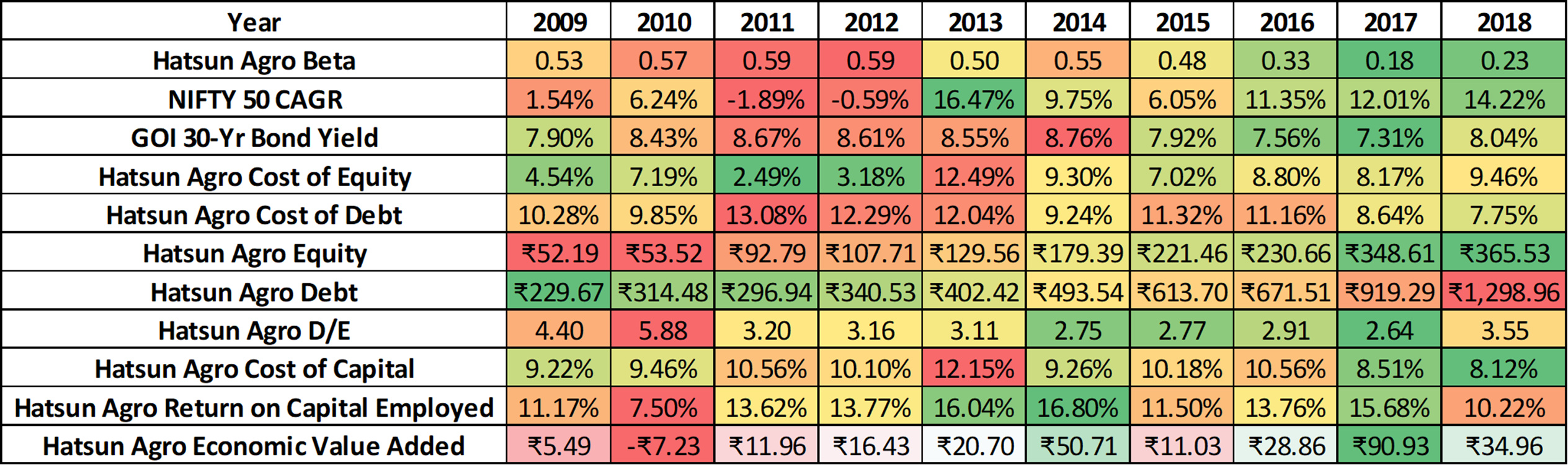

Hatsun has created the most Economic Value when its D/E was 2.64, the second highest being at 2.75. So, I’d conclude that the optimum D/E for Hatsun would be somewhere around these levels. Providing for some Margin of Safety, we could say that a 2-2.5 level would be good.

But we are definitely looking at some oversights:

-

We have no way of knowing how the market viewed the risk in Hatsun at lower Debt levels (Say <2). This was all the data I could gather. If someone has all these data before 2009 (Possibly when Hatsun had lower Debt levels), that would yield more prominent results.

-

Another constraint would be the fact that Hatsun capitalizes interest regularly:

I did not make this adjustment in while doing the analysis (It’s tedious to go through 10 Annual Reports just to locate whether the company capitalized interest or not).

- Hatsun also has some leases in its name, which should ideally be ‘converted’ to Debt while thinking about Enterprise Value. Once again, I didn’t bother doing this.

2 Likes

There is some ongoing very healthy discussions on Hatsun’s high debt and the risks arising out of it.

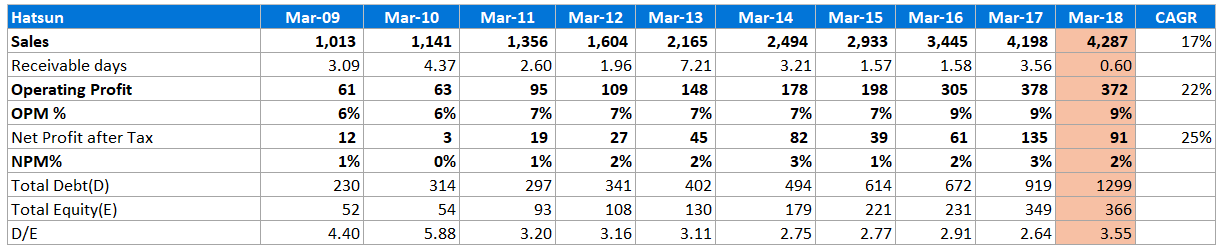

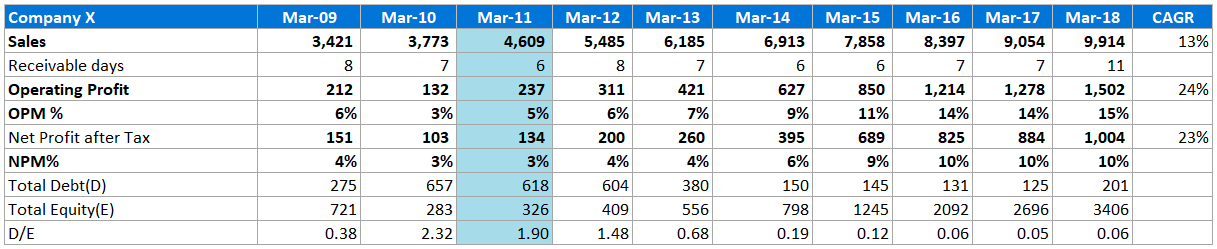

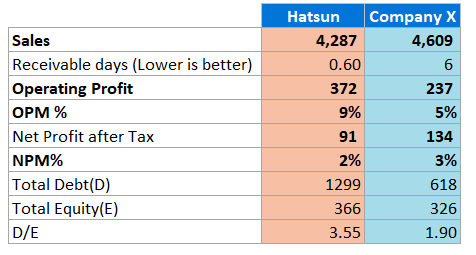

Let me take you through an example. This is Hatsun and this is another company (X) whose numbers look pretty similar - even lower OPM and profit margins, huge debt.

Some more information on Company X:

- Market Cap : 4500 Crores

- P/E : 33x

- Interest coverage : 3.2x

Would you invest in this company ? Most would not, given the high P/E and very high leverage.

…

…

…

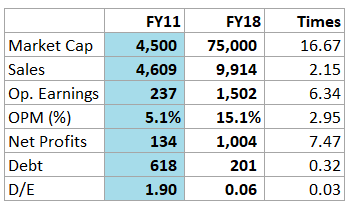

However, we have some benefit of hindsight bias, as the snapshot for company X is from FY2011.

So what happened in the next 7 years ?

The beauty of Operating Leverage and brand moat kicked in, company was able to grow profits 7.5x while improving operating margin by 3x all the while reducing debt to 1/3rd and D/E to 0.06.

For a FMCG play, it is very important to not get perturbed by high A&P spend and leverage in early years, as long the business is able to create strong demand - the key monitorable being the receivable days.

The rest of the things will take care of themselves as growth chugs along and power of Operating leverage kicks in.

Hatsun :

And the Company X:

The company X, by the way is Britannia.

14 Likes

The problem is, as I mentioned, Hatsun has had this large debt for the last decade or so. It fluctuates, but levels remains higher than 2.5x.

If they were actually interested in reducing debt, we’d see a gradual decrease over the years (Regardless of how much that decrease is). But that clearly isn’t happening.

Once again, I’m reminding myself here that the D/E is 3.5x.

2 Likes

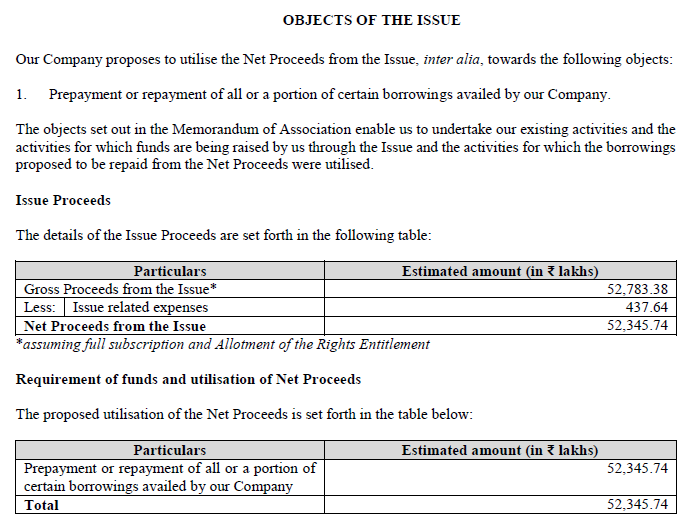

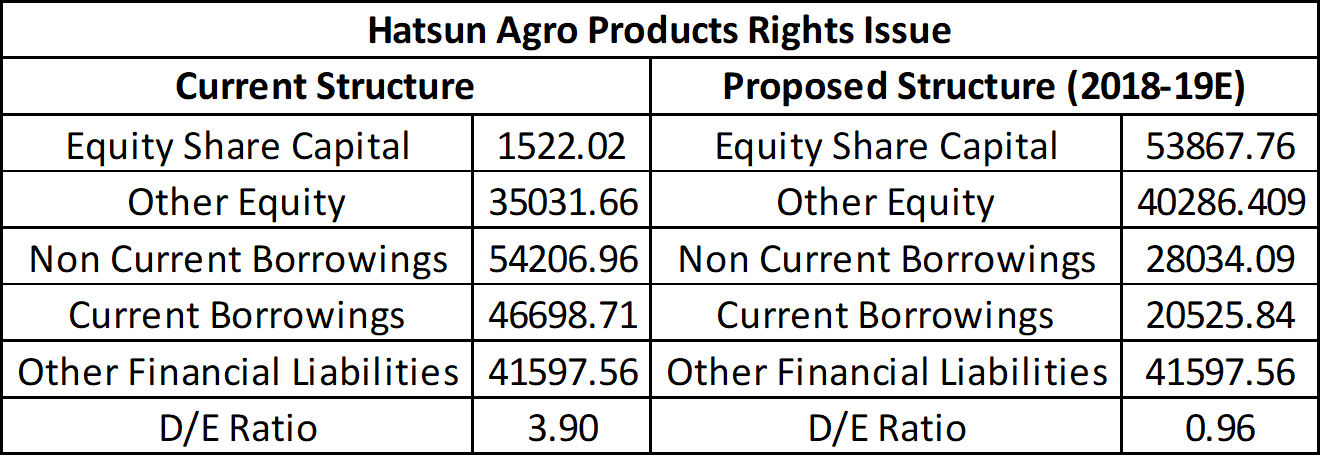

Hatsun is planning to reduce debt using Rights Issue proceeds. Not a big fan of this move but FY19 balancesheet should look different than current balancesheet.

Disc: invested

1 Like

Britannia’s ROC never touched below 25% (during 2011) where as Hatsun’s ROC 14-23% . How should we look at it?

An interesting move. If I’m reading this right, this is how 2018-19 B/S would look like (Retained Earnings is increased by 15% as an estimate):

Of course, the kicker is that the proposed Rights Issue is 143% of the company’s current Equity balance. So, the price should also dilute by so much (Assuming the Rights issue goes through in the first place). This will be very, very interesting indeed, from a Valuation point of view.

Theoretically speaking, Hatsun’s Cost of Equity is higher than its Cost of Debt, so this is a bad move. But speaking from an ‘Antifragile’ point of view, this could augur well for the company’s financial health.

1 Like

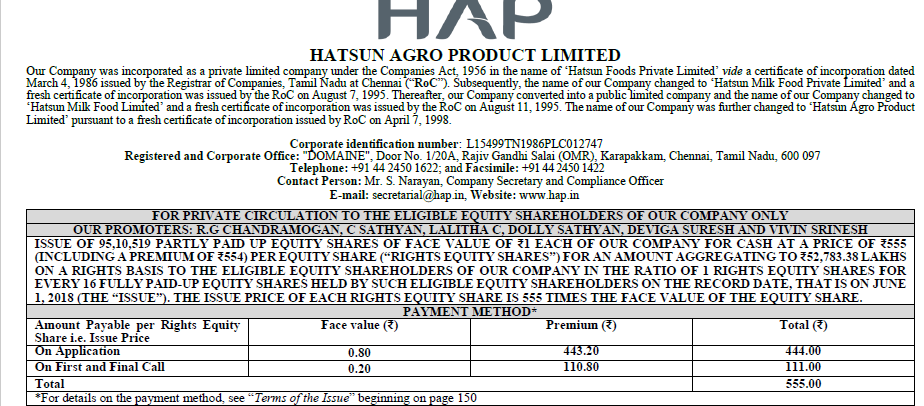

Rights issue closed on July 5th 2018 @ Rs. 555 per share. 80% has been called and paid during application and rest 20% will be called in future.

1 Like

Thanks a lot. I think this will make for an interesting case to value.

A related question - when a company needs capital and can deploy it at very high rates (25-35%) as seen from the track record, why would you pay out hefty dividends (45-110% of profits) instead of redeploying it? Isn’t this what great capital allocators do?

What you mentioned is correct, and what many companies do.

However, many companies have a stated policy and consistent dividend payment record which they don’t want to deter from. Hatsun has a stated dividend policy which you can refer here

In the Indian market, dividends are often considered as strong signalling indicator whether profits are real and sometimes companies also need to match up their peers from the same segment in terms of dividend payout.

2 Likes

Hi Rudra,

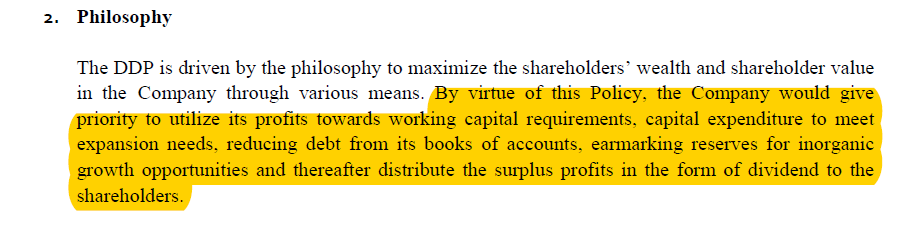

My 2 cents …Hatsun’s dividend policies looks nicer on paper. See the image from Hatsun’s DDP. It clearly says that they would prioritize working capital, capex and debt repayment needs before paying out dividends. But what do they do? Just the opposite- pay dividends and take on more debt (you can see this in the image I posted above).

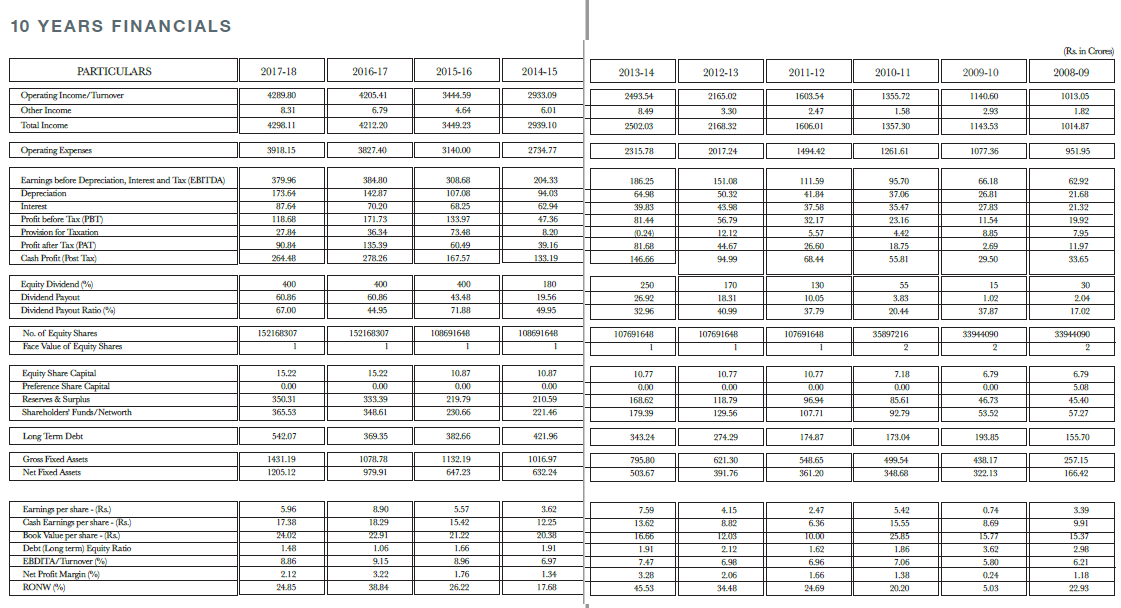

Cumulative PAT (2013-18): 451 Crs

Cumulative dividends paid out (2013-18): 223 Crs

Dividends paid out: ~ 50%

Increase in debt (2013-18): 677 Crs

They paid out 50% of the profits earned, while increasing debt by 677 Crs!

4 Likes

Yes, the management has not increased dividends post FY16 it is maintained at the same level. Also you need to consider primarily change in long term debt during this period which has increased by 367 Cr

As discussed in the posts above, company plans to pay off around 523 Cr from the proceeds of rights issue, out of this Long term debt of 542 Cr, so mostly working capital loans would remain in the future.

2 Likes

https://www.bseindia.com/corporates/anndet_new.aspx?newsid=c1d2acc2-4735-418c-9ab2-e1c21492a6be

The Board of Directors at their meeting held today i.e., October 22nd, 2018 has inter-alia discussed on the following subjects:-

-

Taken note of the completion of acquisition of about 75 acres of Land situated at Solapur District for about Rs.6 Crores towards setting up a dairy manufacturing plant in the State of Maharashtra. The installation of the dairy plant is expected to be commissioned before end of December 2019. This is an update to our earlier announcement made to the Stock Exchanges on 19th July 2019.

-

The Company is envisaging plans to set up a Dairy Plant in the State of Odisha considering an attractive proposition for investment offered by the State of Odisha and has submitted ‘Investment Intention Form’ with the Industry Department of Odisha Government.

1 Like

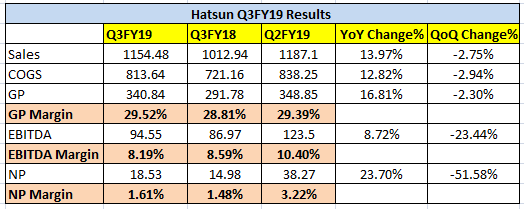

ICYMI Actual (unaudited) figures are now available here. Suppose largely in line except for differences in allocation of Current and Non-Current part of liabilities

1 Like

Yes, I didn’t know which Liability they would pay off first, so I reduced them both equally.

1 Like

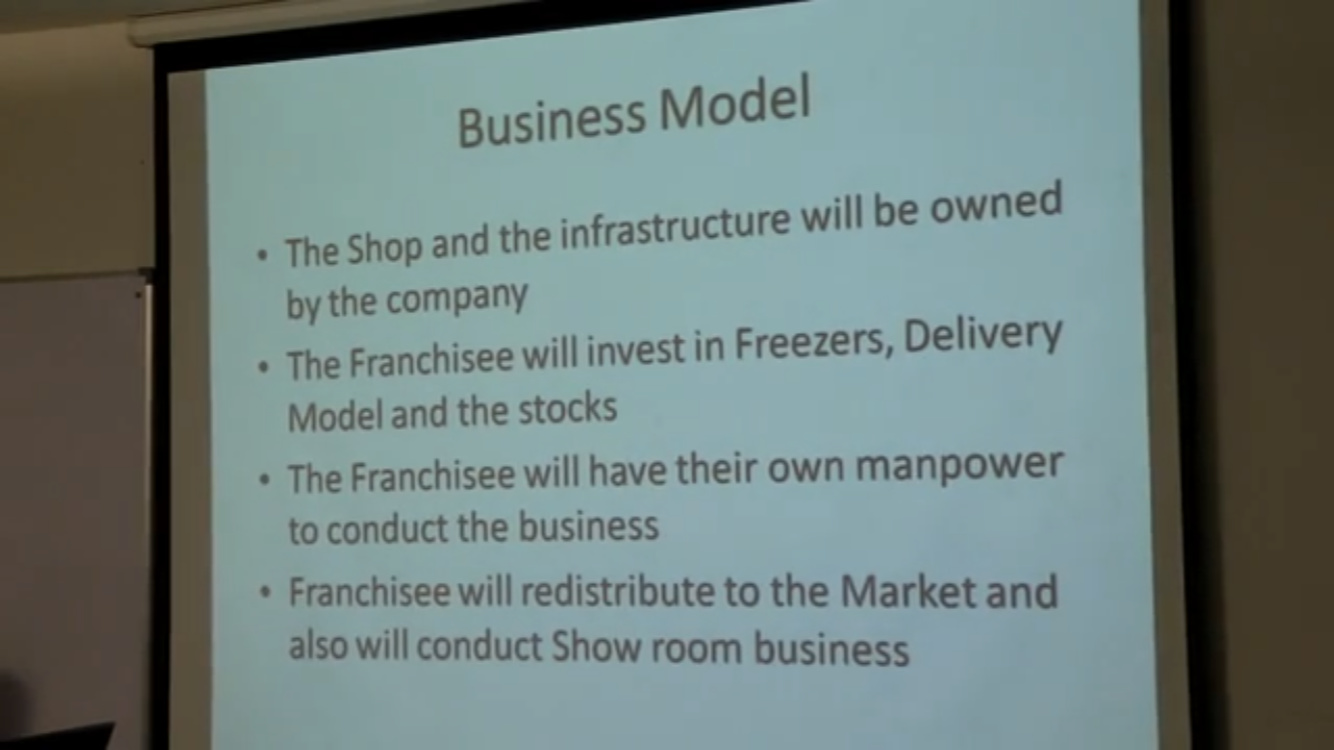

Here is a link to a dated (early 2017) but very informative video on Hatsun Daily Stores at their franchises meet.

As per the Presentation, Hatsun Daily Stores are owned by the Company and the Franchisee has

to make limited investment and earns ~25% Return on Investment.

There are multiple news articles for e.g. this one

which mention the Company’s aggressive expansion in Hatsun Daily Stores.

“The company also has its own Hatsun Daily retail outlets, which sells all its brands. It currently has 1,200 outlets and is adding another 1,800 outlets in a phased manner over the next 15 months.”

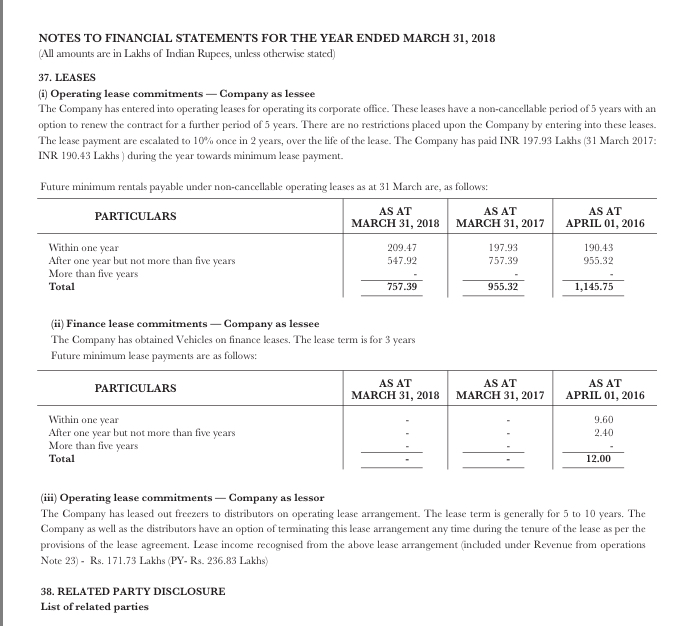

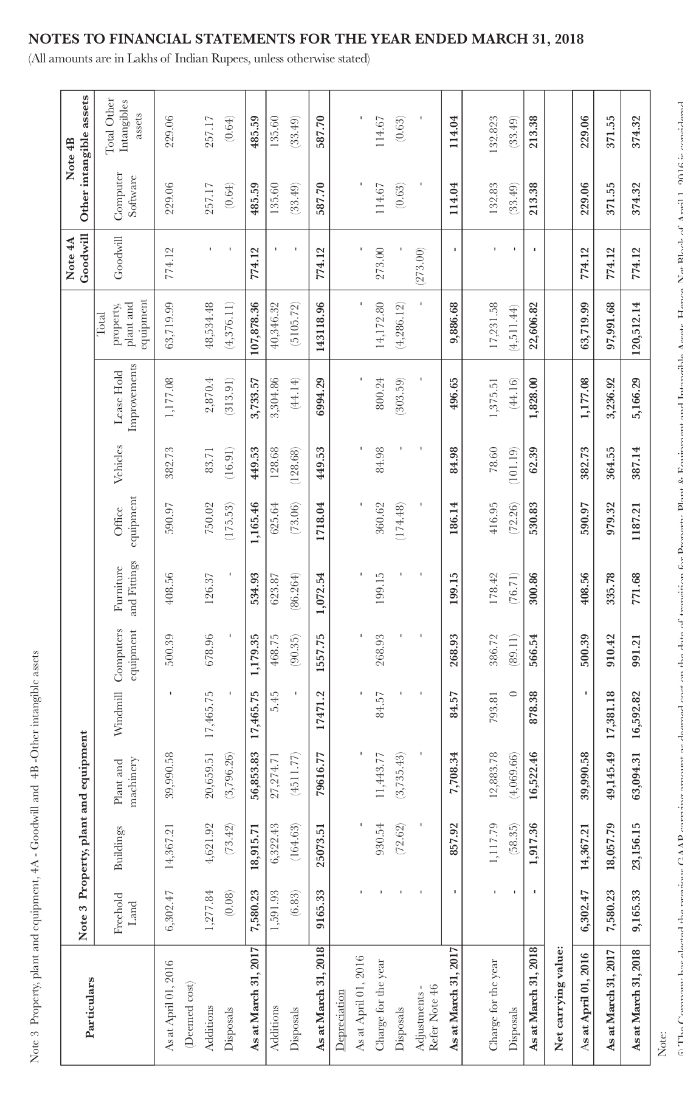

Looking at the Balance Sheet, there has neither been enough capex, nor any lease commitments to support the growth in stores through Company owned / leased stores

Am I missing something here?

2 Likes

At 7:50, the presenter mentions that “rent will be paid by the company”. I don’t think Hatsun “owns” the property but leases the property for Hatsun Daily stores.

1 Like