Stock is now trading at a PE of 88. Even if it dips to 600ish level should we enter?

Disc: Invested at 600 and exited at 750 after stake buyout by sbi mf.

Stock is now trading at a PE of 88. Even if it dips to 600ish level should we enter?

Disc: Invested at 600 and exited at 750 after stake buyout by sbi mf.

If we see a bear market, what PE could it demand?

@anand21 and @Uservijay - I recommend you to not use PE as the only basis to buy or sell any stock. I am not saying that PE is useless but experts have said that PE is a blunt tool if used alone. Focus on business economics, moats, earnings power, management, reasonable valuation etc. Analyze how much cash the business can generate from its operations. And then how much of this cash generated from operations have to used for future business expansion and working capital needs. Whatever is left after spending on business expansion and working capital is called Free Cash Flow. Using reasonable estimates and facts estimate what FCF a business would generate in near future and discount future FCFs to present value with appropriate discount rate to come to your intrinsic value. Compare intrinsic value with the market price. Hope this helps.

Disc: invested.

Very good fundamentals & management team, only eye sore is high debt to equity. If co. dilutes appx 8% equity they can raise 1000cr.by right issue to pare down debts I think it is a positive.

4th quarter results are not good, sales & profits are down. Right issue @ of Rs. 555, announced, investors would get 01 share for every 16 shares, record date for right & dividend of Rs.03 per share is 01st of June 2018.

Equity dilution is 6.25%, if company pays back loans of 500cr. out of total right issue of ₹ 530cr. savings on account of interest would be 50cr./ annum that would be increase of appx ₹03 per share of EPS. I.e. EPS would increase by 44% from ₹06 to ₹09 per share on annualized basis after equity dilution.

*Invested

@Gurmeet thank you for sharing the info. Where did you find above mentioned rights issue info? I see 1st June 2018 as record date for rights issue, but don’t see ratio and price info anywhere. Please share the link/source.

The information is available on Equitybulls web site.

Stock Report

|More

Hatsun Agro Product Ltd approves terms of rights issue

Posted On: 2018-05-22 09:44:03

The Board of Directors of Hatsun Agro Product Ltd, at its meeting held today (i.e., 21st May 2018) has approved the terms of the Rights Issue of partly paid Equity Shares viz., Issue Size, Issue Terms, Ratio of Entitlement, Record date and Treatment of fractional entitlement.

The partly paid up Equity Shares are being offered on a rights basis to Eligible Equity Shareholders in the ratio of 1 (One) partly paid up Equity Shares for every 16 (Sixteen) fully paid up Equity Shares held on the Record Date.

The company proposes to issue 95,10,519 partly paid up equity shares of Re.1 /- each through rights issue.

The record date for shareholders to be eligible for the rights issue is Friday, June 01, 2018.

The issue price is Rs.555 per partly paid equity share (Including a premium of 554 per partly paid equity share).

Shares of HATSUN AGRO PRODUCT LTD. was last trading in BSE at Rs.785 as compared to the previous close of Rs. 788.05. The total number of shares traded during the day was 2457 in over 153 trades.

The stock hit an intraday high of Rs. 795.15 and intraday low of 769.9. The net turnover during the day was Rs. 1929896.

Source: Equity Bulls

Thank you @Gurmeet! I missed this announcement (rights issue details) among other 21st May announcements on BSE site.

For others: below is the BSE link for rights issue details

Does someone have information about utilization of the right issue proceeds?

For expansion or debt retirement?? Kindly post. Thanks.

Excellent presentation from ProsperoTree (Dhruvesh Sanghvi)… watch the presentation video here

Hello Friends,

I started studying this company only recently and immediately a few things came to attention. If any of you have more clarity or have thought about these things, please do share.

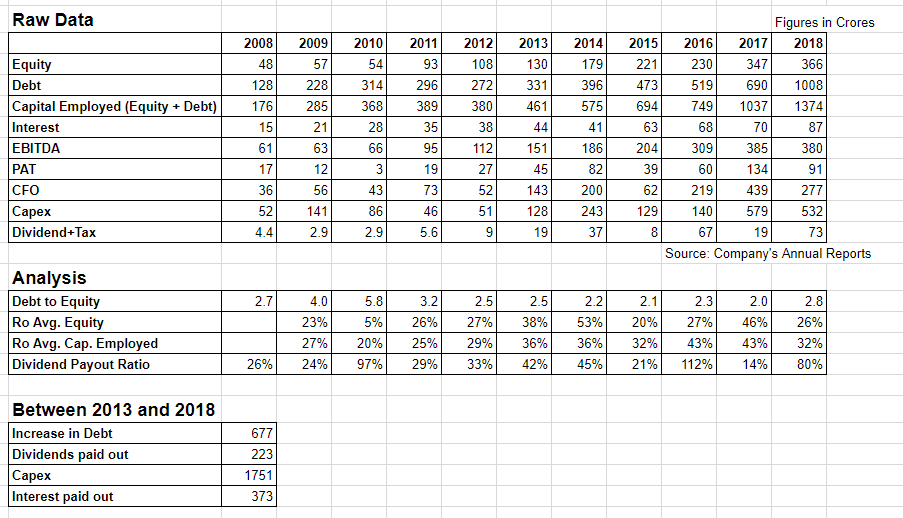

Like I said, if you have thought about these things, please do share the same. For your reference I am sharing a snapshot my spreadsheet.

Hi Vikas,

Not denying high leverage is bad but based on personal experience I think EBITDA/Interest is a better metric than Debt/Equity (for a long time I had been using only debt/equity and then shifted based on experience and suggestion from few mentors). Reason being we want to check ability of company to pay debt using profit made and I have found many instances when debt to equity looked high but EBITDA to Interest looked relatively better. Here too, if you see EBITDA/Interest, it has always remained above 2.5 which means even with 20% fall in EBITDA, you can pay 2 years of interest. Also, you see trend 2010-11 was period when this number went around 2.5 from 4 due to heavy capex made in 2009 and then even when another heavy capex made in 2014, still it remained above 3 and now it is above 4. However, when you see debt to equity, it looks like situation is still equally bad which may not be case. So, I would any day check leverage risk with EBITDA/Interest

No denying that leverage has been a risk in this business but would suggest to read about 30 year of history how this company (promoter ) has evolved. I had a case study in MBA on the promoter and thats how I was introduced to this company. Disc : have held heritage and hatsun in past. No holding now,still in watch list

The only caution we need to take care is interest is evenly spread to avoid any future surprise and interest as % of debt looks legitimate

Interest turns show the short term capacity of the company to meet interest payments.

However, Debt is not just the interest. It also has a principal component, which is supposed to be repaid at some future date. D/E helps in identifying the principal repayment capacity.

Ultimately, it’s okay to have a huge D/E provided the interest is lower than the Cost of Equity. But I’d say a 3+ D/E is pushing it too far.

Hatsun has created some amazing brands and economic value over the years. But choosing to achieve it by excessive debt is a red flag for me personally.

NN Taleb talks about the follies of debt extensively in “Antifragile”:

(Both Motley Fool and Farnam Street have excellent articles on ‘Antifragility’ as defined by Taleb).

Thanks.Makes sense. However, in that case for principal repayment capacity, wont “net debt” to cash from operations will be a better indication ? Just thinking and asking

Yes , that could give an idea how long it may take to service the total debt.

Say the debt is 10 times of average annual CFO, it gives a good indication what kinda position the company is in.

However the interest payment ability also gives clear indication about the debt stress.

This is my way, which has worked fine.

So it is like seeing all the ratio including D/E, average CFO/ Net DEBT, and interest payment ratio together.

Views and counterviews welcomed.

Net Worth is represented via both Assets and Cash in the B/S. That’s why in most Credit Rating companies, some kind of Liabilities / Net Worth ratio has the maximum weightage. For example, look at what we have to say:

Going along with this, we can also understand that liquidity is another problem. Even if Hatsun shut down tomorrow, it’ll take a long time for them to convert their plants and machinery and inventory to cash. Maybe some of it, they won’t even get to convert.

Dinesh- the CRISIL document is absolutely great. Thanks for sharing!

Thanks Saurabh and Dinesh for the great discussion.

My current thought are-

See this snippet from the CRISIL document Dinesh shared:

I still do have a question regarding the dividend payout ratio. Why should the company not follow a more conservative dividend policy, given that it can deploy the accruals at very high rates of return?

“Higher Debt” does not mean ridiculous amounts of Debt. Do this. Find any Credit Analyst you know and ask him what he thinks about a 3.5+ D/E Ratio for a non BSFI firm.

While the risk of default may be low, the impact of default is high. As we all know, the risk in debt is measured as PD * LGD i.e. Probability of Default times Loss Given Default. While PD is low for Hatsun, LGD is quite high.

I suggest you read Taleb’s “Antifragile” or at least the article I shared above. It is very prudent to avoid companies with ridiculous amounts of Debt.

Of course, if you believe that Hatsun can easily pay down their Debt, that’s fine too. Everyone’s risk aversion is different. I wouldn’t want to impose mine on anyone else. I can simply point to reasons why.