Can any Hatsun investor throw some light on why the valuations are so high? What am I missing here. This is for pure educational purpose.

low working capital among the peers, focus on pouched milk rather than value added products leading to stable demand, great brand equity in a core market, very prudent and pragmatic management etc…

Go through this report for a complete understanding of the sector along with all the companies in it.

Hope it clarifies

Before two years i am regularly buying Hatsun ghee but now they cant deliver it in gujarat because of high demand in their home state.

Here is my comparison of Hatsun and Heritage on some specific aspects.

A. Depreciation

| Hatsun | FY16 | FY17 | FY18 | FY19 | |

|---|---|---|---|---|---|

| Net fixed assets | 647 | 991 | 1217 | 1408 | |

| Depreciation | 107 | 143 | 174 | 201 | |

| % of Depreciation | 16.5% | 14.4% | 14.3% | 14.3% | |

| Heritage | FY16 | FY17 | FY18 | FY19 | |

| Net fixed assets | 312 | 296 | 433 | 476 | |

| Depreciation | 35 | 25 | 38 | 47 | |

| % of Depreciation | 11.2% | 8.4% | 8.8% | 9.9% |

Why Hatsun depreciation is 15% while Heritage is less than 10%. What kind of assets depreciate at 15%. Here is what I calculated from annual report of Hatsun.

| land | Building | P&M | Windmill | Compu | Furniture | Office | Vehicle | lease hold | Total | |

|---|---|---|---|---|---|---|---|---|---|---|

| Gross at FY18 | 9165.33 | 25073.51 | 79616.77 | 17471.2 | 1557.75 | 1072.54 | 1718.04 | 449.53 | 6994.29 | 143119 |

| Depreciation till FY18 | 0 | 1917.36 | 16522.46 | 878.38 | 566.54 | 300.86 | 530.83 | 62.39 | 1828 | 22606.82 |

| Net at FY18 | 9165.33 | 23156.15 | 63094.31 | 16592.82 | 991.21 | 771.68 | 1187.21 | 387.14 | 5166.29 | 120512.1 |

| Depreciaiton for FY19 | 0 | 1380.65 | 14459.49 | 792.75 | 480.98 | 186.63 | 422.09 | 83.45 | 2109.8 | 19915.84 |

| Depreciation % | 0.0% | 6.0% | 22.9% | 4.8% | 48.5% | 24.2% | 35.6% | 21.6% | 40.8% | 16.5% |

Some components of assets like Plant & Machinery, Computers, Furniture, Office equp, Vehicles and lead hold are depreciating anywhere between 23% to 48%. which is very high I think.

B. Tax

| Hatsun | FY16 | FY17 | FY18 | FY19 | |

|---|---|---|---|---|---|

| PBT | 134 | 172 | 119 | 161 | |

| Tax | 32.67 | 37.18 | 31.32 | 34.58 | |

| % of Tax | 24.4% | 21.6% | 26.3% | 21.5% | |

| Heritage | FY16 | FY17 | FY18 | FY19 | |

| PBT | 86 | 59 | 90 | 126 | |

| Tax | 29.62 | 29.08 | 28.84 | 44 | |

| % of Tax | 34.4% | 49.3% | 32.0% | 34.9% |

Why Hatsun is paying lower tax at around 20 to 25% while Heritage is paying above 30% taxes?

Is there any Tax benefits to Hatsun?

C. Other important points

1.Heritage haven’t diluted equity in last 10 years, there was a bonus issue in the year 2014. Hatsun has been diluting the equity often. In last 10 year they diluted equity 5 times include the recent rights issue of 527cr.

2. Heritage has been maintaining less debt or we can say reasonable debt. This debt is mostly due to retails business which was loss making. However they have sold the retail business to Future retail so they didn’t lose any money on this venture in fact they made money on this venture. Capital employed in retail business in FY16 was 86.3Cr and they sold business to Future at some 3%+ stock exchange which is now worth at 835cr (At the end of FY19)

Hatsun debt has been increasing continuously since last 12 years. Only last year they have reduced debt with cash not from free cash flow but from rights issue.

Excellent talk by Mr. Chandramogan. Regardless of whether you’re a shareholder in Hatsun or not, you should listen to this. Important lessons is brand building and business strategy.

I am starting to look at this company after having looked early in 2016/17. Noticed that the company has stopped sharing sales mix in the annual report from FY19. Does anyone have any idea about the mix or the growth rates across various categories (milk, milk products, ice-cream, cattle feed etc). Thanks

One key aspect while looking the Company from a long term prospect is about the Succession plan…I think Mr Chandramohan is already more than 75 years and have not heard much about his Son. In this old age it is very difficult to handle a business growing at this pace.

Disclosure : Not invested but tracking

According to me this will defenetly be the takeover target by MNCs.

What NESTLE and HUL can not make mr.chandramohan made so now they have everything ready in form of HATSUN.

Disc. Not invested

- Today

- Hatsun AgroProd. insider trade: Pledge of 725,000 equity shares worth Rs 4218.77 lacs by promoter & director

Why the promoter needs money by way of pledging of Shares???

The Company has anounced around Rs 8 as dividend in 2019, Mr Chandramohan holds around 9.15 Cr shares i.e he has received dividend of around Rs 36.60 Cr .

Instead of paying dividend out of the debt, the management could use the money to reduce the debt. Any debt to equity above 0.5 is adding to the risk. Debt to equity above 3 is ridiculous. The management seems very desperate to grow, putting the owners including the minority shareholders at risk of losing their money.

A good business should be able to grow using operating leverage and also command high operating margin which is lacking in this business and industry in which it operates.

Though we regularly buy their products, I could never convince myself to buy due to high valuation and debt levels.

@mmvravindra Thanks for share your insights regarding differences in Depreciation and Tax for Heritage and Hatsun.

I remember that in one concall management highlighted that assets in there factories are around 15 years old and will need to be renovated. That may be the reason of less depreciation compared to Hatsun. But this requires further investigation.

For Tax differences too, I have no clue.

Can any member help to understand the reasons of differences in Depreciation and Tax for Heritage and Hatsun?

Unable to understand why there are so much pledge transactions.

||DEVIGA SURESH|Promoter|7127938 (4.41)|Equity Shares|122000|61610000.00|Pledge|7127938 (4.41)|30/03/2020

| 30/03/2020 | Pledge Released | 30/03/2020 | |||

|---|---|---|---|---|---|

| — | — | — | — | — | — |

| R G CHANDRAMOGAN | Promoter & Director | 91549563 (56.62) | Equity Shares | 2900000 | 1464500000.00 |

| 30/03/2020 | Pledge Released | 30/03/2020 | |||

| R G CHANDRAMOGAN | Promoter & Director | 91549563 (56.62) | Equity Shares | 602400 | 304212000.00 |

| 30/03/2020 | Pledge Released | 30/03/2020 | |||

| R G CHANDRAMOGAN | Promoter & Director | 91549563 (56.62) | Equity Shares | 5640000 | 2848200000.00 |

| 30/03/2020 | Creation Of Pledge | 30/03/2020 | |||

| C SATHYAN | Promoter & Director | 15196774 (9.40) | Equity Shares | 137500 | 56677500.00 |

| 23/03/2020 | Creation Of Pledge | 24/03/2020 | |||

| R G CHANDRAMOGAN | Promoter & Director | 91549563 (56.62) | Equity Shares | 40000 | 22994000.00 |

| 17/12/2019 | Creation Of Pledge | 19/12/2019 | |||

| C SATHYAN | Promoter & Director | 15196774 (9.40) | Equity Shares | 25000 | 13773750.00 |

| 13/12/2019 | Creation Of Pledge | 17/12/2019 | |||

| R G CHANDRAMOGAN | Promoter & Director | 91549563 (56.62) | Equity Shares | 7400 | 4205790.00 |

| 10/12/2019 | Creation Of Pledge | 10/12/2019 | |||

| R.G.CHANDRAMOGAN | Promoter & Director | 91549563 (56.62) | Equity Shares | 640000 | 365504000.00 |

| 07/12/2019 | Pledge Released | 09/12/2019 | |||

| C SATHYAN | Promoter & Director | 15196774 (9.40) | Equity Shares | 351724 | 203296472.00 |

| 05/12/2019 | Creation Of Pledge | 07/12/2019 | |||

| R G CHANDRAMOGAN | Promoter & Director | 91549563 (56.62) | Equity Shares | 2815000 | 1633122250.00 |

| 02/12/2019 | Creation Of Pledge | 03/12/2019 | |||

| DEVIGA SURESH | Promoter | 7127938 (4.41) | Equity Shares | 122000 | 70778300.00 |

| 02/12/2019 | Creation Of Pledge | 03/12/2019 | |||

| R G CHANDRAMOGAN | Promoter & Director | 91486578 (56.59) | Equity Shares | 62985 | 38042940.00 |

| 31/10/2019 | Market Purchase | 01/11/2019 | |||

| R G CHANDRAMOGAN | Promoter & Director | 91486467 (56.59) | Equity Shares | 111 | 66044.00 |

| 30/10/2019 | Market Purchase | 31/10/2019 | |||

| R G CHANDRAMOGAN | Promoter & Director | 91486462 (56.59) | Equity Shares | 5 | 2895.00 |

| 27/10/2019 | Market Purchase | 29/10/2019 | |||

| R G CHANDRAMOGAN | Promoter & Director | 91482867 (56.58) | Equity Shares | 725000 | 421877500.00 |

| 25/10/2019 | Creation Of Pledge | 28/10/2019 | |||

| R G CHANDRAMOGAN | Promoter & Director | 91482867 (56.58) | Equity Shares | 3595 | 2083303.00 |

| 25/10/2019 | Market Purchase | 28/10/2019 | |||

| R.G.CHANDRAMOGAN (Revised) | Promoter & Director | 91482867 (56.58) | Equity Shares | 2179030 | 1307418000.00 |

| 04/09/2019 | Pledge Released | 07/09/2019 | |||

| R.G.CHANDRAMOGAN | Promoter & Director | 91482867 (56.58) | Equity Shares | 2179030 | 1307418000.00 |

| 04/09/2019 | Pledge Released | 05/09/2019 | |||

| R.G.CHANDRAMOGAN | Promoter & Director | 91482867 (0.57) | Equity Shares | 125000 | 73100000.00 |

| 23/10/2018 | Creation Of Pledge | 24/10/2018 | |||

| R.G.CHANDRAMOGAN | Promoter and Director | 91482867 (56.58) | Equity Shares | 30000 | 18600000.00 |

| 10/10/2018 | Creation Of Pledge | 11/10/2018 | |||

| R.G.Chandramogan | Promoter & Director | 90482867 (55.96) | Equity Shares | 1398852 | 874300000.00 |

| 16/08/2018 | Creation Of Pledge | 20/08/2018 | |||

| R.G.Chandramogan | Promoter & Director | 90482867 (55.96) | Equity Shares | 1000000 | 721069980.00 |

| 17/08/2018 | Market Purchase | 20/08/2018 | |||

| R.G.CHANDRAMOGAN | Director | 84720470 (55.68) | Equity Shares | 5762397 | 2558504268.00 |

| 12/07/2018 | Allotment | 14/07/2018 | |||

| C.SATHYAN | Director | 14199130 (9.33) | Equity Shares | 997644 | 442953936.00 |

| 12/07/2018 | Allotment | 14/07/2018 |

Note-

- Regulation 7(2)- Disclosure to the Exchange by Listed company in terms of Regulation 7(2) (b) of SEBI (Prohibition of Insider Trading) Regulations, 2015.

- -(Promoter/KMP/Director /Immediate Relatives / Employee / etc )

** - (Share/Warrants /Convertible Debenture etc)

-market purchase / public rights/preferential offer / off market / inter-se transfer etc.

- Period of Allotment advice / acquisition of shares / sale of shares

~ - Number of Units = (Contracts * lot size)

Mr Chandra Mohan seems to be very generous in distributing dividends as he holds 74% of the share. He has depledged shares from Kotak and Bajaj Finance and pledged it with some Srinidhi Credit Pvt Ltd. Reasons quoted is Personal finance.

Borrowing from lesser know entity gives a sense of discomfort as to why Bajaj and Kotak are not lending…???HATSUN DIVIDEND.pdf (221.2 KB)

The pledged shares are only 5600000 i.e. 3.5%, imho it is insignificant as his holding 74% is worth appx.6000cr.

Dividend yield is around 0.80% i.e his 74% holding gets him 60cr.of dividend per annum & his interest liability is appx.30cr. only.

The ice cream industry in trouble due to lockdown.

They are facing Twin challenges

First the demand slowdown during the peak season and, second, the financial burden over the lockdown

Second As sales have come to a halt, stock inventories are piled up in cold storages. Having no sales, there is currently only financial outgo for the companies, which have obligations to pay wages, electricity bills, interest payments and other fixed expenses.

Hatsun today declared results for Q1.

Revenue down by 144 cr to 1279.3cr (-10% YoY)

Net profit jump to 56.1cr (+9.6%)

Icecream segment is one of the major component of profits especially for Q1 as it is Seasonally best quarter. It is one of the major hit segments in Q1 due to Lockdown and early mansoon. Then how come company profits increased ? Am I missing something

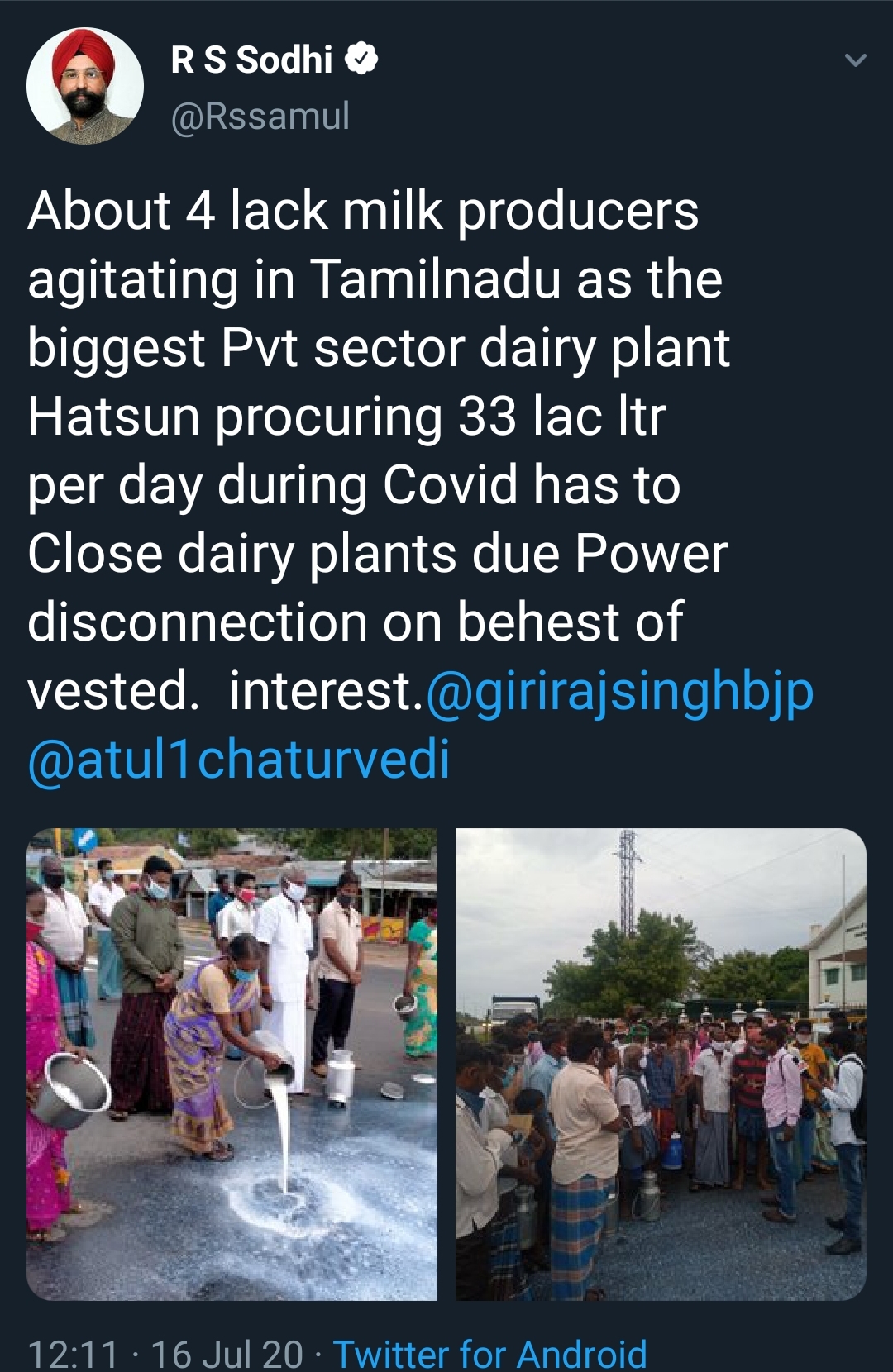

Further, there is a news that farmers are agitating on Hatsun pouring their milk on roads. There is no news coverage or exchange announcement . Any idea on present situation?

Why this company not conducting any conference calls or at least releasing Investor Presentations. As it is enjoying superior valuations compared to its peers I would at least expect yearly conference call if not quarterly.

Disclosure: No Investment

Very good article in Forbes India magazine (issue has Zerodha founders on cover) on Mr Chandramogans journey documenting his humble beginnings from starting with Rs 13000 capital raised by father from selling ancestral property which was used to set up first ice cream factory of Arun Ice Creams. In the 80s, knowing they were unable to match with larger players like HUL, they targeted college mess canteens and ships and gained sizeable market share in that segment. Next they forayed into rural TN by adopting franchisee model where most of the capex such as freezers was incurred by franchisee.

Article also gives interesting insight into use of debt by Mr Chandramogan right from early days, in fact he even calls himself glorified employee of bank once having debt to equity of 5:1.

Those having Jio sim can read the Magazine free on Jio Mags

-

Hatsun AgroProd. insider trade: Pledge of 1,870,000 equity shares worth Rs 15416.28 lacs by promoter & director

Why there are so much of pledging… -

Hatsun AgroProd. insider trade: Pledge of 600,000 equity shares worth Rs 4920.00 lacs by promoter & director

more pledging